Gold and the Great Stage of Fools

Commodities / Gold and Silver 2018 Aug 29, 2018 - 04:59 AM GMTBy: Richard_Mills

Gold prices briefly traded above $1200 on Wednesday due to the legal and political troubles facing Donald Trump following the Paul Manafort guilty verdict on Tuesday. Kitco’s Jim Wykoff reports:

Gold prices briefly traded above $1200 on Wednesday due to the legal and political troubles facing Donald Trump following the Paul Manafort guilty verdict on Tuesday. Kitco’s Jim Wykoff reports:

Wednesday saw some trader and investor anxiety as Trump is in some hot water. Two of his close associates are likely going to jail. This has added a bit of uncertainty to the world marketplace at mid-week. There is talk Trump could pardon those associates, or that he could be impeached. And the mid-term congressional elections are right around the corner.

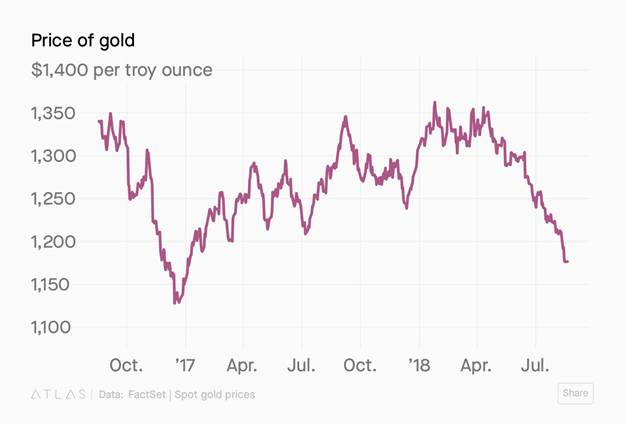

Gold actually climbed for five straight sessions on US dollar weakness, giving some relief to gold bugs shell-shocked by the $1174 low hit on August 22 – the worst level since January 2017. The metal of kings on Wednesday finished above the psychologically important $1200 an ounce, with gold futures trading at $1202.90, though the spot price stayed under, at $1189.70. Gold had a mini-rally on Friday, hitting $1208 an ounce (at time of writing) on comments from Fed chair Jerome Powell that the central bank is committed to gradually, not suddenly, raising interest rates.

Unfortunately however, it doesn’t look like there’s much light at the end of gold’s tunnel which has seen an especially dark summer. Minutes from the Federal Open Market Committee held July 31 to August 1 signalled that the Federal Reserve is likely to raise interest rates next month due to what it deems solid economic growth.

Rates have already been hiked twice this year, and have steadily been increasing since the end of quantitative easing in 2015. Higher rates, or even the expectation of, usually put pressure on gold prices, since gold pays no yield compared to bonds or dividend-paying stocks. Hot US stock markets have only made the situation worse.

In a little over six months, gold has dropped 13.5%, compared to 2017, when the metal was up 12.5% over the year. That puts gold firmly in the grips of a correction and moving in the direction of bear market territory of losses greater than 20%.

Gold’s dip has largely been the result of a parallel climb in the US dollar due to a number of factors, including safe haven demand for US T-bills. In fact the big story line for gold these days is that it no longer appears to be the attractive flight to safety it normally is in times of economic and political turmoil - all of which is in abundance globally right now. Instead, investors are parking their money in the US dollar. But why? Is the US economy really that strong? We have our doubts. So what gives with gold and the US dollar? This article will explain the machinations of the greenback, the yellow metal, and the economic metrics that always coalesce to determine their respective values: interest rates, bond yields and inflation.

Treasury binge

What US dollar assets are being bought and by whom? It’s mostly US Treasuries. Foreign investors purchased some $26 billion of T-bills in May, driven by fear of a trade war and the indecisive result of the Italian election. They were also attracted by higher bond yields, which hit a seven-year peak in May. The two largest Treasury holders, China and Japan, both increased their buying, although Russia didn’t buy any, having cut their purchases by 50% in April - likely in reaction to new US sanctions on Russia, Reuters said. Germany bought $12 billion more in April compared to March.

Interestingly though, it’s not just central banks who are gobbling up Treasury notes. It’s also institutional and retail investors, drawn to their yields which are now competitive with the average S&P dividend yield, reports Wolf Street. It notes that over the previous year from mid-June, $1.22 trillion in new US government debt (Treasuries) was purchased, with just over $1 trillion bought by investors. Foreign holdings only increased by $109 billion over that period, while the Fed’s Treasury holdings were down by $70 billion, as the central bank sold T-bills as part of its plan to unwind quantitative easing.

Gold getting crushed

Because gold, and other commodities, is traded in US dollars, when the dollar strengthens, the value of gold will fall. When the gold price dips it also means that the dollar has jumped. Right now you can buy a lot more gold with a dollar than you could six months ago when it was trading about $100 more an ounce.

The question though, is why is the dollar so strong? Forbes gives one of the best explanations I’ve read, noting that the rally in the greenback is due to the two-pronged strategy being pursued by the Trump Administration and the Fed: a rise in short-term interest rates and a big increase in government spending, fuelled by the $1.5 trillion tax cut passed last December.

The combination of tighter monetary policy (higher rates) and a loose fiscal policy (higher spending) “could be the closest thing to an elixir for currencies. It is the policy mix that the US is pursuing,” Forbes columnist Simon Constable writes. The result has been a flood of capital to the United States, attracted by higher returns. A report from Brown Brothers Harriman, a New York bank, states that foreign investors bought $4.7 billion of US assets in the second quarter, the largest quarterly purchase in a decade. This massive inflow of cash is pushing up the value of the dollar, while at the same time, crushing gold. As Project Syndicate argues, while the Trump Administration would like Americans to believe the dollar’s rise is due to strong economic growth driven by deregulation, tax cuts and defense spending, the reality is it’s more to do with interest rate hikes.

The dollar’s rise has also fed into gold’s supply-demand fundamentals. As the dollar grows stronger, gold-producing countries like South Africa are experiencing a sell-off in their currencies. Because their costs are in local currencies but their revenues are in USD, they have a strong incentive to produce more gold. More supply is pulling down prices further. Interest rate hikes are also denting gold since, as mentioned, it offers no yield.

As for gold demand, it’s all but dried up. According to the World Gold Council, demand slumped across all segments including physical gold (bars and coins), jewelry and ETFs, with the latter down 47% year on year. Overall demand fell 6% to 1,959 tonnes during the first six months of the year versus H1 2017, and was at its lowest level since 2009, MINING.com said.

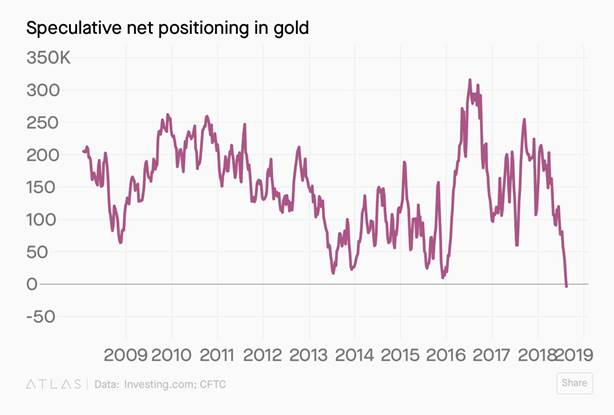

Earlier this month net positioning in gold went short, meaning that for the first time in 17 years, more transactions are betting that gold will go down than up, Quartz reported. As of Aug. 14, investors were short the equivalent of 670 tonnes.

The gold doldrums have gotten so bad, some are calling a market bottom. They include Kitco columnist David Erfle, who noted on Friday that capitulation selling began on Monday after GDX (the VanEck Vectors Gold Miners ETF) fell below $21 a share. But for Erfle, the cup is half full. He points out that “the higher this managed money short position runs, the inevitable mean reversion becomes potentially more explosive once a catalyst materializes.”

Market sentiment is also very bearish, evidenced by the “Consensus Bullish Sentiment Index” among newsletter publishers dropping to the lowest level since 2004. Thus, based on the large number of short positions right now, and sentiment research, “the gold market is a rocket on the launchpad, waiting for ignition,” Erfle writes.

King dollar

Investors love gold because it tends to hold its value through time. They see gold as a way to preserve their wealth, unlike paper or “fiat” currencies which are subject to inflationary pressures and over time, lose their value. In the US there was an increase in inflation for every decade except the Depression when prices shrunk nearly 20%. The Bureau of Labor Statistics’ Consumer Price Index indicates that between 1860 and 2015, the dollar experienced 2.6% inflation every year, meaning that US$1 in 1860 was equivalent to $27.80 in 2015. This also means that prices in 2015 were 2,828% higher than they were in 1860.

When the dollar falls, investors flock to gold, hence the inverse relationship between the two.

Gold has also traditionally functioned as a safe haven. Investors love nothing more than a war, economic crisis or any type of geopolitical instability to watch the value of their bullion grow. Heightened global tensions such as terrorist attacks, border skirmishes or civil wars scare investors into putting their funds into safe havens like gold and stable, high-yield sovereign debt. Geopolitical tensions also drive more government spending (Eg. on arms), which brings inflation, leading investors to look at precious metals as a place to park their money, short term.

But something odd has been happening to gold over the past six months or so. It’s no longer being seeing as the secure investment it once was compared to its alternatives, which include the USD, the Swiss franc and the Japanese yen. Why is that? The answer appears to be, it’s not so much the USD is such an attractive safe haven, but rather, there are no better alternatives.

Look around the world, and every region seems unstable. Compared to places like the Middle East (sanctions slapped on Iran; currency meltdown in Turkey/record inflation; along with the usual hot spots), Africa (corruption in South Africa and a contested election in Zimbabwe), Asia (the Chinese currency is falling/its economy slowing; tension in Pakistan) and even Europe, the US is a bulwark of stability. Not only does the US seem safe - despite the near-constant outbreak of gun violence and always simmering race relations - it’s also expanding. The US economy grew 4.1% last quarter, and while there are questions surrounding that figure - like the fact that there was a burst of consumer spending from the tax cut and exports soared in preparation for an all-out trade war - would you rather park your money in, say, Britain, where the effects of Brexit are putting a dark shadow over its future? The British are being told to hoard goods because they may soon not be able to get them, or afford them. In the rest of Europe resistance to immigration is fueling the rise of right-wing movements. The Italian election was a mess. Greece is still a basket-case.

As CNBC points out, a year ago 19 European countries had negative interest rates in a last-ditch effort to spur lagging growth. In the US the federal funds rate is 2% and likely to rise further this year.

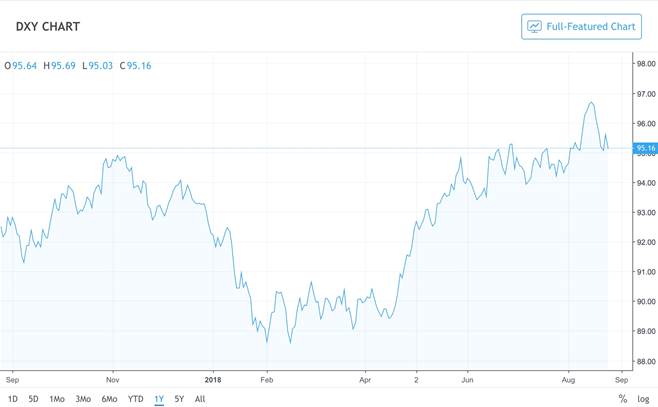

For savers and investors keeping funds in dollars, American banks and/or American securities are more than a little appealing. This may be the reason that the dollar is up 8.7 percent in value from its February low. It explains why U.S.-based bank deposits have risen by $252 billion or 2.1 percent in the same time frame. It may be a reason that the S&P 500 is up more than 9 percent from its February low.

So where do you want your money held? The obvious answer would appear to be in a solid, domestic American bank backed by FDIC insurance. Or a security tied to a U.S.-based company. Despite its political angst, the United States is best. - CNBC

Michael Pento points out that the USD is so strong, pushed higher by efforts to clean up its balance sheet by selling off $2 trillion worth of debt, and a tighter fiscal policy compared to continued loosening everywhere else, that it may spur an emerging market currency crisis reminiscent of the 1997 Asia Debt Crisis. This is because some countries “hold onerous dollar-denominated debt in conjunction with large current account and budget deficits.”

Turing to today, a decade’s worth of interest rate suppression in the developed world has sent global investors on a frenzied chase for yield like never before in the emerging markets. Excess liquidity has resulted in fiscal mismanagement, current account deficits, and large dollar-denominated debt loads. According to the Institute of International Finance, corporate debt in foreign currencies has soared to $5.5 trillion, the most ever on record. - Michael Pento, President, Pento Portfolio Strategies

A wormy apple

So the US dollar is strong, unemployment is at its lowest level in 20 years, 3.9%, the stock market is booming, and the Fed thinks things are going so well that they are ready to pass another interest rate hike next month. US Treasuries are the only game in town for yield-seeking investors because all the other players have been sidelined.

The basis of a strong dollar is a booming US economy, but is it really booming? The fact is, life is just peachy for about 1% of Americans; for the rest of them, it's the pits.

To wit: Should we be surprised that President Trump marked the first year of his first term in office with a massive tax cut to businesses and the rich? Probably not. He owes his loyalty not to the little guy in Alabama, but the big corporations on Wall Street and the financial elites who have bankrolled his real estate empire.

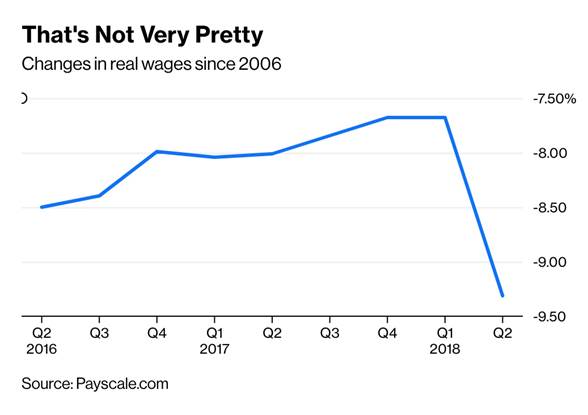

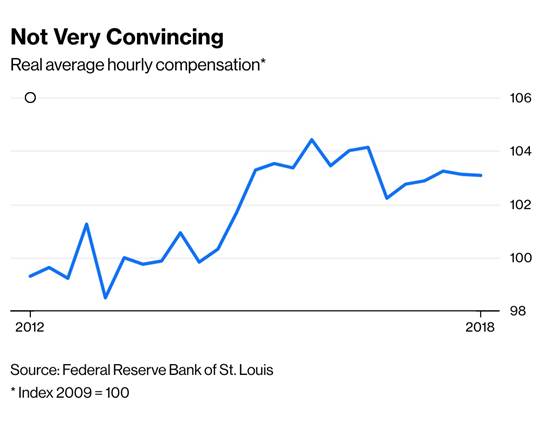

While unemployment has indeed fallen under Trump, it has done since 2010; when Obama left office the jobless rate was at 4.8%. This should have led to higher wages, but it hasn’t. The chart below shows a 9.3% drop in real wages during the second quarter of this year (inflation adjusted), compared to a 12.6% rise since 2006.

The labor force participation rate (people who are either employed or actively looking for work) has stabilized under Trump after plummeting since 2008, but it’s still at 63%, three percentage points lower than during the recession. Lastly, there’s the deficit, which has grown significantly under Trump. Obama managed to narrow the US trade deficit (exports minus imports) to $35 billion in 2013 (it also rocketed to $49 billion in 2015), but it’s widened to $46 billion, as of April, and was over $50 billion in 2017.

The effects of the Trump Administration’s plan, starting in March, to levy import tariffs on billions of goods sold to the United States as a way of protecting American jobs and sectors, are starting to be felt. Many feared that increased protectionism would lead to countervailing duties on US exports, particularly those going to China, which has been the country most targeted by Trump.

And that has happened. After Trump slapped $34 billion worth of duties on July 6, China responded in kind, imposing the same amount of tariffs on US cars, soybeans and seafood. While some Americans will puff their chests at what is an aggressive move to address the $375 billion trade imbalance with China, the reality is these countervailing duties are just a tax, that raises the price of the imported good.

And prices are going up. Who cares if the economy is growing at 4% if your six-pack of Miller is going to take a bigger bite out of your pay check?

The price of Coca-Cola and other carbonated drinks is about to get more expensive due to the higher price of aluminum to make cans.

Safehaven reports other products including furniture, boats, motorcycles and campers are all going to cost more. It references a press release from a beer trade group saying that the aluminum tariff will cost beer producers nearly $350 million and will threaten over 20,000 jobs.

Overall, consumer prices have increased 2.9% in the last 12 months through June.

Inflation has climbed so much, it’s overtaken wage gains. Knowing all this, do Treasuries still look good? Maybe on the outside. But like a shiny red apple teeming with worms in the core, the US is an economy rotting from the inside. It’s only a matter of time before people wake up and see that all is not well in the House of Trump.

Gold fundamentals ignored

It used to be that investors weighed inflation, the dollar, supply and demand for the metal, and perhaps most importantly, real interest rates, as determinants of whether to invest in gold. Now those fundamentals have gone out the window.

For example conventional wisdom says that when real interest rates turn negative, it’s time to pull the trigger on gold. Well, they’ve been negative for awhile, and gold sentiment has collapsed. As noted inflation is running at 2.9% but the interest rate is only 2%. Subtract inflation from the nominal interest rate and you get -0.9%, the real interest rate. Forget about peak gold, gold as inflation hedge, safe haven demand or any other reason to own gold including the fact it looks pretty. The only factor that seems to matter these days is the value of the US dollar.

Remember when the gold price rose and fell according to even suggestions that the Fed might take away the punch bowl and end QE? Now raising interest rates do little to gold; of course, it’s likely baked into the price. When the Fed raised rates in June, gold fell just $4, then rallied to $1299 at the end of the day.

Recession?

The R-word is seldom uttered these days due to the ebullient mood of bankers and brokers, even in a weird Trump universe where the President’s next tweet could send stocks and the dollar falling to Earth. But there have been looming signs of an economic slowdown in recent months by observers who watch the US Treasury yield curves.

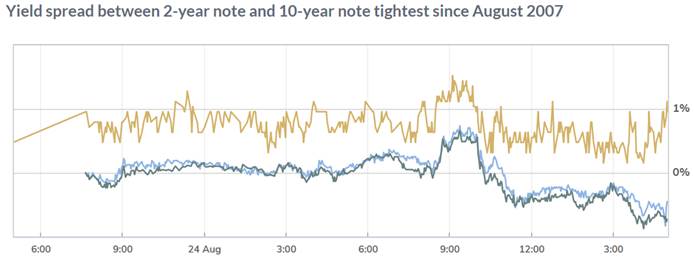

A narrowing spread between short-term (typically 2 years) and longer-term bonds is a signal that investors are worried about the economy’s health.

A negative spread, or inverted yield curve, historically signals a recession. An inversion of the curve (short-dated yields are above long-dated ones) has preceded every recession since World War II.

On Aug. 23 a decline in long-dated Treasury yield narrowed the spread between the 2-year note and the 10-year note to 21.1 basis points, its flattest since August 2007, MarketWatch reported. (2.821% for the 10-year versus 2.610% for the 2-year)

How to explain the flattening yield curve despite good economic fundamentals - at least those not affecting average Americans, like wage growth and inflation?

Despite the central bank’s confidence in the economy, investors are skeptical, writes MarketWatch. “[They] ultimately see the recent burst of growth as fleeting.” The publication quotes the head of US economics for Oxford Economics, a forecaster, saying that Q2 likely represented peak growth and there is pain to come in the form of fallout from the trade war and slower global growth.

Other analysts are more pessimistic, saying that investors should enjoy the last stages of a late-cycle economic boom, because the nine-year expansion period is coming to an end. Scott Minerd, chief investment officer at Guggenheim Investment Management, was even reported saying that continued rate hikes could end up “choking off credit, leading to mass defaults from debt-laden corporations.”

It also needs to be mentioned that the effects of Donald Trump’s trade war - mostly with China but also Europe and Canada - have yet to really be felt. Trump’s fanatical quest to reduce trade deficits with his trading partners could easily backfire. In a recent podcast, Macro Watch publisher Richard Duncan told Financial Sense that a protracted trade war between the US and China could lead to a spike in inflation (prices are already rising), interest rates (ditto for the US) and another Great Depression. His conclusion?

“Combined, the crashing asset prices [of property and stocks] and the contract of credit would be enough to throw the U.S. into a depression, most probably,” Duncan said. “At that point, it’s uncertain whether President Trump’s supporters would continue to support him or not, because they would lose their jobs and they would have to pay much higher prices for the goods that they bought as inflation rose. So there's a possibility that President Trump will not have the power to carry out this trade war long enough to really make it significant.”

Conclusion

My conclusion isn’t quite so apocalyptic, though it’s easy to see how we are on the road to an economic meltdown. In Vancouver, San Francisco and other over-priced cities, the number of people living homeless or pay check to pay check has been rising for years, and with the exorbitant cost of housing eating up a massive portion of household income, even a tiny rise in interest rates could break the bank.

Trump’s policies have done much to help large corporations, who have plowed most of the extra cash from the corporate tax cut into share buybacks, rather than expanding businesses and increasing shareholder dividends. Meanwhile, for average Joe and Jane who can’t afford to invest, their wages continue to decline while prices of everything from beer to diapers keep climbing.

This is the environment into which foreign investors are blindly stashing their funds into US Treasuries, considered the beacon of a safe harbor investment. But are they really? A recession in the US would kill economic growth, force the government to spend on welfare programs to cushion lost jobs, thereby making the already ridiculously large US debt even worse, and lead to deflation. The US dollar would crash, causing a sell-off of US Treasuries. The capital would flee to jurisdictions where currencies are stronger and the returns are better. Like the Great Recession of 2009, the Fed would have to reverse course and start buying back Treasuries in an effort to stem the outflow. More quantitative easing would ensue, with rates pushed down to zero in order to stimulate flagging growth.

Could it happen? Who knows. A major economic calamity would be good for gold, as investors realize their dollars are worthless and investing in real, tangible assets is their only option for preserving wealth. It’s too bad that it would take something this bad for gold to regain its luster. At Ahead of the Herd we still believe in gold’s fundamentals, as a store of wealth, a hedge against inflation, and a safe haven against global turbulence. Are you protected against another recession, or depression, kicked into motion by Trump’s ill-advised trade war and snowballing into something much worse? Despite its current weakness, gold is still the best protection.

Added into this already toxic Trump rotten egg omelet is the fact that so many of President Trump’s inner circle are talking to the FBI about each other, their colleagues criminal activities. Republican congressmen who early on supported Trump, his closest friends and advisers, his lawyers, even his Father’s and his CFO, convicted and going to jail or turning on each other seeking immunity from prosecution. What I fear is the backlash from all this drives Trump to take drastic action, perhaps foreign intervention – war. Republicans might lose the House of Representatives in the upcoming midterms. That would set the stage for Trump’s impeachment, all hell breaks loose then, all the cards are off the table and who knows where that road takes us.

Even scarier. What if Republicans keep the House of Representatives? Everything rotten, every nasty, illegal activity swept under the carpet, business as unusual has been condoned.

Top all of that with a dash of this hollandaise sauce - the state of New York suit against his foundation looks like it could ultimately take the whole family down. Eric, Don Jr. and Ivanka are all named, along with the president, who in this state case has no power to pardon.

Much has been written comparing Nixon, J.R. Ewing and King Lear to President Trump. I don’t know about much about these comparisons but I do know a good line when I read it.

“'We cry that we are come unto this great stage of fools.”

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including: Wall Street Journal, Market Oracle, USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2018 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.