Bailout for the People: Dividend Economics, Basic Income Guarantee- Part2

Politics / Credit Crisis Bailouts Feb 04, 2009 - 09:47 AM GMTBy: Richard_C_Cook

Key Discovery of the 20th Century: Dividend Economics

Perhaps 20-30 percent of the people in the developed world are doing just fine financially. They are either professionals, technical experts who are indispensable in making the world economy function, former government employees on pensions, or a small minority who live off compound interest—i.e., the bankers and the rich. Most of this 20-30 percent, particularly the latter group, do not seem to have a great deal of compassion for the majority within their own nations and even less for the billions of less privileged people around the world.

For the remaining 70-80 percent who realize, with the recession now having arrived, that their livelihoods are on a slippery slope downward, possibly taking them toward personal and family catastrophe, they need only one thing—MONEY!

For many of these it would be nice to have a job, or a better job. But jobs are not the answer, even though any time a politician, economist, activist, or commentator offers an opinion on how to improve the economy they say MORE JOBS! For example, in a recent article in Rolling Stone dated January 14 and entitled “Back to What Obama Must Do,” Paul Krugman wrote, addressing the new president:

“…you have to be really bold in your job-creation plans. Basically, businesses and consumers are cutting way back on spending, leaving the economy with a huge shortfall in demand, which will lead to a huge fall in employment - unless you stop it. To stop it, however, you have to spend enough to fill the hole left by the private sector's retrenchment.”

But the advocates for government job-creation programs as the focal point of recovery are wrong.

The way to generate income security is not to give someone a job. It is to put money—cash—in his pocket. If we began with this simple fact the economy would soon generate far more jobs than people could fill. Of course some of these jobs would be low-paying or even volunteer jobs, which would be acceptable provided that people still had enough to live on and had opportunities to earn more.

For the world economy to function and for there to be enough produced to support everyone at a decent standard of living, not everyone has to work. In fact too many workers get in each other's way. This accounts for the paradox which progressives despise that when companies eliminate jobs their stock value often goes up, because it's a step toward becoming more efficient and more profitable.

In 2007 the world GDP was enormous–$55 trillion. The population was 6.6 billion. Per capita that's $8,300. It's not a large sum, but in many countries the cost of living is far lower than in the developed nations of the West. For a family of four the amount is $33,200. The point is that the world economy is capable of producing enough for all.

The productivity of a modern industrial economy is phenomenal. It surpasses the wildest dreams of generations past. The problem today is not a shortage of goods and services. It is often too many goods and services. For instance, there is a worldwide glut of automobiles. The same goes for many other items such as clothing and electronics. This does not mean that threats like climate change or resource depletion should be ignored. The reason these are not being faced is that industry must work so hard to cut costs and keep prices down in the face of the shortage of consumer purchasing power.

So why do we need more jobs? Only because we are so cheap and poorly informed that we fail to realize that a cash payment to everyone, at least at a subsistence level, should be viewed as a dividend. It's something everyone should receive as the benefit of our incredible producing economy. A Basic Income Guarantee should be treated as a HUMAN RIGHT.

But the situation does not require that someone else should be taxed in order for that dividend to be provided. A BIG does not have to be a transfer payment or a share-the-wealth scheme. Rather it should reflect an acknowledgment by the economic system that the universe is bountiful and abundant. Modern industry has tapped into that abundance.

Today the abundance is being stolen by the bankers and their debt-based monetary system. This is what must be taken back by on behalf of “We the People.” This can be done by payment of a BIG as a dividend. It would not be inflationary, because it would not result in “more money chasing the same amount of goods.” Rather it would replace money borrowed from the banks or would generate new production.

If you want to read the history of dividend-economics, study the worldwide Social Credit movement originated by British engineer C.H. Douglas in the 1920s and 30s. I am not going to repeat that history here. I have written about it in articles over the past two years, most of which can be found at www.GlobalResearch.ca . It's one of the themes in my new book, We Hold These Truths: The Hope of Monetary Reform (Tendril Press, 2008). You can find a lot of information about Social Credit on the internet, including the website for the Michael Journal in Canada at www.michaeljournal.org .

One of the world's leading experts on Social Credit is Wallace Klinck of Alberta, Canada, who provides the following commentary on the crisis:

“The base cause of our essential economic and social afflictions is…a fundamental and widening disparity between effective consumer income and financial prices—resulting essentially from a basic flaw in national financial cost accountancy involving a premature withdrawal of credit because of added allocated capital charges in consumer prices. The consequent widening deficiency of effective purchasing-power forces the consuming public increasingly into dependency upon debt.

“We are now witnessing the inevitable, entirely predictable, and devastating results of such folly (or more likely, high policy). Governments are forced to make a futile attempt to ameliorate this problem by assuming debt to compensate or accommodate the ballooning private debt. I am sure that the financial powers look on with almost puzzled amusement as we engage in a sterile debate about the evils of interest and usury when we obviously have no strategy to deal with the rapid expansion of debt upon which interest is demanded. We waste our energy on a misguided and sterile debate while ignoring the fact that the consumer is charged with capital depreciation but not credited with capital appreciation.

“In other words, we blindly forgo our inheritance for a mess of pottage. You only pay interest on debt—eliminate debt and you have effectively eliminated any tribute of interest or ‘usury.' There should be no need for any overall national consumer debt at all—consumers in aggregate should always be provided sufficient income to purchase the entire final product of industry without resorting to borrowing. The physical cost of production has been provided in full when goods are completed, and the financial means to liquidate the financial costs of that production should be made fully available as each ‘cycle' of production is completed.

“Whatever the costs to industry, including interest or service charges, the consumer should always be in a position to liquidate them with his or her financial income. Being increasingly inadequate under the orthodox system of financial accountancy, that consumer income must be supplemented from a source which originates outside the price-system and does not, therefore, create new financial costs through its issue. The mechanisms to achieve this condition recommended by Social Credit are the payment to all citizens of a National Dividend and to all retailers a compensatory payment in order to effect a falling price-level, i.e., a Compensated Price.

“When the expenditure of human labor is being rapidly replaced by other factors of production, as it is in a most spectacular manner, talk of there being ‘no free lunch' is entirely irrational from the standpoint of reason, downright sacrilegious from a theological standpoint, absolutely disastrous from an economic and social perspective—and absurd from a philosophical aspect.”

Mr. Klinck is explaining why everyone doesn't have to work all the time for us to enjoy a decent standard of living. People in the U.S. understood this in the 1950s, when a single breadwinner could support a family. Does anyone wonder why conditions have changed so much for the worse since then when GDP is so much higher? In a private message to me dated December 13, 2008, Mr. Klinck made the following observations on jobs vs. income:

“I find it quite maddening that we have these recent desperate appeals for industrial state ‘bailouts' to help industry go on producing even more unsalable goods, when it should be quite obvious that what needs ‘subsidizing' is consumption and not production. Of course, as we know from a Social Credit perspective, these appeals are based on a number of major misconceptions about national cost accounting, the purpose of industry, work, and life in general. I think that this erroneous and indelibly entrenched ‘moral' mindset is our biggest obstacle. For instance, I heard extended appeals on television today from the Canadian Autoworker's Union for protection of their ‘jobs', etc. If only we could show them that it is their incomes and not their ‘jobs' which should be preserved. They are so obsessed with ‘work' that they are blinded to reality.”

It's a revolutionary thing to say, but it's true. Unemployment does not have to be “bad” at all. It means fewer people have to work to make what society needs to function. It's an indicator of greater efficiency. It's only bad if jobs are the only way to provide people with income. Dividend economics shows that there are other, often better, ways.

Lessons from the Alaska Permanent Fund

We can find one small but extremely important example of dividend economics in the U.S. by examining the Alaska Permanent Fund, which paid every resident of Alaska a dividend of $3,269 in 2008 out of state resource revenues. The APF was set up in 1976 when Alaska voters passed a constitutional amendment calling for a direct payment to individuals rather than turning the money over to the state bureaucracy for “social services.”

Today the Alaska Permanent Fund is a shining—and rare—example of economic democracy at work. At first the APF made dividends incremental based on a person's years of residency, but the U.S. Supreme Court declared this provision unconstitutional. The Alaska legislature responded by providing equal dividends to all residents of six-months or more. The first dividend, amounting to $1,000, was paid on June 14, 1982.

The APF dividend is not a welfare payment. It is a resident's fair share of the bounty of the earth. There are no means tests, no lines to wait in, and no bureaucrats snooping around to find out what someone used the money for. The APF has not ruined the character of those who get it. A millionaire receives the same payment as a person living in poverty. Spent into circulation, the money becomes part of the lifeblood of the community without having to be repaid and with no interest being charged. Deposited into banks, the money capitalizes consumer borrowing and economic growth.

In the Fall 2008 Newsletter of the U.S. Basic Income Guarantee Network there appeared an editorial on the Alaska Permanent Fund by Karl Widerquist, one of the leaders of the worldwide BIG movement, now a professor at Reading University in England. This editorial is reprinted as follows:

“EDITORIAL: The Alaska Dividend and the Presidential Election (The views expressed in this editorial are my own and do not represent the views of USBIG or its membership. -Karl Widerquist)

“Most people will be surprised to learn that the Republican vice-presidential nominee and the Democratic presidential nominee have both endorsed the Basic Income Guarantee. In one form or another both support policies to guarantee a small government-provided income for everyone. As reported in the USBIG Newsletter earlier this year, Obama has voiced support for reducing carbon emissions with the cap-and-dividend strategy, which includes a small BIG.

“Sarah Palin, like most Alaskan politicians, supports the Alaska Permanent Fund. Existing rules caused the APF dividend to reach a new high of 2,069 this year. That much had nothing to do with Palin. But, whatever else you might think of her, she deserves credit for adding $1200 more to this year's dividend.… She proposed it to the legislature, and pushed it through, resisting counter proposals to reduce the supplement to $1000 or $250.

“Most people who learned about Palin at the Republican National Convention in August would probably be surprised to learn that such a hard-line conservative supports handing out $16,345 checks to even the poorest families. Actually, families the size of Palin's will receive $19,416—no conditions imposed besides residency, no judgments made.

“The support of politicians like Palin provides evidence against the belief that BIG is some kind of leftist utopian fantasy with no political viability. In the one place BIG exists it is one of the most popular government programs, and it is endorsed by people across the political spectrum.

“The APF has not become an issue in the campaign, and I doubt she has plans to introduce a similar plan at the national level, but when the issue has come up, Palin has taken credit for it as a conservative policy. In an interview on the Fox News network, Sean Hannity confirmed that Palin increased the Alaska dividend by $1200 this year. Hannity commented, ‘I have to move to Alaska. New York taxes are killing me.'

“Sounding like some kind of progressive-era land reformer, Palin replied, ‘What we're doing up there is returning a share of resource development dollars back to the people who own the resources. And our constitution up there mandates that as you develop resources it's to be for the maximum benefit of the people, not the corporations, not the government, but the people of Alaska.'

“Tim Graham, writing for the conservative website Newsbuster.com criticized NPR's Terry Gross for asking questions that implied opposition to the APF in an interview with Alaska Public Broadcasting host, Michael Carey. Graham writes, ‘Gross walked Carey through the idea that it's not hard for Palin to be popular in Alaska when she's handing every family a $1200 check from all the oil business. She then elbowed Carey about how that money could have been better “invested” (as Obama would say) in government programs.' Suddenly conservatives are ridiculing people they assume do not support unconditional grants.

“Palin justified a tax increase on the oil companies to support higher BIG on the PBS Now program before she was nominated for vice-president. ‘This is a big darn deal for Alaska. That non-renewable resource, of course, is so valuable …. And of course [the oil companies] they're fighting us every step of the way when we say, “Well we wanna make sure, especially as it's being sold for a premium, that we're receiving appropriate value.” … The oil companies don't own the resources. They have leases and the right to develop our resources for us. And we share a value, we're partners there, because they do the producing for us. But we own the resources.' …

“The lesson here is that the APF is a model ready for export. Readers of this newsletter will know that governments in places as diverse as Alberta, Brazil, Iraq, Libya, and Mongolia have recently thought seriously about imitating the Alaska model.

“Some might be tempted to think that the APF isn't a true BIG and it isn't motivated to help the poor. Not so: Jay Hammond, the Republican governor of Alaska who created the APF, came all the way to Washington, D.C., to speak at the U.S. Basic Income Guarantee Network conference in 2004. He told me that his intention was to create a BIG to help everyone—most especially the disadvantaged. If he had his way the APF fund would now be producing dividends four to eight times the current individual level of $2,069.

“Others might dismiss the Alaska model saying that it is a unique case because Alaska has so much oil wealth. Again, not so: Alaska ranks only sixth in U.S. states in terms of per capita GDP, with an average income just over $43,000 in 2006, more than $15,000 per year less than number-one Delaware, and only $6,000 per year ahead of the national average. Any other state or the federal government can afford to do what Alaska has done.

“Alaska has oil wealth; other states have mining, fishing, hydroelectric, or real estate wealth. Governments give away resources to corporations all the time. The U.S. government recently gave away a large chunk of the broadcast spectrum to HDTV broadcasters at no charge. Offshore oil drilling will soon be expanded on three coasts. Everyone who emits green house gases and other pollutants into the atmosphere takes something we all value and—so far—pays nothing.

“What was different about the Alaskan situation was that Jay Hammond was there to take advantage of the opportunity. With the Alaska model in place, it will be just a little easier for next person at the next opportunity.”

There have been other times in U.S. history when the government “gave away” wealth. An example was the Homestead Act of 1862 which opened the American heartland to settlement and helped create one of the world's most productive agricultural regions. There was also a time when anyone who walked into a U.S. Mint could have their gold or silver stamped into coinage—a critical financial service offered to the public free of charge. Land grants to the railroads also helped capitalize the growth of that industry.

So why isn't a dividend like the one provided through the Alaska Permanent Fund paid to every U.S. resident or, for that matter, to every person in the world? Please don't make up any phony “economic” answers to this question. The answer is obvious—everyone else is being cheated by the monetary system.

The “Cook Plan”

What I am calling the “Cook Plan” would be an effective way to implement dividend economics. The plan is to pay each resident of the U.S. a dividend, at first by means of vouchers for the necessities of life, in the amount of $1,000 per month per capita starting immediately. It would be our fair share of the resources of the earth and the productivity of the modern industrial economy. Under the plan, the money would then be concentrated through deposit in a new network of community savings banks to capitalize lending for consumers, small businesses, and family farming.

I am calling it the “Cook Plan” because I have been advocating such measures for almost two years, every since I published my first article on the subject in April 2007 entitled: “An Emergency Program of Monetary Reform for the United States.” (See Global Research at Bailout for the People: “The Cook Plan” ) One reader who has responded favorably to the plan calls it “Trickle-Up Economics.”

Because we are talking about a dividend, there would be no means test. Everyone—rich, poor, and in-between—is entitled. The dividend would total about $3.6 trillion, which, not by coincidence, is the amount of new debt U.S. residents must incur each year from banks simply to exist. That borrowing, of course, is on top of borrowing in past years, because most people do not entirely pay off old loans before taking out new ones. Debt in this country in recent years has been cumulative, with interest constantly compounding. The annual dividend I have proposed would bring a halt to this “Grip of Death,” as it has been termed by British author Michael Rowbotham in his book: The Grip of Death: A Study of Modern Money, Debt Slavery, and Destructive Economics .

Because we have all been brainwashed to believe that the only possible sources of government funding are through taxes, user fees, or the national debt, it is difficult to believe that a dividend of $3.6 trillion could be paid to residents by other means. In fact it could, and it would not even require a fund to be set up like the Alaska Permanent Fund that is replenished by resource revenues such as oil leases. According to Social Credit theory, the dividend fund could be created sui generis ; i.e., it could be created out of “nothing.”

And why not? John Maynard Keynes pointed out, and everyone realizes today, that the banking system does just this in creating money “out of thin air.” It's what many people refer to as “printing money,” which the Federal Reserve is doing on a massive scale in bailing out the financial system.

The banks that belong to the Federal Reserve use the purchase of Treasury debt as collateral, but the money itself is issued as credit as a multiple of the reserve base. The trouble is we end up paying interest on it, which is why the interest on the national debt in the fiscal year 2009 budget totals more than $500 billion. (Of course one reason adding to the federal deficit today looks so attractive as a means of recovery is that the interest Treasury has to pay is so low—but it is still borrowing.)

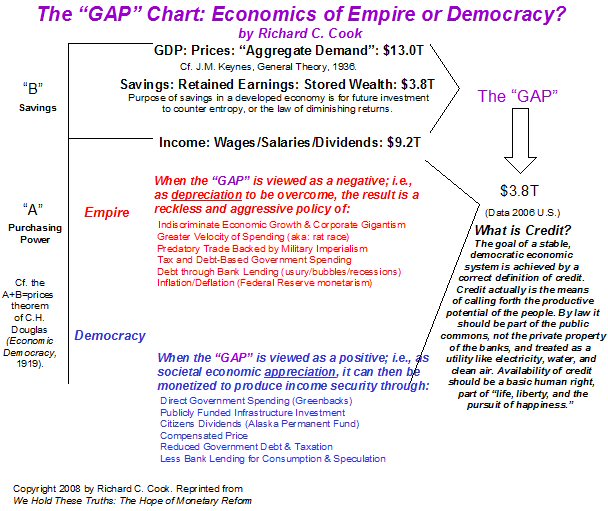

Issuance of credit is mis-defined today as the private property of the banks. I point this out in the “GAP Chart” in my book We Hold These Truths: The Hope of Monetary Reform . I state in the chart:

“The goal of a stable, democratic economic system is achieved by a correct definition of credit. Credit actually is the means of calling forth the productive potential of the people. By law it should be part of the public commons, not the private property of the banks, and treated as a utility like electricity, water, and clean air. Availability of credit should be a basic human right, part of ‘life, liberty, and the pursuit of happiness.'”

Today the banking system has a monopoly on credit which it has seized unlawfully from the government, where, under the U.S. Constitution, Congress alone, according to Article II, has the prerogative to, “coin money and regulate the value thereof.” There is no reason except bankers' propaganda why the federal government, as authorized by Congress, could not issue credit through a citizens' dividend, by direct government spending, or by other means such as loan guarantees or grants/loans for infrastructure. This would be real economic democracy.

The “GAP” Chart is presented in its entirety as follows. What the model shows how we can monetize the productive potential of the nation that today is held back by businesses from payout as wages, salaries, and dividends through the withholding of retained earnings. It is these retained earnings that the business will utilize later to renew its processes of production through investment. But while these funds are idle, their creative potential still exists. That potential is the “energy source” for new consumer purchasing power. It is real, though, like electricity, invisible until harnessed.

As I explain in We Hold These Truths: The Hope of Monetary Reform :

“In order for people to be able to pay for a nation's GDP, sufficient purchasing power must be generated. Purchasing power is what British economist John Maynard Keynes called ‘aggregate demand.' But the income that is generated through wages, salaries, and dividends is never enough to consume the GDP, because a portion must be withheld (saved) as retained earnings for future investment. This is the ‘gap.' The way society decides to fill the gap reflects whether it views itself as an empire, where the rich profit at the expense of the many, or a democracy, where all members of society have the opportunity to prosper. Under the imperial design, the ‘gap' is viewed negatively and filled by bank lending at usurious rates of interest, foreign conquest, the economic growth imperative, aggressive trade policies, or inflation of the currency. But when, by contrast, the ‘gap' is viewed as an opportunity to further democratic ideals, it can be monetized through public control of credit and issued as direct government spending, a citizens' dividend, or low-cost credit. This monetization of savings reflects a definition of credit as a public utility, not the private property of the banks. Keynesian economics tries to compromise between the imperial and democratic ideals by using government debt to monetize savings, but this ultimately destroys the currency through bankruptcy or inflation. Today we are at a late stage of imperialistic monetary policies which have led to financial collapse. Democratic management of credit has been tried at various times in U.S. history with great success [e.g., through the Greenbacks] but never on a sufficient scale to transform the economy. It is now time to take decisive measures to replace the economics of empire with those of democracy.”

Under the “Cook Plan,” the U.S. Treasury would issue the dividend against an account that represents the productive potential of the nation once the money is spent. As stated earlier, the dividend would not be inflationary, because it would replaced money borrowed from banks for consumption and would be matched by the production of new goods and services within the physical economy.

In fact a dividend would have far less tendency to inflate than do Federal Reserve Notes, because it would not have bank interest charges added to it which ended up in prices charged consumers at the point-of-sale. And once created the dividend would remain in circulation—or deposited as savings—because it would not have to go back to a bank to be canceled as loans now do.

Savings would also be an important part of the plan, because today citizens have completely lost the ability to save in the usury-based economy where cancellation of bank credit along with the interest charged sucks up all available cash from people's pockets. And the dividend would not be taxed.

The dividend would be issued as vouchers as a temporary measure until the program caught on and it was clear the money would be spent responsibly. The vouchers would be redeemable at any location licensed to do business for necessities of life such as food, housing, transportation, clothing, communications, or business/home maintenance. In fact they could be used for most purchases except things like the lottery, alcohol, entertainment, etc.

Once received in transactions, providers would then deposit the vouchers in the community savings bank that had been set up in their locality. In order to maintain membership in the bank, providers would be required to keep a certain amount of money on deposit to capitalize lending by the bank within the community. Loans would be made available under the bank's fractional reserve privileges and would be issued at low rates of interest, preferably no more than one percent plus a premium for default insurance, depending on the credit status of the borrower. Persons eligible for lending would include individuals, householders, students, small businesses, local manufacturing concerns, family farmers, etc.

It should be obvious that this system would completely transform and revitalize local economies in any nation where it were implemented. One of the worst features of today's usury-based economy takes place when global companies in league with the banks come into communities and destroy local businesses by underpricing them. Then these companies extract all the liquidity from the community, where people usually are so cash-poor they buy mainly with credit cards, and return only a fraction to the low-wage workers they employ.

The “Cook Plan,” with the direct injection of purchasing power into the community through vouchers, combined with a new system of low-cost credit, would transform this dire situation completely. It would allow people to live and prosper without dependence on credit cards, government job-creation programs, or government welfare bureaucracies. And it would allow a resurgence of volunteer activities and work at lower-paying professions such as family farming, education, and the arts.

In fairness to Paul Krugman, he does propose spending not tied to employment as well as tax cuts. In his Rolling Stone open letter to President Obama he states that:

“…aid to the distressed - enhanced unemployment insurance, food stamps, health-insurance subsidies - is both the fair thing to do and a desirable part of your short-term economic plan.”

This is not far from advocating a Basic Income Guarantee, except that, once again, Krugman would fund such spending from federal borrowing. But he is leaning in the right direction. A little further and he will arrive at the “Cook Plan,” which would have a much better chance of fulfilling President Obama's campaign slogan of rebuilding the economy “from the bottom up” than what is the essentially top-down government-directed program his administration is now proposing.

What amount would the stimulus add up to? The “Cook Plan” would result in $3.6 trillion the first year of implementation being directly added to consumer income, or about 25 percent of the GDP. Debts could be repaid, money could be saved, the necessities of life would be assured, and a renaissance in local, rural, and regional economies would come about within a few years.

Finally we would have the “leisure dividend” the industrial age promised but never delivered. And we would have resolved the “Curse of Plenty” cited in the quotation from Winston Churchill at the start of this paper. These objectives would be achieved not through the chimera of government-engineered “full employment”; i.e., socialism, but through income security leading to real economic freedom and democracy.

The proposal encapsulates the essence of dividend economics by acknowledging the right of the individual to obtain a significant measure of economic freedom through the fact of membership in a society that is heir to the genius of past generations in creating the material environment in which we live.

This heritage is not the property of the banks, and it is not the property of the government. It is the property of the people. The conservative model of government exemplified by the ideology of today's Republican Party subjects people to a bank-run collectivism. And even the most benign progressive model exemplified by ideology of the Democratic Party still subjects us to the collectivism of tax-borrow-and-spend job-creation programs that may or may not work.

So let a national system of dividend economics now be implemented, a plan that draws on much of the wisdom that has been dormant in recent decades as the Empire of Usury has suffocated the life out of the world's economy. It is now time to put that wisdom to work. “We the People” deserve to live in freedom on this beautiful planet, no matter what the bankers say. In fact such a program would be a major step upward in human social evolution.

Do It Now

Obviously it would take time—though not much time—to work out all the details of the program. But in principle, the “Cook Plan” is sound, with the total dividend being recalculated each year. Remember again that the dividend takes a power of nature and what should be a public utility—credit—and gives it back to the people as a human right rather than the private property of the banks. We cannot afford to wait. Conditions today are nearing an emergency. Thousands of people are losing their jobs every day as the recession turns into a monster.

Wallace Klinck sums it up

“If society had followed the Social Credit policy of C. H. Douglas who advocated Consumer Dividends and Compensated Retail Prices instead of the Fabian Socialist social debt policy of the late economist John Maynard Keynes, none of the current madness would have occurred. We would be enjoying increasing prosperity with falling prices and increasing leisure as should be the case in any modern and civilized society.”

By Richard C. Cook

http:// www.richardccook.com

Copyright 2009 by Richard C. Cook

Richard C. Cook is a former U.S. federal government analyst, whose career included service with the U.S. Civil Service Commission, the Food and Drug Administration, the Carter White House, NASA, and the U.S. Treasury Department. His articles on economics, politics, and space policy have appeared on numerous websites. His new book, We Hold These Truths: The Hope of Monetary Reform , can now be ordered for $19.95 from www.tendrilpress.com . He is also the author of Challenger Revealed: An Insider's Account of How the Reagan Administration Caused the Greatest Tragedy of the Space Age , called by one reviewer, “the most important spaceflight book of the last twenty years . ” His Challenger website is at www.richardccook.com . A new economics website at www.RealSustainableLiving.com is upcoming with partner/author Susan Boskey.

Richard C. Cook Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.