Our Future Economy, Jobs, Banking, And Governance

Economics / US Economy Dec 05, 2016 - 12:22 PM GMTBy: Raymond_Matison

Part 1. Our Past and Present Experience

Part 1. Our Past and Present Experience

World leaders, central bankers, leading politicians, and economists are all clamoring for increased economic growth. If growth falls below a perceived minimum rate, financial or fiscal stimulus programs are initiated and maintained in order to accelerate it. The concept for necessity of continued growth is so engrained in our society, that few question under what kind of conditions, when, why, and for whom it is necessary or beneficial. The populace has been brainwashed for decades to believe if economic growth slows that it will have meaningful negative consequences for our quality of life. Contrariwise, we have been falsely led to believe that if the economy grows rapidly, everyone benefits.

Is economic growth is always necessary for financial security and an improved quality of life? Our lack of reflection on this subject is understandable because of persistent propaganda from our elites regarding a need for growth. Similarly, people have not thought about the nature of money, and the system which produces our national currency. Both are critically important for everyone’s improved livelihoods, but there appears little public understanding as to how or under what conditions economic growth translates into public benefit.

Every national election cycle, the presidential contenders outline their specific approach to accelerating growth of our economy. Occasionally they will note that growth is necessary in order to increase national income which will also provide government with a higher level of collected income taxes – both needed to reduce budget deficits and service our national debt. This becomes a rare example of politicians speaking the truth – growth is needed to pay for increased government spending and our monumental national debt as well as its annual interest servicing cost. Growth is also absolutely necessary for the Federal Reserve so that it can collect interest on our presently outstanding and ever increasing debt. But it is not clear at all that economic growth benefits the populace or individuals need growth to enjoy an improved quality of life. In this context we could evaluate the need for economic (GDP) growth under different conditions - where government budget is disciplined, and currency is not issued by the FED, population growth is abating, manufacturing productivity continues to improve, and unemployment continues to rise.

In Part 1 of this analysis, we look briefly at the way America’s economy worked for its first 140 years, and how it appeared to be working for the next 100 years since the founding of the FED in 1913. Finally, in Part 2 we look at the trends presently driving changes in our economic future and look at how continued technological change will affect future employment, incomes, and how our present economic system will force government policies to change, and what that may mean for our future quality of life.

The first one hundred forty years.

At the founding of America in 1776, this new country is estimated to have consisted of about two and a half million people. Now, only two hundred forty years later this nation contains approximately 330 million people. This seems like an incredible rate of growth – to have a citizenry multiply 132 fold in only 240 years. However, mathematically this amazing population expansion actually represents a compound annual growth rate equal to only 2.06% per year over the entire period. In the early years of this nation that growth rate was somewhat higher, but with the beginning of the last century (1900) the rate of growth started to trend lower and dropped below 2.0%; and by the 1980’s this rate had already dropped consistently to below 1%.

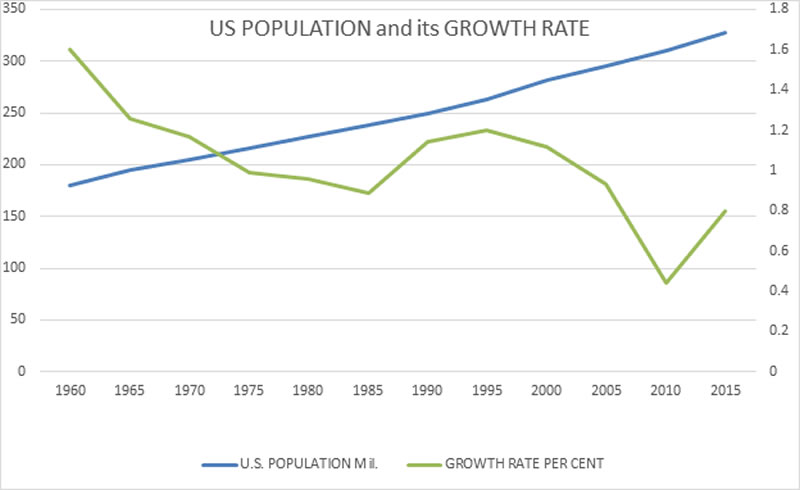

The following chart shows the nation’s population growth, and its rate of growth since 1960. Notice that the decline in the growth rate trend is persistent, except in years 1985-2010 which shows an “echo” of a dramatic rise in population growth shortly after the end of WWII when soldiers coming home from war started new families en masse stimulating population growth.

Source: U.S. Census Data

In the 1800’s an industrial revolution was unfolding based on new scientific advances as it related to the utilization of steam engines and machines to facilitate growth in the production of goods. By today’s standards these relatively primitive factories still significantly increased the amount, and decreased the cost of production for a large variety of goods. Such production fostered the expansion and natural centralization of such manufacturing facilities providing new jobs to an ever larger portion of our then predominantly agrarian populace, while increasing the overall density, growth and population of cities.

Said another way, the population grew both from large family size and immigration from Europe of those seeking religious freedom, escape from poverty or debt imprisonment, and those thirsting for opportunity. This growing mass of humanity required a multitude of consumer products. Industrial factories made possible rapid increases in production, while reduced cost of such consumer products made them available to a broader group of people. This non-farm industrialization made jobs plentiful, providing the employed workers an income which spent it on manufactured goods fostering a virtuous cycle whereby every employed person and the system itself benefited. The economy grew without government guidance, stimulus or manipulation.

Historical economists generally agree that economic growth and wealth creation were best in America during the 1800’s. This period was characterized by rapid population growth, industrialization and productivity improvements, and by very stable money in the form of gold which did not lose value over time.

Taxation of income, fiat currency, usage of government debt, use of corporate or consumer credit and debt, financial or fiscal economic stimulation was rarely practiced before 1913. However, people understood that political decisions do affect the economy. Accordingly, this economy was wisely called the political economy – as it still should. After all, it is politically motivated excessive spending that has corrupted every government, ballooned its national debt, and ruined its currency - ever since people have had rulers or governments. It was understood that economic planning, to the extent that it existed at all, could not be reduced to strict mathematical formulas. That is to say that while in political economics there were some observed correlations, it was never considered a science with precise or absolutely dependable relationships as defined by a scientific formula. Complex and changing human behavior cannot be reduced to a predictable mathematical formula.

It perhaps seems amazing that in the first one hundred forty years of this new country it experienced tremendous growth in prosperity with little or no governmental guidance, regulation, or financial manipulation. This growth occurred without any notable inflation or loss in the value of its currency through inflation, before existence our current fiat legal tender laws, allowing any bank to issue its own local paper currency. The government was small, it had no meaningful budget deficits, essentially no debt (excluding periods of war), and central banking money printing absent. Is it not ironic that all of these characteristics have eroded since governments started to increasingly control, regulate, tax, stimulate and manipulate our economy – and increased centralization of power diminishing state’s and individual rights. Increasing federal dominance has taken place to the apparent detriment of its population, eroding the purchasing power of our currency, and increasing constraints on our individual liberty.

The middle period

In 1900, the population of the nation had already risen to 76.2 million. Concentration of economic power gave rise to a class of wealthy elites, who understandably promoted increased centralization of production, larger corporations, leading to increased profits and political influence. Such trends have continued for decades whereby the relationship between this upper economic class and government leaders and politicians has fortified such that our original constitutional republic has taken on many aspects of corporate capitalism, or worse, a corrupt fascist state. Continued centralization of political and economic power (such as that in the European Union) leads to globalization, a system that increasingly is seen and understood as being hostile to national sovereignty, individual freedom and liberty.

The banking elite saw and implemented a means to both stimulate economic growth and increase initial wellbeing for the populace, while at the same time increasing their dominance of the nation through control and creation of the nation’s money. The system that the newly created Federal Reserve in 1913 utilized was to print and provide the U.S. dollars in exchange for official government debt. Since there was an interest charge on the amount of issued Treasury securities, this system was based on and is dependent on ever increasing amounts of treasury debt issuance. In addition, to secure such debt to the issuing central bank, a national income taxation system had to be implemented. It should be understood that what made this system work was growth of debt and money (both being the two sides of the same thing), secured by increasing taxation of a demographically growing population, supporting or driving an expanding economy. Continued growth of every component of this system is crucial to its survival and very existence.

Money expansion and credit growth

Credit availability initially always feels good, particularly to persons, corporations, or a nation that has very low initial levels of debt. And such credit availability does stimulate spending and investment for a time. The system’s fractional lending also provided a leveraged cyclical increase in credit for over a century. Initially, the FED facilitated America’s participation in WWI by making money and credit available to our government, and soon thereafter it promoted Wall Street speculation by making credit available also to unsophisticated investors and consumers. This stimulation when reversed led to the Great Depression. The FED seemed unable to provide an appropriate financial remedy that would extricate America from its economic depression – it took WWII, with its massive increase in war production spending and attendant national debt explosion to achieve this grudging decades-long recovery.

With America victorious in the war, and much of Europe bombed into rubble, it was not difficult for the dollar to become the currency anchor for Europe, and eventually the world. As the dollar was backed by gold, and after WWII America was by far the largest owner of gold with over 19,000 tons, the global money system seemed solid. But if the currency itself is also to be used in international trade and to become a reserve asset for foreign banks, then there had to be a near infinite rise of dollars printed and available for the rest of the world to use. Another way to say this is that if the US is to satisfy the dollar usage in the world, it must expand its debt so as to create those additional dollars.

Since the dollar was backed by gold at a fixed rate, such large increases in currency created imbalances between dollars and gold. These imbalances were also noticed by foreign governments. Ultimately the amount of dollars created was so large in relation to the value of our gold horde priced at $35 an ounce that the persistent exchange of dollars held by foreign governments for gold had to be forfeited in 1971 – as a means to preserve America’s remaining store of gold of about 9,000 tons. With this unilateral step, which can be characterized as dropping a financial H-bomb on the rest of the world, this system was now free of any constraints to create all the dollars that the world sought, without it impacting America’s gold supply. An agreement by Saudi Arabia to sell oil only in dollars fostered continued globalization of the dollar as its then preferred currency. In addition, the increased utilization of credit for countries, corporations, and consumers expanded the effective amount of currency in the system.

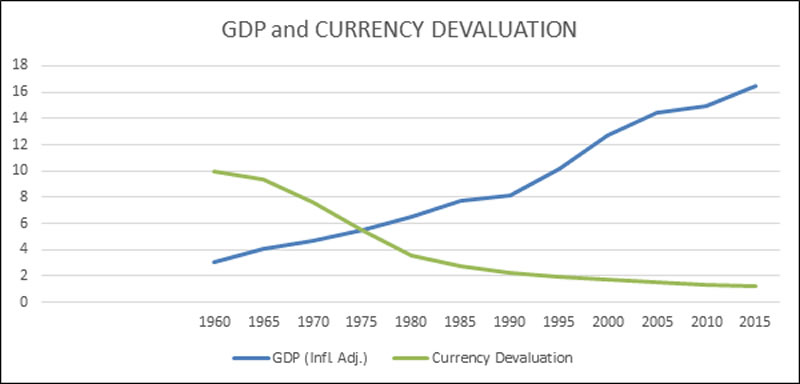

The following chart shows the growth of gross domestic product and the rate of loss in the value of our currency as measured by the change in the CPI over the last 55 years.

Source: Fed Res Bank of Minneapolis

This chart shows that while real GDP has grown from $3.1 billion to $16.5 billion in the last fifty five years, it also shows that over this time the purchasing power of one dollar in 1960 has declined to just $0.12 cents. What this chart therefore demonstrates is that owners of real production facilities and factories benefited from a price increase due to inflation, while wage earners were assaulted with persistent declines in the value of their fiat money savings and earnings.

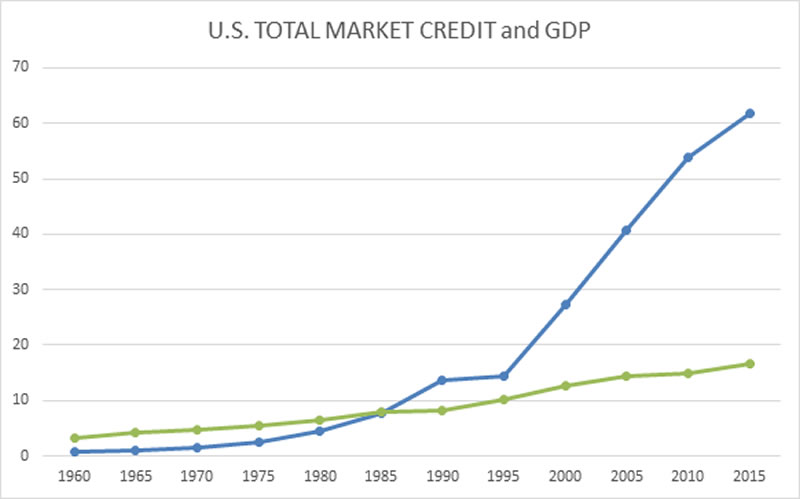

The following table shows the growth of the US growth of GDP between 1960 and 2015, juxtaposed with the amount of money and credit growth in those years. This chart confirms that to provide continued economic growth for an advanced economy, of an aged and slowing growth in US population, it required an ever larger amount of credit stimulus – depicted by the increasing divergence in the two components of this chart. This chart also corroborates that the growth of our economy required ever more credit growth to support it particularly after 1995. Since personal credit is at a level that can no longer be supported, serviced, or increased, it means that little or no more personal credit can be created to support further increases in GDP, which then acts as a drag on future GDP growth.

As a result, government spending has expanded dramatically over the last decade – as our national debt rose from $ 8.2 trillion in 2006 to $19.9 trillion, an astronomical rise. There is some fallacy of calling this national debt. In reality it is debt incurred by the state on behalf of taxpayers but without their direct approval. This debt is created by our elected officials, yet it can only be repaid by the same individual taxpayers who have rejected taking on more personal debt. So the public has been forced to take on this debt by a corrupt government - a debt which citizens cannot afford to repay.

$ Trillions

Source: Fed Res Bank St. Louis

This chart also demonstrates that the old economic model has developed dramatic distortions, and no longer responds to stimulus in familiar ways, nor functions the way that it was previously anticipated – signaling a transition to a new economy with different requirements for its currency, credit, much lower debt saturation, reindustrialization of manufacturing, and decentralization of both manufacturing and government, and other changes described in greater detail in Part 2.

Current demographic trends, and state of our old model economy.

It is worthwhile to reflect on the fact that our domestic population growth has been slowing for decades. It will continue to slow, as more people are postponing or foregoing the formation of families, and those who are seeking to become married are doing so at an older age, leaving less time and opportunity for childbearing. Given the desire for women to have meaningful careers outside the home, it is foreseeable that family size will continue to shrink in the future. Also, the historic expense of raising a child was low when compared to today’s much higher cost. All of these disincentives are operating to reduce family size and population growth and total population in the future.

These are not necessarily unhealthy natural trends for mankind. Consider the 2.06% growth rate of the country over the last 240 years that we cited previously. If America’s population continued to grow at this historic rate our population would double again to 660 million by 2052, in just 36 years. And, in 108 years from today America’s population would rise to 2,640 million, or roughly twice the number now living in China -with its land mass nearly identical with America. Yes, at some point in the not too distant future such growth begins to appear as unsustainable or improbable, and certainly undesirable.

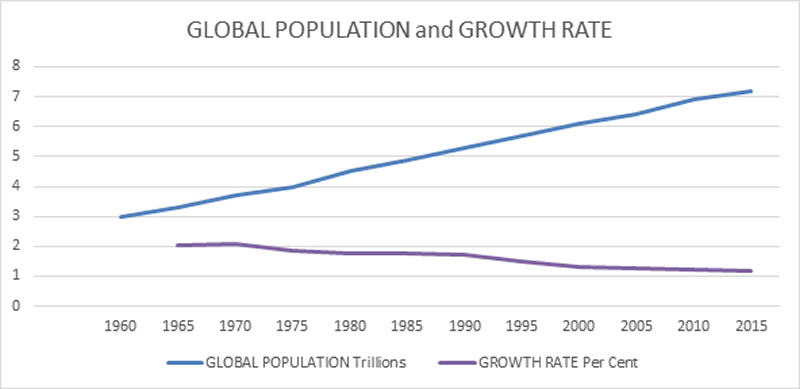

If America’s historic population growth rate, which is lower than that of the emerging and developing world was applied to global population, then in 108 years our global population would bloat by eight times to an approximate 57 billion people. It is debatable what kind of a quality of life that many people could have on this planet with its ultimately finite resources.

Population growth in Europe is experiencing greater deceleration than America. The population of Europe (exclusive of possible massive and continuing Mideast in-migration or invasion) is projected to decline over the next fifty years. Surprisingly, family size has declined over the last fifty years even in the emerging and developing world. Hence there is a reasonable expectation that global population will stabilize by natural trends which have been visible in the world for over four decades.

The mature or more advanced nations are now experiencing a declining growth rate in population. This population has a higher average age than that of developing nations. The people of these more advanced nations have owned more of world produced products – they have likely owned more “stuff” than they need. Now that their average age is trending higher, their spending patterns have changed. Retired people simply spend less money on stuff – they have already accumulated it over previous decades. All of these factors have implications for the amount of money the developed world and the rest of the world consumers will spend in the future. It is an important determinant of the future growth of our economy, and those other mature advanced economies. For those seeking investment opportunities, this divergence between future growth of matured and developing economies, and young and goods-seeking populations in developing countries has definitive investment implications.

From the preceding charts and observations we can see that our economy is no longer working according to economist and politician expectations or their financial models. We are at a transition point where the old economic model must make way for a new one. Is economic growth necessary for a country and its people to thrive? Exactly who does growth benefit most: government, owners of productive facilities, the FED and its banking system, or people? In Part 2 of this thesis we look more closely at changes which will likely occur in our economy and its governance, whether we foster this change with foresight, or resist it through deliberate political obstinacy.

Raymond Matison

Mr. Matison is a U.S. patriot who immigrated to this country in 1949. With a B.S. in engineering physics, an M.S. in Actuarial Science, work in the actuarial field, and as a financial analyst at Legg, Mason Inc., Lehman Brothers, and investment banking at Kidder Peabody, and Merrill Lynch provides a diverse background for experience. First-hand exposure to fascism, socialism, and communism as well as the completion of a U.S. Army military intelligence course in the 1960’s have inspired a continuing interest in selected topics in science, military, and economics. He can be e-mailed at rmatison@msn.com

Copyright © 2006 Raymond Matison - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.