Revolution, Its All About China, Weeks When Decades Can Happen

Politics / China Mar 20, 2012 - 07:24 AM GMTBy: John_Mauldin

My friends at GaveKal are uniquely positioned to help us think about where we have been in the past decade and where we are going in the next one. Their perch in Hong Kong lets them keep their fingers on China’s pulse, but they also have profound roots in Europe – the Gave family is French – as well as a thorough grasp of the US economy and culture. (Louis Gave, the author of today’s Outside the Box, is a Duke grad.)

My friends at GaveKal are uniquely positioned to help us think about where we have been in the past decade and where we are going in the next one. Their perch in Hong Kong lets them keep their fingers on China’s pulse, but they also have profound roots in Europe – the Gave family is French – as well as a thorough grasp of the US economy and culture. (Louis Gave, the author of today’s Outside the Box, is a Duke grad.)

We can all second Louis when he notes “the discomfort and uncertainty we find in most meetings with clients” – we’re treading on uncertain turf here and moving into unexplored territory. We sense that the potential, in the next few years, for both creation and destruction (so yes, creative destruction) is greater than at any time in our lives – and greater perhaps than at any time in the history of the human race.

How do we get our heads around something that big and dynamic? Where do we find the confidence that our next steps will take us forward rather than back? How do we allocate and husband our resources, wisely and profitably? In the following piece, Louis Gave takes an approach that is genuinely helpful: he looks back to the crucial year of 2001 and identifies three big events that largely determined global economic and investment trends in the ’00s.

And then he does something that is rather scary but very necessary. He says, don’t look now, gang, but those trends have stalled; and so we had better come to grips with the great trends that are now forming (lest we be like the British guns of Singapore at the outbreak of WWII: facing the wrong way).

And then – GaveKal to the rescue!– he tells us what those trends are. So, without stealing any of Louis’s thunder, I will deliver you into his capable hands. But first, this note –

I did get my iPad 3 on time. No line, in stock at the local Apple store. I decided to try when I got a few emails from analyst types who actually go to stores to check on lines and inventory instead of just looking at numbers. Lines were down, for whatever reason. And inexplicably to me, there is absolutely no visual difference between the iPad 3 and the 2. None. And there is nothing on the box to reassure you that you actually got the 3, if you don’t get the 4G. Now, the 4G speed is cool, and I can see the increased processor speed, and the display is in fact nicer. Not sure, unless you are an early adopter or hooked on speed (as I am) that the need will be there to buy up. And if you don’t get the 4G? There is no difference in connection speed. And Apple stock is priced for perfection. Just saying…

Finally, I rarely ever provide a link that is simply for fun, but my friend Cliff Draughn of Excelsia sent me the funniest 5-minute clip I have seen in years. I laughed out loud for some time. Do not listen unless you are where you can laugh. This may be something of an inside investment-world joke, but I think most people will appreciate it. http://www.xtranormal.com/w... I think even Suze will get a kick out of this!

Have a great week. I am finishing this up in the airport, and am off in a few minutes to Stockholm and Paris. I intend to take some time and see the Vasa, a 68-gun warship built in 1628 and pulled up from the bay in 1987, where it had been perfectly preserved. Stunning history and something I have long wanted to see. ( en.wikipedia.org/wiki/Vasa_(ship)) Plus a lot more of Stockholm and a few spots in Paris before the GIC conference. And I am also going to spend some time with people who went through the banking/sovereign crisis in Sweden in the ’90s and see what I can learn. And now let’s turn you over to Louis.

Your up on my board, surfing the inevitable analyst,

John Mauldin, Editor

Outside the Box

JohnMauldin@2000wave.com

Weeks When Decades Happen

By Louis Gave March 14, 2012

Talking about the Russian Revolution, Lenin once said that “there are decades when nothing happens and there are weeks when decades happen.” The last quarter of 2001 looks in retrospect like one of those exciting periods: three events occurred which set in motion the main economic trends of the ensuing decade. Successful investors latched on to at least one of these trends. The problem is, all three trends are now over. The investment strategies that worked over the past decade will not continue to work in the next. What comes next?

The three big events of 2001 were:

• The terrorist attacks of 9/11. This unleashed a decade of bi-partisan “guns and butter”policies in the US and produced a structurally weaker dollar.

• China joined the WTO in December 2001. China’s full entry into the global trading system signaled a re-organization of global production lines and China’s emergence as a major exporter. Export earnings were recycled into the mother of all investment booms, which drove a surge in commodity demand and a wider boom in emerging markets.

• The introduction of euro banknotes. The introduction of the common currency unleashed a decade of excess consumption in southern Europe, financed unwittingly by northern Europe through large bank and insurance purchases of government debt.

But today, all three trends have stalled—and this perhaps accounts for the discomfort and uncertainty we find in most meetings with clients. Indeed:

• US guns and butter spending is over. For the first time since 1970, real growth in US government spending is in negative territory:

• Chinese capital spending is slowing. China still needs to invest a lot more, but future growth rates will be in the single digits.

• Excess consumption in southern Europe is done. Money is clearly flowing out to seek refuge in northern Europe.

Thus, like British guns in Singapore, investors whose portfolios still reflect the above three trends are facing the wrong way. Instead of lamenting over the past, investors should be coming to grips with the trends of the future: the internationalization of the RMB, the rise of cheaper and more flexible automation, and dramatically cheaper energy in the US.

1- The internationalization of the RMB

China is now the centre of a growing percentage of both Asian, and emerging market trade (a decade ago China accounted for 2% of Brazil’s exports; today it is 18% and rising). As a result, China is increasingly asking its EM trade partners why their mutual trade should be settled in US dollars? After all, by trading in dollars, China and its EM trade partners are making themselves dependent on the willingness/ability of Western banks to finance their trade. And the realization has set in that this menage à trois does not make much sense. Indeed, for China, the fact that Western banks are not reliable partners was the major lesson of 2008 and again of 2011.

As a result, China is now turning to countries like Korea, Brazil, South Africa and others and saying: “Let’s move more of our trade into RMB from dollars” to which the typical answer is increasingly “Why not? This would diversify my earnings and make our business less reliant on Western banks. But if we are going to trade in RMB, we will need to keep some of our reserves in RMB. And for that to happen, you need to give us RMB assets that we can buy”. Hence the creation of the offshore RMB bond market in Hong Kong, a development which may go down as the most important financial event of 2011.

Of course, for China to even marginally dent the dollar’s predominance as a trading currency, the RMB will have to be seen as a credible currency—or at least as more credible than the alternatives. And here, the timing may be opportune for, today, outshining the euro, dollar, pound or even yen is increasingly a matter of being the tallest dwarf.

Still, China’s attempt to internationalize the RMB also means that Beijing cannot embark on fiscal and monetary stimulus at the first sign of a slowdown in the Chinese economy. Instead, the PBoC and Politburo have to be seen as keeping their nerve in the face of slowing Chinese growth. In short, for the RMB to internationalize successfully, the PBoC has to be seen as being more like the Bundesbank than like the Fed.

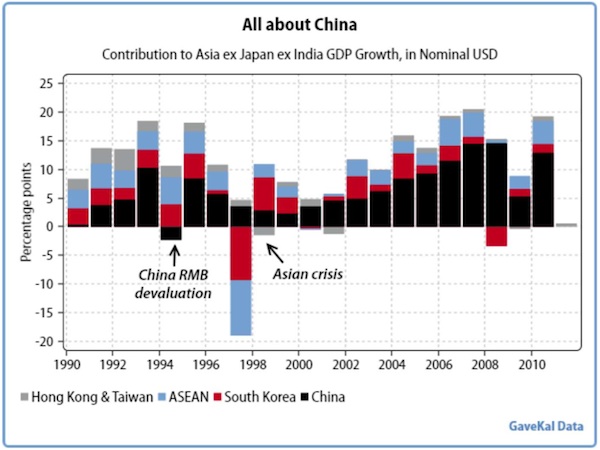

Following this Buba comparison, China has a genuine opportunity to establish the RMB as the dominant trade currency for its region, just as the deutsche mark did in the 1970s and 1980s. But interestingly, China seems to consider that its “region” is not just limited to Asia (where China now accounts for most of the marginal increase in growth—see chart) but encompasses the wider emerging markets. How else can we explain China’s new enthusiasm in granting PBoC swap lines to the likes of the Brazilian, Argentine, Turkish and Belorussian central banks?

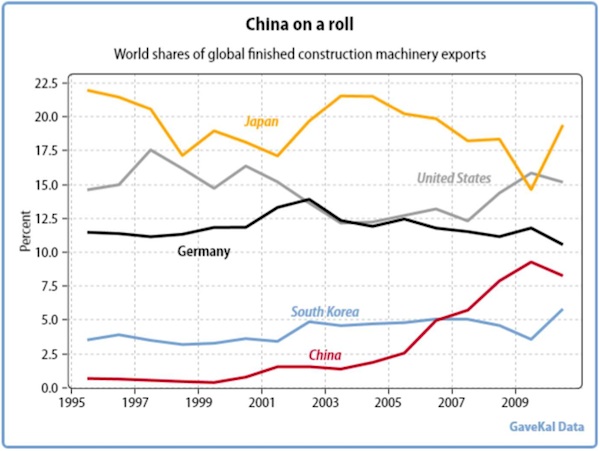

China’s attempt to move more of its trade into RMB is interesting given the current shifts in China’s trade. Indeed, although the US and Europe are still China’s largest single trade partners, most of the growth in trade in recent years has occurred with emerging markets. And China’s trade with emerging markets is increasingly not in cheap consumer goods (toys, underwear, socks or shoes) but rather in capital goods (earth- moving equipment, telecom switches, road construction services, etc; see China Bulldozes a New Export Market). In short, yesterday China’s trade mostly took place with developed markets, was comprised of low-valued-added goods, and was priced in dollars. Tomorrow, China’s trade will be oriented towards emerging markets, focused on higher value-added goods, and priced in RMB.

This would mark a profound change from China’s old development model: keeping its currency undervalued, inviting foreign factories to relocate to the mainland, transforming 10-20mn farmers into factory workers each year, and triggering massive labor productivity gains—gains which the government captures through financial repression and redeploys into large-scale infrastructure projects. But China’s change in development model may be less a matter of choice than of necessity.

2– Virtue from necessity: the rise of robotics

The first harsh reality confronting China is that the country is now the world’s single largest exporter. Combine that impressive status with the reality that the world is unlikely to grow at much more than 3% to 4% over the coming years and it becomes obvious that the past two decades’ 30% average annual growth in exports just cannot be repeated.

Beyond the limits to export growth, the other challenge to China’s business model is the second step, namely the transforming of farmers into factory workers. Not that China is set to run out of farmers (see The Countdown for China’s Farmers). But the coming years may prove more challenging for unskilled workers as robotics and automation continue to gather pace. Over the coming decade, cheap labor may not be the comparative advantage it was in the previous decade, simply because the cost of automation is now falling fast (see The Robots Are Coming).

Of course, factory and process automation is hardly a new concept. What is new is the dramatic recent shift from fixed automation to flexible automation.For decades we have had machines that could perform simple repetitive tasks; now we have machines that can be reprogrammed easily to perform a wide range of more complicated functions. With improved software and hardware, robots can do more, in more industries; and the purpose of automation has shifted from improving crude productivity (making more of the same things at lower cost) to more sophisticated targets like adaptability across product cycles, and improved quality and consistency.

One consequence of cheaper and more flexible automation is that some manufacturing that fled the developed world for cheap-labor destinations like China may return to the US, Japan and Europe, as firms decide that the benefits of low-cost labor no longer outweigh the advantage of better logistics and proximity to customers. Even if this does not occur, factories in places like China may become ever more automated (e.g.: electronics assembler Foxconn, Apple’s main supplier and one of the world’s biggest employers with some 1mn workers, has started to talk about building factories manned with robots). This then raises the question of what China’s hordes of manufacturing workers will do should Chinese factories automate and/or re-localize to the developed world. One obvious conclusion is that China’s leaders will thus have to deal with slowing growth through further deregulation, rather than stimulus and currency manipulation. The remedies of 2008 (large fiscal and monetary stimulus) will not work again.

This dilemma implies that the robotics trend dovetails with the RMB internationalization trend. To understand just why, it is important to recognize one aspect of policymaking which makes China unique: the country’s leaders wake up every morning pondering how to return China to being the world’s number one economy and a geopolitical superpower in its own right (few other world leaders harbor such thoughts). And ever since Deng Xiaoping, the answer to that question has typically been to sacrifice some element of control over the economy in exchange for faster growth.

Today, China faces the imperative of making just such a trade-off between control and growth: the old model of cheap labor and vast capital spending is near exhaustion, so the only way to sustain growth is to go for more efficiency, especially through financial sector reform. For China’s leaders, reform will be painful but the cost of missing out on the global power that comes with further growth would be even more painful. Hence we are convinced Beijing will eventually bite the financial reform bullet, and RMB internationalization is the leading edge of that reform. In that light, the creation of the RMB offshore bond market is an event of much greater significance than is currently acknowledged by the general consensus.

3– Cheap US energy

Along with the possibility of manufacturing returning to the developed world from China and other low labor-cost countries, another key trend of the coming decade should be the gradual achievement of energy independence by the US. Given the discoveries of the past few years in the exploitation of shale gas and oil, and assuming the existence of political will to invest in reshaping US energy infrastructure, such a development is now within reach.

These large natural gas discoveries have two potential global impacts. First, the combination of low-cost automation and low-cost energy could encourage manufacturers to locate their plants not in countries with the lowest labor cost, but in those with the lowest energy cost. For example, on a recent visit to Germany we kept hearing how chemical plants would have a tough time competing with American plants if the price of US natural gas stayed below US$2.50. In fact, with Germany having decided to pull away from nuclear and bet its future on high-cost wind power, energy- intensive industries in the country could be in for a challenging decade.

Second, the return to manufacturing and energy independence should lead to sustained improvement in the US trade deficit. Energy imports account for around half of the US trade deficit (while the other half is broadly manufactured goods from China). Today the US, through its trade deficit, sends roughly US$500bn worth of cash to the rest of the world every year. This money helps grease the wheels of global trade since more than two-thirds of global trade is still denominated in dollars. But what will happen if, in the next ten years, the US stops exporting dollars, thanks to its new strengths in manufacturing and cheap energy? In such a scenario, the dollars would run scarce.

In fact, this may already be happening. This would explain why the growth of central bank reserves held at the Fed for foreign central banks has been in negative territory for the past year—and why, over the past two quarters, the Fed has been exceptionally generous in granting swap lines to foreign central banks (notably the ECB).

This does not make for a stable situation. And given that the RMB is unlikely to replace the dollar as the principal global trading currency for many years to come (see History Lessons and the Offshore RMB), the likely combination of expanding global trade and a shrinking US trade deficit should mean that either the dollar will have to rise, or US assets will outperform non-US assets to the point where valuation differnces make it attractive for US investors to deploy dollars abroad (since US consumers won’t).

4– Conclusion

Obviously, we do not claim to have identified all the big trends of the coming decade. The next several years will doubtless deliver many more important changes and investment opportunities (monetization of Japan’s debt and a collapse in the yen? Demographic challenges in numerous countries? Reform and modernization in the Islamic world? Political upheaval and regime change in Iran? Water shortages in China, India and other Asian countries? Possible energy independence for India through thorium-based nuclear energy plants?). But we are nonetheless confident on these main points:

• The three key macro trends of the past decade have come to a screeching halt. This explains why financial markets seem to lack conviction and direction.

• The internationalization of the RMB and the birth of the RMB bond market is likely to be one of the most important developments of the decade. The closest analogy is the creation of the junk bond market by Michael Milken in the 1980s. Interestingly, just as in the early 1980s, few people are taking the time to work through the ramifications of this momentous event. Understanding this new market will prove essential to understanding the world of tomorrow.

• The likely evolution of the US from record high twin deficits to much smaller budget and trade deficits should help push the dollar higher over the coming years. And this in turn will have broad ramifications for a number of asset prices.

By John F. Mauldin

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2012 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Comments

|

ernie messerschmidt

20 Mar 12, 21:02 |

won't hold my breath

Manufacturing is going to return to the US because of robots? I won't hold my breath. Dream on. |