U.S. Housing Market Two Outs in The Bottom of The Ninth

Housing-Market / US Housing Sep 25, 2015 - 01:27 PM GMTBy: James_Quinn

The housing market peaked in 2005 and proceeded to crash over the next five years, with existing home sales falling 50%, new home sales falling 75%, and national home prices falling 30%. A funny thing happened after the peak. Wall Street banks accelerated the issuance of subprime mortgages to hyper-speed. The executives of these banks knew housing had peaked, but insatiable greed consumed them as they purposely doled out billions in no-doc liar loans as a necessary ingredient in their CDOs of mass destruction.

The housing market peaked in 2005 and proceeded to crash over the next five years, with existing home sales falling 50%, new home sales falling 75%, and national home prices falling 30%. A funny thing happened after the peak. Wall Street banks accelerated the issuance of subprime mortgages to hyper-speed. The executives of these banks knew housing had peaked, but insatiable greed consumed them as they purposely doled out billions in no-doc liar loans as a necessary ingredient in their CDOs of mass destruction.

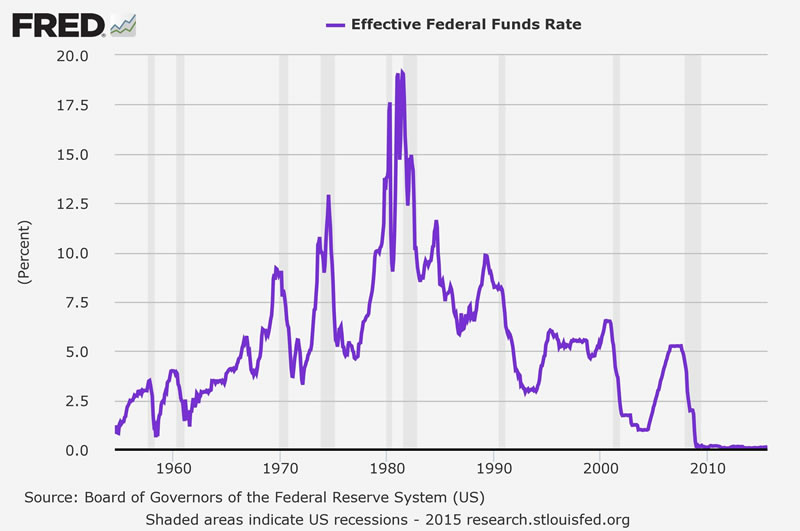

The millions in upfront fees, along with their lack of conscience in bribing Moody’s and S&P to get AAA ratings on toxic waste, while selling the derivatives to clients and shorting them at the same time, in order to enrich executives with multi-million dollar compensation packages, overrode any thoughts of risk management, consequences, or the impact on homeowners, investors, or taxpayers. The housing boom began as a natural reaction to the Federal Reserve suppressing interest rates to, at the time, ridiculously low levels from 2001 through 2004 (child’s play compared to the last six years).

Greenspan created the atmosphere for the greatest mal-investment in world history. As he raised rates from 2004 through 2006, the titans of finance on Wall Street should have scaled back their risk taking and prepared for the inevitable bursting of the bubble. Instead, they were blinded by unadulterated greed, as the legitimate home buyer pool dried up, and they purposely peddled “exotic” mortgages to dupes who weren’t capable of making the first payment. This is what happens at the end of Fed induced bubbles. Irrationality, insanity, recklessness, delusion, and willful disregard for reason, common sense, historical data and truth lead to tremendous pain, suffering, and financial losses.

Once the Wall Street machine runs out of people with the financial means to purchase a home or buy a new vehicle, they turn their sights on peddling their debt products to financially illiterate dupes. There is a good reason people with credit scores below 620 are classified as sub-prime. Scores this low result from missing multiple payments on credit cards and loans, having multiple collection items or judgments and potentially having a very recent bankruptcy or foreclosure. They have low paying jobs or no job at all. They do not have the financial means to repay a large loan. Giving them a loan to purchase a $250,000 home or a $30,000 automobile will not improve their lives. They are being set up for a fall by the crooked bankers making these loans. Heads they win, tails the dupe gets kicked out of that nice house onto the street and has those nice wheels repossessed in the middle of the night.

The subprime debacle that blew up the world in 2008 was created by the Federal Reserve, working on behalf of their Wall Street owners. When interest rates are set by central planners well below levels which would be set by the free market, based on risk and return, it creates bubbles, mal-investment, and ultimately financial system disaster. Did the Fed, Wall Street, politicians, and people learn their lesson? No. Because we bailed them out with our tax dollars and have silently stood by while they have issued $10 trillion of additional debt to solve a debt problem. The deformation of our financial system accelerates by the day.

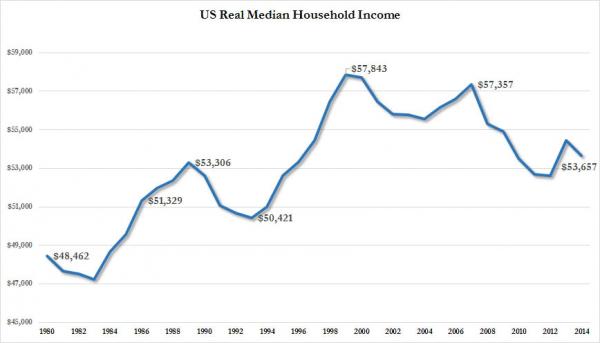

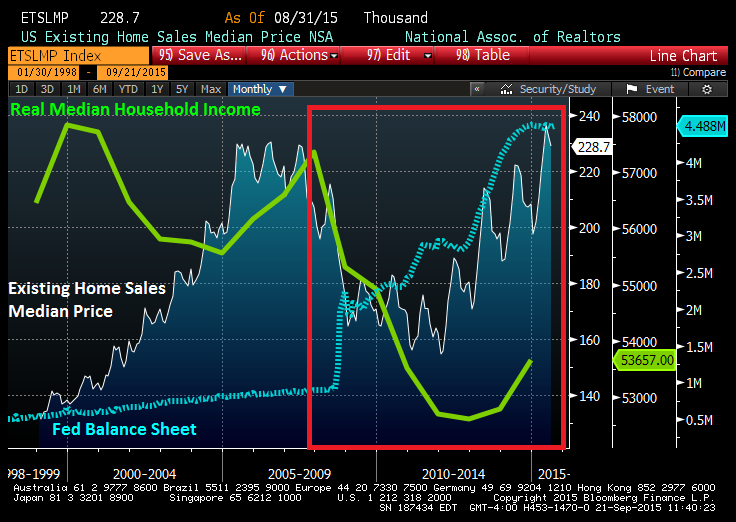

The $3.5 trillion of QE, six years of 0% interest rates for Wall Street (why are credit card interest rates still 13%?), and $8 trillion of deficit spending by the Federal government have provided the outward appearance of economic recovery, as the standard of living for most Americans has declined significantly. With real median household income still 6.5% BELOW 2007 levels, 7.3% BELOW 2000 levels, and about equal to 1989 levels, the only way the ruling class could manufacture a fake recovery is by ramping up the printing presses and reigniting a housing bubble and an auto bubble. They even threw in a student loan bubble for good measure.

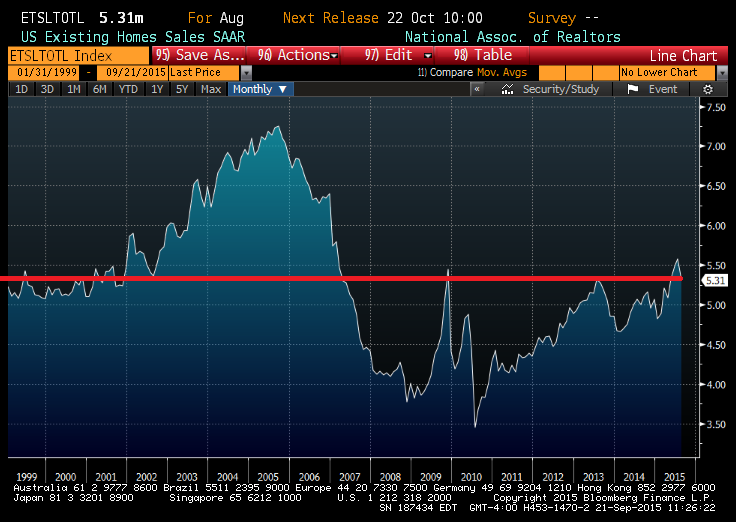

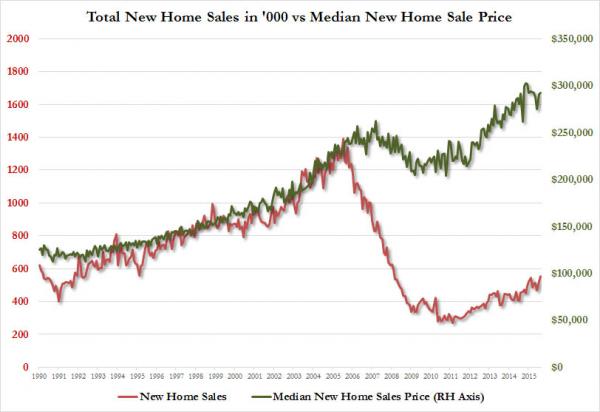

The entire engineered “housing recovery” has had a suspicious smell to it all along. The true bottom occurred in 2009 with an annual rate of 4 million existing home sales. An artificial bottom of 3.5 million occurred in 2010 after the expiration of the Keynesian first time home buyer credit that lured more dupes into the market. The current rate of 5.31 million is at 2007 crash levels and on par with 2001 recession levels. With mortgage rates at record low levels for five years, this is all we got?

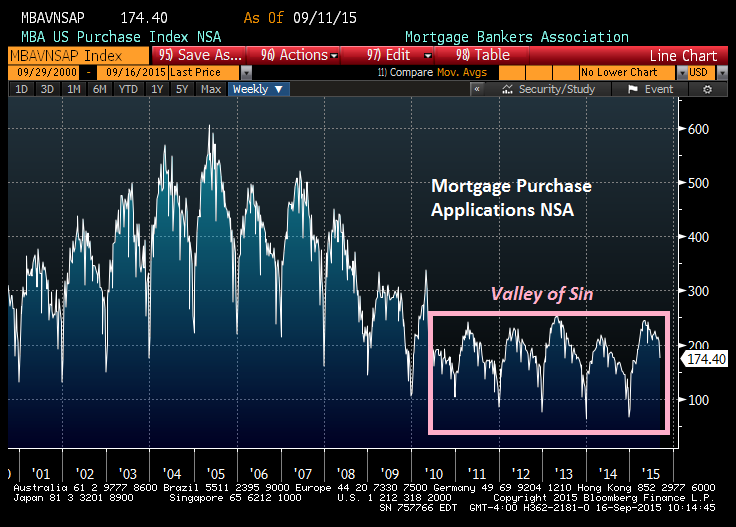

What really smells is the number of actual mortgage originations that have supposedly driven this 35% increase in existing home sales. If existing home sales are at 2007 levels, how could mortgage purchase applications be 55% below 2007 levels? If existing home sales are up 35% from the 2009/2010 lows, how could mortgage purchase applications be flat since 2010?

New home sales are up 80% from the 2010 lows, but before you get as excited as a CNBC bimbo over the “surging” new home sales, understand that new home sales are still 60% BELOW the 2005 high and 25% below the 1990 through 2000 average. So, in total, there are 1.5 million more annual home sales today than at the bottom in 2010. But mortgage originations haven’t budged. That’s quite a conundrum.

As you can also see, the median price for a new home far exceeds the bubble highs of 2005. A critical thinking individual might wonder how new home sales could be down 60% from 2005, while home prices are 15% higher than they were in 2005. Don’t the laws of supply and demand work anymore? The identical trend can be seen in the existing homes sales market. The median price for existing home sales of $228,700 is an all-time high, exceeding the 2005 bubble levels. Again, sales are down 30% since 2005. I wonder who is responsible for this warped chain of events?

You guessed it – the Federal Reserve. There is no doubt these Wall Street captured academics with their models, theories, formulas, and Keynesian beliefs have created another immense bubble that endangers a global financial system already teetering on the brink of collapse due to central bank shenanigans by EU, Japanese, and Chinese central bankers. QE and ZIRP have encouraged rampant gambling by amoral greed driven financial institutions. John Hussman sums up the “solution” implemented by the serial bubble blowers at the Fed.

The main impact of suppressed interest rates is to encourage yield-seeking speculation, to give low quality creditors access to the capital markets, to misallocate scarce saving, to subsidize leveraged carry trades, to reduce the long-term accumulation of productive capital, and to foment serial bubbles and crashes.

The suppressed interest rates and Yellen Put have encouraged Wall Street hedge funds, banks, finance companies, and fly by night mortgage brokers to finance a buy and rent scheme, house flippers, and once again subprime borrowers. The withholding of foreclosures from the market and the hedge fund purchase of millions of homes drove home prices higher. The artificially low mortgage rates also allowed people to buy more house than they normally could buy, thereby driving home prices even higher. This market manipulation has now priced out all but the richest Americans from buying a home. As expected, the Wall Street machine has decided to try and steal home with two outs in the bottom of the ninth. They’ve decided loaning money to people who are incapable of repaying the loan will surely work this time.

Existing home sales fell in August by 4.8%, and the rate of increase has been decelerating over the last twelve months. Hedge funds stopped buying, first time buyers are few as they are saddled with student loan debt, and the middle class doesn’t have the financial wherewithal to trade up. The Wall Street debt machine is running out of financially able customers, so they’ve ramped up subprime lending at the worst possible time. While overall existing home sales were up 6.2% over last year, the number of subprime first mortgage originations was up 30.5%, subprime home equity loans was up 29.5%, and subprime home equity lines of credit rose 20.4%. The percentage of subprime mortgage loans is the highest since 2008. While prime lending declines, subprime lending accelerates. This will surely end well.

And this is being promoted by the government through the FHA. Subprime mortgages are increasingly being underwritten by thinly capitalized non-banks and guaranteed by FHA. In 2012, when this data was first tracked, large banks represented 65.4% of FHA-backed loans. That number is now 29.6%. In their place, non-banks now represent 62.2% of the FHA lending. These fly by night outfits, who proliferated during the 2003 – 2008 subprime disaster, have little or no capital cushion and when these mortgages begin to default they will go bankrupt quickly, leaving the FHA (you the taxpayer) on the hook for the inevitable losses.

The FHA has been directed by their politician benefactors to pump up the housing market at any cost. You can get an FHA loan with a credit score as low as 500, so long as you have a 10% down payment. And once you hit a 580 credit score, you only need a 3.5% down payment. The FHA is exempt from the qualified mortgage requirement of a 43% debt-to-income ratio. Many loans have a debt-to-income above 55%. The FHA only looks at mortgage payments in their calculation. The FHA is willing to accept a gift or inheritance as a down payment. You could have no savings, a 500 FICO, a 50% debt-to-income and an inheritance and that would be sufficient to get you a loan.

These fly by night mortgage companies are created by slimy get rich quick hucksters who are willing to take huge risks, because there is a big difference between the risk that faces the company, and the risk that faces the owner. He will take incredibly rich commissions on all loans he books. Wall Street is again packaging these subprime slime loans into high yielding mortgage backed securities and getting the rating agencies to stamp it with a AAA rating.

Foolish investors receiving a good yield and a guarantee from the US government, are as clueless as they were in 2008. The owner of the mortgage company doesn’t care about default risk, since some other sucker has assumed that risk. When the mortgage company goes bankrupt, the owner has no personal liability. When it all blows up again, an already bankrupt FHA will be on the hook, which really means the taxpayer will pay again. You are underwriting the new subprime crisis.

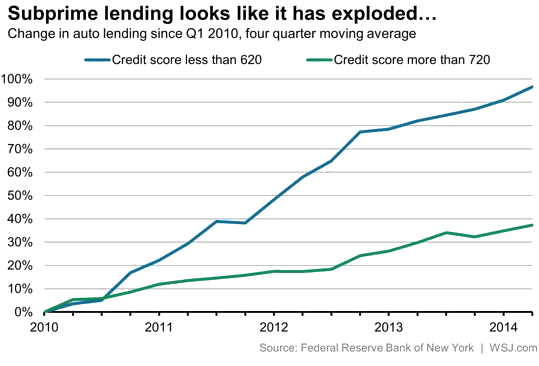

This exact same scenario is also playing out in the economically important auto market. It is clear the Fed, Treasury, Wall Street and the politicos in D.C. decided they needed to re-inflate the housing and auto bubbles to provide the appearance of economic recovery so they could resume their looting and pillaging of the national wealth. They have succeeded in ramping up auto sales from the 10.4 million annual rate in 2009 to 17.5 million in 2015, if you can call these sales. Short-term rentals is a better description. Auto leasing now accounts for 30% of “sales” (up from 22% in 2012), while subprime auto “sales” accounted for another 23.5%. The vast majority of the other sales are done with 7 year 0% financing. Does that sound like a sound business formula?

And now they’ve run out of dupes. The seasonally adjusted annual rate of sales for August 2015 was 17.2 million, flat with August 2014 and down from 17.5 million in July 2015. As the auto sales have gone flat and are poised to fall, the Wall Street finance machine has ramped up subprime lending from 18% of all loans in 2010 to 23.5% today. With overall sales flat with last year, subprime lending is up 9.6% in the last year. The pace of subprime auto loans has been more than double the pace of prime auto loans since 2010.

Over 10% of subprime auto loans are delinquent within the first twelve months. Subprime auto loan delinquency rates are soaring by 20% at Ally Financial. Santander is a Lehman Brothers in the making as their total delinquency rate approaches 20%. A critical thinking person might wonder why automaker profits are in decline, while GM and Ford stock prices are well below 2011 levels, if the auto market is booming.

The table is set for the next financial crisis. The apologists for the warped ideology that has resulted in $10 trillion of additional debt being layered on the original un-payable $52 trillion, argue subprime lending is lower than the 2008 peak, so all is well. They fail to realize the system is far more fragile and will collapse once the next Lehman moment arrives. The country is already in, or headed into recession. All economic indicators are flashing red. The stock market has fallen over 10% in the last month. Virtually every new car owner you see driving that fancy BMW, Lexus, or Volvo is underwater on their auto loan. Home price growth has stalled at record levels. Mortgage rates are poised to rise from record lows. We all know what happens next. Look out below.

Some people never learn. They follow the same path that destroyed their finances in the past. Wall Street is desperately packaging the increasing amounts of subprime slime in new derivatives of mass destruction and peddling them to clients, while shorting those same derivatives. It’s called the Goldman Sachs method. When home prices begin to tumble, these derivatives will self-destruct again. What is happening today is nothing more than rearranging the deck chairs on the Titanic. The iceberg has been struck, we’re taking on water, and this sucker is going to sink. Game Over.

“Part of the reason the Fed found it so difficult last week to justify a move away from zero interest rates is that the Fed seems incapable of recognizing, much less admitting, the speculative risks it has created. The strongest reason to normalize monetary policy was to reduce those risks, but the proper time to have done that was years ago. At this point, obscene equity valuations are already baked in the cake on valuation measures that are reliably correlated with actual subsequent stock market returns. At this point, hundreds of billions of dollars of low-grade covenant-lite debt have already been issued at risk premiums that are next to nothing. The bursting of this bubble is no longer avoidable. If history is any guide, policy makers will manage the resulting disruption by the seat of their pants, since they seem incapable of learning from history itself.” – John Hussman

Join me at www.TheBurningPlatform.com to discuss truth and the future of our country.

By James Quinn

James Quinn is a senior director of strategic planning for a major university. James has held financial positions with a retailer, homebuilder and university in his 22-year career. Those positions included treasurer, controller, and head of strategic planning. He is married with three boys and is writing these articles because he cares about their future. He earned a BS in accounting from Drexel University and an MBA from Villanova University. He is a certified public accountant and a certified cash manager.

These articles reflect the personal views of James Quinn. They do not necessarily represent the views of his employer, and are not sponsored or endorsed by his employer.

© 2015 Copyright James Quinn - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

James Quinn Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.