Shiller PE Ratio Continues to Mislead Investors, S&P 500 Is Fairly Valued Early 2013

Companies / Corporate Earnings Jan 16, 2013 - 07:10 AM GMT

Allow me to start this article by emphatically stating that I have a real problem with forecasting stock markets in the general sense. Instead, I prefer to forecast the intrinsic values of individual businesses based on their earnings justified fundamental values. I hold this position because I believe that it is not only possible, but also quite practical to analyze a specific business and then make an intelligent forecast (not a guess) but a rational estimation, based on the assimilation of fundamental facts, as to its past, present and future intrinsic value. Importantly, I’m not suggesting this can be done with absolute perfect precision down to the precise penny, rather I am suggesting it can be done within a reasonable range of rational probabilities.

Allow me to start this article by emphatically stating that I have a real problem with forecasting stock markets in the general sense. Instead, I prefer to forecast the intrinsic values of individual businesses based on their earnings justified fundamental values. I hold this position because I believe that it is not only possible, but also quite practical to analyze a specific business and then make an intelligent forecast (not a guess) but a rational estimation, based on the assimilation of fundamental facts, as to its past, present and future intrinsic value. Importantly, I’m not suggesting this can be done with absolute perfect precision down to the precise penny, rather I am suggesting it can be done within a reasonable range of rational probabilities.

In contrast, trying to estimate the collective results of a large group of companies such as the S&P 500 (SPY) is a very daunting task. There are just too many variables and too many data points to contemplate from which to make a rational and/or reasonably accurate forecast. On the other hand, the evidence I’ve reviewed suggests that the earnings and price correlation and relationship is just as valid on an index, as it is on an individual stock. In other words, earnings will be the primary driver of stock price for both a specific company and an index.

With the above said, I have been periodically posting articles relating to the valuation of the S&P 500 based on the earnings and price correlated fundamentals analyzer software tool F.A.S.T. Graphs™. My rationale for engaging in an activity that I generally eschew is born of my desire to help people to being better informed investors. To my way of thinking, this means injecting more fact-based information into our analysis and less opinion. Facts provide information that can be quantified and evaluated. Opinions, on the other hand, are often emotionally-charged which can lead to irrational responses and behaviors. Therefore, I feel that the emotional response does not belong in something as important as making prudent investing decisions. Reason should dictate behavior rather than emotions such as fear or greed.

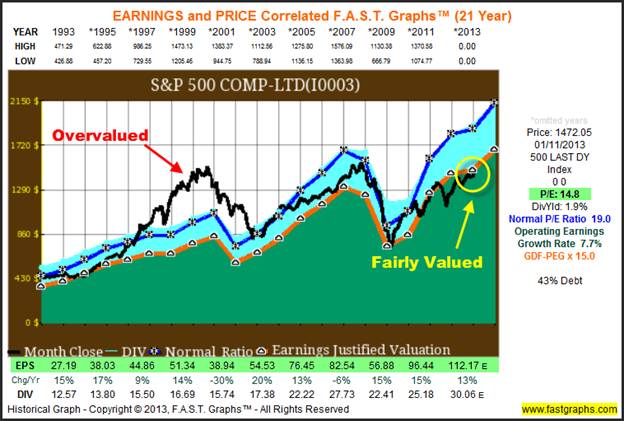

Allow me to try to clarify this a little more by presenting the current earnings and price correlated F.A.S.T. Graphs™ on the S&P 500 since calendar year 1993. The orange line on the graph plots earnings-per-share at the historical normal PE ratio of 15. The reader should note that the blue line on the graph represents a historically normal PE ratio of 19 over this time period. This simply indicates that for much of this time frame, that the S&P 500’s stock price was in overvalued territory. Importantly, notice how the stock price tracked the orange earnings justified valuation line, and that whenever it deviated away from the line it inevitably moves back towards alignment. Today, with a blended PE ratio of 14.8 the S&P 500 is reasonably valued. (Note: that because of the long duration of this graph, that only every other year is typed in, although data for all years is plotted).

At this point, it’s important to state that historical F.A.S.T. Graphs™ valuation measurements are based on actual S&P 500 operating earnings as reported, and estimated earnings (numbers marked with E for estimate) come directly from the Standard & Poor’s website. This is in contrast to the very popular statistical S&P 500 valuations based on the Shiller PE ratio calculation known as CAPE which utilizes earnings calculated as a 10-year average. If you carefully study the earnings and price correlating graph above, it is obvious that earnings for the S&P 500 (the orange line) have mostly advanced with the exception of the two recessions of 2001 and 2008.

This is important, because mathematically speaking the 10-year average of an advancing number will most often calculate earnings to be lower than they actually are. Of course, the exception would be when you’re calculating a 10-year average during a recessionary period when earnings have fallen. The point is that the only way that the Prof. Shiller statistical calculation can be correct is if future earnings fall. Again, an average of 10 years worth of increasing numbers will, mathematically speaking, always be lower than the current number. However, the problem is that as the graphic clearly indicates, earnings of the S&P 500 increase much more often than they fall. This clearly, at least, has been true for the last couple of decades.

This creates a problem for investors that I find appalling. For the great majority of the time, the Shiller calculated PE ratio will generally indicate that the market is overvalued. Consequently, investors who buy into this thesis will generally tend to avoid investing in stocks. Yet, if they were to calculate valuation based on actual numbers, they would more often than not find that stocks are fairly priced to even cheap, instead of overvalued. Therefore, they are often avoiding stocks at precisely times when the risk of investing in them is lowest, and simultaneously, when the rewards for owning them are highest.

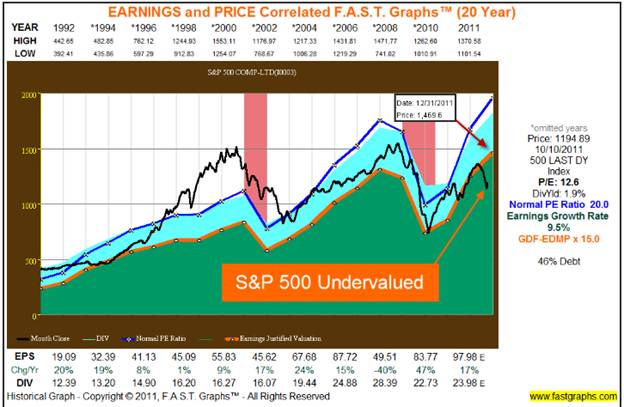

To further illustrate my point, here is an article published on 10/12/2011 where real earnings data indicated that the S&P 500 was cheap with a PE ratio of 12.6 based on the then estimated earnings for the S&P 500 for 2011 of $97.98. Actual 2011 earnings came in slightly lower at $96.44 (1.6% lower than originally estimated), but still represented a 15% advance over 2010. Consequently, the S&P 500 was still trading at a PE ratio below 13, and less than its historical normal PE of 15. Unfortunately, the Shiller PE for the S&P 500 was at 20.15. Since anything over 16 is considered expensive, CAPE was declaring that the S&P 500 was overvalued, not undervalued.

The following earnings and price correlated graph shows the S&P 500 at a price of 1194.89 on October 10, 2011. As of this writing, the S&P 500 is priced at 1472.05 or approximately 23% higher than it was in October of 2011. Therefore, investors believing in the Shiller statistical PE missed out on a great buying opportunity.

In the spirit of accountability, the following are links to several other similar articles to this one, utilizing the actual PE of the S&P 500 based on real earnings and the near estimate of future earnings. For perspective, I’ve reported the date the article was published and the respective Shiller PE ratio on that date. Once again remember that according to Prof. Shiller, his statistically calculated PE ratio has to be approximately 16 or lower for fair value to exist. All of the following examples show that the Prof. Shiller CAPE (Cyclically Adjusted PE) would have caused investors to avoid investing in equities when the opportunities in doing so were high, and the risks based on valuation low.

When this article was written on January 6, 2010, the Shiller S&P 500 PE was 20.52 indicating overvaluation. The F.A.S.T. Graphs™ calculated PE on actual earnings of 19.1 agreed.

However, by February 21, 2010 when I published this next article the Shiller S&P 500 PE was 19.91 still indicating overvaluation. However, it is interesting to note that earnings forecasts for both 2008 and 2009 ended up being lower than the actual results.

Then on November 2, 2010, I published an update suggesting that the S&P 500 should reach 1254 by year-end based on estimated earnings, the Shiller S&P 500 PE was 21.69 continuing to say that the market was overvalued.

When I published the next article on December 23, 2010 the Shiller S&P 500 PE of 22.39 was still indicating overvaluation. But as actual earnings were higher, the S&P 500 target of 1254 was reached.

By January 9, 2011, I published this article when the Shiller S&P 500 PE 22.97 continued to suggest overvaluation even though the Index continued to make above-average returns for those investors with the foresight to focus on actual earnings rather than a statistical representation.

When I published an article on April 7, 2011 the Shiller S&P 500 PE of 23.05 continued to relentlessly suggest overvaluation. Nevertheless, the market has advanced approximately another 10%, from 1333 to 1472, since that time. Yet all of the gains were achieved during times when the Shiller PE was suggesting that stocks were overvalued.

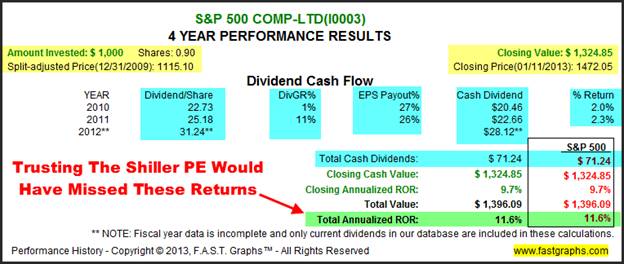

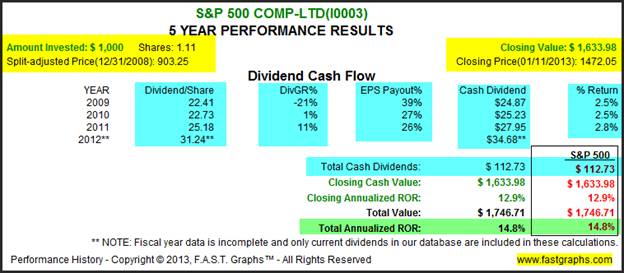

Since the beginning of 2010 when the first article I cited above on the valuation of the S&P 500 was published, the S&P 500 has produced a compounded annualized rate of return of 11.6% (including dividends), while all the while, the Shiller PE was screaming overvaluation. In contrast, the valuation based on the actual earnings of the S&P 500 suggested reasonable valuation. The following performance results since December 31, 2009 illustrate what investors, afraid of owning common stocks, missed out on.

This is why I prefer decisions based on facts over decisions based on artificial constructs and mere statistical representations such as CAPE. Perhaps if you keep yelling that the sky is falling long enough, it may one day occur. However, where I sit, it appears that that may be a long way off. Therefore, I much prefer serious analysis based on the facts that I do some hypothetical estimation based on what can be very misleading statistics.

A Fair and Balanced View

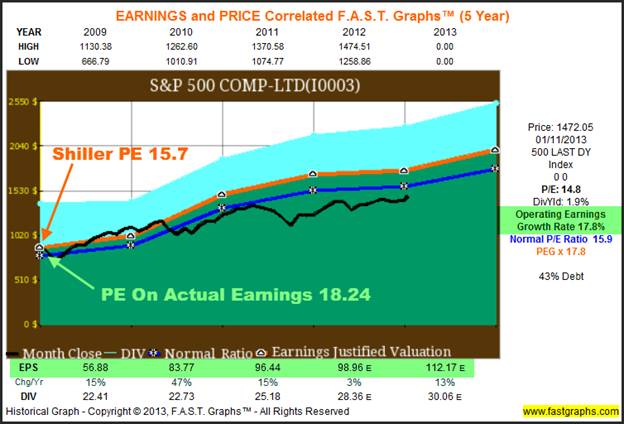

However, and in order to be fair and balanced with this article, the following F.A.S.T. Graphs™ looks at the S&P 500 since January 1, 2009 when the Shiller PE ratio was at 15.17 indicating undervaluation. From this picture, it is clear that both real operating earnings and the CAPE (Shiller’s Cyclically Adjusted PE) both indicated fair value. However, it’s important to recognize that this was a time when the S&P 500’s earnings had actually fallen from $87.72 in calendar year 2006 to $49.51 by 2008. In other words, the Shiller CAPE was accurate because it was measured at a time when S&P 500 earnings had fallen for two consecutive years in a row, and just prior to strong S&P 500 accelerating earnings growth coming off of the low base.

Consequently, the S&P 500 performance when the Shiller PE ratio was at 15.17, indicating a solid buy, was exceptional. However, it was also during a time when the S&P 500 was moderately overvalued based on actual earnings, and just prior to the strong earnings advance previously mentioned and illustrated.

A Few Words About Specifics Versus Generalities

As I indicated in my opening remarks, I prefer analyzing individual companies over attempting to forecast the earnings of a broad market like the S&P 500. One of my primary reasons for believing this is that my research has suggested that in every market, whether bull or bear, there can always be found overpriced, underpriced or fairly priced individual selections among the group. Therefore, I believe in making specific decisions rather than general ones.

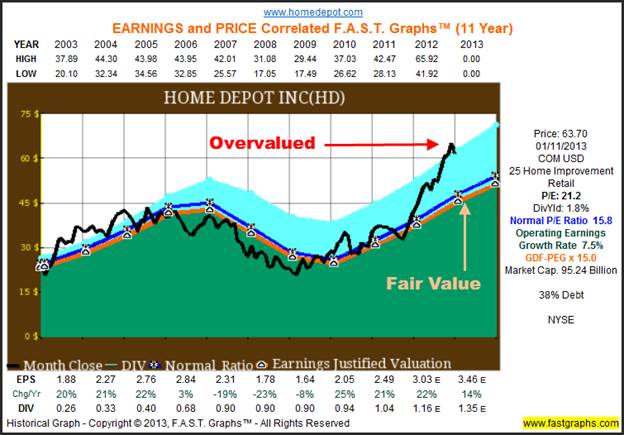

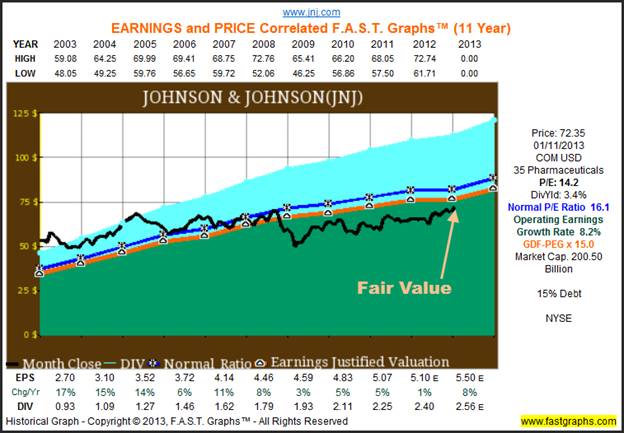

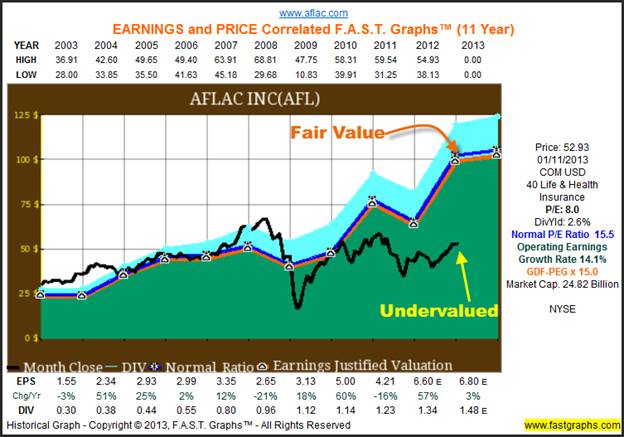

Since a picture is worth 1000 words, I am going to present earnings and price correlated graphs on the following three well-known S&P 500 stocks to illustrate my point. I will let the graphs speak for themselves and offer only this brief explanation. When the price is above the orange earnings justified valuation line, the stock is overvalued, when below the line, undervalued, and when on the line (or very close to it), fairly valued. Therefore, I offer Home Depot (HD) as an overvalued S&P 500 company, Johnson & Johnson (JNJ) as a fairly valued example, and finally Aflac (AFL) as an undervalued company.

Summary

With a blended PE ratio of 15, I believe the S&P 500 is fairly valued based on real current and near forecast earnings. My optimism rests on the idea that the world economy is improving coming out of the great recession, and that we will soon see significant productivity enhancements as the deployment phase of the information revolution comes into high gear. Moreover, I believe that high-profile blue-chip publicly-traded US companies are well-positioned for profitable long-term growth. The great recession of 2008 forced many of them to take long hard looks at their balance sheets and P&L’s. As a result, I believe corporate America is leaner and meaner, so to speak, than they have been in a long time. Consequently, productivity enhancements should feed their bottom lines.

In their October 5, 2012 edition, Trends Magazine published an article titled “The Truth About Stocks.” A few select excerpts from the article both summarize and highlight my optimistic views:

On the Market’s Long-term Record

“Since 1912, the inflation-adjusted total return for investments in common stocks has averaged 6.6 percent per year, compounded. That’s 100 years of solid performance despite numerous surges and crashes.

Any way you slice it, it’s an impressive record.

But, after more than 12 years of minimal price appreciation and weak dividend performance, many investors find themselves asking the question, “Will we ever see 6.6 percent average annual returns again?”

On Future Earnings Growth

“As soon as 2014, we’ll begin to see rapid economic growth return; the exact timing will depend on policy factors that are hard to predict. Houses will begin to move, demand for autos will grow, and sales will pick up in retail stores. As a result, corporate profits will grow at a renewed pace, which will drive up stock prices. As long as long-term interest rates move up, improved investor confidence will eliminate much of the pervasive “worry deficit” that’s held down “relative P/E ratios” for a decade. Another factor contributing to equity returns will be demographics: Domestically, solid birth rates plus immigration will create demand for more goods and services. Although it’s true that Europe and Japan will remain stagnant due in large measure to aging and declining populations, this will be more than offset by The $30 Trillion-a-Year Opportunity of 2025 discussed later in this issue.”

On the Sources of Growth

“Second, in the coming decade, total returns on stocks should actually exceed historic norms, as the Deployment phase of the global Information Revolution takes off.

This phase will drive the biggest boom in world history, providing the “productivity miracle” Bill Gross could evidently not imagine happening. This boom will materialize for a number of reasons. Here are a few:

This is the first time that over 5 billion people living in the developed world will take part in this type of revolution; previous revolutions have been limited to the developed world.

New technologies will make low-cost energy available in enormous quantities.

The combination of infotech, biotech and nanotech will dramatically increase the amount of GDP that can be produced per unit of matter and energy, eliminating much of the traditional drag created by resource shortages.

Increasingly, the most valuable resource will become information, which can be made available to almost anyone, anywhere, at any time for free once it is created. “

The bottom line to my thesis is that I expect future earnings of the S&P 500 to be higher than they are today, not lower, as the Shiller PE would want you to believe. On an absolute basis, in other words, on actual current earnings, I believe the S&P 500 is fairly priced. In my experience, when the markets in general are fairly priced, it is easier to find fairly priced individual selections than it would be if the market were truly overvalued. Furthermore, like all markets there are overpriced stocks in the general market, I shared an example with Home Depot above. Nevertheless, there is plenty of value to be found for the discerning investor willing to dig deep enough.

Conclusions

I believe there is no substitute for making intelligent decisions based on factual information. Having an intelligent framework with which to make investing decisions can eliminate mistakes that are too often made when emotion is overtaking reason. Within this process, I believe it’s important to recognize that over the vast majority of the time, positives outweigh negative. Therefore, it’s important to realize that negative economic cycles such as recessions only come rarely, and usually end rather quickly. So, I suggest that instead of being traumatized and frightened away, it’s worth considering that the best times to be looking at equities is when times are tough. Because, it is during these times when great businesses go on sale.

Disclosure: Long HD, JNJ and AFL.

By Chuck Carnevale

Charles (Chuck) C. Carnevale is the creator of F.A.S.T. Graphs™. Chuck is also co-founder of an investment management firm. He has been working in the securities industry since 1970: he has been a partner with a private NYSE member firm, the President of a NASD firm, Vice President and Regional Marketing Director for a major AMEX listed company, and an Associate Vice President and Investment Consulting Services Coordinator for a major NYSE member firm.

Prior to forming his own investment firm, he was a partner in a 30-year-old established registered investment advisory in Tampa, Florida. Chuck holds a Bachelor of Science in Economics and Finance from the University of Tampa. Chuck is a sought-after public speaker who is very passionate about spreading the critical message of prudence in money management. Chuck is a Veteran of the Vietnam War and was awarded both the Bronze Star and the Vietnam Honor Medal.

© 2013 Copyright Charles (Chuck) C. Carnevale - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Chuck Carnevale Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.