The Burden of Lower Economic Growth and Frequent Recessions

Economics / US Economy Feb 05, 2011 - 12:13 PM GMTBy: John_Mauldin

"My best guess is that we'll have a continued recovery, but it won't feel terrific. Even though technically we'll be in recovery and the economy will be growing, unemployment will still be high for a while and that means that a lot of people will be under financial stress." -- Benjamin Bernanke, Chairman of the Federal Reserve in a Q&A at the Woodrow Wilson International Center for Scholars

"My best guess is that we'll have a continued recovery, but it won't feel terrific. Even though technically we'll be in recovery and the economy will be growing, unemployment will still be high for a while and that means that a lot of people will be under financial stress." -- Benjamin Bernanke, Chairman of the Federal Reserve in a Q&A at the Woodrow Wilson International Center for Scholars

Tonight (Thursday) I am flying to Thailand and will "lose" my normal Friday writing day, so I am going to give you a preview of my new book, Endgame, out and in the bookstores next month. This is the beginning of chapter four, and it stands alone quite nicely. It will print out a little longer than normal, as there are a lot of graphs. My co-author Jonathan Tepper and I deal with why there will be slower growth, more volatility, and more frequent recessions in our future.

And I want to ask a favor of my 1 million closest friends. It's a long story, but if you pre-order at Amazon or other online stores, there is a high probability that the sale does not count in the NYT bestseller list sales. Besides the small amount of ego involved, making the list will drive sales and major media invitations. I have written the book to try and help foment the various national conversations that must be had around the world about getting our fiscal houses (and sanity) in order. The more people who read this book, the better the chances that something will get done. Or at least that is my hope. So, wait until I tell you it is time to order the book online if you can, or tell your local bookstore to go ahead and get you a copy. That you can do now. Thanks.

Quick note: I will be speaking in Phoenix at the Phoenix Investment Conference & Silver Summit February 18-19, 2011, at the Renaissance Glendale Hotel and Spa. Attendance is free. You can register at http://www.cambridgehouse.com. The conference focuses on metals and mining, and if that is among your interests, check it out.

And now, let's look at the first half of chapter four of my book Endgame.

The Burden of Lower Growth and More Frequent Recessions

We're optimists by nature. The natural order of the world is growth. Trees tend to grow, and economies do, too. Real economic growth solves most problems and is the best antidote to high deficits, but the problems that we have now won't be solved by growth. They're simply too big. Unless we have another Industrial Revolution or another profound technological revolution like electrification in the 1920s or the IT revolution in the 1990s, we will not be able to grow enough to pull ourselves out of the debt hole we're in.

After the dot-com bust in 2000, the phrase "the muddle through economy" (a term coined by John) best described the U.S. economic situation. The economy would indeed be growing, but the growth would be below the long-term trend (which in the United States is about 3.3 percent) for the rest of the decade. (Indeed, growth for the decade was an anemic 1.9 percent annualized, the weakest decade since the Great Depression. Muddle through, indeed.)

The muddle through economy would be more susceptible to recession. It would be an economy that would move forward burdened with the heavy baggage of old problems while facing the strong headwinds of new challenges. The description of the world was accurate then, and it is even more accurate now. In March 2009, when almost everyone was predicting the apocalypse, it was hard to see how things could improve. The GDP turned around, industrial production has shot up, retail sales have bounced back, and the stock market rebounded strongly. Everything has turned up. However, GDP growth is slowing in the United States as we write in November 2010. Compared with previous recoveries, growth does not look that great, and people don't feel the recovery. This is unlikely to change.

The muddle through economy is the product of a few major structural breaks in the world's economies that have important implications for growth, jobs, and when we might see a recession again. The U.S. and most developed economies are currently facing many major headwinds that will mean that going forward, we'll have slower economic growth, more recessions, and higher unemployment. All of these are hugely important for endgame since they vastly complicate policy making.

Lower growth will make our fiscal choices that much scarier. Importantly, these big changes also mean that governments, pension funds, and even private savers are probably making unreasonably rosy assumptions about how quickly the economy and asset prices will be able to increase in the future. As endgame unfolds, the reality of these big changes will set in.

Three Structural Changes

Investors are good at absorbing short-term information, but they are much less successful at absorbing bigger structural trends and understanding when secular breaks have occurred. Perhaps investors are like the proverbial frogs in the frying pan and do not notice long, slow changes around them. There are three large structural changes that have happened slowly over time that we expect to continue going forward. The U.S. economy will have:

1. Higher volatility 2. Lower trend growth 3. Higher structural levels of unemployment (The United States here is a proxy for many developed countries with similar problems, so much of this chapter applies elsewhere.)

1. Higher Volatility

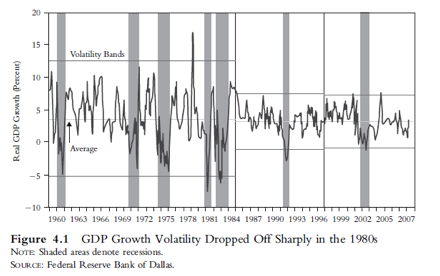

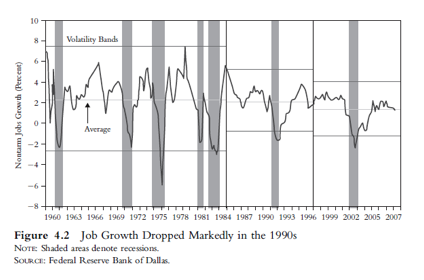

Before the crash of October 2008, the world was living in "the great moderation," a phrase coined by Harvard economist James Stock to describe the change in economic variables in the mid-1980s, such as GDP, industrial production, monthly payroll employment, and the unemployment rate, which all began to show a decline in volatility. As Figures 4.1 and 4.2 from the Federal Reserve Bank of Dallas show, the early 1980s in fact constituted a structural break in macroeconomic volatility. The GDP became a lot less volatile. As did employment.

The great moderation was seductive, and government officials, hedge fund managers, bankers, and even journalists believed "this time is different." Journalists like Gerard Baker of the Times of London wrote in January 2007: Welcome to "the Great Moderation": Historians will marvel at the stability of our era. Economists are debating the causes of the Great Moderation enthusiastically and, unusually, they are in broad agreement.

Good policy has played a part: central banks have got much better at timing interest rate moves to smooth out the curves of economic progress. But the really important reason tells us much more about the best way to manage economies. It is the liberation of markets and the opening-up of choice that lie at the root of the transformation. The deregulation of financial markets over the Anglo-Saxon world in the 1980s had a damping effect on the fluctuations of the business cycle ... The economies that took the most aggressive measures to free their markets reaped the biggest rewards.

In retrospect, this line of thinking looks hopelessly optimistic, even deluded. We do not write this to pick on Gerard Baker, but rather to point out that low volatility breeds complacency and increased risk taking. The greater predictability in economic and financial performance led hedge funds to hold less capital and to be less concerned with the liquidity of their positions.

Those heady days are now over, and we have now entered "the great immoderation." One can confidently say that 2008 represents a structural break, moving back toward a period of greater volatility. Robert F. Engle, a finance professor at New York University who was the Nobel laureate in economics in 2003, has shown that periods of greatest volatility are predictable. Market sessions with particularly good or bad returns don't occur randomly but tend to be clustered together. The market's behavior illustrates this clustering. Volatility follows the credit cycle like night follows day, and periods following credit booms are marked by high volatility, for example, 2000-2003 and 2007-2008.

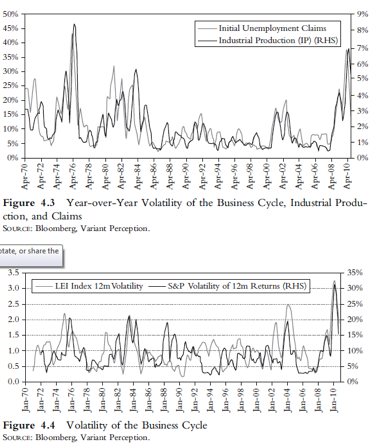

The period of low volatility of GDP, industrial production, and initial unemployment claims is now over. For a period of more than 20 years, excluding the brief 2001-2002 recession, volatility of real economic data was extremely low, as Figure 4.3 shows. Going forward, higher economic volatility, combined with a secular downtrend in economic growth, will create more frequent recessions. This is likely to lead to more market volatility as well.

You can measure economic volatility in a variety of ways. Our preferred way is on a forward-looking basis. We have seen the highest volatility in the last 40 years across leading indicators, as Figure 4.4 shows. These typically lead the economic cycle. This only means one thing, higher volatility going forward.

For far too long, volatility was low and bred investor complacency. Going forward, we can expect a lot more economic and market volatility. We have had a strong cyclical upturn, but we will continue to face major structural headwinds. This means more frequent recessions and resultant higher volatility.

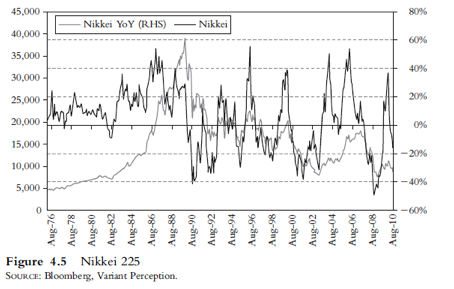

If we look at Japan following the Nikkei bust in 1989, we can see that volatility increased. Note that before the peak in the Nikkei, volatility had been largely subdued, with periodic movements corresponding to increases in the level of the market. As Figure 4.5 shows, following the crash, stock market volatility increased markedly, and volatility to the downside became far more prevalent.

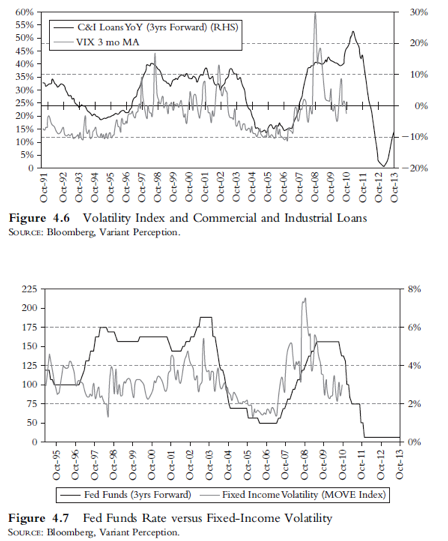

Equity volatility follows the credit cycle. If you push commercial and industrial (C&I) loans forward two years, it predicts increases in the Market Volatility Index (VIX) almost down to the month. We should expect heightened episodes of volatility for the next two years at a minimum. (See Figure 4.6.)

Fixed-income volatility also follows the credit cycle with a two-year lag. Figure 4.7 shows how the Fed Funds rate lags Merrill Lynch's MOVE Index, which is a measure of fixed-income volatility, by three years.

Another very good reason to believe we'll continue to have high volatility even after we recover from the hangover of the credit binge is that the world is now much more integrated. This is a paradox and may seem hard to believe, but increased globalization actually makes the world more volatile through extended supply chains! (See Figure 4.8.)

Production in Japan, Germany, Korea, and Taiwan fell far more during the 2007-2009 recession than U.S. production fell even during the Great Depression. Not only was the downturn steeper than during the Great Depression but also the bounce back was even bigger.

This is truly staggering. If you believed in globalization, supply chain management, and deregulation, you would have thought they would lead to greater moderation, but the opposite happened. This was due to the credit freeze that particularly hit export-oriented economies because trade credit temporarily dried up. It was not about globalization per se.

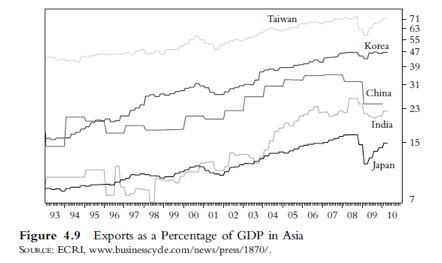

Why has the world economy been so volatile? One of the main reasons is exports. If you look at exports as a percentage of GDP since the end of the Cold War, you'll see that in almost all countries around the world, exports have rapidly risen in the last 20 years. In Asia, they have doubled, in India they have tripled, and in the United States they have increased by 50 percent. This makes us all more interconnected, and it means that supply chains become longer and longer.

Longer supply chains have enormous macroeconomic implications. As the Economic Cycle Research Institute points out, we're now experiencing the bullwhip effect, "where relatively mild fluctuations in end demand are dramatically amplified up the supply chain, just as a flick of the wrist sends the tip of a bullwhip flying in a great arc." The bullwhip effect makes greater export dependence very dangerous to supplier countries, which only contributes to cyclical volatility. This is easily seen in Figure 4.9. That is why Asian countries had some of the largest downturns and steepest upturns in the Great Recession and the following recovery.

2. Lower Trend Growth

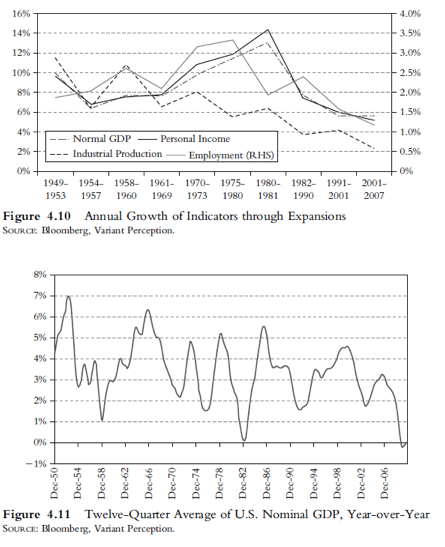

We are also seeing a secular decline over the last four cycles in trend growth across GDP, personal income, industrial production, and employment. You can see that in Figure 4.10.

Another view of declining trend growth is the decline in nominal GDP. Figure 4.11 shows that the 12-quarter rolling average has been on a steady decline for the last two decades.

A combination of lower trend growth and higher volatility means more frequent recessions. Put another way, the closer trend growth is to zero and the higher volatility is, the more likely U.S. growth is to frequently dip below zero. Figure 4.12 shows a stylized view of recessions, but as trend growth dips, the economy will fall below zero percent growth more often.

Higher volatility has very important implications for equity and bond investors across asset classes. Indeed, the last three economic expansions were almost 10 years, but in previous decades, they averaged four or five years. From now on, we are apt to see recessions every three to five years.

Thailand, Phoenix, and Japan

I am sitting in the Las Vegas airport, on my way to LAX, where I will do the final edits on this letter and send it off. Then it's a 15-hour-plus flight to Hong Kong and on to Bangkok, and then on to Phuket. 21 hours on airplanes, plus about ten hours in layovers. I may get to catch up on some reading and writing. Cathay Pacific is supposed to be comfortable. I am actually quite excited about visiting Phuket and Bangkok. Turns out I have readers everywhere so will be meeting people here and there. I am going to try and visit Phi Phi for a day trip, as I am told the beaches and waters are breathtaking, and I'm not sure when I will get the opportunity to be there again. I have traveled too many times to exotic locations for business, without stopping to see the local sights. I do not intend that to happen this time. One of my great friends, Tony Sagami, has promised me I will get to see the real Bangkok. I get back home the following Sunday, when I will recover the day I "lost" going over. Then the next weekend I'm in Phoenix (noted at the beginning of the letter).

Then at the end of the month I take a long flight to Tokyo for a short trip (three days) to speak at a CSAL conference. Given my views on Japan, that should be interesting. I will get to have dinner with Chris Wood, who is one of the guys I really respect, hosting a dinner I am truly looking forward to. He writes the famous Greed and Fear letter, and is bullish on Asia and very bearish on the dollar, so there will be a lot to discuss. Thankfully, Tokyo is a direct nonstop flight from Dallas.

It is time to hit the send button. They are calling my plane. I see some sleep in my near future (we leave at 10:30 pm), and some reading. Beaches, Thai food, good conversation with friends. I am excited. Have a great week. It will be interesting to see what I learn and write back to you next week.

Your glad to be away from the cold analyst,

John F. Mauldin

johnmauldin@investorsinsight.com

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2011 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.