How Multinational Treasurers hedge their Foreign Exchange Exposure in Global Operations

Currencies / Forex Trading Nov 15, 2012 - 05:39 AM GMTBy: Sam_Chee_Kong

As can be seen from below since 1990, world trade between countries have been on the rise. The decline in world trade during 2008-2009 is due to the global financial crisis that affected many countries. However it did managed to reverse its direction by end of 2009 and continue its upward trend ahead. The ‘take off period’ actually happened since the year 2000 where world trade went up from 100 to 150 on the index.

As can be seen from below since 1990, world trade between countries have been on the rise. The decline in world trade during 2008-2009 is due to the global financial crisis that affected many countries. However it did managed to reverse its direction by end of 2009 and continue its upward trend ahead. The ‘take off period’ actually happened since the year 2000 where world trade went up from 100 to 150 on the index.

Figure 1: Volume of exports of developed, developing and transition economies: 1990-2009

(Index, 2000=100)

Source : World Trade Organisation

Rise of Globalization

The rapid rise of international trade is made possible by the ‘Globalisation’ of the world trade. Globalisation refers to the integration of the international capital, resources, labour and markets. The rapid rise in Globalisation in the world trade is made possible by the ‘theory of comparable advantage’ devised by David Ricardo in the Principles of Political Economy (1817). According to him it will be a win-win situation for countries if they are engaged in the production of goods that are advantageous to them and trade them with other countries. If Malaysia is cost effective in palm oil plantation while Taiwan is comparatively better in manufacturing computers then Malaysia should concentrate in producing palm oil while Taiwan in manufacturing computers and then they trade their products. At the end of the day both countries will benefit from the increase production of both goods. This can be illustrated with the following table.

Table 1

As can be seen from Table 1 above, without trade with other countries Malaysia’s production of palm oil stays at 5000 tons while Taiwan’s production of Computers is only limited to 6000 units which is for domestic consumption. If both countries trade their goods then the volume of trade and production will jump to 9000 tons of palm oil and 8000 units of computers respectively. In the end both countries benefited from the increase in volume of production.

A good example of Globalization will be Dell Computers. The unit of Dell computer that you bought is no longer made in the United States. It is a concerted effort of different production centres that specializes in different products that are of advantage to them. Malaysia may be the centre for parts assembly and distribution of the final product but most of its components are from various parts of the world. The hard disks and DVD-ROMs are from Thailand, mother boards from Taiwan, casings from China and so on. Its call centre is based in India due to its specialisation in outsourcing.

Why Globalize?

This brings us to the question why Multinationals want to globalize their operations? A Multinational corporation can be defined as a corporation that have production, sales and distribution in a number of countries. The following reasons may provide the answer as to why Multinationals prefer to move some of their operations overseas.

- Enables it to both horizontal and vertical integration of its business. It can integrate backwardly by sourcing its raw materials/parts from one country and forward integrate its final assembling and distribution in another country as can be seen from the Dell example above.

- Enables it to take advantage of certain quota that is given to certain countries especially in Africa and other least developed countries. One such example is the WTO’s Multifiber Arrangement (MFA) that regulated the global textile industry.

- It enables firms to take advantage of incentives, subsidies and tax holidays offered by the host countries. It can also take advantage of the low labour costs that existed in many developing countries.

- Provide opportunity to expand their operations overseas through ‘greenfield investments’ like setting up new plants or takeovers of existing plants or through Mergers and Acquisitions.

However due to increasing globalization, multinationals found that many of their operations are exposed to foreign exchange movements. Their sales receipts, project financing, cash flow from foreign operations are subjected to movements in the foreign exchange that will greatly affect the bottom-line of the company. For example an American automobile multinational with operations in Asia will be subjected the movements of various Asian currencies. If say the Malaysian Ringgit depreciates by 5% against the dollar then American cars like Chevrolet, Ford and the likes are more expensive than the local brands like Proton and Perodua. Hence due to the appreciation of the dollar the American automaker will have to raise the price of its cars and will hurt its bottom line due to decreasing sales.

On the other hand even purely domestic domiciled Malaysian companies are also subjected to foreign exchange exposures. A Malaysian latex glove manufacturer will be subjected to foreign exchange exposure if it competes with imports say from Thailand. If the Ringgit appreciates against the Baht, then it results in the local gloves being more expensive than their Thai counterparts. Hence it will boost the sales of the imported gloves at the expense of the Malaysian latex gloves manufacturers.

Foreign Exchange Exposures

There are three types of foreign exchange exposure risk a multinational will encounter when it invest in foreign markets. They are,

- Economic Exposure.

Economic exposure is also known as long term cash flow exposure. A multinational buys and sells goods and services around the world and due to the volatility of the foreign currencies it will post a threat to the receipts and payments of those transactions. An example will be a Malaysian multinational that buys latex from Indonesia and Thailand and then process it into rubber sheets which in turn exports to China, Japan and Korea. Since the Malaysian Ringgit fluctuates against other foreign currencies over time the value of the receipts and payments will also varies. The movements can be so large that it not only inflict losses to the company but also threaten its survival.

- Transaction exposure.

Transaction exposure involves short term cash flow denominated in foreign currencies due to a sale of goods or services. Whenever a firm had receivables or payables denominated in foreign currencies, then the firms cash flow denoted in local currency will fluctuates. The following are some forms of transaction exposures.

- Purchasing of goods and services on credit denominated in foreign currencies

- Borrowing and lending of funds denominated in foreign currencies

The following example illustrates how a company’s cash flow will be affected when its foreign exchange is not hedge. Suppose a Malaysian plantation company sold 10,000 tons of palm oil valued at CNY 50 million to another company in China. The following manifest shows the complete transaction from quotation to payment.

Table 2

What will be the amount received if there is no hedge and will there be an exchange loss? Table 3 below summarize the loss from foreign exchange exposures due to an unhedge position.

Table 3

As you can see from above when the quotation was first made in March the total contract sum is worth MYR24.75 million. When it was shipped in June the spot rate of Ringgit depreciates to 0.489. When payment was finally received in September the Ringgit further deteriorates to 0.483 and the final sum received was only MYR24.15 million. This represents a foreign exchange loss of MYR 300,000.00 (MYR24.45m – MYR24.15m) due to the Ringgit depreciation.

- Translation Exposure.

Translation exposure is concerned with a company’s assets and liabilities denominated in foreign currencies or its plant, machineries, debts, loans, lands and buildings or any other items that is related to its Balance Sheets. Due to the increasing globalization of the world economy, many multinationals have subsidiaries all over the world. As of the year 2010, Toyota Motor Corporation has about 51 manufacturing facilities in 26 countries. All its plants, machineries, lands, receivables, payables, loans and so on are normally recorded in the currencies of the countries they are operating in. To consolidate its accounts in Japan, all Toyota subsidiaries around the world will need to translate their accounts to Yen. As a result there exists a translation exposure due to the changes in the foreign currencies.

Should we hedge Currency Exposures?

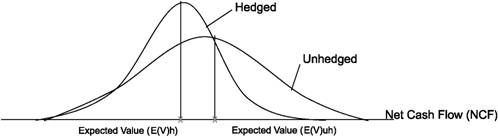

Being a Corporate Treasurer our next question is should we hedge our foreign exchange exposures? The following graph shows the distribution of both hedge and unhedge cash flows

Not too long ago Merck & Co. has done some research on the distribution of hedge and unhedge cash flow. The result is similar to the distribution graph above. As you can see when the cash flow is hedged, the mean seems to be higher and the standard deviation is lower. What this implies is that when you hedge your cash flows you are able to reduce your risk and at the same time increase your cash flows.

As a Treasurer, after acknowledging the fact that hedging does help reduce the impact of foreign exchange exposure in the company, the next question is what strategy will we employ to make sure the objectives are met. A lot of companies adopt the ‘hedge all’ strategy whereby they hedge all their transaction and translation exposures in areas where foreign currencies fluctuate widely. This can be very costly as some hedging tools like the currencies options and forward contracts are quite expensive. So, the right strategy to employ is to only hedge those cash flows, assets and liabilities that are more severely affected by exchange rate fluctuation and leave out those that can self hedged.

Foreign Exchange Management Strategy

To be effective in managing the overall foreign exchange exposure the company can employ the following strategy. First it will have to setup a Centralized Currency Information System where all possible foreign exchange exposures in the operations of the company be identified. Then all short term cash flows data are then consolidated. After that cash flow projections will be made available for monthly estimates for the next six months ahead. Hence when the data is consolidated then we should have a summary of the different kind of foreign exchange exposure facing the company and also the different currencies. After that the treasurer should decide on how much to hedge on different exposures, whether non-monetary and short term foreign loans will be best to be left alone since they are self-hedged.

Having established the Centralized Currency Information System with all the consolidated data on various foreign exchange exposures, the company needs to decide on one of the following.

- Maximum Hedge. That is when the company feels that it will seek to hedge as many of its exposures as possible so that it will reduce its risk of being exposed to foreign exchange fluctuation to a minimum.

- Minimum Hedge. This is a situation where the company will try to minimise its hedging activity through some internal and external ‘netting’ of its exposures.

- Speculative Hedge. A speculative hedge happens when the company feels that it can make a profit in hedging through currency forecasting.

Having established the goal of the company in regards to hedging its foreign exchange exposures the Treasurer will then have to look into the various hedging techniques. In view of the globalize operation of the company naturally the hedging techniques will encompass both internal and external hedging. The treasurer will first have to use its internal hedging techniques to downsize the exposure position and then only use external hedging techniques to hedge the balance of the exposure. This strategy is commonly used by treasurers because external hedging costs more than internal hedging. What encompass the internal and external hedging techniques?

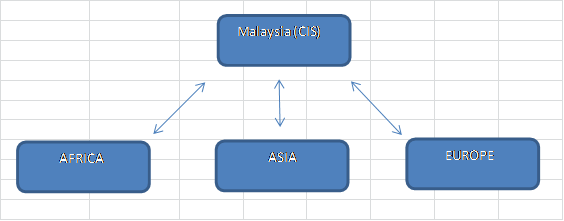

We shall use the following company as an example to illustrate the various techniques used for both internal and external hedging.

Name Of Company : Ipoh Plantations Berhad

Market Capitalization : MYR 650 million

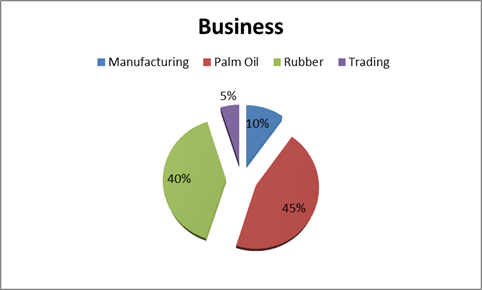

Nature of Business : Rubber, Palm Oil Plantation, Manufacturing and Trading

Market Reach : Domestic and Overseas

Subsidiaries : 1) Indonesia – PT Indo-Rubber - Manufacturing

2) Singapore – Sino Rubber Industries - Trading

3) Thailand - Evergreen Trading – Palm Oil Estate

4) China - Malay-Sino Industries - Chemical

5) Europe - Eurasia Trading Co. – Trading

6) Africa - Ivory Coast – Cocoa Plantation

Ipoh Plantation’s Currency Information System

Internal Hedging

Internal Hedging as its name implies mostly involves using internal resources and techniques to resolve certain type of foreign exchange exposure.

- Netting. This technique is used between the Head office and its subsidiaries to ‘net off’ as much currency flows as possible so as to minimize the amount that needed hedging. For this we shall use our Indonesian subsidiary PT Indo-Rubber to illustrate the use of Netting. In June Ipoh Plantations send MYR10 million worth of Rubber Latex to its Indonesian subsidiary (PT Indo-Rubber) to be processed into rubber sheets.

In July, PT Indo-Rubber sends back MYR15 million worth of rubber sheets. In normal conditions the solution will be to hedge the two transactions separately totalling MYR25 million. However with netting Ipoh Plantations need only to transfer MYR5 million (MYR15-MYR10 million). Hence instead of paying for two hedging contracts totalling MYR25 million, the company now only pay for one hedging contract which is MYR5 million. With netting it not only helped to reduce currency exposure but also the cost in commissions.

- Bilateral Netting. By this it means the use of two subsidiaries of the company to net off their cash flows exposure in payables and receivables without involving their HQ. As for our example our subsidiary in China can performed bilateral netting with another subsidiary in Thailand.

- Multilateral Netting. This normally will involve more than two subsidiaries and the HQ. Subsidiaries will need to notify their HQ on the intra company currency flows in payables and receivables. The Treasurer in HQ will interact with the subsidiaries to perform the inter-company currency hedging. In our example the subsidiary in Europe might be buying rubber sheets from Indonesia, palm oil from Thailand and chemical products from our China subsidiary. In turn our both our Thailand and Indonesian subsidiaries are buying chemicals from our Chemical plant in China. Our Singapore unit is buying products from our HQ in Malaysia, Indonesia and Thailand.

So it’s the job of the Treasurer to integrate all the different cash flows and provide the most cost effective measure in dealing with the various currency exposures. So you see things can get very complicated with intra companies netting and this involves a company with five subsidiaries. Just imagine if it is a Multinational company like Merck & Co with more than 100 subsidiaries around the globe?

- Matching. Matching is another way to hedge currency flows but it involves third parties. How does matching works? In matching, a company will try to match the outflows and inflows of a currency through timing both events. Say our HQ in Malaysia sold a consignment of palm oil to India and instead of receiving the payment (in US$) in a couple of months. It can then arrange for some import from India say rice and then try to match this payment with the expected dollar receipts which is due in a couple of months. Hence with this so called ‘natural matching’ it will eliminate the need for any hedging against foreign exchange movements.

- Leading and lagging. This involves the speeding up or delaying payments after a transaction had been accomplished. However this technique requires some form of speculation due to the need to identify the movement of the exchange rates. How it works? If the foreign currency of the payable (receivable) is expected to depreciate in due time then it is of the best interest of the company to delay (speed up) the transfer the payment. Say for example recently our HQ bought a consignment of rice from India payable in USD which is expected to appreciate in the coming weeks. It will be the best interest for our HQ to pay up as soon as possible before the USD appreciates further. This is what we call leading currency payments.

External Hedging

Obviously there are limitations as to what an internal hedge can do and it is not possible to cancel out all exposures. For example through nettings the company cannot always net off the receivables with the correct amount of payables and at times there will be no netting at all due to the problem in timing. Under such circumstances the treasurer will have no choice but will have to consider an alternative strategy other than the traditional internal hedging techniques on how much to hedge and what instruments to use. The following are some of the strategies that are often used for external hedging.

- Forward Contract. It is the most widely use external hedging techniques. Forward Contract is an agreement on buying/selling a fixed amount of currency at a fixed rate and at specified date in the future. This will enable any currency exposure be eliminated because the future rates will be lock-in at the time the forward contract is executed. The only risk is the counter-party risk of default from the customer in making payment or the failure on the bank side. To illustrate we used the following example. Suppose our HQ (Ipoh Plantations) in Malaysia exports 10 million tons of palm oil to a company in U.S. The following are the details

- Contract size is USD 8 million.

- The spot rate is MYR3.00 : USD1.00 valuing the contract at MYR 24 million.

- Payment in 90 days

- 90 days Forward market rate is MYR2.950

If our HQ feels that there is a possibility of a depreciation of the USD against the MYR due to the discount in the forward market, the next logical step is to do is to sell forward the USD8 million that it is due to receive in 90 days. At maturity in 90 days, Ipoh Plantations will simply deliver the USD8 million it will receive from the U.S importer to the bank (the counter party) and in return we will receive MYR23.60 million (MYR2.95 x 8 million) regardless of what exchange rate is prevailing then. Hence Ipoh Plantation’s anticipated receivable of USD8 million will be offset by the USD 8 million payable by the forward contract. The end result will be zero exposure. The following table shows the hedge and unhedge position at maturity.

Table 4

- Currency Options. An option is a right but not obligation to buy/sell a certain amount of foreign currency at a fixed rate in a specified date in the future. A Call/Put option is a right to Sell/Buy a fixed amount of certain currency in a specified date in the future. The beauty about options is that it will protect the exporter from any adverse movement in foreign exchange but also help it to capitalize on any favourable exchange rate movement. From the table above, when using forward contract Ipoh Plantations will only gain if the US dollar depreciates below 2.95 but it will not stand to profit from the appreciation in the dollar. If the dollar appreciates to 3.05 then Ipoh Plantations will have to forgo MYR800,000 in profits.

In view that the dollar is going to depreciate in the next few months, Ipoh Plantations decided to buy a put option on USD8 million at an exercise price of $2.95. Assume that the premium for the option is 1.5%, then the cost of hedging USD8 million will be MYR23,600,000 x 0.015 which is MYR354,000. At maturity in 90 days, if the exchange rate falls below 2.95 then Ipoh Plantations will exercise the Put option to sell USD8 million at 2.95. So it will still receive MYR23,600,000 at the end of the day. What if the USD appreciates to 3.05? Then Ipoh plantations will not exercise the option and rather let the option to expire. It will then convert the USD8 million receivables from the U.S importer and convert it at the prevailing rate of 3.05 which results in MYR24,400,000. After deducting the option premium of MYR354,000 Ipoh Plantations will still make a profit of MYR446,000.

A good example of currency play will be sports car maker Porsche AG. In 2007 when the euro is strengthening against the dollar most European car makers like Jaguar, Volkswagen, Daimler Mercedes and the rest are either making a loss or plunge in profits due to the higher price of imported cars. However, Porsche managed to make about Euros 1.1 billion during this period. According to Goldman Sachs, about 75% of this profit is due to smart currency plays. It believed that Porsche entered into a call option contract to buy euros while the dollar is low. So when the euro subsequently appreciates in the coming months, Porsche make a hefty profit and at the same time its losses are capped at the price of the premium which ranges from 1.5 – 2%. Even though if the dollar appreciates, for a Euro 1 billion hedge Porsche’s losses only limited to Euros 15 – 20 million.

- Invoicing in Local Currency. This technique of hedging is lesser known among other hedging techniques. In our example instead of invoicing the American importer USD8 million why not invoice them MYR24 million based on the spot rate of MYR3.00/USD1.00. By doing so Ipoh Plantations did not eliminate the foreign exchange exposure but merely transfer the risk to the American importer. However such an arrangement is not always possible it might risk losing sales to other competitors. It can only be done if the product exported by Ipoh Plantations command near monopoly status where substitutes are hard to find. If this proved to be difficult then other arrangements such as risk sharing with the importer can be considered. Instead of billing the importer fully in MYR why not bill them half in MYR and the rest in USD.

- International Factoring. Factoring is a transaction whereby a business sells its invoices to a third party normally a factor at a discount. When the contract is signed the seller will be paid between 70-80% of the invoice value. The rest will be paid upon collection and will be net of the commission and other charges. Hence any foreign exchange exposure will also be absorbed by the factor company. If the USD depreciates against MYR then the factor will have to absorb the losses but if it appreciates then the factor will take the gain.

- Foreign Exchange Swaps. Foreign exchange swaps are like interest rate swaps because both are doing a ‘cash flow swap’. An example of interest rate swap will be the swapping of a flexible rate loan to a fixed interest rate loan. A foreign exchange swap is an agreement to swap one currency for another at a predetermined date. The swap period ranges from a few months to a few years making it very flexible. To initiate a swap between MYR and USD, Ipoh Plantations will have to deliver USD8 million at the end of the 90 day period to a counter party of the contract (normally a bank) in exchange for the MYR24 million. In this way Ipoh Plantations manage to eliminate any foreign exchange exposure derived from exchange rate fluctuations.

Despite the many innovations in Financial Engineering and new foreign exchange management tools being developed the traditional tools still remained the most used. The following table list the most commonly used Foreign Exchange Management (FEM) tools by Multinationals around the world.

Source : Andrew Marshall, Journal of Multinational Financial Mgnt

From the finding it is obvious that the most commonly used FEM tools are forward contracts followed by options and swaps. In other words these FEM tools will be here to stay and how and what tools a Treasurer will use to minimize his company’s currency exposure depends on his creativity and skills.

by Sam Chee Kong

cheekongsam@yahoo.com

© 2012 Copyright Sam Chee Kong - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.