Inflation is No Miracle Cure, Impossible to Inflation Out of this Mess

Economics / Inflation Apr 25, 2011 - 03:24 AM GMTBy: Mike_Shedlock

Inquiring minds are reading The "Miracle" of Compound Inflation by John Mauldin. Here are a few paragraphs worthy of a closer look.

Inquiring minds are reading The "Miracle" of Compound Inflation by John Mauldin. Here are a few paragraphs worthy of a closer look.

Albert Einstein is famously quoted as saying, "Compound interest is the eighth wonder of the world." And compounding is indeed the topic of this week's shorter than usual letter, but compounding not of interest but of inflation.

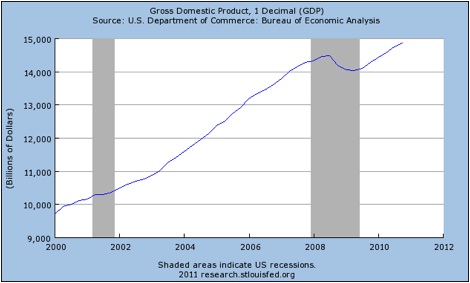

First, let's look at nominal GDP over the last 11 years, from the beginning of 2000. The data only goes through the third quarter of last year, so sometime this year it is quite likely that GDP will top $15 trillion.

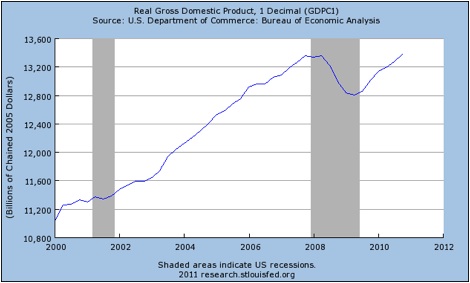

Now, to see this in an interesting graph, the Fed has real GDP based on 2005 dollars. You can see that we are about back to where we were in 2008, prior to the crisis, and growing well below trend. But if we adjust for inflation, growth has not been close to what it was in nominal terms.

Now let's run through a few "what-if" scenarios.

What if the next 11 years look more or less like the last, with 4% nominal GDP growth? That would mean that in 2022 nominal GDP would be 50% larger than now, right at $22.5 trillion. But that is with only 2% inflation.

What if inflation were 4%, with the same growth? Then nominal GDP would be $30 trillion! What a roaring economy, except that gas would $8 a gallon (assuming current levels of supply and demand). In essence, you would need $2 to buy what $1 buys today. Don't even ask about health-care costs. If your pay/income did not double, you would be in much worse shape in terms of lifestyle. That is the insidious nature of inflation.

But let's think about that from a federal budget perspective. Let's assume we get 20% of GDP in federal tax revenues, which is roughly a little higher than the historical average. That means total tax revenues would be in the range of $6 trillion. With 2% inflation, revenues would be just $4.5 trillion. If the federal government froze its spending at current levels for 12 years (no inflation adjustment), we would be running large surpluses under either scenario.

Higher inflation means US debt is easier to pay back, as nominal GDP is what we pay taxes on, not inflation-adjusted. Inflation is a tried and true method of dealing with too much debt. Inflation is also just another word for default, but it sounds so much better to the ear.

Whoa!

- What about interest on the national debt?

- What if we have inflation without the growth?

- What about wage growth and revenue assumptions?

- What about health-care costs and other government expenditures?

Mauldin is correct about the "insidious nature of inflation" yet provides an example that suggests inflation is the government's best friend. Let's quickly dispel such thinking starting with a look at interest on the national debt and health-care costs.

Health-Care Costs

Mauldin said "Don't even ask about health-care costs." Well we have to ask about them. If health-care costs rise sharply, so will Medicare and Medicaid expenses unless they are capped.

Mauldin proposed such a cap to make his "what-if" model work.

Unfortunately, it is not rational to assume such a cap, nor is it rational to think other government expenses such as road-work, food stamps, education spending would be capped either.

Interest on the National Debt

Speaking of caps, there is no way to cap interest on the national debt except by eliminating the debt entirely.

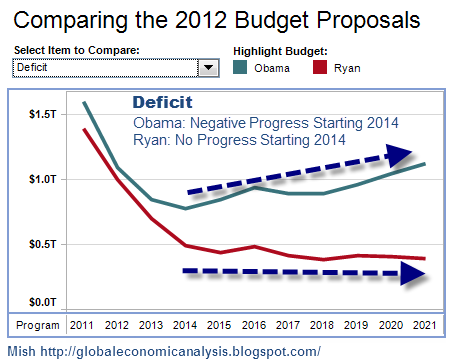

I discussed interest on the national debt in Interactive Map: Paul Ryan vs. Obama Budget Details; Path of Destruction

Here are the pertinent charts but please take a look at the entire post if you have not seen it.

Deficit: Obama vs. Paul Ryan

Paul Ryan made good headway for three years, then fell flat for another 7. This is no way to shrink the national debt or reduce interest on the national debt as we shall see in a moment.

Obama's proposal is abysmal. He made some progress for a few years, then went into reverse.

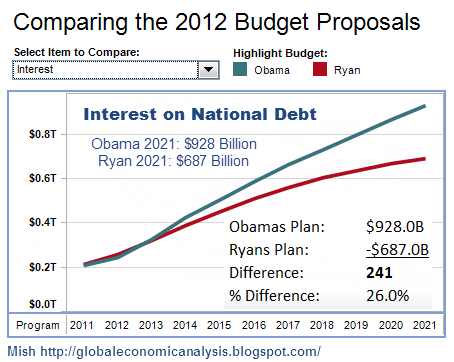

Interest on the National Debt: Obama vs. Paul Ryan

The above chart shows the effect of cumulative failures to shrink the deficit.

Note that in 2021 president Obama proposes to spend over $900 billion a year on interest on the national debt. This is sickening, not amusing.

Paul Ryan would have us spending $687 billion on interest in 2021. His deficit proposal for 2021 is $731 billion.

CBO Analysis

Mauldin continues, and gets back on much firmer ground with a critique of CBO analysis.

What the CBO Assumes

The Congressional Budget Office makes projections, based on various Congressional tax bills, as to what future income and expenses might be. But to do that they have to make assumptions about the growth of the economy and inflation.

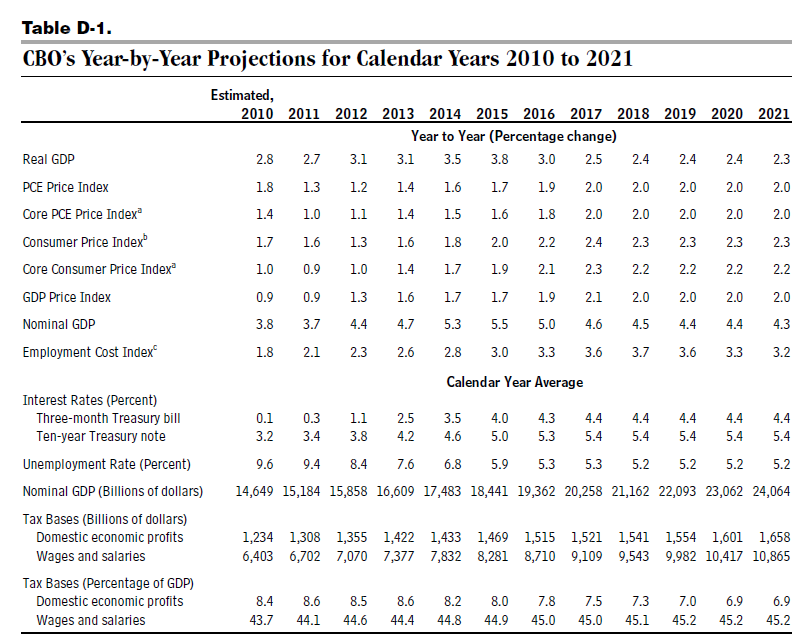

You can go to their website and see their economic forecasting. The data I will be discussing is on page 7, in http://www.cbo.gov/ftpdocs/120xx/doc12039/EconomicTables%5B1%5D.pdf.

Let's look at one of the tables. Note that they have nominal GDP at $24 trillion in ten years (not far from my 2% inflation scenario above), but they assume rather robust economic growth for the next five years (beginning with 2012) of well over 3% and inflation down around 1.5%. Not a bad world if we could get it.

Let's look at one of the tables. Note that they have nominal GDP at $24 trillion in ten years (not far from my 2% inflation scenario above), but they assume rather robust economic growth for the next five years (beginning with 2012) of well over 3% and inflation down around 1.5%. Not a bad world if we could get it.

What Happens at "Modest" 4% Inflation?

Now that we have interest rate and inflation assumptions from the CBO, let's take another look at what might happen with 4% inflation.

The CBO projects the CPI will peak at 2.3% except for 2017 at 2.4% (quite an assumption). The CBO also projects short-term interest rates to be about 2 points higher than CPI, and 10-year rates at 3 points higher than the CPI.

Using those guidelines, at 4% inflation, short-term interest rates would be 6%, and 10-year rates would be 7%.

National debt will rise to $23-26$ trillion in the Obama -Ryan scenarios shown above. At 4% inflation (and 6% interest rates) what would interest on the national debt be?

At 6% interest, interest on $26 trillion would be $1.56 Trillion a year. However, that statement assumes we got to 2021 and then interest suddenly spiked to 6% and all the revenue assumptions held up. It would not work that way in practice.

Remember that we are running budget deficits and adding to the national debt under every scenario proposed so far. If we had 4% inflation along the way, interest on the national debt would rise sharply every year and that amount would add to the cumulative debt, as would any revenue misses.

If we had 4% inflation, would we have the revenue growth as presumed in Mauldin's "what-if" example? I highly doubt it. However, we can be sure that government expenditures would rise.

Also note that even IF revenues rose with inflation, so would government expenditures on health-care, road work, education, food stamps, etc unless one makes irrational assumptions.

Thus any scenario that suggests a budget surplus is possible with 4% inflation is preposterous.

What About Another Recession?

Finally, and as Mauldin correctly pointed out, the chance of a recession in the next 10 years is quite high.

Indeed, I think it is likely there are two or more recessions in the next decade. Thus, the CBO estimate, Ryan's estimate, and president Obama's estimate are all unrealistically optimistic.

Locking in Long-Term Rates

Ironically, the Fed could take advantage of low interest rates now by locking in favorable long-term rates now just as corporations have done.

Instead of buying treasuries and bloating its balance sheet, in theory, the Fed could have been selling treasuries, locking in debt at exceptional prices under 4.5% for 30 years, or 10-year debt at 3.4% (and could have done much better some time ago).

I said, "in theory" because that action would have reduced money supply, and Bernanke believes tightening money supply in the Great Depression made matters worse.

Exit Strategy Will Put Upward Pressure On Yields

Today the Fed has a different problem of its own making.

The Fed's balance sheet is stuffed with treasuries. Attempts to unload them would put upward pressure on yields regardless of what Bernanke says about his exit strategy (or lack thereof).

Impossible to Inflate Out of This MessThe idea that inflation is a "tried and true method" of dealing with debt is complete Keynesian foolishness. Inflation is never a cure, it only seems to work in the short run.

Please consider these Statements of Ludwig von Mises regarding Interest, Credit Expansion, and the Trade Cycle.

There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.Tried and True Illusion

Careful analysis including a look at interest on the national debt and other government expenditures shows there are no "miracle" cures from inflation, only a temporary illusion of success, much like the illusion that the housing bubble represented a solution to the collapse of the dot-com bubble.

Inflation it is the disease. Deflation is the cure, but it sure will not be painless.

In the meantime, the Monetarist clowns at the Fed and the Keynesian clowns in government are simply digging a bigger hole, cheering the illusion of success of ever-bigger bubbles.

The collapse of the housing bubble should be proof enough that the model does not work, yet Keynesian clowns everywhere persist with proposals that have never worked in practice, and cannot possibly work mathematically.

Addendum - A Long One:

Who Does Inflation Benefit?

One misguided soul commented that I ignored the fact that inflation benefits those with first access to money.

Hardly.

A search of my blog for inflation benefits access turns up hundreds of hits of which at least 20 use those three words in a single sentence.

Moreover, some of the posts were entirely devoted to that theme. For example please consider Hello Ben Bernanke, Meet "Stephanie" a post containing an email from a retired person living on social security complaining about the ravages of inflation. Please read it. Here is on key snip.

Fed's Policy Is Theft

Stephanie, it's a little known fact that inflation benefits those with first access to money, such as the banks, the wealthy (via rising asset prices), and the government (think rising sales taxes and property taxes when prices go up).

Everyone else gets screwed. You are right in the middle of the pack of those most hurt by the serial bubble blowing policies of the Fed.

Viewed this way, Bernanke's policies are nothing but theft, robbing the poor, for the benefit of banks and the wealthy.

This is why I support Congressman Ron Paul's effort to end the Fed.

Systemic Theft

Inflation most benefits banks not only because they have first access to money, but also because government and the Fed will bail them out if they get in trouble. The insidious result is the moral hazard policy known as "too big to fail".

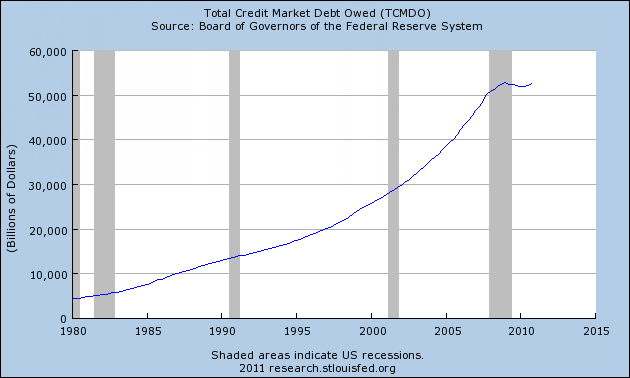

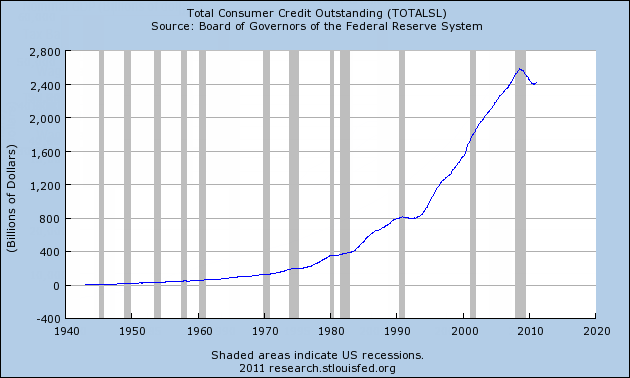

However, that does not negate the possibility of deflationary busts as the following chart shows.

Total Credit Market

Total Consumer Credit

The proper way of viewing inflation is via expansion and contraction of credit. The first chart shows that credit dwarfs money supply, regardless of what your measure of money is.

We have never before in history seen a credit bust of this magnitude, yet there is no good reason to think another bust cannot happen.

Indeed we just went through a deflationary bust, and there will be more, just as happened in Japan. All the current focus on prices is simply misguided. The fact that gasoline prices have soared pales in comparison to $trillions in debt wiped off the books in the housing bust. That is not conjecture subject to debate, but a simple logical fact, yet people tell me all the time we have inflation as measured by the price of eggs or gasoline or whatever.

Phooey, we have inflation now and have been in a state of inflation since Bernanke revived the corporate bond market in Spring of 2009. When the corporate bond market heads down again, the economy will once again feel the effects of deflation.

Inflation and Deflation Defined

My model defines inflation as a net expansion of money and credit with credit marked-to-market. Deflation is a net contraction of money and credit with credit marked-to-market.

The marked-to-market concept takes the market perception of credit into the picture. Debt that cannot be paid back won't, but if the market lets banks pretend that it will, the system still functions. Such is the state of affairs right now.

Hyperinflation Ends The Game

There are numerous misguided proponents of hyperinflation. Most do not understand that hyperinflation is a political event (the complete loss of faith in currency), not a measure if interest rates or price inflation.

A political event happens first (complete loss of faith of currency), and hyperinflation is the result. For a discussion please see Debating the Flat Earth Society about Hyperinflation

For a discussion about the nature of money and how much is needed, please see

Gold is Money, What About Silver? Can Gold be Debt?

The key issue regarding hyperinflation is that it is a political event and that it would destroy the banks and the Fed if it happened. In tat sense it benefits no one. The Fed would not want it to happen, nor would banks and the wealthy.

That does not make hyperinflation impossible, but given the political stability of the US, it sure makes it damn unlikely.

Hyperinflation Theory vs. Practice

This is what it comes down to: In theory, Congress can easily cause hyperinflation. In practice, they won't, and neither will the Fed. As Yogi Berra once quipped "In theory there is no difference between theory and practice. In practice, there is."

Does Government Benefit From Inflation?

Earlier I stated how government benefits from inflation (higher tax collections was one of the ways).

However, unlike banks and the wealthy who can and do invest money in assets, government squanders money.

Sure, government may collect more in taxes than before, but governments everywhere perpetually spend more than they take in. In practice, interest on the national debt and rising expenditures more than chew up any alleged "benefit" of inflation.

Thus it is an illusion that government benefits from inflation (depending of course on your definition of "government").

However, politicians prey on the illusion of benefit and also on the public's demand for government to "do something". In that sense, corrupt and ignorant politicians do benefit from inflation.

Summation

Hyperinflation ends the game and is unlikely.

Periodic bouts of deflation in conjunction with longer periods of inflation serves to concentrate wealth in the hands of bankers and other wealthy individuals.

In general, there are No "Miracle" Cures from Inflation. Rather, inflation slowly destroys the middle class over time for the benefit of banks and the wealthy who were not so foolish as to be over-leveraged in debt.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2011 Mike Shedlock, All Rights Reserved.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Comments

|

Nadeem_Walayat

25 Apr 11, 08:52 |

Deflation Mantra ending ?

Another one that is coming to the realisation that he has been wrong with his deflation mantra for several years. Much of the above was covered at greater depth in the Inflation Mega-Trend Ebook (Jan 2010) - Free Download |

|

Ernie Messerschmidt

25 Apr 11, 12:27 |

banks don't squander?

Intriguing and pretty convincing, Mish – inflation is no cure-all. But this statement of yours, “However, unlike banks and the wealthy who can and do invest money in assets, government squanders money” seems downright stupid to me. Bankers and the wealthy spend money responsibly, but government doesn’t? Hogwash. The Fed is privately owned; that’s fact. It piled trillions that it created out of thin air onto banks, which the banks invest anywhere other than in the U.S. economy, about which they don’t give a shit. I call that squandered money. The banks and hyper-wealthy create nothing of value; they are just parasites on the real economy. |

|

TOM SAWYER

26 Apr 11, 20:56 |

WARS

Do you ever ask yourself why is there always enough money to spend knocking down buildings and infrastructure and then enough money left over to rebuild them in some far off land? Why not encourage business to raise wages which would have prevented the present disaster we are in. We have dumbed down wages and benefits so that the wealthiest and fewest among us control that vast amount of total wealth. This country was at its peak when the workforce was highly unionized and markets were protected. Why not ask all those free traders how their dream looks today. Lets abandon free trade and embrace free trade. Lets take back a percentage of markets that we have given away . If corporations want to leave let them and don't let them back in with their products . We don't need them because if there is a market for the product someone will rise to replace them. |

|

James

28 Apr 11, 09:49 |

USA Issues

The USA needs to restrict immigration to blue collar workers. These were the immigrants that built the States, not the overeducated, pencil pushing spongers that are now coming on H visas. To many of our jobs have either been off shored or are being taken over by Asian companies that import workers on H visas. They pay these workers less, have the threat of losing their visas hanging over worker heads and the workers rarely are up to the standard of native Americans. Companies have little sense of corporate responsibility and have effectively screwed over the workers. The people taking the jobs dont care a jot for USA culture, only that they dont have to build an infrastructure. If they could do this, they would fix their own countries instead of riding on the backs of previous hard working immigrants. |