Euro and Oil in the Year Ahead 2015

Commodities / Crude Oil Jan 10, 2015 - 06:42 AM GMTBy: HRA_Advisory

There was enough good news in the US through December to send all the major indices in New York except NASDAQ to new all-time highs and the tech index isn’t far off. It’s all rainbows and ponies on Wall St right now which should make any sensible person a bit nervous.

There was enough good news in the US through December to send all the major indices in New York except NASDAQ to new all-time highs and the tech index isn’t far off. It’s all rainbows and ponies on Wall St right now which should make any sensible person a bit nervous.

As I expected oil is still in the dumps and that state of affairs should last for a while. As noted in the last issue this big a drop in oil prices is a stimulus though it’s a smaller stimulus in the US than Wall St. wants to believe. Expectations are high after the US printed 5% GDP growth in Q3. That was indeed impressive and cheaper oil should help generate good growth numbers in Q4 and Q1 2015. Things may tail off after that though.

There is a lot of detail and nuance in the markets. After struggling to get it all into a manageable serving for you I’ve decided that’s not in our best interest. For that reason you should expect to see three issues (this one included) in quick succession that will deal with my outlook for different metals, regions and currencies. All will be in play against each other in 2015. In this issue I’m focusing on the Euro and oil, two things both the $US and gold react to on a day to day basis. The € may bounce after the ECB meeting but (as usual) we may get the pain before the gain.

I wish all of you a happy, healthy and prosperous 2015.

Eric Coffin

***

It’s been a wild ride since the last Journal issue. The ride isn’t over though things should get briefly smoother as we get through year end. Not necessarily “better” but volatility in the metals markets may ease off a bit when we return to a post-holiday trading environment. Whatever the hell “normal” is these days.

I don’t expect the major theme of the past month—weak oil prices—to change any time soon. I’ll go into more specifics on a range of commodities in this and in the next two issues. There are more moving parts and contradictory influences than I’ve seen for a long time.

While I think there will be relative calm at the start of the year storm flags have been raised. There is plenty of room for surprises in 2015. I’ll concentrate on oil and EU—particularly Greece—in this issue.

One potential mover for markets is the anticipated start of a QE program by the ECB. Another is renewed instability in Greece. Both of these issues will come to the fore in January with Greek elections closely following the next ECB monetary policy meeting.

I remain a skeptic about large scale QE by the European Central Bank. It’s not that I think it’s unnecessary or a bad thing. I think QE helped the US and the ECB, unlike the Fed, has a balance sheet that is one trillion Euros smaller than it was a couple of years ago. The ECB has actually been tightening which is insane given the Continent’s economic situation.

For the ECB the question is whether Mario Draghi and a few other fiscal doves are willing to push QE through without unanimous consent. I think there is no way the Germans will vote for it and several Nordic countries share the German opinion.

Draghi isn’t going to change their minds on the subject. Technically, a majority vote of the ECB ruling council is all that is required but the bank has never taken this major an action in the past without a unanimous vote. Is Draghi willing to ignore convention?

It seems increasingly likely. Draghi is impatient and hinting he is willing to go it alone if he has to.

I would expect a QE announcement, if it comes, after the next scheduled monetary policy meeting on January 21. How the Euro reacts to that is going to be interesting. It will partially depend on how big a QE program Draghi is willing to commit the bank to.

The Euro has trended down for months and the QE question has created some of the selling pressure. The chart above shows its been nothing but down for the Euro since early in the year.

It’s taken as a given that the Euro will have another big drop if and when the ECB finally pulls the trigger. That’s certainly possible but the market is already plenty short and most traders seem less skeptical than I about this situation. Expectations are high the ECB will act and go for shock and awe.

It seems counter intuitive but I would not be surprised to see a Euro rally after the announcement. That’s not what the ECB wants. They want the Euro to weaken further but there will be some “sell on news” trades on the short side. By the same token, long Dollar is an extremely crowded trade and some pullbacks along the way should be expected.

The market is expecting something impressive from the ECB but the fact is Draghi as been all talk and no action for the past year or more. He’s gotten away with that as traders remember his “do whatever it takes” speech during the last Euro crisis. That can’t go on forever. I think traders lose patience (and start closing Euro short positions) if he doesn’t announce something soon.

Unless Draghi builds a consensus for a large QE program—which I do not think is possible where Germany is concerned—a QE announcement will be a disappointment. It seems everyone and their dog is calling for Euro-Dollar parity in 2015. Expectations are high for a QE program of at least €1 trillion. We’ll see.

There are of course valid reasons to expect the Euro to keep falling based on growth differentials but don’t be shocked if the Euro actually rises later in January. I think that is a real possibility if short trades are unwound after a disappointing QE announcement. If there is no announcement after the next meeting the bounce would be that much larger. I don’t think Draghi can jawbone any longer and get away with it.

The other January event just added to the calendar is a new election in Greece. The large graphic below shows the results and percentage vote in the 2012 election for the currently ruling New Democracy and challenger Syriza parties as well as the current poll standings for different Greek political parties. The graph below that compares the current “recession” in Greece to recent historical depressions, all courtesy of The Economist.

The graph really jumps out at you and shows why Greeks are so fed up. Whomever is at fault, Greece is suffering a depression that so far looks like it will be worse than the Great Depression was for the US. Little wonder the place is volatile.

The current voting intentions show Syriza is ahead but by only a small margin. This may be why markets outside of Greece have taken this news calmly. Syriza wants to renegotiate or repudiate the debt deal with the EU. Interestingly, the majority of Greeks say they want to stay in the Euro so New Democracy may gain in the polls leading up to the election if Syriza scares voters with promises to leave the Euro. Either way its going to be an unruly coalition. It's not likely any party can win a majority.

Does this have the potential to crash the Euro? Perhaps, though the potential for contagion is far less than it was in 2011. Almost all external Greek debt is held by EU institutions and the IMF, not private banks or funds. The debt stands at about €300 billion. That’s a big number but nowhere near large enough to destabilize these institutions.

Even if Syriza wins they haven’t got much negotiating leverage. If they repudiate the debt they’ll be tossed out of the Euro. I don’t see northern Europeans being cowed by them.

If Greece exits it would be years before they could borrow externally. That would be a disaster but they would have a much smaller debt load and could devalue their currency at will. Inflation would explode but so would tourism as Greece again became the cheap destination.

The biggest danger for the EU would be Greece exiting and appearing to come out of a devaluation well. That could have other Europeans thinking it was a chance worth taking. The majority of Italians, for instance, think the Euro is a bad thing for their country. Italy has over €2 trillion in debt, plenty of it held by foreign and domestic banks. If it looked like Greece was weathering an exit from the Euro Italians (and French and…) might start wondering. That’s the real nightmare for Brussels.

A big stimulus package or disastrous election in Greece. Those are the two potential negatives for the Euro. It matters for resource investors because, right or wrong, most commodities are heavily impacted by moves in the US Dollar and the Euro is the big pair trade. I think traders should worry less about the Dollar where gold is concerned. I’ll touch on that again briefly at the end of this piece after some comments about oil.

The 1 year oil chart on this page says it all. This doesn’t look like a chart that has found its bottom yet, though oil stocks have been getting support in the market lately.

Oil and gas (the natural gas chart doesn’t look a lot better) traders obviously think a bottom is very close. Energy indices had a good bounce in mid-December when oil had a dead cat bounce. Oil stocks have been holding those gains but oil itself is at new lows again so I’m not convinced the bounce will hold.

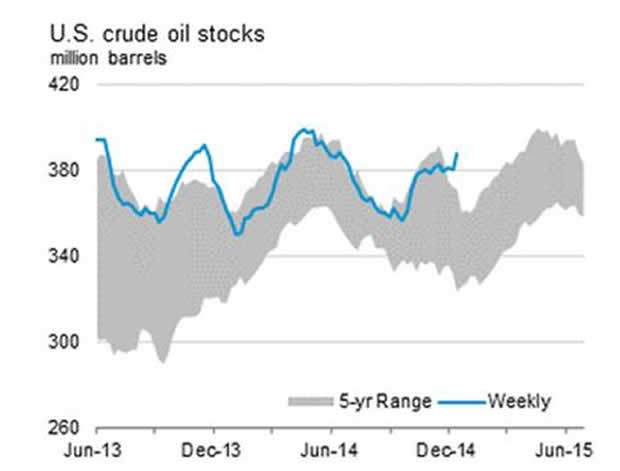

The top chart on this page shows US crude inventories and helps explain why the oil price bounce didn’t hold. It shows crude inventories since mid-2013 superimposed on the five year range. Not surprisingly the inventory rises during shoulder seasons in the spring and fall and dips as summer driving and winter heating increase demand.

What freaked traders out was the rise in current inventories—the blue line—going through December when it would normally be starting to fall.

Inventory levels have been high for over a year. A few weeks of cold weather could turn things around but this doesn’t look like a blip. It’s an indication of oversupply and the reason hopeful hedge funds started to panic and close long oil positions as the year wrapped up.

Much has been made of falling rig counts in North America but the drop has been small in percentage terms and its coming off decade highs. The count will keep falling but as I noted last month this is not a situation that will correct itself quickly.

Unless one of main oil producing nations cuts production unilaterally oil will stay under pressure for some time to come. That is a good thing for the world economy and will help a lot of bulk miners, especially ones running off generators as many remote ones do. It will take time for lower prices to work through the supply chain but it could be a nice bonus in the Q1 and Q2 reporting for many miners.

I’m going to focus on gold and a couple of other things in the next issue but I wanted to leave you with one important chart.

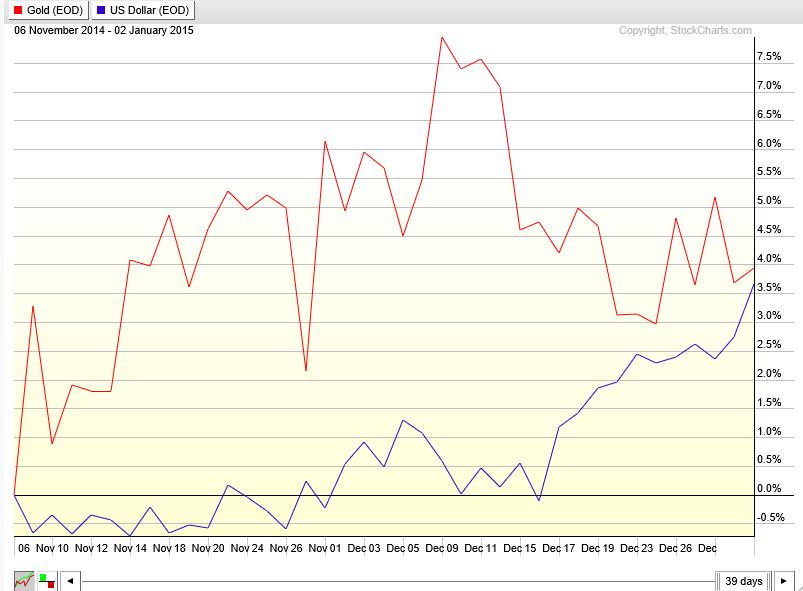

The chart on this page compares the performance of gold and the US Dollar since gold fell to the $1130 range in early November. There is an important message in this chart. Both gold and the $US have gained since early November. It would surprise most dollar bulls to realize the percentage move in gold has actually been larger.

The greenback as surged since mid-December. That hurt the gold price but less than it “should” have and bullion recently found a bid and held higher lows, though volatility has been high.

That is not how it’s supposed to work according to Wall St. Gold is assumed to have a near perfect negative correlation with the $US. Most of the calls for sub $1000 gold this year are based simply on that assumed correlation. Wall St expects the dollar to keep rising which, ipso facto, means gold prices must fall.

It doesn’t always work that way though, as I have pointed out several times recently. The chart above indicates a moderate positive correlation, not a perfect negative one. This could be hugely important to how the gold price acts this year. And, it makes sense if you think of gold in currency rather than commodity terms.

As I’ll show in more detail in the next issue gold is the world’s second strongest major currency. The market is obsessed by the dollar gold price but when viewed in terms of other currencies its appeal is easier to understand. That appeal is our best chance for a better 2015.

To view Eric Coffin's recent video interview at the Canvest Vancouver Conference, please click here

By Eric Coffin

http://www.hraadvisory.com

Eric Coffin, editor of HRA Advisories, recently sat down with President and CEO of Colorado Resources, Adam Travis, to discuss more about the company, its recent successes and why investors should stay tuned to this story. Click here to download Eric’s interview with Colorado Resources now!

We think there will be more discovery winners but it's still a "show me" market. HRA understands that which is why we are offering you a chance to try out HRA for three months for only $10.00!

The HRA – Journal, HRA-Dispatch and HRA- Special Delivery are independent publications produced and distributed by Stockwork Consulting Ltd, which is committed to providing timely and factual analysis of junior mining, resource, and other venture capital companies. Companies are chosen on the basis of a speculative potential for significant upside gains resulting from asset-based expansion. These are generally high-risk securities, and opinions contained herein are time and market sensitive. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer, solicitation or recommendation to buy or sell any securities mentioned. While we believe all sources of information to be factual and reliable we in no way represent or guarantee the accuracy thereof, nor of the statements made herein. We do not receive or request compensation in any form in order to feature companies in these publications. We may, or may not, own securities and/or options to acquire securities of the companies mentioned herein. This document is protected by the copyright laws of Canada and the U.S. and may not be reproduced in any form for other than for personal use without the prior written consent of the publisher. This document may be quoted, in context, provided proper credit is given.

Published by Stockwork Consulting Ltd.

Box 85909, Phoenix AZ , 85071 Toll Free 1-877-528-3958

hra@publishers-mgmt.com

©2014 Stockwork Consulting Ltd. All Rights Reserved.

HRA Advisory Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.