U.S. and Global Economic Forecast 2011, Russia and the Roots of World Inflation

Economics / US Economy Jan 09, 2011 - 08:39 AM GMTBy: John_Mauldin

It is time once again to throw caution and wisdom to the wind and actually make my 11th annual forecast. I have to admit this is the most stressful letter I write each year. I do at least 5-10 times more research and thinking about this issue than any other. On a positive note, this may be one of the more optimistic forecast letters I have done in a long time. But there are some asterisks, as always. We will survey the world, trying to peer through the fog of the future. There are some very interesting side trails we will want to explore. Did you know some events in Russia could have real ramifications for inflation in China, the US, and the world? I pay attention to the background details and bring them to you. So settle back as we tour the world.

It is time once again to throw caution and wisdom to the wind and actually make my 11th annual forecast. I have to admit this is the most stressful letter I write each year. I do at least 5-10 times more research and thinking about this issue than any other. On a positive note, this may be one of the more optimistic forecast letters I have done in a long time. But there are some asterisks, as always. We will survey the world, trying to peer through the fog of the future. There are some very interesting side trails we will want to explore. Did you know some events in Russia could have real ramifications for inflation in China, the US, and the world? I pay attention to the background details and bring them to you. So settle back as we tour the world.

But first, as you are fastening your seat belts, I am proud to announce that FINALLY we are a full go on my new web sites, which have been in soft launch for a few weeks. The main site is now www.johnmauldin.com, where you can access everything I do, including Thoughts from the Frontline and Outside the Box, as well as ten years' worth of archives.

There's a lot that's new, as Tiffani is dragging me into the new world of Internet 2.0. Our old site was so '90s. Now we are the cutting edge. Everything is done in HTML 5, and we are one of the first and few financially oriented sites to use this new code. Very crisp and clean.

But more importantly to you, we have ways for you to interact with me and the "Mauldin Community." You can comment on each weekly Thoughts from the Frontline and Outside the Box, and I will read your comments. There is a forum where you can join the community and discuss topics I bring up, whether you agree with me or not. I have always contended that my readers are the smartest, most well-informed of any writer's, and now you can benefit from your collective wisdom.

The only general rule is that you have to be civil and have some sense of decorum.

At least on the small part of the Web I own, there will be a sense of dignity and probity. You can disagree with me or some other commenter to your heart's content, and I encourage it, as that is the way I (and we) learn; but no flame mails, no casting aspersions on anyone's character because of the views they hold.

I will also be doing voice podcasts that we call The Mauldin Minute. And you can view my latest media spots. Want to ask me a question? There's a spot for them in the upper left-hand corner of our home page, and each week I will pick 1-3 questions to respond to. Rule: it has to be a question that does not need a book chapter or an e-letter to answer!

We also have a new site called The Mauldin Circle, where you can find investment professionals around the world who can help you find appropriate investments, generally in the alternative space, which can add some real diversification to your portfolio. (If you have signed up for the accredited investor letter in the past, you do not need to do so again. In this regard, I am president of and a registered representative of Millennium Wave Securities, LLC, member FINRA.)

If you have a minute, go to www.johnmauldin.com, put in your email address, and sign up. (You won't get two copies of my letters if you are already on the list!) Tiffani and I really would like your feedback on the new site.

And now on to the topics of Forecast 2011, in no particular order.

How Did We Do in 2010?

I rarely go back and read my annual forecast until the following year, and this year was no exception. So I was pleasantly surprised to see that my batting average was pretty good. You can read the first two letters of last January, which comprised the forecast, at http://www.johnmauldin.com/frontlinethoughts/archive/2010/01/.

After noting my bearishness on the yen, euro, and pound (against the dollar), I wrote:

"So, where are the strong currencies going forward? The Canadian dollar is on its way to parity. I would want to own the Aussie, if I was a trader. Maybe the Swiss franc, although it is so high on a parity-value basis right now. [Note: if the Swissie was high this time last year, it is wildly overvalued now. And there is nothing the Swiss can seemingly do about it. Their central bank has lost billions trying to fight appreciation against the euro. As Dennis Gartman notes, this fighting the euro may be the all-time largest losing trade in history.]

"But the currency I want the most if I am a central banker [or an individual] is that barbaric yellow relic, gold. Just as India has recently bought 200 tons of gold, I think central banks in other emerging nations will want to buy more, too. [They continued to do so!] They all have relatively little gold as a percentage of their reserves. Look for that to change.

"I also like gold in terms of the euro, the pound, and the yen - more than I like it in terms of the US dollar, but even there I like gold long-term, at least until we get some fiscal sanity."

I think that is reasonable for this year as well. I am less pound-bearish than I was a year ago, as it has already dropped a lot, but think the yen and euro could come under real pressure. The Canadian loonie blew through parity, but is still strong. I think the Aussie dollar could see some relative weakness this year, for reasons we will go into later, and I think a basket of Asian currencies will be the stronger bet. Asian countries must deal with higher inflation by tightening monetary policy or allowing their currencies to rise. I think it will be the latter, as they will not want to choke off growth with higher rates, which would attract more dollars and mean potential capital controls on the order of Brazil's.

I was bearish on equities in 2010, which was the right stance in the US until late August, when Bernanke gave his Jackson Hole speech, telling us that we would see QE2, which set up rallies all over the world. Things change. I have to admit I was somewhat surprised he decided to launch QE2. I think it is ill-advised, and that money is now setting up bubbles in emerging markets and commodities. But they are going to continue until June. What will happen then? Not much, as monetary policy has a time lag, but it suggest headwinds in risk assets beginning late in the year.

While on the stock market, let me revisit a theme from a few weeks ago. There are all sorts of indicators from any number of services that I follow that are telling us about the possibility of a short-term sell-off. But given that the Fed and other major central banks are maintaining an easy stance, the medium-term outlook following a drop should be a return to a bullish trend.

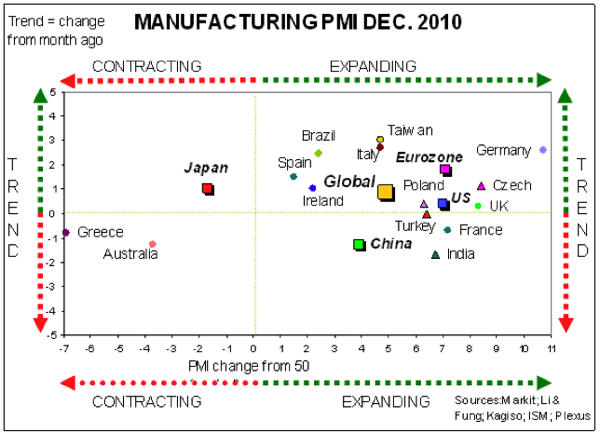

My friend Dr. Prieur du Plessis of Plexus, in South Africa, sent me the following graphs about world Purchasing Manager Indexes (the equivalent of ISM in the US), for both manufacturing and services. Source: Investment Postcards (You can sign up for free if you like.)

What you will notice is that most of the world except Japan, Greece, and Australia is expanding in the manufacturing chart below, some countries aggressively so, like Germany. Globally, the world is expanding and (subject to the caveats later in the letter) should continue to do so this year.

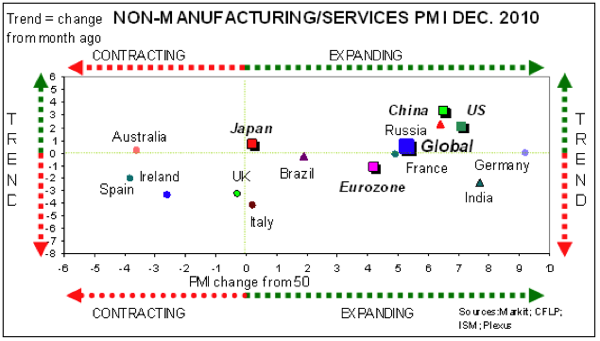

And below is an estimation of what the services chart looks like. Again, most countries are in an expansion mode. It is rather interesting to see which countries are doing well in both sectors, and it seems odd that Australia is not doing all that well in either.

Russia and the Roots of World Inflation

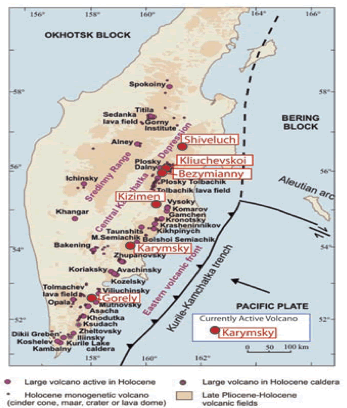

I hinted at something in Russia that threatens to cause inflation. No, it is not some nefarious scheme by Putin or Medvedev. It is Kamchatka, or more specifically volcanic activity in the Kamchatka Peninsula. There is a reason the weather is so harsh this winter, and a big part of that is Kamchatka.

I am a voracious consumer of information from a wide variety of sources. Most of it never gets into this letter, but it helps me understand what is going on in the background. As my friend Don Coxe says, it is what is on page 16 that will be important in the future. I read a lot of page 16s.

One of those "Outside the Box" sources is the Browning Newsletter on climatology, a completely different look at weather from the normal meteorological view we get in newspapers and on TV. Started some 36 years ago by Ibn Browning, famed and (then somewhat) controversial climatologist, it is continued today by his daughter Evelyn Browning Gariss. As an aside, I met Ibn many years ago, when he would regularly speak at the New Orleans conference. He was fascinating and brilliant.

Climate as a whole goes through cycles. If we look to the past, we can better understand the future. Evelyn Browning Garriss has succeeded with this idea for 20+ years. Each month, I get her letter on weather patterns. It is somewhat technical, and admittedly will take a few issues and some study to get your head around, but once you do, oh my. There is a reason Australia is undergoing severe rains and that the north of the US and Europe are experiencing serious winters.

First, the Pacific is going through a cooler period, called La Nina (with this one being particularly strong), and the Atlantic is going through a warmer period. This would normally change weather patterns in rather predictable ways. But then throw in the Kamchatka volcanoes, which are throwing massive amounts of dust into the air, causing the Arctic to be even colder and Arctic winds to push farther south, and you get a very drastic change in patterns.

Australia's wheat crop is down by 10%, but the bulk of it has been so damaged by the worst rain in a hundred years (by far) that it is no good as human food and can only be used to feed animals. Throw in drought in Russia, severe drought in Argentina, floods in Brazil and Venezuela, odd weather in the agricultural parts of China, and you get rising food costs all over the world - all because Putin cannot keep his volcanoes under control. (But hey, he's controlling everything else!)

If those volcanoes don't back down, there is the real possibility that this year's bad weather could repeat.

As Evelyn writes this month:

"Basically, both the Pacific and Bering plates are subducting (sliding beneath) under [the Kamchatka Peninsula] and each other. Just as fenders crumple during a car wreck, so the Kamchatka Peninsula surface is buckling with mountain ranges. When the ocean plates sink deep enough, portions are melted by the intense heat generated within the mantle, turning the solid rock into molten magma. The magma bubbles up through the crust, ultimately bursting to the surface and forming volcanic eruptions.

"As a result of all this geological activity, Kamchatka tends to be somewhat active - but recently it has been ridiculous! Since late November, Kizimen, Sheveluch, Karymsky, and Kliuchevskoi have been erupting almost constantly. Most of the eruptions have ranged from 2-10 km (1.2-6.2 miles) high. While the smallest eruptions have caused only minor local disruptions, the larger ones have entered passing fronts, cooling temperatures, altering air pressure, and increasing precipitation.

"Volcanic ash screens out incoming temperature, cooling the air below. This lowers air pressures which, in turn, changes wind patterns. In particular, in polar regions it appears to weaken the Arctic Oscillation winds. When the Arctic Oscillation turns negative, that is, when the winds weaken, the cold air normally trapped around the North Pole surges south."

She was writing months ago about the weather that we see today, so when she tells us that it's possible we'll see a repeat next year, I pay attention. This could further exacerbate food costs and force emerging-market central bankers to fight inflation by allowing their currencies to rise. Weather makes a difference.

For those interested, I have asked Evelyn to allow me to post her latest January letter on my website, at http://www.johnmauldin.com/frontlinethoughts/special/browning-newsletter-1210. For those as obsessed as I, or who are hedge funds that run serious money, you can subscribe at www.browningnewsletter.com. It is only $250 a year, which is cheap for what it offers, at least in my opinion.

The US Will More than Muddle Through

I think of a Muddle Through Economy as around 2% growth. That is enough to keep things going forward, but not enough to substantially dig into unemployment or raise incomes. The entire last decade was a Muddle Through decade, with growth averaging 1.9%. After I wrote about a Muddle Through decade at the beginning of the last one (in 2002), I caught some flack during the middle years of the decade. Turns out to have been a pretty good call, though. I still think we are in for a repeat, over the coming decade, of slower growth on average than we would like, but not this year. Let's look at some reasons why.

First, the Bush tax cuts were extended. Not doing so would have put us into recession. One could make an argument that not extending them for the rich would not have pushed us back into recession, but it would have been the wrong policy at a time of high unemployment.

Somewhere between 50-70%, depending on whom you want to listen to, of the "rich" are small business owners. I know something about the entrepreneurial mindset, as I am a serial entrepreneur. I do two things when I get some extra money: I invest some and then look for ways to put it to work to grow my business. The more I have the more I try to grow the business.

That is the way the entrepreneurial mind works. For whatever reason, we want to grow, whether we are running a Korean deli in Manhattan or a financial services firm or an electronics manufacturing company. We look for new markets and products, which usually means more jobs. When times get slow we pull back, hoping to last until things get better.

Small businesses are the backbone of job creation in the US. Yes, some rich lawyers and bankers get by with lower taxes, but that is the price of leaving businesses with more of their profits to reinvest.

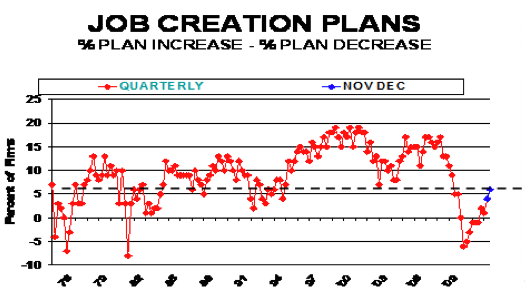

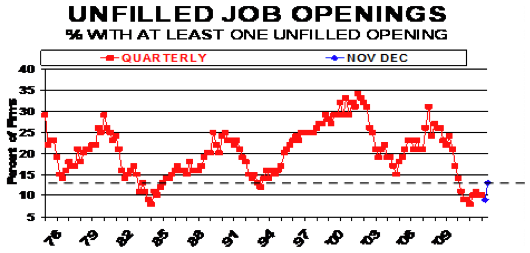

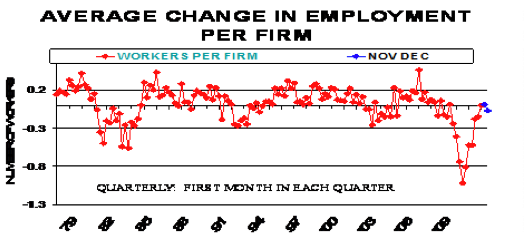

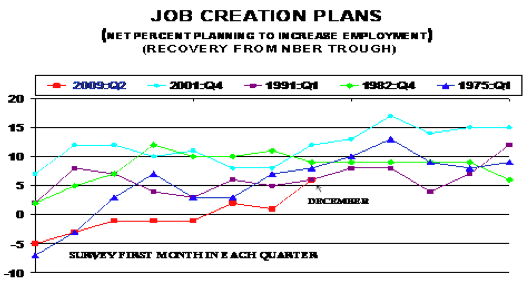

My friend Bill "Dunk" Dunkelberg, Chief Economist of the National Federation of Independent Business, notes that prospects for future job growth look better than at any time since the beginning of the Great Recession. Look at the graphs from his latest survey:

"Reports of net job creation continued to oscillate around the "0" line in December. Asked about changes in total employment over the last three months, 13% of owners reported increasing employment at their firms by an average of 3.5 workers while 14% reported reducing total employment an average of 2.9 workers per firm. Clearly, no surge in hiring in December. This produced a reduction of -0.07 workers per firm, basically unchanged from the "0" October reading and +0.01 reading in November. In normal times, this measure would be in the range of 0.1 to 0.2 workers per firm (chart below). Still, the percent reporting higher employment levels is the second highest reading since December, 2007 (the peak of the last expansion according to the National Bureau of Economic Research) and the percent of owners reporting lower employment was down 2 points from November.

"The good news is that the two job creation indicators, job openings and job creation plans both reached new recovery highs. The percent of owners reporting hard-to-fill job openings rose 4 points to 13 percent, the best reading in 24 months. This indicates that the unemployment rate should improve in December and the months ahead. Plans to create jobs gained 2 points, rising to a net 6% of all owners, the best reading in 27 months. These indicators point to a pickup in job creation activity in the first quarter of 2011. But the small business sector continues to underperform on job creation in this recovery compared to other recovery periods (charts below)."

Looking at the charts below, we can see a bit of light at the end of the unemployment tunnel.

December Unemployment Better than Headline

I know that everyone expects me to tell them that the headline number of 103,000 was too soft. And on the surface they would be right. But there were revisions of a plus 70,000 for the last two months. We have now seen four months of upward revisions in a row. (More on that later.)

And the household survey showed an increase of 297,000 jobs. If you adjust that to match the establishment survey, it would show a surge of 500,000 jobs! Now, the household versus the establishment surveys are extremely noisy, as the following chart from my fishing buddy Stuart Hoffman of PNC shows. Note the wide divergences of the last five months.

At the risk of boring long-time readers, let me address the problem of the unemployment numbers at turning points in the economy. The establishment survey, which is the number we read as the "headline" number, is created by calling up a statistically significant percentage of established businesses every month and asking them how many people they employ. Almost by definition they do not poll small businesses and start-ups, which is where the job creation really happens. They have to make an estimate of those jobs, and this is called the birth/death ratio.

The B/D ratio is based upon past trends. There is no other way to do it. The BLS does its best at guessing the right number in a systematic way. And usually it is not all that bad a guess. Except - except - at turning points in the economy. When the economy starts to recover from recession, they underestimate the number of jobs. When the economy is rolling over into recession, the trends they use force them to overestimate the number of jobs. As the years go by and they get better data, they go back and revise their numbers.

Remember the jobless recovery of the Bush years? A few years later, it turned out that job growth was pretty good, at least compared with the initial estimates. But did anybody care three years later? Did it make the front page of the Wall Street Journal? No, as no one cares a lick about old data.

The key is to watch the direction of the monthly revisions. As noted above, it is now four months of upward revisions. That is a positive. We need that to continue.

The negative is that it will be years before we get back to a 5% unemployment rate. We will need 5-6 years of 2.5 - 3 million jobs a year to get there. We have never done even two years in a row like that. Unemployment is still going to be a headwind for some time to come, and that is likely to keep a lid on incomes, which is not good for final sales. As David Rosenberg notes:

"While the details were obviously better than the headline, it would be a mistake to read much into the unexpected decline in the unemployment rate, which fell to 9.4% from 9.8% - the lowest it has been since May 2009 (when the economy was still technically in recession) and the sharpest one-month decline since April 1998. While some of this 'decline' did indeed reflect the rebound in Household employment, it was largely due to the sharp decline in the labor force participation rate, which tumbled to a 27-year low of 64.3% in December from 64.5% in each of the prior two months. The culprit: discouraged workers soared to a new record high of 1.32 million."

As employment starts to actually rise, people who have give up looking for work will want to come back into the workforce. As they start looking for jobs, they will be counted as unemployed. And then the unemployment number will stay stubbornly high.

A Very Fluid Economy

My friend John Vogel does private analysis of the employment numbers every week and shares the results with a few of us. He did a longer opus this week, talking about the very fluid job picture in the US. If you add up all the initial jobless claims from 2006 through 2009, the number is 83,772,000 lost jobs. Yet during that same period we must have created 81,258,000 jobs, for the BLS numbers to balance. In the last year (11 months), we saw 21,696,000 initial unemployment claims, yet we created 25,893,000 jobs.

We have 130 million people working in the US, but that is down from 137.6 million in 2007, and less than were employed ten years ago, in 2000. But that also means some 15% of all workers had to find new jobs last year, not even counting those who left willingly to go to another job. I seem to remember that if you count the latter, the number goes to some 20% of US workers changing jobs each year.

That seemed rather high to me until I thought about my own seven kids, six of whom are in the workforce. On average for them, 20% change a year (one job every five years) would be rather low. Admittedly, they are young, but it does give some credence to the BLS numbers, which show how fluid the US job market really is.

My deep fear, as we leave this topic, is that we are creating a structurally unemployed or underemployed class of workers, people with skills that are not keeping up with the times or who are chronically undereducated. The McCormick reaper and the tractor put tens of millions of farm workers out of a job, forcing them to go to the cities and learn new skills. Who would want to go back to the 1860s, when the majority of the US population worked on farms? But that was a time of tremendous upheaval. I think we are facing such a time ourselves.

Wrapping up for this week, I think the US grows at 2.5 - 3% GDP this year, with the world doing better and Europe ex-Germany much worse. Much of peripheral Europe may fall into recession.

Next week we will finish the forecast (the letter is long enough for this week), where we will deal with the things that could make my somewhat rosy forecast look rather Pollyannaish. Mostly Europe, but we need to look carefully at China as well. And commodities, the emerging markets, and a few other things. But now it's time to hit the send button.

Cabo, LA, Winnipeg, Meet Me in Vegas, and Thailand

If you are an investment advisor or broker, meet me in Las Vegas, where I will be speaking for my partner Steve Blumenthal of CMG on February 3-4. We have a very solid lineup, including Christopher Geczy, Ph.D. of Wharton, at the CMG Investment Forum. Go to http://cmgfunds.net/sys/docs/234/Feb%20Las%20Vegas%20Invitation.pdf to learn more.

Tomorrow (actually later this morning, as it is now late) I leave with Tiffani and Ryan (and granddaughter Lively!) to go to Cabo San Lucas to meet with Jon Sundt and the partners at Altegris for our annual strategy session. They won this cool villa at a charity auction, so we get to work in splendid surroundings, complete with fresh guacamole. Home Tuesday night, then we go back west to LA to meet with Ken Aldrich and the team at ISCO, and then I'll attend a charity event with my good friend Lee Stein. Then back home on Sunday.

I'll go to Winnipeg, where Evelyn Browning Gariss tells me it will still be cold, to speak at the 46th annual CFA Forecast Dinner. The event is open to the public. You can learn more by sending a note to info@cfawinnipeg.ca.

Thailand? Japan? Miami? The Barefoot Ranch in East Texas? All within the next two months. Busy, but I love it. And then my new book, called Endgame: The End of the Debt Supercycle, comes out in March, so that means a lot of travel as well, plus Europe. I will probably get my miles again this year.

Finally, last year I attended a 13-day executive program where experts from many different fields brought us up to date on where their respective fields were headed. Quite the gathering of futurists. This year Singularity University will hold an Executive 7-Day Program April 1-8, at a cost of $12,000, at the NASA Ames Research Park in Mountain View, California. It is worth every penny if you need to know where the world is going. You can get more information at http://singularityu.org/programs/executive-programs/.

It really is time to hit the send button now. Have a great week, and enjoy yourself.

Your ready for some guacamole and margaritas analyst,

John F. Mauldin

johnmauldin@investorsinsight.com

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2010 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.