Confiscation of Retirement Accounts - Another Brick in the Wall

Politics / Banksters Jul 12, 2013 - 01:53 PM GMTBy: Andy_Sutton

For the past few months we have been sounding the alarm both separately and collaboratively regarding the impending (although not necessarily imminent) looting of the Western financial system including bank accounts, public pension funds, and likely private retirement accounts to some extent. With regard to the bail-in doctrine now in place in much of the rest of the world, it appears as though Australia is jumping on board as well - as part of the 2013-2014 government budget no less. Details are still sketchy, but we’ll analyze what we have so far.

For the past few months we have been sounding the alarm both separately and collaboratively regarding the impending (although not necessarily imminent) looting of the Western financial system including bank accounts, public pension funds, and likely private retirement accounts to some extent. With regard to the bail-in doctrine now in place in much of the rest of the world, it appears as though Australia is jumping on board as well - as part of the 2013-2014 government budget no less. Details are still sketchy, but we’ll analyze what we have so far.

We remain absolutely convinced that a minimum of 95% of the people will do absolutely nothing. Most of them will not become familiar with the term ‘bail-in’ until it is already too late. We can’t do a thing about that. What is most depressing is that of the numerous people we have talked to who actually understand what is going on, the vast majority of them have also done nothing. Now is not the time to have that deer in the headlights, over analysis paralysis mindset.

The Latest Moves in the Chess Match

Australia, through its budgetary process, has endorsed the global bail-in resolution mechanism for GSIFI’s (Globally Active Systemically Important Financial Institutions). We’re going to use some terminology from April’s article authored by Andy Sutton regarding the FDIC/BOE and BIS whitepapers. That article is an absolute pre-requisite for understanding the situation down under.

One by one, the G20 has succumbed to the bail-in resolution mechanism. And it has been a very subtle process. You won’t hear about this on any of your favorite ‘news’ and opinion-shaping programs. The globalist elite are playing chess and the Proletariat are playing checkers. We obviously can’t shame anyone into looking out for themselves. We can beg, implore, beseech with hat in hand, but we can’t force this on you. You have the right to your ignorance just as we have the right to ours about the things that you might be passionate about. The big difference is this affects everyone. We are no better and no worse than any other pair of analysts who might someday look upon 2013 and comment and critique. Our plea comes from the heart and from a duty to both God in Heaven and our respective nations to spread the truth.

Let’s get to some details from Australia. It is difficult to assign credit, but we first discovered the information on the ‘Barnaby is Right’ blog with direct citations to Australian government budget documents. We have no reason to doubt the validity of the information at this point, especially given the fact that the blog cites Australian Treasury documents and the links are valid. It is pretty obvious that there is a good effort underway to hide these revelations as much as possible and our thanks go out to everyone who is digging on behalf of the Earth’s population.

The two snippets from Australia’s budgetary docs tell most of the story in very similar fashion to how the story was told in the FDIC/BOE collaboration and the separate but eerily similar BIS whitepaper:

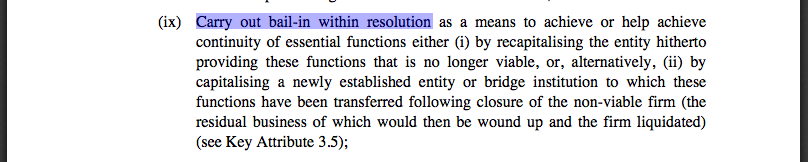

The term ‘bail-in’ as applied in Cyprus has now become accepted jargon for the fleecing of bank depositors to restore liquidity in a failed GSIFI. The mechanism is identical, even down to the establishment of a ‘bridge institution’. The USFed has several of these: ‘Maiden Lane 1,2, and 3, LLC’. They contain the junk assets from now defunct financial institutions. You can find the Maiden Lanes in the weekly H.41 releases from the USFed here. These are the types of bridge institutions we’re referring to.

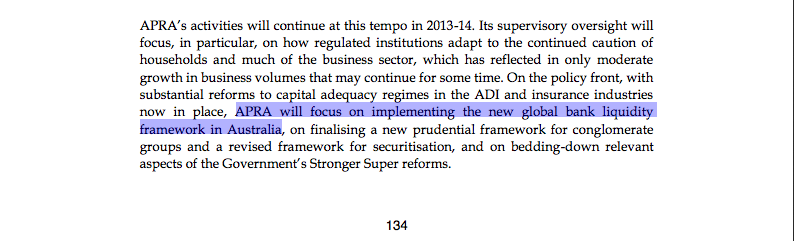

However, the bridge institutions are not what should concern depositors most. The next snippet, from page 134 of the budgetary document, deals with the responsibilities of APRA (Australian Prudential Regulation Authority). See below:

There are some rays of light shone into areas not covered in the expository blog that broke the story. Note the portion at the beginning of this paragraph detailing APRA’s responsibility to help institutions adapt to the ‘continued caution of households’. You may interpret this in the following manner: households aren’t borrowing and spending enough, so we need to figure out how to help the banking system create enough inflation to simulate (not stimulate) growth. Furthermore, the document states that there is an expectation that this condition will continue for sometime. To break it down, what Australia suffers from is identical to that of the rest of the G20: stagnant aggregate demand and upward pressure on end-user prices, also known as persistent stagflation.

And the chicken dinner winner is that APRA is tasked with focusing on implementing the ‘new global bank liquidity framework’ in Australia. How nice. We hereby submit to all the detractors, naysayers and threat-makers from March and April that they can proceed to the nearest pier and take a long walk – straight off. The bail-in mentality is real, it is here, and it is either already present in your land of domicile or is well on its way.

The Inadequacy of the Bail-in Framework Alone

There is one small problem with all of this in practice. In theory, it sounds great. We’re not going to put the losses from GSIFIs on the tab of the taxpayers. That’s great news! Instead we’ll just re-characterize depositors and place them into the same category as bondholders, who, in a Lehman/Bear Stearns type situation, can expect to get nothing back. There are some who might opine and argue that this is the responsible thing to do since the taxpayers shouldn’t be on the hook for the irresponsibility of some bank they might have never even heard of. We can sort of buy that. However, there are a couple of problems with this logic.

This has been pointed out in other articles, but we’ll state it again anyway. When Joe Main Street deposits his paycheck into the bank, he is doing so under the impression that it is his money, it doesn't belong to the bank. The rules have been quietly changed in order to give clear title of Joe Main Street’s deposited paycheck to the bank. Essentially, the decision to deposit money in a bank has now become an investment decision. Who do you trust not to go broke and steal your money during the new resolution framework? In order to make a wise deposit decision, the average individual now must be able to adequately assess the risk profile of their bank and perform specialized analysis, generally left to professionals. Yet the banks still place the FDIC stickers with the gold stars all over the place as if nothing has changed.

We can pretty much guarantee you that 99% of the G20 population doesn’t even realize that this change has occurred. We could charge the banks with constructive fraud among other things, but the courts of dishonor, particularly in the US, have already effectively ruled that this is a legitimate business practice, albeit on the brokerage side of the fence. The principle, however, minus all the legalese, is pretty simple: money you thought was yours in fact belongs to someone else. And in typical fashion, you won’t find that out until the most inconvenient of times.

The biggest fly in the ointment here is that the depositor money is not going to be nearly enough to cover the losses of firms that are leveraged 50:1. This is true by the very definition of leverage. If a bank is leveraged 50:1, it has $50 in liabilities (money borrowed to invest/speculate) for every dollar in capital. They now count your deposits as capital. See the problem? If one of these guys goes down, they can take every dollar of your deposits and there is still going to be a gaping hole. Who is going to fill it? The FDIC and its $25 billion ‘insurance fund’? If you believe that, you might as well wait for Elvis to show up in your local mall. He must be out there somewhere, sideburns and all. Right?

The Retirement System Becomes the Proverbial Dutch Boy

This is where we ultimately believe the retirement system will come into play. While the total notional value of OTC derivatives exceeds the assets of the US retirement system by a factor of at least 25-40, depending on which numbers you look at regarding OTC derivatives, retirement savings around the globe are the last real pool of legitimate capital that can be tapped in order to perform even a moderate resolution of the failure of even ONE of these large GSIFI institutions. But, like the Dutch boy, the retirement system might certainly plug a hole or two in the dam. Printed funny money from the USFed, ECB, or whoever else will make them whole. Or at least partially whole. Keep in mind there is no resolution mechanism to make you whole when this happens.

It is our firm belief that the retirement savings of the G20 will ultimately end up in the coffers of the large banks under the bail-in resolution mechanism outlined in the US, Europe, Japan, Canada, and now Australia. Many of our contemporaries opine that the retirement system will be looted to solve a sovereign crisis or series of sovereign crises. While sovereign debt may be a trigger, those monies will almost certainly go to the banks rather than governments.

Why? Because banking institutions make insane profits by managing and gambling with retirement savings on a global scale. They’re not going to just give that up without getting something in return. So instead of getting the fees from managing those funds, they’ll end up with the funds themselves. Make no mistake, there is not a government in the G20 with the spine to say no. Governments have become little more than weaponized enforcement arms of the banking elite and as such will do what they’re told. We’ve seen evidence of this over and over again, with the most notable example being Henry Paulson’s grandstanding in the US House back in the fall of 2008, making all sorts of dire predictions and threats should the bailout money not be approved. He was not advocating for ‘We the People’, but rather on behalf of his former employers and their ilk, while people are getting arrested in America for writing derogatory comments about those same banks on sidewalks with kids chalk.

Conclusions

We draw the same conclusions we did the last time around. The stage is being set through the usual Hegelian dialectic used by the power elite to separate Westerners from their savings. These same methods have already been used quite successfully, particularly in America, to strip people of their freedoms. Why would this be different and more importantly, why change methods when something works so well?

The only real questions that remain are what exactly will transpire to bring about the implementation of the bail-in resolution mechanism? Will it be piecemeal (one or a few countries at a time) or all at once? And when will it happen? Unfortunately, we don’t know the answers to these questions. We have our guesses, but we’re keeping them to ourselves, at least for now.

What we do know is that there is a light at the end of the tunnel. Unfortunately, this time around it is a freight train coming our way. There is still time for most to take at least some evasive action. Human history and the nature of human action tells us that most will do nothing, and the only reason we even went ahead with publishing this article to begin with is for the very few who are either on the fence and need to see some more substantiation (as opposed to the wild speculation, rumor, and innuendo so prevalent on the Internet) and those who have already decided to do something and need help remaining grounded and convicted that they are taking prudent steps.

As for the rest of you out there, we have no ulterior motives. You can take this information and use it or leave it. To accentuate this point, we close with a famous quote by Sam Adams:

“If you love wealth greater than liberty, the tranquility of servitude greater than the animating contest for freedom, go home from us in peace. We seek not your counsel, nor your arms. Crouch down and lick the hand that feeds you; May your chains set lightly upon you, and may posterity forget that you were our countrymen.”

Graham Mehl is a pseudonym. He currently works for a hedge fund and is responsible for economic forecasting and modeling. He has a graduate degree with honors from The Wharton School of the University of Pennsylvania among his educational achievements. Prior to his current position, he served as an economic research associate for a G7 central bank.

By Andy Sutton

http://www.my2centsonline.com

Andy Sutton holds a MBA with Honors in Economics from Moravian College and is a member of Omicron Delta Epsilon International Honor Society in Economics. His firm, Sutton & Associates, LLC currently provides financial planning services to a growing book of clients using a conservative approach aimed at accumulating high quality, income producing assets while providing protection against a falling dollar. For more information visit www.suttonfinance.net

Andy Sutton Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.