Stock Market 'Sell in May, and Go Away,' Strikes Again

Stock-Markets / Stock Markets 2012 May 11, 2012 - 01:52 AM GMTBy: Gary_Dorsch

Mark Twain, one of America's most famous literary icons, and known for his folksy humor, used to say, "History doesn't repeat itself, but it sure does rhyme."

Mark Twain, one of America's most famous literary icons, and known for his folksy humor, used to say, "History doesn't repeat itself, but it sure does rhyme."

On Wall Street, it's been the "least loved Bull market" in history. Since the start of 2008, there's been a massive exodus of more than $400-billion from mutual funds that invest in US companies, after the biggest and scariest plunge this generation of investors has ever seen. Yet at the same time, the current Bull market, that's grown up in the shadow of the worst financial crisis since the Great Depression, is the seventh best percentage gainer in market history. It's also the first Bull market to double in value in less than three years. Despite its impressive résumé, this Bull market gets little respect from retail investors. It's considered to be a bubble that's artificially inflated by the Federal Reserve's cheap money policies. Spooked investors prefer to be clear of the maniacal stock market, before the grizzly Bear arrives.

By historical standards, this 38-month-old Bull has beaten the odds. Only 14 of the past 34 Bull markets lived to their second birthday. Only eight of the past 34 Bull markets (22%) on Wall Street lived to see their third Birthday. Bull markets are tricky. They frequently try to throw investors off the bandwagon. There are "pullbacks" that rattle the stock markets about 3-or-4-times per year, and usually toss fortune seekers off the gravy train. Pullbacks have ignited an average loss of -7%, but the loss is usually recouped in 31-trading days.

There are also frightening "Corrections" that rattle investors' nerves. Since 1928, there've been 94-corrections of -10% or more, leading to upheavals in the stock market, about once in every 11-months. They typically last for four months and have erased -14% of the stock market's value, on average. Since 1928, there have been 42 "severe corrections," or market declines of -15% or more. In 60% of the instances where a severe correction of -15% has evolved, the stock market's downturn has morphed into an outright Bear market.

Nobody rings a bell to let everyone know that the stock market has reached a top or bottom. And no one knows for sure how far a Bull or a Bear will extend. The average decline of a Bear market is -36%, which is an experience that most investors prefer to avoid. The last two Bear markets on Wall Street were the most severe since the 1929-32 stock market crash, with the S&P-500 index losing as much as -49% and -57% of its market value, respectively.

Historically, it's taken about nine months for a severe correction to reach the -20% threshold of a genuine Bear market. However, in today's world of high frequency trading (HFT), what used to take nine months to accomplish, can now be achieved in 2-weeks. With about 65% of stock trades in the US-markets now executed by high-frequency traders that use super-smart and super-fast computer programs, the market's sharp moves are amplified many times over. Sometimes, hedge funds and HFT's that use borrowed money to buy stocks are forced to sell shares in order to raise enough money to meet margin calls, when markets turn sharply lower. And in today's computer-generated world, these forced sales are done immediately, causing sharp declines in equity and increasingly in commodity markets.

Seasonally, US-stock markets usually see a strong start to the New Year, but begin to flatten out in the second quarter. Often there's a summer swoon that ends with a losing month in September. Traders call it "Sell in May and Go Away!" When analyzing the raw trading data since 1950, the worst period of performance for the US-stock markets, is between May 1st and Halloween. The month of October is famous for some of the biggest crashes in history, but it also has a reputation as a Bear market killer. Roughly 85% of the gains in the stock market are usually made in the months of November through April.

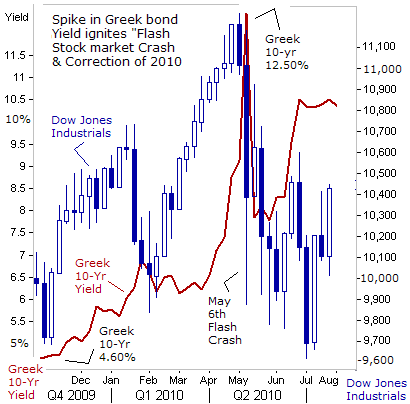

In an eerie sense of déjà vu, the US-stock market is beginning to get a bit wobbly again, and has tumbled lower in the month of May, for the third year in a row. Two years ago, the Dow Jones Industrials topped out on April 26th. There was the infamous May 6th "Flash Crash," when the Dow Industrials fell as much as -1,000-points lower within a few hours hours, wiping out about $1-trillion in market capitalization at one point, before recouping 600-points of its losses within 20-minutes of trading. The wild swings in the marketplace were exacerbated by computerized algorithm traders, but the catalyst for the crash was an unexpected upward spiral in Greek bond yields, that ushered in the Euro-zone's debt crisis.

Prior to the May 6th "Flash Crash," the majority of professional investors were complacent and still in a bullish frame of mind, after watching the stock market bounce back from previous pullbacks and corrections, during the first year of recovery for the "Least Loved Bull." Every decline in the stock market turned out to be a better buying opportunity . Earnings for S&P-500 companies were rebounding strongly, and surprising to the upside by a 3-to-1 margin. Yet the Greek debt crisis ushered in a whole new element of instability, and reopened the horrible memories of the subprime debt crisis. Following the initial shock from the May 6th "Flash Crash," the Dow Industrials moved erratically lower, surrendering -15% of its value from its peak level. There were sporadic rallies, but on weak breadth and lower volume.

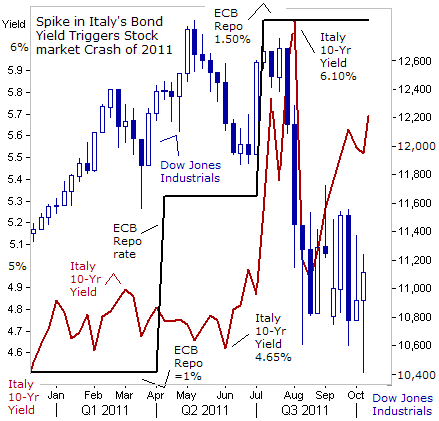

Last year, the "Least Loved Bull" rally began to run out of steam on May 2nd, 2011. Over the next two months, the Dow stumbled -1,000-points lower to the 11,900-level. There was a last gasp rally to the 12,650-level that fizzled out on July 26th, when stock markets across Europe were rattled by an upwards spiral in Italy's 10-year bond yield, which suddenly jumped +144-bps higher to above 6-percent. The upward spiral in Italian bond yields triggered a meltdown in the Dow Jones industrials, knocking it -2,000-points lower. Swings of several hundred points in just minutes were commonplace. The most extreme was on August 9th, when the Dow soared +600-points in the one hour and 45-minutes after the Fed pledged to keep the fed funds rate locked at zero percent through mid-2013. HFT programs make up about half of the trading volume in a normal market day but 70% or more on a volatile one.

The upward spike in Italy's 10-year bond yield conjured-up fears that Italy could default on its €2-trillion pile of debt. That could've started a global credit freeze, through a chain reaction throughout the Euro-zone's banking system, and spreading to large US-banks that have huge loans to European banks. Europe is a big consumer market for S&P-500 Multi-Nationals, accounting for 25% of their sales last year. On August 10th, US President Barack Obama met Fed chief Bernanke, Treasury chief Tim Geithner, National Economic Council chief Gene Sperling and White House chief of staff Bill Daley at the White House, - the infamous "Plunge Protection Team," (PPT) and it was agreed that the PPT would put a floor under the US-stock market to prevent investors from dumping stocks in a selling frenzy. The PPT drew a line in the sand for the Dow Industrials at 10,600, aiming to prevent the widely watched index from falling into the clutches of a cyclical Bear market.

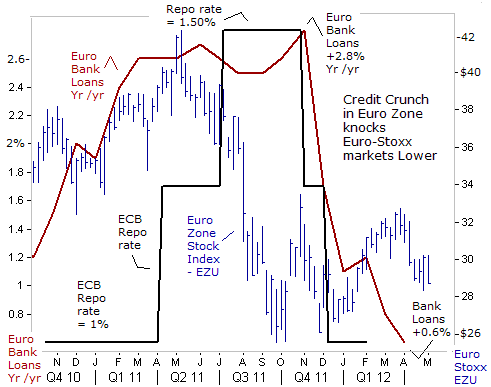

The Fed's rescue operation - dubbed the "Bernanke Put" succeeded in putting a floor under the jittery stock market. The Fed's agents on Wall Street began a massive buying spree, bidding up Dow Jones Industrial futures contracts, and signaled that it was safe to buy stocks. The Fed got plenty of help from its allies - the Bank of England and Japan unleashed additional rounds of QE. The ECB arranged a € 1-trillion LTRO scheme that put a temporary lid on Italian and Spanish bond yields, recognized as a backdoor type of QE- scheme.

History shows that when the US-stock market narrowly dodges a Bear market, the market quickly shifts into rally mode. Buying during a correction can be profitable. Following the past eight near misses of a Bear market, the S&P-500 index has rallied + 31.7% over the next 12-months, when fears of an imminent recession are not realized. Closely following the historical script, the S&P-500 index rallied +30% from above its October 4th low, over the next six months. The S&P-500's recovery rally peaked on April 2nd, 2012, but didn't begin to pullback at least -5% or more, until May 1st.

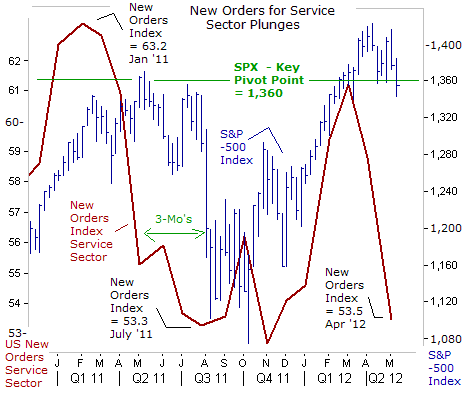

Ominously, the New Orders index for US-services fell -5% in April to the 53.5-level. Ninety percent of US-economic activity is linked to the service sector, and a sharp drop in new orders signals a broader economic slowdown in the months ahead. Last year, the New Orders index for US-services plunged in April and June, and preceded a July-August swoon on Wall Street.

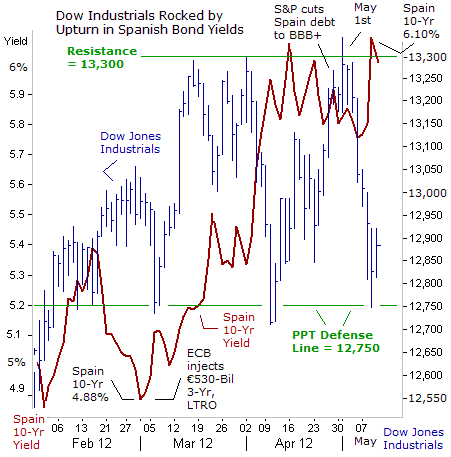

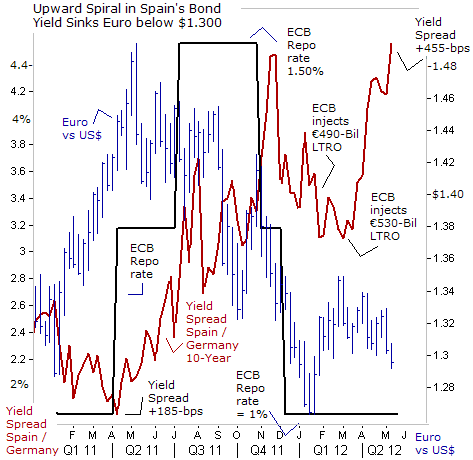

This time around, "Sell in May and Go Away," was ignited by an upward spiral in Spain's 10-year bond yields to above 6-percent. There's mounting evidence that the Euro-zone trading bloc is sliding into a severe economic recession, and it won't be easy to pull out of the quagmire anytime soon. Nagging problems originating from Europe have a knack for whacking Wall Street and global stock markets in the May to June quarter, with uncanny timing. Bullish traders on Wall Street had figured they could put the Euro-zone's debt crisis to rest, after the ECB's recent injections of €1-trillion into the Euro-zone's banking system. Yet following the second LTRO installment on Feb 29th, Spain's bond yields ratcheted upwards.

Banks in Spain stuffed their coffers with government bonds, using the ECB's ultra-cheap 1%, three-year loans to stock up on Spain's sovereign debt. Spanish banks are estimated to have borrowed €316-billion directly from the ECB, equivalent to 11% of their total balance sheet. In the last four months, Spain's banks have bought a net €80-billion worth of government paper, and boosted total sovereign holdings to a record €263-billion. However, the upwards spiral in Spanish bond yields to above 6%, has translated into big losses for Spanish banks.

The bursting of Spain's property bubble has also left Spanish based banks holding vast amounts of foreclosed properties. Madrid is expected to announce Friday that banks will be required to set aside an additional €35-billion to cover potential losses on real estate assets. This would be on top of the €36-billion in loss provisions that Spanish banks are required to meet under legislation announced in February. Spain 's Foreign Minister Jose Manuel Garcia-Margallo said his country faced a crisis of "huge proportions" and that the Spanish banking system may ultimately need a bailout of €120-billion by year's end.

The cost of insuring €10-million of Spain's debt against the odds of default, have climbed to record highs, of €512,000, which would put added responsibility on the IMF to step-in with a bailout for the Spanish government and banking system. Shares of Banco Santander (STD) and Banco Bilbao (BBVA) have tumbled to their lowest levels since March 2009, reflecting fears that they'll need an emergency bailout.

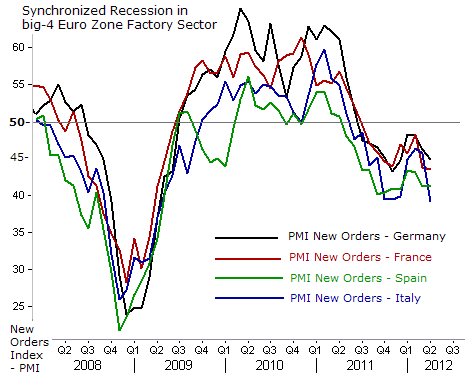

"Sell in May and Go Away" for 2012, is getting its cue from Europe's economic malaise, which in turn, has snake bitten Asian exporters in China, Korea, and Taiwan. A key forward looking gauge, the Purchasing Manager's Index (PMI), for New Orders is flashing a deep and protracted recession in the Euro-zone's factory sector, led by Italy and Spain. The recession is spreading to the pillars of the 17-member economy, - France and Germany. Euro-zone factories have cut workers at the fastest pace in over two years. New Orders have fallen for the 11th straight month. Spain's factory sector is shrinking at its fastest pace in 3-years and New Orders for Italian made factory goods evaporated more quickly than at any time since March 2009. The downturn is also taking a toll on jobs. Unemployment in the Euro zone rose to 10.9% of the workforce in March - it's highest in 15-years. The jobless rate rose to 24% in Spain, 21% in Greece, 10% in France, and is 9.3% in Italy.

The ECB's emergency loans put in place in December and February, through its LTRO program has rescued the banking system, but did not help the Euro-zone economy. The ECB provided more than 500-banks with €1-trillion in 3-year loans at a borrowing cost of 1%. However, the Euro-zone's banks are using the LTRO funds to refinance their own bonds that come due this year, instead of financing business activities in the real economy. Bank loans outstanding in the Euro-zone were only +0.6% higher in March from a year earlier, signaling a highly restrictive "credit crunch" is strangling the Euro-zone's economy.

In the wake of the € 1-trillion LTRO, European governments have unveiled austerity measures that include sweeping attacks on jobs, wages and basic social services. It has now become abundantly clear that the European political elite and the IMF are not aiming at staving off the bankruptcy of Greece and other EU states gripped by sovereign debt crises. Instead, the EU fiscal pact is designed to enable a massive transfer of wealth from the masses of the European population and into the coffers of the Oligarchic banks.

European taxpayers now own the bulk of Greece's € 266-billion ($345-billion) of debt. Over the course of the past two years, the Euro-zone banking Oligarchs were able to offload about €194 billion of toxic Greek bonds onto the balance sheets of the European Central Bank, the Euro-zone taxpayers and the IMF . In 2010, before the first bailout of the banking Oligarchs, Greece owed about €310 billion to the private sector.

Contagion risks are back. With Greece edging towards the Euro exit gates, Spanish and Italian borrowing costs are creeping up. The charts are pointing to another attack on the Euro. And, once again, Greece is at the epicenter. A return to the drachma, a massive devaluation, and a default on the remaining private sector debt would create massive tensions across Europe. The ECB's holdings of Greek sovereign debt would suffer big losses.

Austerity is increasingly unpopular in Europe because it doesn't work. In late March, Madrid announced its most severe package of tax hikes and budget cuts yet, aiming to reduce its annual budget deficit by $36-billion. Spain missed its deficit target in 2011, and, without the latest austerity package, would have done so again in 2012. However, the austerity drive failed to achieve what it aims to do: rebuild investor confidence, and bring down bond yields. Instead, bond investors are spooked by Spain's zombie banking system and its economic state of depression. Foreign lenders are demanding higher interest rates for Spanish bonds. Despite its new austerity budget, Spain's-debt-to-GDP ratio is expected to increase to 80% this year, from 68.5% in 2011. Simply put, Spain is moving backwards.

Bonds of at-risk countries have suffered since the May 6th balloting. Spain's 10-year yield over German Bund yields widened to +458-basis points today from 415-bps at the end of last week. Italy's widened to 412-basis points from 385-bps over the past three days. The Euro skidded to $1.2930, or -10% lower from a year ago. Politically speaking, Greece is already has one foot outside of the Euro currency. The only question is about the timing and disorderliness of its exit. France's new president, Francois Hollande has pledged a 75% tax on annual incomes of €1-million or more and would raise the minimum wage, - measures that could ignite capital flight from the French stock market, and from the Euro.

There are signs that the two pillars of the Euro-Zone are starting to split apart, and the consequences could be a further weakening of the Euro. " Germans could end up paying for the Socialist victory in France with more guarantees, more money. And that is not acceptable. Germany is not here to finance French election promises," said Volker Kauder, a leader of Merkel's Christian Democrats. Berlin says it will not agree to issue a joint Eurobond with its troubled neighbors, and won't agree to expand the ECB's charter so that it can pursue the same quantitative easing schemes of the Fed and the Bank of England. That leaves Greece, Spain, and Italy with no easy way out of the austerity death trap.

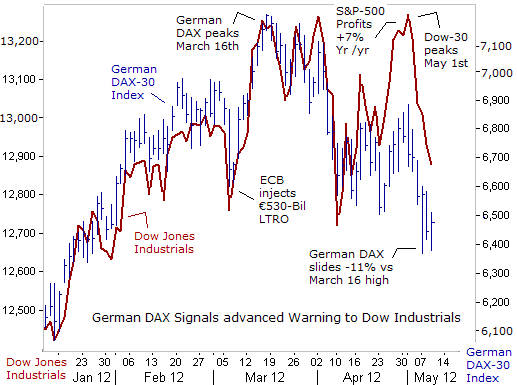

"Sell in May and Go Away" started early this year on the Frankfurt Stock Exchange. The German DAX index, the kingpin of the Euro-zone equity markets, reached the zenith of its post October 4th rally, six weeks earlier than the Dow Industrials. Since peaking on March 16th, the German DAX index has lost roughly -10% of its value, - sliding to the cusp of correction territory. German Multi-Nationals listed in the DAX-30 were scurrying around the world, and boosting exports to record highs. Germany exporters shipped goods and services worth €91.8 billion in March, up +0.9% from the previous month. It was the third successive month-on-month increase in exports, following a +1.5% gain in February and +3.4% in January.

The surprisingly strong export figures, coupled with a stronger-than-expected +2.8% increase in industrial production figures, suggest that the German economy expanded in the first quarter, - avoiding a technical recession . Yet the data released by the Federal Statistics Office is sharply at odds with the Purchasing Managers Index figures, which suggests that Germany's industrial sector is contracting. The German data also flies in the face of slumping Asian imports and a severe recession in the Euro-zone's #3 and #4 economies. Since mid-March however, the German DAX has lost -10% of its value, suggesting that traders believe that the high point for German exports has been reached, and a slippery slope lies ahead.

For market technicians, focused on the chart patterns, it's interesting to note that the German DAX topped out on March 16th at the 7,200-level, falling short of its 2011 high at 7,550, before falling -10% to the threshold of a full fledged correction. During this "pullback" phase, many traders continue to hold their weakened equities, figuring that the bad news is already discounted and that the DAX index is nearing a bottom. At this point, the German stock market may rally again. However, it would be a "suckers rally," if the market's breadth is narrow and trading volume is low. The DAX rally would fizzle out and head south again.

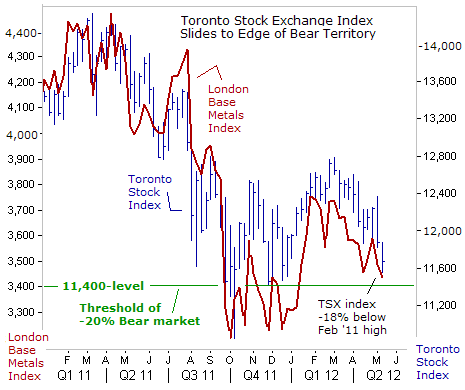

The Toronto Stock Exchange index (TSX) struggled to hold onto its meager gains in Q'1 of 2012 and has significantly lagged the S&P-500 Index for a second straight year. The hefty weighting of resource companies, such as Barrick Gold, Teck Resources, First Quantum Minerals, Suncor Energy, Canada's largest oil producer, and Canadian Natural Resources is mostly to blame. The TSX index gained +3.7% in the first quarter, - helped by gains in foreign stock markets. However, the gains have vanished, - wiped-out by a deeper than expected economic recession in Europe, and dwindling Chinese imports of base metals. The TSX's materials sector is down -21% over the past three months, signaling that a sharp slowdown in the global economy is already underway.

Since early February, the TSX index has lost more than -8% of its value. It's sliding towards the 11,400-level, which is the demarcation line into Bear market territory. The TSX never really recovered from its Crash of 2011. Many TSX powerhouses are weighed down by slumping prices for base metals, and record low prices for natural gas. In sharp contrast to the Fed's interventionist schemes, the Bank of Canada has refused to succumb to the use of QE, - thereby depriving the TSX of the extra liquidity that can artificially inflate the value of equity prices. Also, the BoC is pegging its overnight loan rate is pegged at 1%, and is even sending signals that a further rate hike could be in the cards. That's in sharp contrast to the Fed's Zero Interest Rate Policy (ZIRP), that the Fed aims to keep in place through the end of 2014.

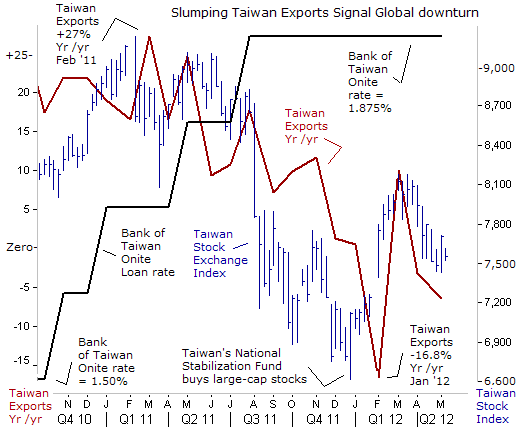

Taiwan has the 17th largest economy in the world, and it's the 14th largest exporter. It's also one of Asia's "Four Tigers" along with South Korea, Singapore and Hong Kong, known for the rapid growth of their economies. Taiwan's economy barely crept out of recession in the first quarter, with a +1.1% gain, after suffering two quarters of contraction. Seventy percent of Taiwan's economic output is linked to exports, so any global turmoil hits the country hard. Standing at the 7,550-level, the Taiwanese Stock market index is trading -17% lower from a year ago, and is weighed down by slumping exports to China, Europe, and the US.

It's interesting to note, that Taiwan's NT$500-billion National Stabilization Fund entered the local bourse on December 30th, to pick up large-cap stocks, including Taiwan Semiconductor and Hon Hai Precision Industry, to help lend support to the stock market in a bid to keep the index above 7,000 points in the short term. The intervention helped to put a floor under the market, and there was a first quarter rally to the 8,100-level. However, Taiwanese share prices are slumping again, Taiwan's exports contracted for the second time in a row in April due to weaker demand for the island's electronic and telecommunication products.

Taiwan 's exports in April fell -6.4% from a year earlier to $25.54-billion. The Ministry of Finance expects exports to fall further in the next two months. Exports to the US fell -16.3% in April from a year earlier, deteriorating from March's -8% decline. Exports to China, Taiwan's biggest trade partner, fell -9.3% compared with the -7.1% drop in March, and those to Europe rose +3.5%, following a -11.6% decline in the previous month. Exports of communication products, including the popular iPhone and iPad, fell -16.8% in April from a year earlier, - worsening from March's -6.9% decrease.

"Sell in May, and Go Away," is unfolding for the third year in a row. This time around, - Spain at the epicenter, following similar acts of instability brought upon the world markets, by Italy and Greece in the previous two episodes. The first correction knocked the S&P-500 index -17% lower. The second correction extended for a -21% loss. The corrections get bigger, if they begin from a higher plateau. But traders are conditioned to expect intervention from the Federal Reserve to stop the markets' slide, whenever risky bets go sour. Rescuing the stock market from natural corrections has become the Fed's de-facto third mandate. Traders are also conditioned to expect bank bailouts by the Euro-zone governments, with some help from the ECB that staves off a calamity, and keeps kicking the can further down the road.

What's different this time around however, is the severity of the economic malaise in Europe, - a depression in Greece and Spain, and France and Italy teetering at the tipping point of a deep recession. Europe's slump is dragging down the export sectors of Brazil, China, India, Korea, and Taiwan, and a host of other countries. A slumping global economy, signaled by weaker industrial commodity prices, would eventually be difficult for Wall Street to ignore. The odds of the Fed launching a third round of QE in the months ahead are slim to none, since the Fed can't be seen electioneering for the Obama administration, while fending off strident attacks from the Republican opposition. In a bid to stay neutral, the most the Fed can do to help a slumping US-economy is to promise to keep the fed funds rate locked at zero percent and possible extend Operation Twist. "History doesn't repeat itself, but it sure does rhyme."

This article is just the Tip of the Iceberg of what’s available in the Global Money Trends newsletter. Subscribe to the Global Money Trends newsletter, for insightful analysis and predictions of (1) top stock markets around the world, (2) Commodities such as crude oil, copper, gold, silver, and grains, (3) Foreign currencies (4) Libor interest rates and global bond markets (5) Central banker "Jawboning" and Intervention techniques that move markets.

By Gary Dorsch,

Editor, Global Money Trends newsletter

http://www.sirchartsalot.com

GMT filters important news and information into (1) bullet-point, easy to understand analysis, (2) featuring "Inter-Market Technical Analysis" that visually displays the dynamic inter-relationships between foreign currencies, commodities, interest rates and the stock markets from a dozen key countries around the world. Also included are (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, with the latest news on global markets, and view our updated model portfolio 2008. To order a subscription to Global Money Trends, click on the hyperlink below, http://www.sirchartsalot.com/newsletters.php or call toll free to order, Sunday thru Thursday, 8 am to 9 pm EST, and on Friday 8 am to 5 pm, at 866-553-1007. Outside the call 561-367-1007.

Mr Dorsch worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group.

As a transactional broker for Charles Schwab's Global Investment Services department, Mr Dorsch handled thousands of customer trades in 45 stock exchanges around the world, including Australia, Canada, Japan, Hong Kong, the Euro zone, London, Toronto, South Africa, Mexico, and New Zealand, and Canadian oil trusts, ADR's and Exchange Traded Funds.

He wrote a weekly newsletter from 2000 thru September 2005 called, "Foreign Currency Trends" for Charles Schwab's Global Investment department, featuring inter-market technical analysis, to understand the dynamic inter-relationships between the foreign exchange, global bond and stock markets, and key industrial commodities.

Copyright © 2005-2012 SirChartsAlot, Inc. All rights reserved.

Disclaimer: SirChartsAlot.com's analysis and insights are based upon data gathered by it from various sources believed to be reliable, complete and accurate. However, no guarantee is made by SirChartsAlot.com as to the reliability, completeness and accuracy of the data so analyzed. SirChartsAlot.com is in the business of gathering information, analyzing it and disseminating the analysis for informational and educational purposes only. SirChartsAlot.com attempts to analyze trends, not make recommendations. All statements and expressions are the opinion of SirChartsAlot.com and are not meant to be investment advice or solicitation or recommendation to establish market positions. Our opinions are subject to change without notice. SirChartsAlot.com strongly advises readers to conduct thorough research relevant to decisions and verify facts from various independent sources.

Gary Dorsch Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.