Stock Market Bottom Near? We Don't Think So

Stock-Markets / Stocks Bear Market Oct 27, 2008 - 01:53 PM GMTBy: Richard_Shaw

Market timing is not a good idea, but standing aside when a global train wreck is happening in proportions that rival the worst periods in modern history is not market timing — it is self-preservation.

Market timing is not a good idea, but standing aside when a global train wreck is happening in proportions that rival the worst periods in modern history is not market timing — it is self-preservation.

Being out of the market makes deciding how to re-enter problematic, and some opportunity could be missed, but far greater opportunity is missed if capital is destroyed.

We are in cash from 80% to 100% in various accounts since mid-summer.

We believe that discretion is the better part of valor in this situation. Nobody really knows what comes next. We are in a Black Swan. The unknown unknowns dominate.

In times of such lack of clarity, we think keeping powder dry is probably a good thing to do.

As Alan Abelson said in his editorial this week in Barron's:

The climate, in our jaundiced view, remains treacherous. The economy is destined to get worse - much worse, before it gets better. And that means that in the months ahead, and perhaps longer, stocks are in for a remorseless barrage of disappointments, jolts and shocks.

Or as a 92 year-old economist, Anna Schwartz, who has lived through most of modern stock market history said this about the current US government “bailout” in the same Barron's issue:

It's like a bunch of guys that are making it up as they go along. They talk about transparency and what they present is opacity, programs that don't make sense, and are not fully laid out. This only increases the already high level of uncertainty and anxiety. … we don't know who's solvent and whose not … the risk of being unclear and doing things ad hoc is that you gradually destroy faith in the financial system.

Earnings estimate are falling and actual dividends are reducing.

Until the government stops announcing new programs to solve new problems most investors didn't know existed, confidence will not return. Until the “E” in P/E stops going down, the “P” won't stop going down, whether the trailing P/E is historically fair or not.

See our prior articles on:

- S&P 500 Calendar Returns Since 1927

- S&P 800?

- S&P 400?

- No Place to Hide (country funds)

- 360 World Markets View

Pitfalls of Cash:

High cash positions are seen by some as tactically or strategically wise. Others see holding cash as a futile attempt to beat the market — having to be right twice, once getting out, and then getting back in again.

Certainly, on average in most periods market timing is not a good idea. Most timers underperform in the long-run. However, in these extraordinary circumstances, our concern is surviving the short-term to participate in the long-term.

We acknowledge the arguments that there have been strong recoveries from many of the prior negative years. For example, the S&P 54% rise in 1933 two years after the 43% loss in 1931.

An unfortunate counterpoint is that going down from 100 to 57 (a 43% loss) and then experiencing a 54% gain, only brings the total back to 88 — still a loss.

Those who had cash at the end of 1931 might have participated in the 54% gain. Those who rode down and up, still had a loss of 12% after three years (1931-1933).

It is true that there are bursts of upward movement in the market that if missed, leave the cash holding investor permanently behind. The converse is also true that there are downward bursts in the market that if experienced by holding stocks, leaves the stock investor permanently behind the cash holding investor.

Arguing against timing, Morningstar calculates that the average mutual fund investor achieves a significantly lower average portfolio return than the returns of the funds they hold. That is presumably due to ineffective market timing — getting out late and getting back in late.

Let's assume for the moment that the market goes down 50% in year one and then goes up 75% in year two. That means $100 goes down to $50 and then up to $87.50.

If the investor got out late after 1/2 of the crash, the cash position would be $75. If the investor then got in late after 2/3 of the recovery, the final net worth would be $93.75 — better than staying fully invested.

As of Oct 24, our $100 beginning Jan 1, 2008 is now $92.53. We have conserved about $32 so far by standing aside. If this is the bottom and if somehow the market rises all the way back to its prior peak (a 67% rise) AND if we miss 2/3 of that rise by somehow being reluctant to get back in, we would still end up with over $112 — a net gain. We hope we are clever enough to get back in before 2/3 of the recovery takes place, but think we have room to be conservative.

Raise Cash Now?

The big question for those invested today is whether it makes sense to raise cash now. For most TV talking-heads, the answer is a resounding “NO!” — either because timing is bad, or because the market is near a bottom.

When you listen to or read comments by those saying a bottom is in, or that it is not a good idea to be out of the market, or to rotate to defensive sectors, ask yourself if their self-interest requires people to stay invested.

Separate those commentators who do not depend on your money being exposed to risk from those who do. You will notice quite different appraisals and suggestions.

Those whose self-interest is neutral to your investment decisions give answers ranging from “No”, to “It Depends on your time time horizon to spend the money” to “Yes, because the market is not close to a bottom yet”.

Most TV talking-head advice is dispensed as if all investors are the same. However, advice for 25 year old investors is not suitable for 65 year old investors. Advice for abundantly wealthy mature investors is not suitable for mature investors with little margin for error.

Are We Near a Bottom?

We don't know. We don't think so, but hope so.

Perhaps a deeper bottom is better for us and other cash holders, but we'd be happy for a bottom here and now.

We are certainly watching closely, but not in an over-reactive way for clear signs of stability and value we can believe in. Our shopping list is growing, but our cash is still in our pocket. There is no hurry.

We hope for a bottom, because far worse things than market crashes could arise if the world economy falls too much further — major wars, for instance, are sometimes born out of economic disasters. Unknowable, but likely undesirable further and permanent changes to the US role in world economics could result — the alternatives are unclear and could be worse.

Arguments For a Near Bottom:

Statistics can be used to project a bottom around this level.

Barron's says the S&P 500 at 876 is trading at about 10 times 2007 trailing earnings of $85, and the dividend yield is at 3%. They say European stocks are yielding 6%.

Some say the decline approaches that of the Great Depression, and we aren't in a depression.

Others are comforted that governments are now in charge of the solution, and have the ability to print all the money they need to fix things.

Dividend yields are high and juicy. Warren Buffet is buying in. Short interest in NASDAQ stocks fell 10% in the first half of October.

Even standard deviations can be used to support a bottom.

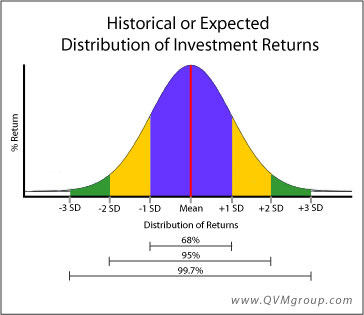

Standard Deviations:

The real world of investing does not behave in a theoretically pure way, but according to theory, more than 99% (nearly 100%) of all observed returns over time fall within the mean return, plus or minus three standard deviations of return. There are rare “fat tail” situations that fall outside of three standard deviations, but probabilistically, three standard deviations covers almost all of what we experience.

With that as background, where are we with the S&P 500 index today?

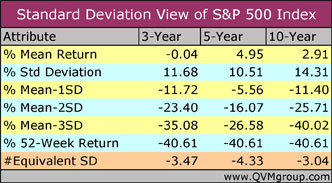

The 3-year, 5-year and 10-year mean returns and standard deviations reported on the Index Universe site today, are shown in this table. The table also shows the mean return for each time period minus 1, 2 and 3 standard deviations of return. Comparing those calculations to the current 52-week S&P return, we can see that we are outside of the three standard deviation range. That provides a strong “mean-reversion” argument — probabilistically. In fact, we are past 4 standard deviations on a 5-year basis.

Arguments Against a Near Bottom:

This is a Black Swan period, not just a down market period. We are in the “fat tail” outside of three standard deviations. That is like being inside of worm hole in space. The unknowns are huge. You don't know where it goes until you come out the other side.

We have some long-term growth channel arguments that another 25% to 50% decline from here is possible, although not necessarily probable.

Our leaders are just ordinary humans, not geniuses or gods, and they are the ones who let the current situation develop (arguably, some of them encouraged steps that led to the problem).

The president of the US doesn't go on TV trying to reassure the population that all is well or will be soon, unless the problems are overwhelming. The US Treasury Secretary doesn't say, “raw capitalism is dead” inside of three standard deviations.

The typically hedged and obfuscated language of former Fed Chairman Greenspan was crystal clear, when he said this to Congress last week:

We are in the midst of a once-in-a century credit tsunami … This crisis … has turned out to be much broader than anything I could have imagined.

We would never have imagined we would hear words like that from him.

Bridgewater Associates of Weport CT ($150 billion in currency and bonds) says, according to Barron's:

… the world is entering a depression caused by irreversible deleveraging spiral in which super-low interest rates will have little economic impact.

Post-script to the Bridgewater statement; think Japan after their crash.

January 2008 could be a watershed month. New leaders are about to be installed — new president, new Treasury Secretary, new Congress, possibly new agency heads. New regulations and new taxes are about to be enacted, and probably new economic resurrection programs.

A global recession is descending.

Earnings reports and estimates are still declining. Dividends are declining, not just earning and prices.

Senator Schumer has called for a ban on dividends to shareholders from banks receiving federal investments. How such a ban would roll through the markets is unclear, but probably not pretty.

Newly “cheap” oil will moderate the negative effect on developed world economies, but cheap oil can't compensate for no job or higher taxes. And, the reduced stress on the developed world due to reduced oil prices will be replaced by increased stresses in developing economies that generally supply the world with oil.

The Christmas retail season is nearly upon us and the combination of poor retail earnings that are likely, along with the negative psychology associated with the news of a poor retail season will not be helpful to the markets.

Even inspirational characters such as Warren Buffet, say they are looking at 5, 10 and 20 years as their investment time horizon. He is not calling a bottom, just the sense that value exists — and he is negotiating senior positions not availale to you and me.

Billionaires can afford to endure major drawdowns and wait years. Retirees who rely on portfolios to live cannot, unless they have hefty dividend and interest income to tide them over. Just hope Senator Schumer doesn't manage to ban those dividends.

Conclusion:

Great caution is appropriate. Holding cash is no cause for shame.

Take the long-view both forward and backward as you decide what the future holds. No advice can be a one-size fits all. Know you resources, needs and limits; both financially and psychologically.

These are not ordinary times and you should not use usual and customary thinking to attempt to appraise the situation.

Listen to all the voices, but understand their intrinsic biases and conflicts, apply your own judgement and chose wisely.

Be clear to yourself which assets you must conserve and which you can risk losing or risk holding at lower price levels for years while awaiting recovery.

Decide now what you would like to own, and set target prices to buy when and if the price levels are achieved.

Consider emphasizing dividend cash flow to you more than in past periods, to enable you to comfortably afford to hold assets that may fall in price after you buy them.

Be sure to have liquid cash for all portfolio dependent expenditure needs for the next 12 months. Keep at least those assets you may need in the next couple of years in short-term, high quality bonds.

With the rest, make your strategic decision about the level of risk you wish to take for return, and be aware of the time horizon required for your risk investments to likely work out.

Sell (raise cash) until you can sleep, and hold at least enough cash to see you through the current troubles for 12 months or more.

By Richard Shaw

http://www.qvmgroup.com

Richard Shaw leads the QVM team as President of QVM Group. Richard has extensive investment industry experience including serving on the board of directors of two large investment management companies, including Aberdeen Asset Management (listed London Stock Exchange) and as a charter investor and director of Lending Tree ( download short professional profile ). He provides portfolio design and management services to individual and corporate clients. He also edits the QVM investment blog. His writings are generally republished by SeekingAlpha and Reuters and are linked to sites such as Kiplinger and Yahoo Finance and other sites. He is a 1970 graduate of Dartmouth College.

Copyright 2006-2008 by QVM Group LLC All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Richard Shaw Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.