Is it Safe to buy BP Junk Bonds?

Companies / Corporate Bonds Jul 09, 2010 - 10:53 AM GMTBy: Gary_Dorsch

For fixed income investors, who seek a steady cash inflow from bonds, either to supplement their income, or to subsidize their retirement, - these are the worst of times. The so-called “risk-free” rate of return on money market deposits, or those of FDIC insured bank CD’s in the United States are offering a razor thin 7-basis points. Worse yet, the Federal Reserve might be a year away, before it has the courage to begin lifting short-term interest rates to more “normal” levels.

For fixed income investors, who seek a steady cash inflow from bonds, either to supplement their income, or to subsidize their retirement, - these are the worst of times. The so-called “risk-free” rate of return on money market deposits, or those of FDIC insured bank CD’s in the United States are offering a razor thin 7-basis points. Worse yet, the Federal Reserve might be a year away, before it has the courage to begin lifting short-term interest rates to more “normal” levels.

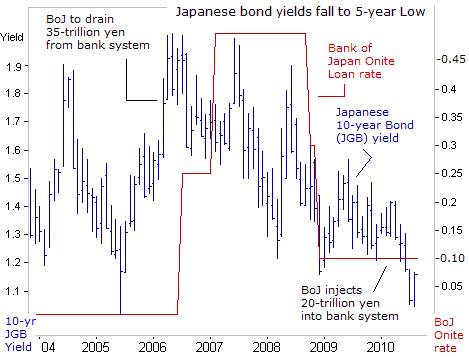

The specter of ultra-low interest rates has plagued Japanese investors for more than a decade. The Japanese experience could become the nightmare scenario for fixed income investors in other countries, if the world economy experiences a “double-dip” recession. For the past ten-years, yields on Japan’s 10-year government bond (JGB) have been locked within a narrow trading range between 1% and 2-percent. Last week, JGB yields fell to 1.07%, anticipating a deflationary spiral and a recession.

The graveyards are filled with bearish speculators, predicting the collapse of the JGB market over the past few years. Despite Japan’s rising tide of red ink, ($8.73-trillion of outstanding debt equaling 178% of GDP), the yen has been rock solid and JGB yields have been the lowest in the world for more than a decade. Yield starved Japanese investors, who own 1,440-trillion yen ($16.3-trillion) in assets, command six-times the size of China’s foreign currency reserves. As such, Japanese traders, - in search of higher yields, might be attracted to the bonds of British Petroleum, offered through dealers operating on the US over-the-counter market.

British Petroleum, commonly known as BP, is one of the oldest companies in the world, established in 1908. It’s the UK’s largest corporation, and is one of the six “super majors,” with vertically integrated businesses, including exploration for oil and natural gas, refining and marketing of petroleum products, bio-fuels, and green energy. The company is listed on the London Stock Exchange, the New York Stock Exchange, and is a heavyweight in the FTSE-100 Index. Forty percent of BP’s shareholders are in the United States, and the same percentage based in Britain.

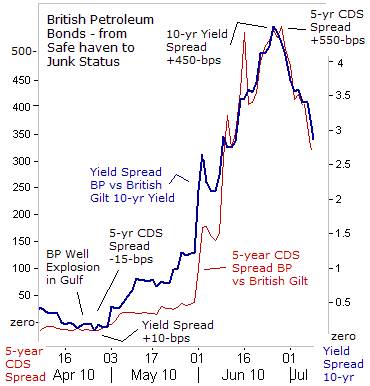

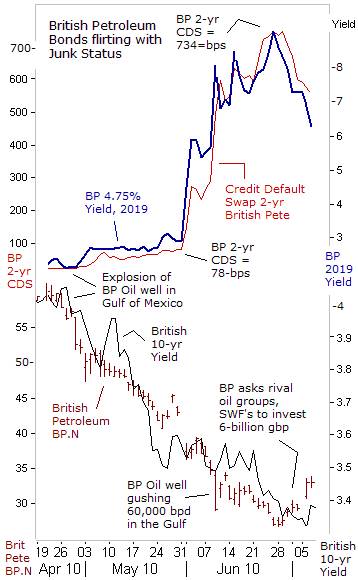

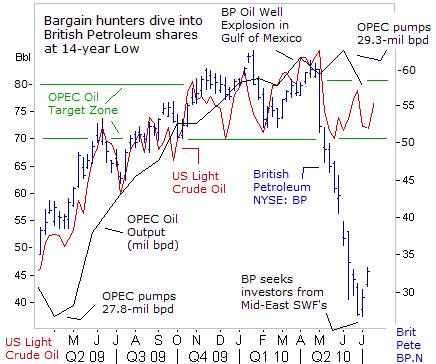

BP’s bond yields have ratcheted sharply higher in recent weeks, to levels that are normally associated with BB rated junk bonds. It’s a shocking event, since BP’s bonds were considered to be safer than British Gilts. Prior to the April 20th explosion of BP’s oil well in the Gulf of Mexico, its balance sheet was in great shape, with a debt-to-equity ratio of only 16%, a level so low, the oil company giant could’ve easily borrowed $15-billion without denting its previous AA+ rating.

Prior to April 20th, credit default swaps (CDS), measuring the cost of insuring $10-million of BP’s debt against the possibility of default cost $15,000 less than the cost of insuring British gilts. Three months ago, the yields on BP’s benchmark 4.75% note, due in 2019, were equal to those offered by the British Treasury, - and was managing its finances, better than the British Exchequer’s.

Of course, the world has turned upside down for BP and its bond and shareholders since April 20th, with 60,000 barrels a day of crude oil gushing from the Deepwater Horizon oilfield, situated in the Gulf of Mexico. The worst environmental disaster in world history, - shutting down rich fishing grounds, killing hundreds of turtles and seabirds, and dolphins and soiled the coastlines of four US states, has unleashed a gusher of litigation against BP, that will cost the oil giant tens of billions of dollars. More than two million barrels of oil have been released into the Gulf of Mexico.

Last week, the cost of insuring $10-million of BP bonds against default was $550,000 more than comparable British gilts. The yield spread on BP’s 10-year note rose to +450-basis points above British gilts, after Fitch downgraded its credit rating by six notches to BBB. Under heavy political pressure, BP has agreed to suspend its dividend for three quarters, equaling about $7.5-billion, and will deposit $20-billion into an escrow fund to pay for damages to oil spill victims.

On June 25th, BP’s American Depository shares in New York hit a 14-year low at $27, slicing $105-billion off its market value, since the April 20th explosion in the Gulf. Its credit weakened sharply as clean-up and compensation costs for the ecological disaster escalated. BP Capital’s 4.75% note, due in 2019, saw it yield soar to as high as 8.75%, up from 2.75% just two-months earlier. While BP’s yields were soaring into junk status territory, British 10-year gilt yields were sliding 75-basis points lower to 3.35%, tumbling in tandem with BP’s share price. Bonds listed under Atlantic Richfield, which is owned by BP, offer 1% more in yield than the parent’s bonds, since traders are less certain the BP would honor its debts for Arco holders.

BP’s oil spill in the Gulf of Mexico is also an oil gusher for litigation lawyers. Litigation could last for 20-years, and the cost and negative publicity has badly crippled Britain’s largest company. Nowadays, guessing the ultimate liability that lies ahead for BP is what investing in its bonds and stocks is all about. Analysts figure that cleanup and legal costs could range from as low as $27-billion, to as high as $63-billion. BP also faces an onslaught of litigation with investors, businesses, and municipalities, and even criminal penalties are also possible.

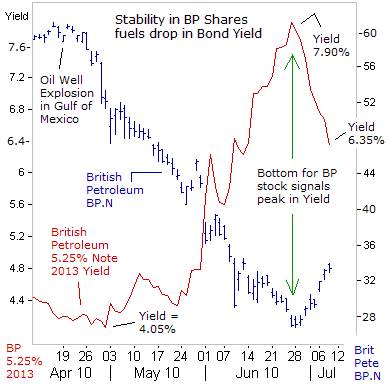

The yield on BP’s shorter-term 5.25% note, due in 2013, briefly spiked to as high as 7.90%, on June 25th, at the same time its ADR share price skidded to a 14-year low of $26.75 in New York. Subsequently, the yield has dropped to around 6.35% today. The drop in BP’s bond yield coincided with a rebound in BP’s share price, to as high as $33.20 today. The rebound in BP’s share price restored $19-billion of market capitalization, heartening investors in BP junk bonds.

BP is a giant colossus, generating $265-billion in revenue last year, and $30-billion of operating cash flow. It ended March with $105-billion of assets net of liabilities, - a large capacity to withstand tens of billions of spill costs. Already, as many as nine European banks have offered standby credit lines totaling $14-billion for BP. It also has $7-billion in cash, will pocket $7.5-billion by cancelling three quarterly dividends. BP plans to trim $2-billion from its capital expenditure this year.

BP’s boss Tony Hayward is courting sovereign wealth funds in the Middle East, including in Abu Dhabi, Kuwait, Qatar, Saudi Arabia, and Singapore, to buy significant stakes in the company. The al-Eqtisadiyah newspaper said a delegation of Saudi investors is heading to London for direct talks with BP, to discuss buying a stake worth 10 to 15% in the British oil company. BP could also launch a rights offering to its existing shareholders to raise additional capital.

BP could also sell about $10-billion worth of strategic assets, to pay for the oil spill damages. China National Offshore Oil Corporation (CNOOC) is understood to have expressed an interest in buying the 60% stake held by BP in Pan American Energy, Argentina’s fastest-growing oil and gas group, worth $9-billion (£6bn). The Kremlin has also made no secret of its desire to see Russian oil companies buying assets from the beleaguered company in other parts of the world.

In other words, BP is probably big and strong enough to sustain $50-billion in legal bills, and clean-up costs, and still survive in decent shape. However, if the 11 deaths caused by the BP explosion results in criminal liability, BP’s costs could spiral above $50-billion. Much would also hinge on BP’s ability to convince a jury, to shift part of the blame for the disaster to its partners, - Anadarko Petroleum (APC), and Mitsui. BP has a 65% stake in the oil well, while APC controls 25% and Mitsui 10-percent.

About 450,000-million bpd or 12% of BP’s oil output comes from the Gulf of Mexico. The largest-single producing field in the Gulf is BP’s Thunder Horse joint venture with Exxon-Mobil, with 25 subsea wells. So it’s important to note that the Deepwater Horizon oilfield only represents a sliver of BP’s total proven reserves of 18.3-billion barrels worldwide. BP’s ongoing revenues haven’t been materially impacted so far. Also working in BP’s favor is the belief that the company’s efforts to contain the oil spill would be successful by the end of July.

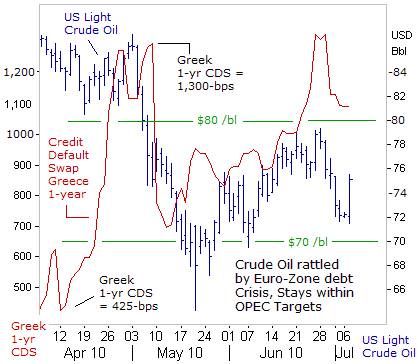

Oil prices are holding steady, gyrating within OPEC’s targeted trading range of $70-to-$80 /barrel, despite worrisome signals that the world economy is poised to slip backwards into a “double-dip’ recession. Thus, there is a measure of inelastic demand for crude oil, that’s resistant to downturns in the global economy. “Right now we are seeing strong growth in the emerging world and a sluggish response from advanced countries,” said OPEC chief Abdullah al-Badri.

The OPEC cartel and Iraq have boosted their combined oil output by 1.5-million bpd since April 2009, offsetting growing demand from China, and slumping oil output from Mexico’s Cantrell oilfield. Still, on June 27th, al-Badri called on OPEC members to lower their output and adhere to their production targets, having slipped from 80% compliance when crude oil was below $50 /barrel, to around 53% today. “When you look at the inventory overhang and floating storage, about 244-million barrels, there is a lot of oversupply. We need more discipline,” he warned.

The price of crude oil is a key risk variable for any investor in bonds or shares of oil companies. If crude oil prices were to tumble far below OPEC’s lower target at $70 /barrel, due to mounting signs of a “double-dip” global recession, it would shrink BP’s cash inflows, making investing in its bonds even riskier. Same goes for investing in bonds issued by Canada’s largest oil company, Suncor – Petro-Canada, whose cost of production from the tar sands region is about $34 /barrel.

Oil’s $20 /barrel plunge from May 5th to May 20th, was sparked by an upward explosion in Greece’s credit default swaps, underscoring the volatility of the crude oil market, which is still heavily populated by speculators. The OPEC cartel responded to the sharp drop in crude oil, by cutting its combined output by 200,000-bpd, to 29.1-million bpd, to help buoy oil prices. Since then, crude oil has rebounded into OPEC’s targeted range, requiring only modest tweaking of supply.

Chinese demand is a key driver for crude oil prices. China’s oil imports are expected to grow 5% this year from 2009, and the proportion of its imported oil compared with total consumption is expected to reach 54% this year. However, Yang Guozhong, a senior official at the People’s Bank of China, warned of a slowdown in the Chinese economy in the second half of the year, and said the central bank would continue to soak-up excess liquidity, with tools such as bank reserve requirements and open market operations, at an appropriate time,” he warned.

Tension in the Persian Gulf could also ratchet higher in the months ahead, after US President Barack Obama signed into law on July 1st, Congressional legislation against Iran that broadly targets foreign banks and corporations doing business in Iran and sets out unilateral US penalties against those that do not fall into line. Companies could be denied access to the US Export-Import Bank, restricting their ability to sell into the US market, or denied US government contracts.

Last week the French oil company Total ended sales of gasoline to Iran and Spain’s Repsol pulled out of a development contract with Royal Dutch Shell for Iran’s South Pars gas field. Russia’s LUKOIL, India’s Reliance Industries, Malaysia’s Petronas, Royal Dutch Shell and the Swiss firm Glencore have also halted gasoline sales to Iran, which has the potential to bring Iran’s economy to its knees. A gasoline boycott of Iran might be regarded by Tehran as an act of war, and could ignite an explosive military outbreak in the Persian Gulf, lifting crude oil sharply higher.

Is it safe to buy BP’s Junk Bonds? It’s probably safe to say, that the June 25th peak in BP bond yields, has fully discounted the negative scenario of $30-billion in legal expenses and clean-up costs. Although a grey cloud should cast its shadow over BP for the next few years, reminiscent of the shadows of fear over the tobacco companies, legal precedent suggests that BP’s ultimate payout might be less than $30-billion, and therefore, - leaning bullish for BP bond prices.

The Valdez disaster in 1989, which caused roughly 257,000 barrels to spill off the Alaska coast, offers a glimpse into what is expected to be a grueling and extremely costly legal battle for BP. Litigation dragged on for two decades as Exxon Mobil Corp fought punitive damages, saying the $5-billion that an Alaska jury awarded in 1994 was excessive. A federal appeals court later cut that to $2.5-billion, and in 2008 the US Supreme Court slashed it to $507-million.

If Middle Eastern wealth funds are willing to take a 15% stake in BP, the odds of its survival go up considerably. There’s also the perception that the British government, would view its flagship oil company, as “too-big-to-fail,” and some type of rescue operation would be engineered by Downing Street. Any signs of stability or recovery in BP’s share price would signal to traders that BP’s “junk” bonds, are safe to buy.

Investing in bonds entails a lot less risk than stocks. There is lots of room for error for the bondholder, since a company’s share price could fall significantly in value, without impairing the company’s ability to service its debts. It would only become alarming for bondholders, if BP’s share price fell too low for comfort, say below $10 /share and moving into single digits. For now, BP’s short-term 5.25% note, due July 2013, is yielding 6.35% - a hefty spread of 575-basis points above Treasuries.

This article is just the Tip of the Iceberg of what’s available in the Global Money Trends newsletter. Subscribe to the Global Money Trends newsletter, for insightful analysis and predictions of (1) top stock markets around the world, (2) Commodities such as crude oil, copper, gold, silver, and grains, (3) Foreign currencies (4) Libor interest rates and global bond markets (5) Central banker "Jawboning" and Intervention techniques that move markets.

By Gary Dorsch,

Editor, Global Money Trends newsletter

http://www.sirchartsalot.com

GMT filters important news and information into (1) bullet-point, easy to understand analysis, (2) featuring "Inter-Market Technical Analysis" that visually displays the dynamic inter-relationships between foreign currencies, commodities, interest rates and the stock markets from a dozen key countries around the world. Also included are (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, with the latest news on global markets, and view our updated model portfolio 2008. To order a subscription to Global Money Trends, click on the hyperlink below, http://www.sirchartsalot.com/newsletters.php or call toll free to order, Sunday thru Thursday, 8 am to 9 pm EST, and on Friday 8 am to 5 pm, at 866-553-1007. Outside the call 561-367-1007.

Mr Dorsch worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group.

As a transactional broker for Charles Schwab's Global Investment Services department, Mr Dorsch handled thousands of customer trades in 45 stock exchanges around the world, including Australia, Canada, Japan, Hong Kong, the Euro zone, London, Toronto, South Africa, Mexico, and New Zealand, and Canadian oil trusts, ADR's and Exchange Traded Funds.

He wrote a weekly newsletter from 2000 thru September 2005 called, "Foreign Currency Trends" for Charles Schwab's Global Investment department, featuring inter-market technical analysis, to understand the dynamic inter-relationships between the foreign exchange, global bond and stock markets, and key industrial commodities.

Copyright © 2005-2010 SirChartsAlot, Inc. All rights reserved.

Disclaimer: SirChartsAlot.com's analysis and insights are based upon data gathered by it from various sources believed to be reliable, complete and accurate. However, no guarantee is made by SirChartsAlot.com as to the reliability, completeness and accuracy of the data so analyzed. SirChartsAlot.com is in the business of gathering information, analyzing it and disseminating the analysis for informational and educational purposes only. SirChartsAlot.com attempts to analyze trends, not make recommendations. All statements and expressions are the opinion of SirChartsAlot.com and are not meant to be investment advice or solicitation or recommendation to establish market positions. Our opinions are subject to change without notice. SirChartsAlot.com strongly advises readers to conduct thorough research relevant to decisions and verify facts from various independent sources.

Gary Dorsch Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.