How Savers Can Get 10% Yields Without Buying a Single Stock?

Personal_Finance / Investing 2012 Mar 12, 2012 - 02:29 PM GMTBy: Casey_Research

By Alex Daley, Casey Research : The average interest rate for a savings account today is 0.45%. It wasn't that long ago that one could easily earn 5% in a well-chosen savings account, like those offered by ING Direct, or bump that up by a point or two by putting money away in a CD. Thanks to the largesse of our Federal Reserve and the antics of bankers around the country and world, those days are over, probably for a very long time. Interest rates are at an all-time low, and they look poised to stay there for a while. It's just about impossible for a saver to find the kind of yield that will beat inflation, let alone be enough to provide an income one can live on.

By Alex Daley, Casey Research : The average interest rate for a savings account today is 0.45%. It wasn't that long ago that one could easily earn 5% in a well-chosen savings account, like those offered by ING Direct, or bump that up by a point or two by putting money away in a CD. Thanks to the largesse of our Federal Reserve and the antics of bankers around the country and world, those days are over, probably for a very long time. Interest rates are at an all-time low, and they look poised to stay there for a while. It's just about impossible for a saver to find the kind of yield that will beat inflation, let alone be enough to provide an income one can live on.

Savings and CD rates are at extreme lows. Bonds aren't much better. The S&P 500 dividend yield sits at 1.97%. Yet the interest rates that banks charge for consumer loans – other than mortgages, which are artificially low thanks to government subsidies – are still quite high. Federal Reserve statistics peg a 24-month personal-loan interest rate at an average of 10.92% at the end of 2011, down just under 1.5% from 2007 highs. With credit cards the rate is even higher, an average of 12.78% as of the end of November 2011.

The agreement between banks and savers has always been one of mutual convenience. Savers put their money on deposit with a bank, and in exchange the bank pays interest while keeping that money safe, generating income from lending it out. That income comes from all sorts of sources, ranging from mortgages to commercial business loans, but consumer credit is and has always been a large part of that equation. In fact, today consumer credit outstanding in the United States is just north of $2.5 trillion. (Commercial banks hold nearly $1.1 trillion of those debts; finance companies more than $500 billion; credit unions over $225 billion; and now the federal government is in the game, with $453 billion on its books, up more than fourfold since 2008. The remainder is held in savings institutions, nonfinancial businesses, and pools of securitized assets.) In the past, as banks made more and more money from their loan operations, they were able to share more with savers. They competed based on interest rates, even offering higher rates of return to customers willing to sacrifice liquidity and lock up their money for a few months or a few years in savings accounts with minimum balances or certificates of deposit with early-termination fees.

However, these days that accord seems to have fallen apart. With official inflation hovering above 3%, and the real rate – including the types of things every consumer needs to buy, like energy and food – well above 6%, half-a-percent interest simply doesn't make the grade. Banks continue to charge high interest rates, yet federal policy leaves the individual investor or saver holding the bag.

However, thanks to technology, new alternatives have been developed that allow individuals to earn some serious interest without having to turn to the stock market and the higher-yield, higher-risk securities one can find there. While I make my living investing in the stock market and welcome all of the liquidity, volatility, and options that come with it, I also realize that many savers would prefer something much closer to the model they get with a certificate of deposit. And even for us avid investors, any alternative market where one can consistently earn high single-digit and even double-digit yields is quite welcome… especially one with very little correlation to the stock market when things go bad.

It's a new idea but is based on the familiar technologies of the Internet; it's known as peer-to-peer (P2P) lending. The premise is simple: cut the bankers out of the loan market and keep the difference for yourself by making loans directly to other consumers.

I know, that sounds rather risky. When I see my neighbor pull up in his driveway with a shiny new car that I can guarantee costs more than his annual salary, the idea of loaning money directly to other consumers seems a little crazy. However, that's where the real innovation lies. With peer-to-peer lending, an individual investor doesn't make a single $10,000 loan. Instead, he can buy 400 different loans, taking only $25 of risk per loan, for example. Services that offer this option pull together large numbers of investors, who each take a small slice of large numbers of loans, thereby distributing risk much like an index fund. The result is usually a steady and expected rate of return after fees and defaults.

And there are plenty of defaults. Consumer credit is a risky space, after all. With peer-to-peer lending one can choose among unsecured loans only. However, despite what you may have gathered from your last attempts to find a parking space at Home Depot on a Saturday, the majority of people are good. And those good people have a tendency to pay back their loans. As an investor, these P2P services allow you to pick loans by risk category. Credit scores, debt-to-income ratios, income verification, and all the familiar tools of the professional lender are there, allowing you to make decisions about what kind of loans to buy and which to avoid.

This allows individual investors to tailor a portfolio to their own risk tolerance. Whether selecting all the individual loans by hand, or using the bulk investing tools each of the suppliers provide, a portfolio can be built in a variety of ways: from only investing in "A" grade loans with single-digit interest rates and predictably low defaults, to debt-consolidation loans for consumers with much lower credit scores, paying much higher interest but coming with significantly higher defaults as well, and everything in between.

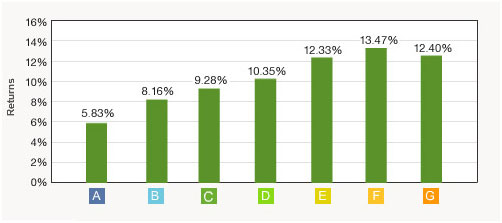

At Lending Club, the largest of the new breed of peer-to-peer loan providers, which now funds over $36 million in loans per month, investors with more than 800 notes in their account have all earned positive income after fees, with 93% of those investors earning between six and 18% interest. The net annual return in its various classifications of loans (where A is low credit risk and G is highest), after both defaults and fees, is as follows:

Lending Club is not alone in this business, either. Its competitor Prosper offers similar products and similar rates of return. Prosper has funded some $300 million in loans since its inception in 2006 through the end of 2011, compared to the $500 million funded by Lending Club in the same time frame. Smaller upstarts like Lonio and LendFriend are putting their own twists on the market as well. Even charities are getting into the game. Organizations like Lendesk and Kiva allow people to make low- or no-interest microloans to people in developing economies. That's fine for your annual charity budget, if you have one. However, when we're talking real investments, we are focused solely on those that can generate a decent return for us.

These companies make their money on a combination of small fees to borrowers for successfully funding the loan, and to sellers as a processing fee for collecting the interest, handling collections, etc. In all, their fees are small as they are spread out across a large number of loans, usually in the range of 1-2%, depending on loan value. Compared to the 8-9% spread banks are keeping for the same service today, the comparison for investors is excellent. Like a long-term CD, your funds are locked up in the loans for three to five years, but the return is much better.

However, for these services to work for investors, they must work for borrowers as well. And they do, mainly by passing on some of those Internet economies of scale. Some of the savings that P2P lenders realize from cutting out the many middlemen in the banking industry are also passed along to borrowers. This makes their rates extremely attractive and keeps a flow of new candidate loans in the system. Of course, just as banks are doing fewer and fewer loans for things like auto buying (where it is difficult to compete with captive finance corporations which are willing to incentivize interest rates to move product), Lending Club and Prosper attract borrowers mostly for major purchases and debt consolidation. On Lending Club, more than 67% of the loans are for paying off credit card debts. Other loan types for borrowers and investors include home improvement, small business, and major purchase financing.

The reason the technology works is the same reason the Internet works for any large-scale e-business, such as Amazon.com. Because these lenders operate entirely virtually, they save massive amounts on not having to build, maintain, and staff branches all around the country. Instead, they connect borrowers to sellers entirely online, using largely automated systems, and thus can keep their costs extremely low. They can also handle much larger volume than any one bank branch, and they can reach large amounts of territory from a single location. Granted, SEC and local regulations for the companies are still onerous, and thus their services are not available in all the states – including my own, Vermont. But most major-population states are within their reach.

The marketing couldn't be simpler: everybody – investors and borrowers alike – would love to get one over on the bank or credit card company. And these P2P lenders allow both sides to do exactly that.

That has resulted in a rapidly increasing base of both. Loans on record at Lending Club have been increasing at a rapid pace, and competitor Prosper grew loans by 178% last year. That kind of growth is attracting big-name investors. Peter Thompson, director at Thomson Reuters and owner of Thomvest, just put $25 million into investments at Lending Club and took an equity stake in the company.

While not quite as big a name as he is, I can say that I have been an active investor utilizing both services myself (never as an equity investor, only as a customer) for a number of years. I still actively use Lending Club today, and my own return on capital – after fees, charge-offs, and taxes – across a large number of notes has been a solid 7.5% net annualized. Also take into account that I am not a particularly aggressive investor when it comes to these notes. My technology portfolio more than takes care of my appetite for high risk/reward. This is just a portion of what I consider my "safe" portfolio.

What the Internet has done to retail, to music, to movies, and many more industries, it is now starting to do to banks. I for one am glad to see it happening. Better yet, I'm especially glad to be able to profit from it.

[If you decide to follow the same route, it seems Lending Club is currently offering a 2% bonus for new accounts to help boost your yield a few more points. We could not find anything similar for Prosper.]

This article was originally published in the Casey Daily Dispatch. Sign up today for more insightful articles about investing, technology, energy, metals and big-picture, contrarian analysis of current trends… all completely free. Learn more and sign up now.

© 2012 Copyright Casey Research - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.