US Bailout of Bond Insurers to Prevent Collapse of US Banking System

Stock-Markets / Financial Crash Dec 20, 2007 - 04:39 PM GMTBy: Jim_Willie_CB

The hidden bond insurers used by Wall Street firms are in the news, especially ACA Capital and MBIA. Implications are huge, with monumental ripple effects. Financial press reporting of the bond insurers is woefully inadequate. Moodys and Fitch are giving analysis review to nine ‘AAA' rated bond insurers to see if they have sufficient capital to conduct their insurance operations. The list includes ACA Capital, MBIA, Ambac Financial, and Financial Guaranty Insurance. ACA Capital has only $1.1 billion in cash for payout of bond failure claims, but has lost $1 billion in the most recent quarter. More losses are assured. This insurer is very important, since it is widely abused by Wall Street banks to hide cratered bond derivative losses.

The hidden bond insurers used by Wall Street firms are in the news, especially ACA Capital and MBIA. Implications are huge, with monumental ripple effects. Financial press reporting of the bond insurers is woefully inadequate. Moodys and Fitch are giving analysis review to nine ‘AAA' rated bond insurers to see if they have sufficient capital to conduct their insurance operations. The list includes ACA Capital, MBIA, Ambac Financial, and Financial Guaranty Insurance. ACA Capital has only $1.1 billion in cash for payout of bond failure claims, but has lost $1 billion in the most recent quarter. More losses are assured. This insurer is very important, since it is widely abused by Wall Street banks to hide cratered bond derivative losses.

If ACA insures a bond, then Goldman Sachs or Merrill Lynch for instance can take the under-water bond off the balance sheet. They can do so under fast changing rules, since any potential loss is not perceived to affect the firms themselves. ACA is widely called the ‘garbage can' for Wall Street, where tremendous losses are concealed from stock investors, corporate bond investors, debt rating agencies, and bank regulators. But the Financial Accounting Standards Board (FASB) is changing against the firms, forcing firms to bring losing assets onto their balance sheets in droves. Several Wall Street firms own sizeable stakes in ACA, a ploy that enables them to hide gigantic losses in blatant collusion. Bear Stearns is the fifth largest US securities firm. They own a 39% stake in ACA Capital.

Once again, leveraged mortgage bonds and mortgage-based Collateralized Debt Obligations (CDO) bonds are the root cause of the problem. Losses are amplified with the CDO packages of credit derivatives. My expectation is that mortgage bond losses will be an order of magnitude larger in 2008 than 2007, as prime adjustable mortgages face their nightmare, next on the debacle docket. JPMorgan bank analyst Andy Wessel claims if ACA defaults, banks would be forced to bring their ACA-guaranteed CDO bonds onto their books. Wessel says, “ACA is a likely candidate to get thrown to the wolves first.”

If ACA loses ‘AAA' rating, then possibly $60 billion in CDO bonds will be forced onto bank balance sheets in the banking sector generally. For instance, an ACA default would force Merrill Lynch to declare a $3 billion writedown of its CDO bonds. Expect this type of story to continue endlessly. Yesterday Morgan Stanley announced an additional $5.7 billion in bond writedown losses, making their recent total a robust $9.4 billion. Expect that their ultimate total will be three to five times larger. Bear Stearns is engaged in a parade of announced losses, each touted as the climax. Their latest made Thursday was for another $.19 billion. In my book, the entire gaggle of corrupted Wall Street broker dealers is insolvent, defending against bankruptcy with accounting shenanigans, all with the USGovt and Dept Treasury blessing.

MBIA faces similar threats, as a bond insurer. They have faced a likely downgrade by Moodys for weeks, sure to put in grave doubt the status of $652 billion of structured finance bonds, as well as state and municipal bonds that they insure. The world's largest bond insurer, MBIA beat the market to the punch in surprising admission of having $8.1 billion in CDO bond exposure. They also opened the door to discussion of ‘CDO Squared' derivatives, which are leveraged instruments built recklessly atop other leveraged mortgage bonds securities. Expect the MBIA actual losses will ultimately be three to five times larger. MBIA, ACA Capital, and six other bond insurers sweat bullets over debt rating agency downgrades. A loss of their top rating would cast serious doubt on $2400 billion in asset backed debt securities collectively.

Given the size of their total insured bond portfolios, Bloomberg Data estimates the downgrades could result in $200 billion in bond losses and bank writedowns. The rating agencies consider the bond insurers as a group to be holding far too little capital for to justify ‘AAA' ratings as corporate entities. Remember, the entire US bank/bond risk management model is dissolving before your eyes!!!

Finally on Wednesday this week, the bomb hit. Debt rating agency Standard & Poor lowered the ratings on Ambac and MBIA to NEGATIVE. S&P lowered ACA Capital was lowered to CCC grade, suggesting strong potential of actual default. The ripple effects to the bank/bond system will reverberate for weeks, if not months. In fact, my expectation is that successive ripples in 2008 will be larger than all previous. The ACA Capital ratings cut will lead to massive writedowns at Merrill Lynch and the Canadian Imperial Bank of Commerce (CIBC).

The Toronto-based CIBC announced it will probably take a $3.5 billion loss from bond writedowns. Ironically, and surely mindlessly, Merrill Lynch and Bear Stearns are working to organize several major banks to bail out ACA. The giants are toppling. The exercise is mindless since whatever new capital is infused to ACA will melt in a matter of two to three months. They are trying to buy time, to hope for a recovery, a mirage in the desert. They are dying in public view, but with a very opaque lens trained on their balance sheets.

The group of bond insurers combine to insure over 80,000 bonds and related securities. The insurers wrote contracts on almost $100 billion in risky CDO bonds backed by subprime mortgages as of mid-June, according to Fitch. The disaster that befalls ACA Capital will serve as the first true tough test of credit default swaps, those insurance contracts for corporate bonds and mortgage bonds. In June, the value of bonds linked to credit default swaps rose to a staggering $42.6 trillion, up from only $6.4 trillion at yearend 2004. These figures are supplied by the Bank for International Settlements in Switzerland . A melt-up precedes a melt-down.

My contention is that the entire US financial engineering contraption is being dissolved, a crumbling pile of wreckage, with evidence of fraud throughout the structure. It is an historically unprecedented failure in innovation, a reckless extension to develop the inflation-based system. Such a system is destined for the scrap heap though, since every bubble in history suffered a contraction, this one no different, only bigger. The threat to the entire banking system has never been this great since the Great Depression.

When comparison after comparison is made to magnitudes of this or fact factor never being so great since the Great Depression, one must raise the possibility that conditions are indeed similar and approaching such an outcome, but with central bank reactions assured. The Euro Central Bank infusion of $500 billion is such a powerful reaction, enough to soil the boxer shorts of any Deflation Theorist. My contention is that the inflation forces will ramp up considerably, in offset to the deflation forces building momentum, enough to create massive scheiss storms. The lightning, high winds, and resulting destruction will be enormous. Opportunity abounds.

Details are provided on the banking debacle, with many specifics on the asset backed bond problems, in the December Hat Trick Letter reports. The January report upcoming will surely continue the sad saga. It is honestly very difficult to provide complete reporting on a mushrooming national catastrophe. As an editor, one must pick & choose what is important.

BANK/BOND TARGETED BAILOUT

My expectation is that the USGovt will ultimately step in to offer a gigantic bailout to the bond insurers, the current focal point of destruction. The threat to the USDollar will then be known globally, from bank system collapse coupled with broad bond system insolvency. One might expect that some bond insurers will go bankrupt themselves. Imagine what your commercial building is worth if its insurance lapses.

THE FIRST GIGANTIC RESCUE GESTURE IS NOT THE MORTGAGE FREEZE, BUT RATHER WILL BE THE USGOVT BAILOUT OF THE ASSET BACKED BOND INSURERS . Why? Because they serve as the operator of the dike main valve toward a flood of liquidations, the focal point of destruction. The impact on the reputations of the US banking system, the integrity of the US financial sector, the confidence in the US Federal Reserve, and of the viability of the USDollar by implication will surely suffer. If the USGovt fails to bail out the bond insurers, expect a monumental flood of well north of $300 billion in bond losses, extending to the municipals. Communities will not be able to continue, and will announce layoffs. It will not just be a California story. The most tragic, but absurd, yet hilarious, observation is that the investment community has yet to conclude that the US bank/bond system is officially bankrupt, broken, insolvent, and wrecked beyond repair!!! Imagine Homer Simpson sitting on his couch, watching television, while all the walls around him collapse.

GOLD WILL REACT TO THE FIRST GIGANTIC ACTION MANIFESTED IN POLICY, THE BOND INSURER BAILOUT. Many factors force the gold price up:

1) monetary debasement with huge money supply growth (inflation),

2) broad price inflation downstream, but also

3) threats to the integrity of the banking system .

My forecast is that the Western banking system, including Europe and England , will be similarly threatened on matters of integrity. The English banking system perhaps is as royally screwed and doomed as that of the United States . To the extent that European banks loaded their vaults with toxic US$-based mortgages, their banks will suffer integrity problems also. Integrity is basically defined as having sufficient reliable capital to support a portfolio of loans and asset backed bonds. Both figures are changing, reductions in both, as ratios are strained and turn negative.

The bank system is burning, in need of urgent medicine. The BKX bank sector stock index chart looks downright catastrophic. Moodys reports the Home Equity Line of Credit (HELOC) market, which peaked in 2004 & 2005 at $600 to $700 billion annually, is running arrears late by 60 days at a 16.5% rate. This HELOC delinquent rate is on par with subprimes. HELOC loans are not subprime. The main theme of the banking debacle in 2008 will be the extension far beyond subprimes into PRIME mortgages, as fully detailed in the article last week. The impact fallout from the bond insurers might hit home soon, as Wall Street will be forced to bring countless more wrecked billion$ in mortgage bonds onto balance sheets.

A further $2400 billion in municipal bonds might be subjected to distress sales after institutions are forced to sell bonds unable to maintain investment grade ratings, a second shoe from bond insurers. The banks are under siege. In time, the USFed and USGovt will have to bail out both major banks and bond insurers, in addition to mortgage bond holders, and maybe to home owners. The bigger better question might be what the USGovt will not bail out??? With the bank crisis growing worse, not better, gold will be a powerful safe haven, not USTreasurys.

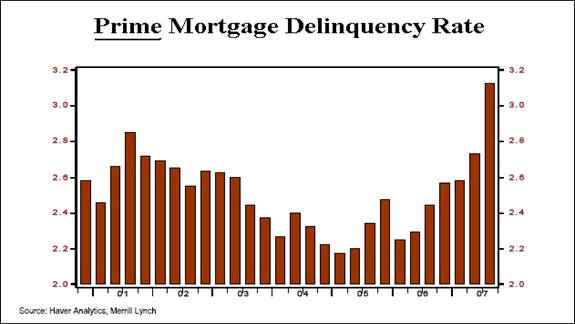

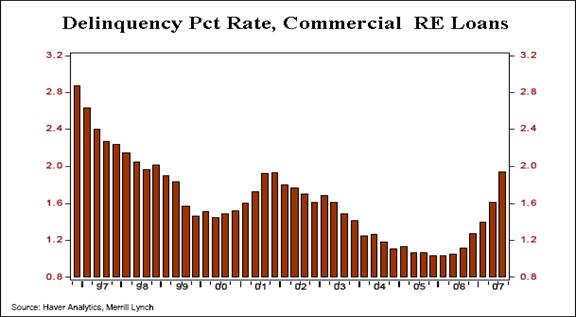

The theme in 2008 will be the broadening of the banking bond system debacle. More evidence for example can be found in the rising delinquency rate for prime mortgages and commercial loans. The prime DQ rate is already higher than the 2001 rate, the time of the last officially recognized recession. Soon the DQ commercial rate will easily eclipse the 2001 rate, when a recession hit. Anyone who believes the worst is over with mortgage problems lives in a fairy tale world, or downwind from Wall Street media effluent (not affluent) trumpets. US national housing values are destined to decline another 7% to 10% next year, directly leading to an all-out assault on prime mortgage bonds. Their collateral is falling, so the bond must fall in value. With leverage, losses will be amplified. In all my reading, only in two cases have analysts mentioned the harmful effect on ‘AAA' mortgage bonds from falling home valuation. They frequently cite inclusion of prime mortgages in with subprimes, packaged as damaged CDO bonds. They home valuation factor will be in the prime news next year.

USDOLLAR & GOLD

Notice that while the USDollar DX index has enjoyed a moderate bounce, the gold price has held firm, resilient to the DX counter-trend rally. My conclusion is that gold is resilient since monetary inflation is fast rising, and bank turmoil is in the news on a daily basis. The money supply growth, always intentionally confused by the financial media and USGovt itself, is rising in every major continental corner. In Europe and the United States , that money growth rate is in the 15% neighborhood. The spillover into actual price inflation and rising cost structure is assured. On Tuesday, the Euro Central Bank announced a $500 billion (half a trillion dollars) in funding lines, the details of which will take time to be digested. Talk finally hit the media networks of a ‘Weimar-like' situation, which means reality is slowly seeping in for desperation not seen in 70 years.

Look for the DX index to enjoy some coordinated lift from foreign central banks, as well as a perverse lift from gradually worsening conditions in Europe generally. The central banks are acting together in the US $ lift, out of vested interest. Traders are covering their US $ short positions, resulting in a cover rally. My expectation is that in January, all those successful speculators will load up again on the next round of US$ short exercises. They enjoy the higher starting points. The current rally could reach 78.5 on the DX, perhaps 79. Regard the current bounce as now of an intermediate variety. The tighter grip of USEconomic recession will harm the USDollar in the coming months. The list of dollar negatives is long, powerful, and growing, counter-trend rally or not.

The gold price is consolidating, a process well along into its second month. The important moving averages are both rising. The uptrend provides a line of support at the 780-785, exactly at the 3/8-ths retracement level pointed out in previous articles. So far, gold has managed to resist the USDollar bounce, which has a little gusto. Monetary inflation has replaced the USDollar as the primary driver for the gold price in my view.

A warning signal comes in the MACD (moving average convergence divergence) cyclical indicator. A crossover would be bearish in the intermediate term for gold. The worsening bank/bond debacle serves as a powerful bullish supporting factor for gold. While a decline to the 20-week moving average near 760 is possible, or to 750 where minor support shows, this rally could end in a flash. My forecast is for the USDollar rally to be abruptly ended by emergence of news on the bank/bond debacle, or broader USGovt bailout announcements, or focus given to mounting money inflation as being dangerous. A quiet holiday season could invite an attack on the US $ DX index after a considerable runup, whose basis rests little on the reality of fundamentals. That would further firm the gold price.

THE HAT TRICK LETTER PROFITS IN THE CURRENT CRISIS.

From subscribers and readers:

“There are four writers that I MUST READ. You are absolutely one of those favorites!! William Buckler, Ty Andros, Richard Russell, and YOU!!” (BettyS in Missouri )

“I find your pieces brilliant because they are not just about the markets or investment trends or even the emerging new world order, but the way the ice is breaking beneath our feet. You capture the tragedy and farce and corruption of the decline of the United States in a way that no one else quite does.” (LiviaL in Florida )

“You do excellent work. Your paid service is extremely helpful to me as I attempt to catch up with the non-documented science of market finance and ‘market physics' which is what I am most interested in learning. Additionally the effort you put forth is recognizably stronger than other financial writers.” (JackM in Maryland )

“Your newsletter caught my attention when the Richebächer report ended. Yours has more depth and is broader in coverage for the difficult topics of relevance today. You pick up where he left off, and take it one level deeper, a tribute.” (JoeS in New York )

“I am currently subscribed to over 60 paid newsletters. Your analysis is by far the most accurate every time. The most impressive characteristic of your thought processes is your ability to think in multi-factorial terms. You are one of the few remaining intellectuals with such capacity intact.” (Gabriel R in Mexico )

By Jim Willie CB

Editor of the “HAT TRICK LETTER”

www.GoldenJackass.com

www.GoldenJackass.com/subscribe.html

Use the above link to subscribe to the paid research reports, which include coverage of several smallcap companies positioned to rise like a cantilever during the ongoing panicky attempt to sustain an unsustainable system burdened by numerous imbalances aggravated by global village forces. An historically unprecedented mess has been created by heretical central bankers and charlatan economic advisors, whose interference has irreversibly altered and damaged the world financial system. Analysis features Gold, Crude Oil, USDollar, Treasury bonds, and inter-market dynamics with the US Economy and US Federal Reserve monetary policy. A tad of relevant geopolitics is covered as well. Articles in this series are promotional, an unabashed gesture to induce readers to subscribe.

Jim Willie CB is a statistical analyst in marketing research and retail forecasting. He holds a PhD in Statistics. His career has stretched over 24 years. He aspires to thrive in the financial editor world, unencumbered by the limitations of economic credentials. Visit his free website to find articles from topflight authors at www.GoldenJackass.com . For personal questions about subscriptions, contact him at JimWillieCB@aol.com

Jim Willie CB Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.