Words from the Investment Wise for the Week that Was (23rd March)-Part2

Stock-Markets / Financial Markets Mar 23, 2008 - 05:56 AM GMT

Continued from Part 1

Ambrose Evans-Pritchard (Telegraph): Foreign investors veto Fed rescue

“As feared, foreign bond holders have begun to exercise a collective vote of no confidence in the devaluation policies of the US government. The Federal Reserve faces a potential veto of its rescue measures.

“Asian, Mid East and European investors stood aside at last week's auction of 10-year US Treasury notes. ‘It was a disaster,' said Ray Attrill from 4castweb. ‘We may be close to the point where the uglier consequences of benign neglect towards the currency are revealed.'

“The share of foreign buyers (‘indirect bidders') plummeted to 5.8%, from an average 25% over the last eight weeks. On the Richter Scale of unfolding dramas, this matches the death of Bear Stearns.

“Rightly or wrongly, a view has taken hold that Washington is cynically debasing the coinage, hoping to export its day of reckoning through beggar-thy-neighbour policies. It is not my view. I believe the forces of debt deflation now engulfing America – and soon half the world – are so powerful that nobody will be worrying about inflation a year hence.

“Yes, the Fed caused this mess by setting the price of credit too low for too long, feeding the cancer of debt dependency. But we are in the eye of the storm now. This is not a time for priggery. With the ‘financial accelerator' kicking into top gear – downwards – we may need everything that Ben Bernanke can offer.”

Source: Ambrose Evans-Pritchard, Telegraph , March 17, 2008.

The New York Times: The “B” Word

“OK, here it comes: The unthinkable is about to become the inevitable. Let's talk about why a bailout is inevitable.

“The US savings and loan crisis of the 1980s ended up costing taxpayers 3.2 % of GDP, the equivalent of $450 billion today. Some estimates put the fiscal cost of Japan's post-bubble cleanup at more than 20 % of GDP – the equivalent of $3 trillion for the United States.

“If these numbers shock you, they should. But the big bailout is coming. The only question is how well it will be managed.”

Source: Paul Krugman, The New York Times , March 17, 2008.

Paul Craig Roberts (321gold): US inflation twice as high as government's figures

“Today the US, heavily dependent on imports, is subject to double-barrel inflation from both domestic money creation and decline in the dollar's foreign exchange value.

“The US inflation rate is about twice as high as the government's inflation measures report. In order to hold down Social Security payments, the government changed the way it measures inflation. In the old measure, inflation measured the nominal cost of a defined standard of living. If the price of steak rose, up went the inflation rate. Today if the price of steak rises, the government assumes that people switch to hamburger. Inflation doesn't go up. Instead, the standard of living it measures goes down.

“This is just one of the many ways that the government pulls the wool over our eyes.”

Source: Paul Craig Roberts, 321Gold , March 17, 2008.

Paul Kedrosky (Infectious Greed): Alan Greenspan loses his mind

“Judging by a just-released Washington Post interview , ex-Fed chair Alan Greenspan has gone mad.

“Here is Alan, talking in an interview about how misguided his critics are for suggesting that the recently-ended real estate bubble had its roots in the post dot-com bubble low rates. Implicit in this, of course, is that he should have increased rates sooner to arrest the real estate bubble's expansion:

“‘Those who argue that you can incrementally increase interest rates to defuse bubbles ought to try it some time.'

“Well, there's no denying you can't get any evidence on the matter from Greenspan's career: He avoided raising rates during both bubbles with which he was faced.

“And Greenspan continues, offering the following:

“‘If it weren't the subprime crisis it would have been something else,' he said. That is because an era was ending that had seen ‘disinflationary forces' from developing countries such as China and a ‘protracted period' in which there was an ‘underpricing of risk'.

“Really? Really? Greenspan's Fed didn't prick the real estate bubble because it was saving us from another bubble, whatever it was, that would have been worse? What was it? A lava dome under Los Angeles? Sewer gas under New York? Something else? Because it's really hard to imagine what would have been worse than the real estate bubble, but maybe I lack imagination.

“But the tricksy Mr. Greenspan doesn't stop there. Having first said that raising rates doesn't prick asset bubbles, and then sneaking around the side of the issue by arguing that another bubble would have formed anyway, he then spun about and said the following:

“Even after the Fed starting raising short-term rates, long-term rates did not rise. He said that at the time ‘it became apparent that we lost control' of long-term interest rates ‘as did the Bank of England and all the central banks. As a consequence, we had very little ability to put a brake on the rise in home prices'.

“Oooh, awesomely argued Alan. In short, even if you had raised rates — which you wouldn't have, because the Fed can't prick bubbles, and because another worse (unnamed) bubble would have happened anyway – nothing would have happened, because the Fed lost control of long-term rates. You were totally boxed, and anyone who criticizes you is a clueless nitwit for not seeing that.

“Does anyone buy that? I know I don't. Greenspan ably demonstrated that he would cut rates in the face of falling asset prices, so why so skittish about raising them in the face of rapid asset price increases? Something doesn't work in that illogic.

“Then again, what does Greenspan care. He has built a career out of this sort of thing, of dancing around clumsy questioners' questions, and this is easy stuff for a skilled obfuscator. Greenspan's minting money as a hedge fund advisor, speaker, and author, and likely giggling every day at the mess that he left on Ben Bernanke's desk.”

Source: Paul Kedrosky, Infectious Greed , March 21, 2008.

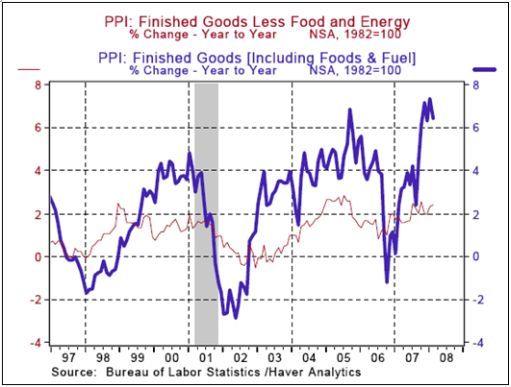

Asha Bangalore (Northern Trust): Wholesale prices continue to advance

“On a year-to-year basis, the PPI for finished goods is up 6.4%, marking the fifth monthly reading that exceeds 6.0%. Energy prices have advanced 19.6% and food prices have risen 6.0% during past twelve months.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary , March 18, 2008.

Asha Bangalore (Northern Trust): Housing Starts post largest cyclical decline on record

“Construction of new homes declined 0.6% to an annual rate of 1.065 million units in February. Starts of homes have now fallen 53.5% from the peak reading of 2.292 million in January 2006. There should be additional declines in the months ahead because the bottom of the housing market crisis is not here yet.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary , March 18, 2008.

Financial Times: Fannie, Freddie to boost mortgage market

“Fannie Mae and Freddie Mac, the government-chartered mortgage financiers, yesterday got the go-ahead from their regulator to pump as much as $200 billion of liquidity into the beleaguered US mortgage market.

“The Office of Federal Housing Enterprise Oversight (Ofheo) reduced surplus regulatory capital requirements for the mortgage companies from 30% to 20% and secured a commitment that they would each soon raise a ‘significant' amount of new capital to allow them to buy and guarantee more mortgages.

“Ofheo said the move was a bid to give Fannie and Freddie the flexibility to support the highly distressed market for so-called ‘jumbo' mortgages greater than $417,000, as well as the capacity to refinance more subprime home loans and conduct loan modifications for struggling borrowers.

“Henry Paulson, US Treasury secretary, said the decision was ‘encouraging' and should provide a boost for the mortgage market.

“But some analysts doubted the new flexibility for the agencies would go far enough. Josh Rosner, consultant at Graham Fisher, said: ‘This will make a psychological difference in the short term, but the agencies are not going to be very aggressive – they have become very risk averse from a credit perspective.'

“Dan Alpert, managing partner of Westwood Capital, an investment bank, said: ‘Washington believes this is a liquidity crisis. But this is a credit crisis brought on by the falling value of underlying housing assets.'”

Source: Saskia Scholtes, Financial Times , March 19, 2008.

The Wall Street Journal: Lehman finds itself in center of a storm

Source: Susanne Craig, The Wall Street Journal , March 18, 2008.

Bloomberg: HBOS has “ready access” to funding

“HBOS, Britain's biggest mortgage lender, declined to its lowest-ever price in London trading even after saying it has ‘ready access' to funding.

“‘There are no liquidity problems,' HBOS spokesman Shane O'Riordain said in an interview today after the shares initially fell 17%. ‘We have ready access to a deep pool of deposits. We can access the wholesale markets whenever we feel appropriate to do so.'

“Edinburgh-based HBOS recovered to close down 7.1% at 446.25 pence, the lowest level since it began trading in September 2001. HBOS has fallen 32% in the past three weeks on concern it may face writedowns and higher inter-bank lending costs.

“HBOS is ‘reliant on wholesale funding, and from their most recent reports, we saw the bank wasn't just under pressure from a balance-sheet perspective, but also from a funding point of view,' said Graham Neale, head of equities at Killik & Co. in London. ‘It's clearly at risk' should funding spreads widen or money-market borrowing costs rise, he said.”

Source: Jon Menon and Ben Livesey, Bloomberg , March 19, 2008.

Times Online: How UBS got bitten by betting

“Dear UBS shareholder, We Swiss are thorough. Our 2007 annual report stretches to a mammoth 464 pages in four separate documents. After translating from German, the text can be a bit hard going. Wrestling with fondue would be easier. In the interests of brevity, therefore, I have summarised the main points below.

1. In a matter of months we have managed to turn our investment banking arm, built out of the old SG Warburg, once the greatest merchant bank in Europe, into the laughing stock of the securities industry. Losses from mortgage-backed securities by our in-house traders have reached $18 billion and led to our first full-year loss, and there could be more pain to come. Our lawyers won't let us apologise in print in case that brings a volley of lawsuits, but we really are terribly regretful.

2. We know what went wrong. The UBS name and balance sheet was so strong that we were able to borrow laughably cheaply in the benign markets prevailing before last summer. That meant all ki999nds of leveraged bets looked attractive. Our biggest competitors seemed to be making lots of money in US mortgage-backed securities, so we piled in, too. It worked so well initially that we doubled up, creating an in-house hedge fund to take even bigger bets. Our stress-testing was inadequate: we failed to make pessimistic enough assumptions about what could go wrong.

3. We've put in place reforms to prevent anything similar happening again. Trading activities will be financed at rates prevailing in the wider market, rather than at the cheapo rates achievable by UBS. We're going back to the basics of looking after clients and partly pulling out of proprietary trading. Our risk-management experts have been given a kick up the backside and told to imagine a wider range of outcomes when stress-testing particular investment positions. And we have strengthened our balance sheet, courtesy of a capital injection from the Singaporeans and an anonymous friend from the Middle East.

4. Even at 464 pages, there, er, wasn't room to apportion individual blame for this fiasco. Both I and my new chief executive, Marcel Rohner, have forgone any bonus and my total pay is down 90% to $2.6 million. By contrast, three ousted executives have walked away with $90 million. Rewards for failure? I couldn't possibly comment.

“Yours sincerely, Marcel Ospel, Chairman.”

Source: Patrick Hosking, Times Online , March 19, 2008.

Jeffrey Saut (Raymond James): Markets offer opportunity and danger

“As for the equity markets, they are clearly involved in a ‘selling panic' … However, for the well prepared investor this kind of volatility affords opportunity. Remember, the Japanese kanji symbol for the word ‘crisis' consists of two characters. One of them represents ‘danger', the other ‘opportunity'.”

Source: Jeffrey Saut, Raymond James , March 17, 2008.

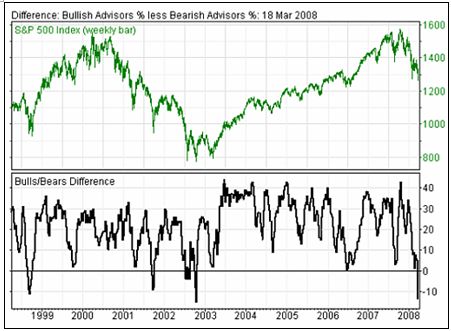

Mike Burke & John Gray (IIAS): Bearish sentiment pointing to buy signal

“Advisors continued to express new pessimism regarding the market, and the bulls fell further to 30.9% this week. That extends last week's dramatic drop to 31.1%, from the previous reading at 41.3%.

“There were also more bears at 44.7%, up from 43.3% and 36.2% the prior two weeks. The bears remain well above the level of the bulls.

“The advisors calling for a correction were 24.4%, down from 25.6% a week ago. This group is short term bearish but longer term bullish and wish to buy on weakness.

“The sentiment reading for the last two weeks are very positive for long term markets gains. The means we expect substantially higher index levels a year from now. To find comparable sentiment levels you have to look back to October 2002. That was the last time we had fewer bulls, with reading at 28.4% on October 11, 2002 and 31.0% the week before that. October 2002 was the middle of the bear market bottom that extended from that July through March 2003.”

Source: Mike Burke & John Gray, Investors Intelligence Advisors Sentiment , March 19, 2008.

David Fuller (Fullermoney): Stock market already discounts bearish news

“Just as a crescendo of bearish news stories tell us that the media is feeding on known fears, stock market action tells us the extent to which it has already been discounted. … consensus expectations are always worst at the bottom of the trend, not least because at that stage of the cycle everyone knows why the market fell; they have had ample time to sell; bear traders are talking their book, and potential buyers are hoping for even better bargains. The same process works in reverse near market peaks.

“Today's Advisors Sentiment readings from Investors Intelligence tell us that Wall Street has either seen its lows or is quite close to them. There is a possibility that this could be wrong, in that we live in an uncertain world and no signal comes with a money back guarantee. However, if it were to be proved wrong, I suspect it would be due to factors that few people are talking about today. Meanwhile, II's Advisors Sentiment Indicator has an enviable track record at market bottoms.

“The main uncertainty, as far as I am concerned, is the length of convalescence time required before meaningful gains are seen. I suspect it could vary considerably from sector to sector.”

Source: David Fuller, Fullermoney , March 19, 2008.

John Authers (Financial Times): Bear market rally?

“It has been a terrible week. Can the stock market now indulge in a brief bear market rally?

Wednesday's Merrill Lynch survey of fund managers made clear that the preconditions are in place. More global fund managers are overweight in cash, compared to their benchmarks, than at any time since the survey started in 1998. Fund managers also believe that equities are undervalued by the biggest margin since the bear market bottomed in 2003, and that bonds are overvalued.

“So, there is a lot of cash on the sidelines, in the hands of managers who believe stocks are cheap, and the end of the quarter is close. Many may want to use that cash to buy stocks before the quarter is up.

“There is another reason to expect a rally: the bounce from Monday's panic levels, as traders realised that Wall Street's banks were not about to collapse one after another, has led to a rash of predictions that the bottom has been hit.

“There are also hopes that the authorities have at last found a ‘silver bullet' to end the crisis. False hopes have been invested in several other putative silver bullets, but the news that Fannie Mae and Freddie Mac, the powerful US mortgage agencies, will be allowed to buy more mortgage-backed securities is as good a candidate as any.

“Does a bear market rally need a catalyst? Not necessarily. Tuesday's surge was triggered by terrible results from two investment banks. Given how negative sentiment had become, the mere fact that they were not epochally disastrous was enough to trigger a rally. In the short term, the mere absence of bad news (which is not a given) might allow the markets to enjoy a bounce.”

Source: John Authers, Financial Times , March 19, 2008.

Richard Russell (Dow Theory Letters): Are stock markets at lows?

“Now check this out – today both the Dow and the Transports were trading well ABOVE their January lows. What, after all this horrendous news those two are still above their January lows? Makes me wonder if Bennie and the Feds could be winning the game.

“It's really remarkable to note how many millions of words are being written about the ‘awful economy' and the ‘recession', but it's also remarkable how little is being written about the market's reaction to all the negative news. And from an investment standpoint, of course, what we're interested in is not the news of the day – no, what we're interested in is the market's reaction to the news. Right now it seems that the analysts and the newspapers are so transfixed by the depressing news of the day that they fail to note the stock market's action.”

Source: Richard Russell, Dow Theory Letters , March 18, 2008.

GaveKal: Fed and tape point to stock market rally

“In recent weeks, we have seen two of the oldest Wall Street adages – namely ‘don't fight the Fed' and ‘don't fight the tape' – in an open clash. And just as it looked like ‘don't fight the tape' was about to win, the Fed took out the heavy artillery and a) slashed rates further (-75bp yesterday) and b) announced a new policy whereby all non-junk-rated paper could be deposited at the Fed.

“We are now in a situation where both the Fed and the tape are pointing in the same direction. This should mean that, if nothing else, the markets rally hard over the coming weeks.”

Source: GaveKal – Checking the Boxes , March 19, 2008.

Bloomberg: Barton Biggs expects 1,000-point gain in Dow

“The decline in US stocks is ‘way overdone' and the Dow Jones Industrial Average may rally 1,000 points, investor Barton Biggs said.

“‘We're in a financial panic,' Biggs said during a telephone interview with Bloomberg Television from New York. ‘We're setting up for a really big rally. I don't mean three or four hundred points on the Dow, I mean 1,000 points on the Dow. I don't know if we're going to get it next week or the week after. But this thing has gotten crazy and is overdone.'

“Biggs, a former Morgan Stanley strategist who now runs the $1.5 billion hedge fund Traxis Partners LLC, said stock markets from Germany to Hong Kong may bottom out soon after tumbling this year.

“‘We're at a really crucial point,' Biggs said. ‘This is a time to be buying stocks around the world and not to be selling them. Yeah, it's scary. It's always scary at bottoms. But I don't believe the economy is collapsing,' Biggs said. ‘This is not the end of the world.'”

Source: Brian Sullivan and Michael Patterson, Bloomberg , March 14, 2008.

Bill King (The King Report): Merrill's Rosenberg – We're a long way from a stock market bottom

“We're a long way from a bottom. The sentiment is way too bullish and the calls for a bottom or to do bargain hunting are far too pervasive and far outnumber the calls for capital preservation.

“… [from] David Rosenberg's (Merrill Lynch) latest research piece: There is a legitimate case to be made that as bad as things are, we may only be at the halfway point of this bear market in equities in general and consumer cyclicals in particular …

“Mr. Rosenberg echoes our view that few people on the Street have experienced a credit cycle turn or a vicious recession. The problem is that so many of the economists that are calling for a recession believe it will be mild. We are not sure why, except that many Wall Street pundits have lived through at most two downturns, and indeed, the last two recessions (2001 and 1990 to 1991) were mild by historical standards, both in terms of magnitude (a peak-to-trough 1.3% decline in real GDP for the former and -0.4% for the latter) and duration (both lasted just eight months). The models that economists use may be skewed by undue reliance on the experience of the last two recessions.

“David also asserts, ‘monetary policy alone will not solve the problem; current backdrop has more in common with 1973-75 cycle.'”

Source: Bill King, The King Report , March 19, 2008 and The Wall Street Journal , March 20, 2008.

Reuters: US dollars tough to sell

“The US dollar's value is dropping so fast against the euro that small currency outlets in Amsterdam are turning away tourists seeking to sell their dollars for local money while on vacation in the Netherlands.

“‘Our dollar is worth maybe zero over here,' said Mary Kelly, an American tourist from Indianapolis, Indiana, in front of the Anne Frank house. ‘It's hard to find a place to exchange. We have to go downtown, to the central station or post office.'

“That's because the smaller currency exchanges – despite buy/sell spreads that make it easier for them to make money by exchanging small amounts of currency – don't want to be caught holding dollars that could be worth less by the time they can sell them.”

Source: Svebor Kranjc, Reuters , March 18, 2008.

Times Online: US dollar tumble spells trouble for yen carry trade

“Deepening misery on Wall Street, prophesies of recession and the recent freefall of the dollar could set off a $300 billion time bomb in the global yen carry trade, dealers are giving warning.

“The carry trade, which involves cheaply borrowing the Japanese currency to buy other assets, comes unstuck in volatile currency markets. If the carry trade does implode, sending the yen to new heights against a wide basket of currencies, dealers say that the cast of victims could include individuals, corporates and hedge funds.

“The yen is at a 12-year high against the greenback and Tokyo-based economists are speculating that a severe crash in the carry trade could trigger a more devastating ruction in the $1 trillion overseas investments of Japanese mutual funds as the dollar/yen exchange rate edges towards the pain threshold of individual investors.

“Hedge funds have long used the carry trade for cheap leverage, but there are also thought to be vast exposures to yen volatility in the Thai, Korean and Indonesian banking sectors, where the Japanese currency has been borrowed heavily to meet funding needs. Because the trade has been so popular, Goldman Sachs analysts said yesterday that the sharp fall in the US dollar against the yen had prompted them to reassess the ‘cash-call risks' for Asian banks and corporates.

“But the practice is also uniquely sensitive to general global risk appetites: when investors batten down the hatches, as they have done in the wake of the Bear Stearns collapse, the carry trade unwinds, often spectacularly.

“It was advanced fear of that unwind, currency analysts at Mitsubishi Tokyo UFJ said, that has caused so much volatility over the past few days in the so-called yen cross-trades - where the low Japanese lending rate is exploited to buy high-yield currencies such as the New Zealand dollar, the South African rand, the Mexican peso and the Icelandic krone. Sudden spikes in the yen against the Australian dollar, euro and sterling, Nomura dealers said, indicated a first wave of fleeing from carry trades as risk appetites collapse.”

Source: Leo Lewis, Times Online , March 19, 2008.

Daisaku Ueno (Nomura): Yen intervention on the cards?

“The sharp strengthening of the yen has prompted talk of intervention by the Japanese authorities to stem the currency's advance, says Daisaku Ueno, senior economist at Nomura.

“Mr Ueno sees only a limited likelihood of Japan intervening on its own, as neither the Japanese government nor the Bank of Japan has adopted policies aimed at stimulating the economy. He adds that any impact from selling the yen to buy the dollar would likely be short-lived as long as the US continues to cut interest rates while Japan holds its rates steady.

“But he says the possibility remains of a co-ordinated international response if the dollar's weakness intensifies. ‘The recent acceleration in the dollar's decline has lifted US inflation expectations, raising concerns of reduced leeway for US monetary policy,' he says.

“‘If the dollar were to weaken further, we think attention would increasingly focus on co-ordination of monetary policy as well as whether the dollar appears headed for a steady recovery.'”

Source: Daisaku Ueno, Nomura (via Financial Times ), March 19, 2008.

Richard Russell (Dow Theory Letters): Ride the gold bull

“What would be the reaction of the world's central banks be to deflation or even a slowdown? My guess is that they'll fight those trends tooth and nail. They'll fight it by creating more fiat money. You remember my old adage, my old warning – ‘INFLATE or DIE'. I think that's where we're heading or maybe where we are.

“How will this affect gold? It should put bearish short-term pressure on gold and bullish long-term pressure on gold. Gold's first reaction to deflation? We're seeing it now, and the direction is down (besides, gold was technically overbought anyway). Gold's later reaction to central bank massive creation of paper – upward pressure on gold.

“I've been a bull on gold ever since 1999, and I've never tried to time the moves. My theme song has been: ‘Ride the gold bull and don't let it buck you off', and so far that's been the way to go. I've always maintained that the hardest thing to do in this business is to get into a bull market early, stay with that bull market, and ride it to somewhere near its final top.

“I don't believe we've seen the phase of frantic global gold-buying yet. That phase, I'm convinced, lies ahead. The gold bull market should wind up with some eye-opening fireworks. It should end up in a state of speculative fever. Or as my old-timer subscribers remember, ‘There's no fever like gold fever.' Believe me, we haven't seen the gold-fever yet – at least not during this bull market.”

Source: Richard Russell, Dow Theory Letters , March 18 & 20, 2008.

MarketWatch: $2,000 an ounce gold is in the cards

“Frank Holmes, chief executive officer at US Global Investors, says that gold will hit $2,000 an ounce and that while the move won't be straight there from current levels investors should not be surprised by it.

“Holmes noted that virtually all commodities have gone through their ‘inflation-adjusted 1980 price levels', with the notable exception of gold, and that to get to that range the price of gold would have to top $2,000 an ounce. Holmes said he expects a short-term pull-back in gold – based on a correction he sees coming in oil and a short rally in the dollar, both of which will impact gold prices – but that the long-term trend will be strongly upward.

“In a radio interview with Chuck Jaffe, MarketWatch senior columnist, Holmes noted that gold correlates to the price of oil 90% of the time – meaning it moves with oil prices almost all the time – and has an inverse relation to the dollar 70% of the time. With oil prices on the rise and the dollar weakening, it's a market condition that bodes well for gold, especially because gold is ‘not at astronomical levels yet, when compared to other commodities … There's a lot more room.'

“Holmes also noted that he's more concerned with the market entering a ‘big deflationary cycle' than he is about Federal Reserve rate cuts sparking inflation, noting that ‘inflation is easy to stop'.

“Holmes recommended that investors looking for a plan to follow through the current whipsaw conditions should take a long-term approach that divides a portfolio as follows: 25% in international investments, 25% in resources, 25% in domestic stocks and 25% in high-income and dividend-paying stocks.”

Source: MarketWatch , March 18, 2008.

David Fuller & Eoin Treacy (Fullermoney): Commodities susceptible to medium-term corrections

“Commodity price headlines again today but this time for not maintaining record highs. I do not think that it has much to do with a global slowdown, which is mainly in the west. However I do think deleveraging is a big factor. A number of the better hedge funds with a global brief have done very well in commodities, as have many individual investors who have profited from commodities …

“To risk a brave contrarian call today, I think many commodities, great secular theme that they undoubtedly are, have run ahead too quickly during the frenzy to buy the one sector with upside momentum. Those that have accelerated the most are increasingly susceptible to medium-term corrections, which I would describe as anything from a few months to two years.

“Undeniably, billions have flowed into commodities over the last few months, but given recent action, at least some of that money is being taken off the table. Additionally, the US dollar is looking quite oversold and ripe for a technical rally. This could encourage investors to go elsewhere in search of returns.”

Source: David Fuller & Eoin Treacy, Fullermoney , March 17 & 19, 2008.

Richard Russell (Dow Theory Letters): Commodities topping out?

“One very negative development that I see is the potential topping out of commodities and materials. This provides early hints of a world slowdown in commerce and activity. Below we see a daily chart of Dr. Copper, long considered a barometer of global activity, since copper is used worldwide in almost everything that's manufactured. Note the rolling over of MACD on the chart below. Copper could be topping out. If so, that's not good, not good at all.”

Source: Richard Russell, Dow Theory Letters , March 19, 2008.

John Hussman (Hussman Funds): Cyclicality in commodity prices to remain

“… the main downside risk for commodities is likely to emerge after the year-over-year CPI inflation rate falls below 10-year Treasury bond yields. We are not at that point, so my impression is that further weakness in the dollar will help to sustain commodity prices despite growing evidence of a recession (which we view as baked-in-the-cake).

“Still, it is again important to emphasize that commodity prices are cyclical, and there is no reason to believe that this has changed despite demand from China and other developing countries. We may observe higher levels of commodity prices in the years ahead, but cyclicality – the tendency for commodities to experience parabolic advances followed by precipitous drops – is likely to remain a feature of these markets.”

Source: John Hussman, Hussman Funds , March 17, 2008.

Bill King (The King Report): Chinese behind commodity dump?

“On Wednesday, the market teemed with rumors and rationales for the commodity dump. We noted in Tuesday's missive that China Premier Wen Jiabao vowed to move against inflation. Except for gold and oil, commodities rolled over a week ago. Who and what was Wen signaling?

“For the past few years, China has adroitly played commodities. When prices surge too far, particularly copper, a Chinese official makes inflation warnings or issues policy directives aimed at curtailing inflation. This forces leveraged speculators out of commodities and gives the Chinese a later opportunity to keep building their strategic commodity reserves at better prices.”

Source: Bill King, The King Report , March 20, 2008.

Reuters: China buyer defaults on US soy as CBOT slumps –trade

“Word that a Chinese buyer had defaulted on the purchase of a US soy cargo has stoked concerns that more defaults may occur, as international prices of oilseeds and vegetable oils slide from record highs early this month.

“‘There has been a default on an expensive soy by a small player in Shandong. This has been confirmed,' said a senior trader at an international house. The trader added there had been some defaults on soyoil and possibly as much as 150,000-200,000 tonnes of palmoil.”

Source: Nao Nakanishi, Reuters , March 19, 2008.

Minyanville: Fashionomics point the way

“Economists use an array of tools to forecast where the economy is headed – like hair length and hem lines. Whether the trends are bullish or bearish, Hoofy and Boo reveal what the latest fashions mean for finance.”

Source: Minyanville

Did you enjoy this posting? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2008 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Prieur du Plessis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.