Margin Rules Changes Force New Private Funding Of Public Debt

Interest-Rates / US Debt Jan 19, 2016 - 04:53 PM GMTBy: Dan_Amerman

The Federal Reserve and other regulators around the world (including all members of the G-20) have recently agreed to alter margin rules, which will allow them to claim new powers over lending and leverage. In the United States these developing regulatory changes will not be restricted to the Fed's legal oversight over banks alone, but will affect all financial companies.

The Federal Reserve and other regulators around the world (including all members of the G-20) have recently agreed to alter margin rules, which will allow them to claim new powers over lending and leverage. In the United States these developing regulatory changes will not be restricted to the Fed's legal oversight over banks alone, but will affect all financial companies.

The new margin rules will impact about $4.4 trillion in investments in the US. In combination with new rules for $2.7 trillion in money funds, the regulations are changing for about $7 trillion in investments. And the combined effect of these changes may be to drive up to $2.5 trillion out of the private investment markets and into purchasing the debts of a heavily indebted US government, thereby providing a very low cost source of funds.

In a matter of a few months and with almost no notice, changes in obscure regulations are being used to create a new captive market for US Treasuries and agencies that is approximately equal to the total amount of federal debt purchased by the Federal Reserve over the course of many years of quantitative easing.

The headlines are that the United States is starting to slowly release its control over interest rates, and return them to private market control. The reality is that the government is doing just the opposite, and is capturing formerly free and private money at a fantastic rate. Which brings up the question: just why is the government quietly deploying two massive financial stabilizers for the federal debt in 2016?

The effects are likely to persist far beyond 2016, and could help depress interest rates for all investors for potentially years and decades to come. Yet, because these trillions of dollars of major changes are hidden inside of obscure financial regulations, the general public is completely unaware of what is happening, or how it could change their investment results, their lifestyle in retirement, or even their ability to retire at all.

Margin Rules & The New Regulations

A detailed overview of the new rules in process can be found in a Wall Street Journal article published on January 11th. 2016 and linked here. As of November 12th, 2015, the US and the other member nations and organizations of the Financial Stability Board agreed to implement margin rules changes (although there was almost no notice at the time). The intent of so many nations doing so simultaneously is to keep investors from dodging the regulations by moving their assets offshore.

Traditionally, stock purchases were the primary focus of margin rules. The Federal Reserve's Regulation T requires a minimum of a 50% margin on new stock purchases. This means that if an investor purchases $200,000 in stock, no more than $100,000 of that can be with borrowed money.

Increasing margin requirements requires investors to either come up with more cash or to very quickly sell their assets – at a time when the market is potentially being flooded with other sellers who are also forced to sell at almost any price because of their own unexpected margin calls. Because of this power to push prices downwards, it is considered to be a textbook means of dampening speculative bubbles. Of course, the regulatory power of margin rule changes to rapidly change prices can also be used for other purposes and with other instruments, such as futures and options.

Perhaps the most infamous series of margin rules changes in recent years occurred in 2011, when the Chicago Mercantile Exchange repeatedly and sharply raised margin requirements for silver futures contracts, with most increases occurring in late April and early May of that year.

In the spring of 2011, silver prices were soaring above $45 an ounce, but were rapidly sent to below $35 an ounce as repeated margin increases forced investors to either come up with large sums of cash overnight, or liquidate into a plunging market as everyone around them faced the same dilemma. Prices then slowly rebuilt to above $40 an ounce, until a new margin increase in September inflicted another round of pain and quickly knocked the price of silver below $30 per ounce.

The new Federal Reserve regulations will vastly expand the reach of margins rules because it is proposed that they will apply to securities financing transactions, such as repurchase agreements. In this market, which the US Office of Financial Research estimates to be approximately $4.4 trillion in size, high quality collateral is provided to secure a very short term and very low interest rate loan. The value of the collateral provided is somewhat more than the amount of loan, with the excess collateral (the margin) securing the lender against a reduction in the value of the collateral.

Under the still developing new regulations, the Federal Reserve will be able to set a minimum margin, rather than the market. The theory then is that by raising margin requirements, the Fed will be able to reduce leverage in the system at will. And because the margin rules will apply to all financial companies and not just the banks, the Fed will have new powers to control the behavior of the entire financial system.

Now some might portray this extraordinary expansion of powers via regulatory fiat to be a good thing. After all, there is a lot of risk in the system, highly leveraged systems are generally riskier, and it is said to be in all of our interests for the government to have additional new powers to reduce that leverage and pull risk from the system as needed. Or at least that seems to be the publicly presented justification for this change.

Interestingly enough however, there happens to be a rather major loophole, whereby if the private sector more closely aligns its behavior with what the government wants it to do, then market participants no longer have to worry about this new generation of regulation induced financing risks.

The Danger & The Loophole

The key loophole is that when US Treasury obligations and agency securities are used as the collateral, the borrower will be immune from the new margin regulations. This then creates a split market, with two kinds of secured financings.

For those who own Treasuries and agencies and use them as collateral, they are not subject to the planned new rules. According to the US Office of Financial Research, about two thirds of the collateral currently being used is Treasuries and agencies, so this will be true for most of the current market borrowers.

For the remaining one third of borrowers, however, there is a potentially substantial increase in risk. The dangers are those of liquidity and market risk. If the Fed increases margin requirements in order to pull leverage from the system, then more or less by definition, that action creates a liquidity crunch for borrowers who were not invested in Treasuries and agencies.

For that is what reducing leverage is all about – short term loans cannot be rolled over, as they usually are, but have to be actually paid off. Which means a scramble to come up with the cash to pay down the borrowings. Which likely means forced asset sales as well, because that is the essence of what financial companies do – they purchase assets with borrowed money. And to pay back the money, they need to sell the assets.

These asset sales and borrowing reductions may potentially occur on a massive scale, because that is more or less the point of the Fed expanding the reach of its powers - to be able to make the entire financial system, and not just the banking system, quickly and simultaneously reduce their borrowings.

Because these asset sales are occurring on a system wide basis, this then sets up the possibility of a feedback loop. Too many companies simultaneously selling the same type of assets drops the price of those assets. Which reduces their value as collateral. Which means that still more loans must be paid down, as the existing collateral will not go as far. Which forces still more asset sales, which then further reduces the market value of the assets, and requires the payback of still more loans – and so forth.

The alternative is to sell the other collateral up front, use the proceeds to buy Treasuries and agencies as replacement collateral, and thereby escape any exposure to increases in margin requirements and the abrupt need to reduce borrowings.

The Stick & The Carrot

Viewed from the perspective of market participants, what the Federal Reserve is really doing is creating a "stick" and a "carrot".

The stick applies to all financial companies who refuse to buy US Treasuries and agencies, and use them as collateral for their secured borrowings. Once the new rules take effect, then these participants can be forced into a liquidity crunch and/or asset losses at will, as they are made to reduce their borrowings and sell assets. It should also be noted that liquidity crunches, i.e. not being able to come up with the cash to pay off overnight or other borrowings, are an existential risk for financial companies, as they can take down what previously appeared to be a healthy company in a matter of days.

So the stick of margin rules changes is potent indeed in general, as silver market participants found out in 2011, and there are particularly powerful aspects when it comes to highly leveraged financial companies.

And then there is the carrot, which is the safe harbor of buying US Treasuries and agencies to use as collateral for secured financings. For the financial companies willing to do their part in helping to finance the national debt – then all these newly created problems go away. Just sell the other collateral, buy the debt of the government to use instead, and the risk of margin rules changes, the risk of the potential associated liquidity crunch and the risk of the potential associated forced rapid sale of assets are all no longer a concern.

Because the total market is about $4.4 trillion, and about a third of the market uses non-exempt collateral, that means that roughly $1.5 trillion dollars of investments are stake. An enormous incentive is being created for financial companies to sell about $1.5 trillion in other types of investments which are currently being used as collateral, and to purchase Treasuries and agencies instead.

Is This Really About Controlling Leverage At All?

The other fascinating implication is that so long as most market participants act rationally – the power of the new margin rules disappear, as does the ability to pull leverage from the system. Two thirds of the market is already exempt from the margin rules changes. If the market reacts rationally to both the new rules and the safe harbor, and changes to the place where 90% to 95%+ of the collateral is Treasuries and agencies, then the Fed has very little power to pull leverage from the system.

The new margin rules therefore make no sense when it comes to their stated purpose, which is giving the Federal Reserve the power to reduce risk by mandating a reduction in leverage. Why create a rule to control market conduct, if a wide open loophole is simultaneously created such almost all of the market can be expected to be exempt from the rule?

Crucially, there is no difference in systemic risk from leverage if Treasuries are used as collateral rather than high quality private instruments. The issue is the borrowing level in the system, and not the credit quality of the collateral.

The new rules are likely to be of little use when it comes to the stated purpose of reducing leverage – but are likely to be very useful indeed in motivating investors to seek safety in the loophole, and thereby increase the funding of the national debt by private investors for potentially many years to come.

Textbook Financial Repression

The regulatory changes planned by the Federal Reserve are a textbook example of what economists refer to as Financial Repression. For those who are not familiar with the term, or are unsure about exactly what it means, I have written an understandable tutorial on the subject which can be read here.

Financial Repression is one of the four core tools available for heavily indebted governments to manage and reduce their debts, along with austerity, high rates of inflation and outright default. While the least known by the general public, Financial Repression has an extensive history in the United States and other nations.

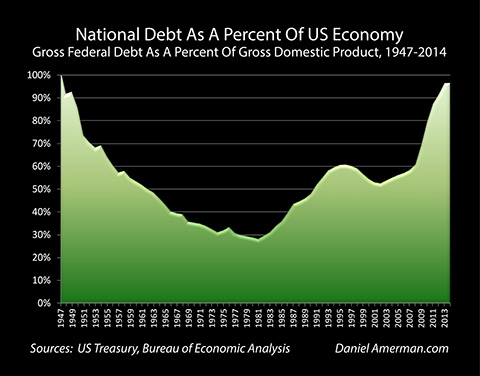

What most people don't realize is that the United States has been here before, in terms of a national debt approximately equaling the size of the national economy. This was the situation after World War II. And as shown below, that debt steadily came down over a period of decades, when measured as a percent of the economy.

Financial Repression is exactly how it was done, from the 1940s until the early 1970s. Indeed, the previously linked Wall Street Journal article does point to the not at all coincidental timing, even though the words "Financial Repression" are never used:

"The Fed's return to margin requirements is symbolically significant, a kind of throwback to an earlier era of empowering regulators to try to steer markets. Until 1974, the Fed regularly tinkered with the amount of margin, or collateral..."

The very high levels of debt are back - and increasingly, so are new variants of the old tools.

In general terms, Financial Repression can be used to refer to one half of a long term cycle between free market-dominated economies (Financial Liberalization), and more government-dominated economies (Financial Repression).

The heavily indebted US government moved to Financial Repression in the 1940s. The cycle changed to Financial Liberalization in the 1970s and 1980s as the national debt dropped to about 30% of the size of the economy. And the cycle then swiftly moved back to Financial Repression as the national debt surged in the aftermath of the financial crisis of 2008.

There is much more specific meaning for Financial Repression as well, which involves governments forcing negative real (inflation-adjusted) returns on savers over a period of decades. The idea is that unmanageable national debts are held down or reduced while economic growth continues, so that the economy gradually pulls away from the level of national debt, until a now manageable level of debts allows a return to the alternating cycle of Financial Liberalization (in theory anyway, many other issues are at play in this current round that were not there in the 1940s).

As part of that process, there is an effective checklist for how governments can accomplish this, as covered in the linked tutorial.

The first principle is that financial institutions will be made to participate through regulatory means, and because the institutions are really just intermediaries, that means the public is being forced to participate, without realizing that is happening.

Margin Rules Changes – Check.

A second principle is that a combination of sticks and carrots will be used to compel participation, and create a captive audience for government debt.

Margin Rules Changes – Check.

A third principle is that the regulatory changes which compel the purchase of government debt will be described as being done in the name of public safety.

Margin Rules Changes – Check.

A fourth principle is that this be done in a manner where history shows that most voters won't understand what is happening, and there will therefore be few if any political consequences.

Margin Rules Changes – Check.

A fifth principle is that for the few people who are aware of what is happening, they will be prevented from leaving a rigged playing field by the use of capital controls.

Margin Rules Changes – Check. This is why the entire G-20 simultaneously said (via the Financial Stability Board) that they would be doing this, so that wherever the financial companies go, they can't get away (at least not in the major markets).

The Federal Reserve's plan to change margin rules checks all five of those boxes. The rules changes may be a poor and strange way to attempt to control financial system leverage, but they are likely to be highly effective as a straight out of the textbook example of Financial Repression.

Part II

Part II of this article explores 1) the combined effect of the margin rules changes and the new money fund regulations; 2) the creation of a new captive funding for the national debt that could equal Federal Reserve purchases of Treasuries via quantitative easing; 3) the quiet and almost unnoticed deployment of two massive financial stabilizers and the question of why that is happening now; and 4) the powerful implications for retirement savers and other long-term investors.

Daniel R. Amerman, CFA

Website: http://danielamerman.com/

E-mail: mail@the-great-retirement-experiment.com

Daniel R. Amerman, Chartered Financial Analyst with MBA and BSBA degrees in finance, is a former investment banker who developed sophisticated new financial products for institutional investors (in the 1980s), and was the author of McGraw-Hill's lead reference book on mortgage derivatives in the mid-1990s. An outspoken critic of the conventional wisdom about long-term investing and retirement planning, Mr. Amerman has spent more than a decade creating a radically different set of individual investor solutions designed to prosper in an environment of economic turmoil, broken government promises, repressive government taxation and collapsing conventional retirement portfolios

© 2016 Copyright Dan Amerman - All Rights Reserved

Disclaimer: This article contains the ideas and opinions of the author. It is a conceptual exploration of financial and general economic principles. As with any financial discussion of the future, there cannot be any absolute certainty. What this article does not contain is specific investment, legal, tax or any other form of professional advice. If specific advice is needed, it should be sought from an appropriate professional. Any liability, responsibility or warranty for the results of the application of principles contained in the article, website, readings, videos, DVDs, books and related materials, either directly or indirectly, are expressly disclaimed by the author.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.