Are Asian Central Bankers Even Crazier Than Our Own?

Interest-Rates / Central Banks Feb 22, 2016 - 10:21 AM GMTBy: Raul_I_Meijer

That the world’s central bankers get a lot of things wrong, deliberately or not, and have done so for years now, is nothing new. But that they do things that result in the exact opposite of what they ostensibly aim for, and predictably so, perhaps is. And it’s something that seems to be catching on, especially in Asia.

That the world’s central bankers get a lot of things wrong, deliberately or not, and have done so for years now, is nothing new. But that they do things that result in the exact opposite of what they ostensibly aim for, and predictably so, perhaps is. And it’s something that seems to be catching on, especially in Asia.

Now, let’s be clear on one thing first: central bankers have taken on roles and hubris and ‘importance’, that they should never have been allowed to get their fat little greedy fingers on. Central bankers in their 2016 disguise have no place in a functioning economy, let alone society, playing around with trillions of dollars in taxpayer money which they throw around to allegedly save an economy.

They engage solely, since 2008 at the latest, in practices for which there are no historical precedents and for which no empirical research has been done. They literally make it up as they go along. And one might be forgiven for thinking that our societies deserve something better than what amounts to no more than basic crap-shooting by a bunch of economy bookworms. Couldn’t we at least have gotten professional gamblers?

Central bankers who moreover, as I have repeatedly quoted my friend Steve Keen as saying, even have little to no understanding at all of the field they’ve been studying all their adult lives.

They don’t understand their field, plus they have no idea what consequences their next little inventions will have, but they get to execute them anyway and put gargantuan amounts of someone else’s money at risk, money which should really be used to keep economies at least as stable as possible.

If that’s the best we can do we won’t end up sitting pretty. These people are gambling addicts who fool themselves into thinking the power they’ve been given means they are the house in the casino, while in reality they’re just two-bit gamblers, and losing ones to boot. The financial markets are the house. Compared to the markets, central bankers are just tourists in screaming Hawaiian shirts out on a slow Monday night in Vegas.

I’ve never seen it written down anywhere, but I get the distinct impression that one of the job requirements for becoming a central banker in the 21st century is that you are profoundly delusional.

Take Japan. As soon as Abenomics was launched 3 years ago, we wrote that it couldn’t possibly succeed. That didn’t take any extraordinary insights on our part, it simply looked too stupid to be true. In an economy that’s been ‘suffering’ from deflation for 20 years, even as it still had a more or less functioning global economy to export its misery to, you can’t just introduce ‘Three Arrows’ of 1) fiscal stimulus, 2) monetary easing and 3) structural reforms, and think all will be well.

Because there was a reason why Japan was in deflation to begin with, and that reason contradicts all three arrows. Japan sank into deflation because its people spent less money because they didn’t trust where their economy was going and then the economy went down further and average wages went down so people had less money to spend and they trusted their economies even less etc. Vicious cycles all the way wherever you look.

How many times have we said it? Deflation is a b*tch.

And you don’t break that cycle by making borrowing cheaper, or any such thing, you don’t break it by raising debt levels, and try for everyone to raise theirs too. Which is what Abenomics in essence was always all about. They never even got around to the third arrow of structural reforms, and for all we know that’s a good thing. In any sense, Abenomics has been the predicted dismal failure.

Now, I remember Shinzo Abe ‘himself’ at some point doing a speech in which he said that Abenomics would work ‘if only the Japanese people would believe it did’. And that sounded inane, to say that to people who cut down on spending for 2 decades, that if only they would spend again, the sun would rise in concert. That’s like calling your people stupid to their faces.

The reality is that in global tourism, the hordes of Japanese tourists have been replaced by Chinese (and we can tell you in confidence that that’s not going to last either). The Japanese economy simply dried out. It sort of functions, still, domestically, albeit it on a much lower level, but now that global trade is grasping for air, exports are plunging too, the population is aging fast and there’s a whole new set of belts to tighten.

So last June, the desperate Bank of Japan governor Haruhiko Kuroda did Abe’s appeal to ‘faith’ one better, and, going headfirst into the fairy realm, said:

I trust that many of you are familiar with the story of Peter Pan, in which it says, ‘the moment you doubt whether you can fly, you cease forever to be able to do it’. Yes, what we need is a positive attitude and conviction. Indeed, each time central banks have been confronted with a wide range of problems, they have overcome the problems by conceiving new solutions.

And that’s not just a strange thing to say. In fact, when you read that quote twice, you notice -or I did- that’s it’s self-defeating. Because, when paraphrasing Kuroda, we get something like this: ‘the moment the Japanese people doubt whether their government can save the economy, they cease forever to believe that it can’.

Now, I’m not Japanese, and I’m not terribly familiar with the role of fairy tales in the culture, but just the fact that Kuroda resorted to ‘our’ Peter Pan makes me think it’s not all that large. But I also think the Japanese understood what he meant, and that even the few who hadn’t yet, stopped believing in him and Abe right then and there.

Then again, Asian cultures still seem to be much more obedient and much less critical of their governments than we are, for some reason. The Japanese don’t voice their disbelief, they simply spend ever less. That’s the effect of Kuroda’s Peter Pan speech. Not what he was aiming for, but certainly what he should have expected, entirely predictable. Why hold that speech then, though? Despair, lack of intelligence?

In a similar vein, we chuckled out loud on Friday, first when president Xi demanded ‘Absolute Loyalty’ from state media when visiting them, an ‘Important Event’ broadly covered by those same media. Look, buddy, when you got to go on TV to demand it, someone somewhere’s bound to to be thinking you don’t have it…

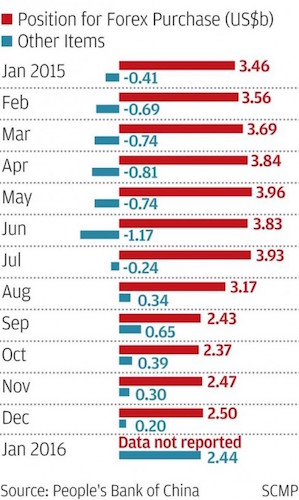

And we chuckled also when the South China Morning Post (SCMP) broke the news that the People’s Bank of China, in its monthly “Sources and Uses of Credit Funds of Financial Institutions” report has stopped publishing the “Position for forex purchase”, which is that part of capital movements -and in China’s case today that stands for huge outflows- which goes through ‘private’ banks instead of the central bank itself.

It’s like they took a page, one-on-one-, out of the Federal Reserve’s playbook, which cut its M3 money supply reporting back in March 2006. What you don’t see can’t hurt you, or something along those lines. The truth is, though, that if you have something to hide, the last thing you want to do is let anyone see you digging a hole in the ground.

But the effect of this attempt to not let analysts get the data is simply that they’re going to get suspicious, and start digging even harder and with increased scrutiny. And they have access to the data anyway, through other channels, so the effect will be the opposite of what’s intended. And that too is predictable.

First, from Fortune, based on the SCMP piece:

Is China Trying to Hide Capital Outflows?

China’s central bank is making it harder to calculate the size of capital outflows afflicting the economy, just as investors have started paying closer attention to those mounting outflows, which in December reached almost $150 billion and in January around $120 billion. The central bank omitted data on “position for forex purchase” during its latest report, the South China Morning Post reported today.

The unannounced change comes at a time pundits are questioning whether outflows have the potential to cripple China’s currency and economy. Capital outflows lead to a weaker currency, which concerns the hordes of Chinese companies that borrowed debt in foreign currencies over the past few years and now have to pay it back with a weaker yuan.

The news of the central bank withholding data is important because capital outflow figures aren’t released as line items. They are calculated by analysts in a variety of ways, one of which includes using the omitted data. The Post quoted two analysts concluding the central bank’s intention was to hide the true amount of continuing outflows.

The impulse to hide bad news shouldn’t come as a surprise. China’s government has been evasive about economic matters from this summer’s stock bailout to its efforts propping up the value of the yuan. Analysts still have a variety of ways to estimate the flows, but the central bank is making it ever more difficult.

And then the SCMP:

Sensitive Financial Data ‘Missing’ From PBOC Report On Capital Outflows

Sensitive data is missing from a regular Chinese central bank report amid concerns about capital outflow as the economy slows and the yuan weakens. Financial analysts say the sudden lack of clear information makes it hard for markets to assess the scale of capital flows out of China as well as the central bank s foreign exchange operations in the banking system.

Figures on the “position for forex purchase” are regularly published in the People’s Bank of China’s monthly report on the “Sources and Uses of Credit Funds of Financial Institutions”. The December reading in foreign currencies was US$250 billion. But the data was missing in the central bank’s latest report. It seemed the information had been merged into the “other items” category, whose January figure was US$243.9 billion -a surge from US$20.4 billion the previous month.

[..] “Its non-transparent method has left the market unable to form a clear picture about capital flows,” said Liu Li-Gang, ANZ’s chief China economist in Hong Kong. “This will fuel more speculation that China is under great pressure from capital outflows. It will hurt the central bank’s credibility.”

[..] All forex-related data released by the central bank is closely monitored by financial analysts. They often read item by item from the dozens of tables and statistics to try to spot new trends and changes. China Merchants Securities chief economist Xie Yaxuan said the PBOC would not be able to conceal data as there were many ways to obtain and assess information on capital movements.

“We are waiting for more data releases such as the central bank’s balance sheet and commercial banks’ purchase and sales of foreign exchange released by the State Administration of Foreign Exchange for a better understanding of the capital movement and to interpret the motive of the central bank for such change,” Xie said.

It’s like they’ve landed in a game they don’t know the rules of. But then again, that’s what we think every single time we see Draghi and Yellen too, who are kept ‘alive’ only by investors’ expectations that they are going to hand out free cookies, and lots of them, every time they make a public appearance.

And what’s going on in Japan and China will happen to them, too: they will achieve the exact opposite of what they’re aiming for. They arguably already have. Or at least none of their desperate measures have achieved anything close to their stated goals.

They may have kept equity markets high, true, but their economies are still as bad as when the QE ZIRP NIRP stimulus madness took off, provided one is willing to see through the veil that media coverage and ‘official’ numbers put up between us and the real world. But they sure as h*ll haven’t turned anything around or caused a recovery of any sorts. Disputing that is Brooklyn Bridge for sale material.

Eh, what can we say? Stay tuned?! There’ll be a lot more of this lunacy as we go forward. It’s baked into the stupid cake.

Professor Steve Keen and Raúl Ilargi Meijer discuss central banking, Athens, Greece, Feb 16 2016

By Raul Ilargi Meijer

Website: http://theautomaticearth.com (provides unique analysis of economics, finance, politics and social dynamics in the context of Complexity Theory)

© 2016 Copyright Raul I Meijer - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Raul Ilargi Meijer Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.