Global Stock Markets Short Covering Rally

Stock-Markets / Stocks Bear Market Mar 15, 2009 - 06:03 AM GMT

Global stock markets surged over the past four days as investors adopted a more positive view of the prospects for the beleaguered financial sector and shrugged aside gloom about the economy. Citigroup (C) on Tuesday said it had turned a profit from operations for January and February (BUT did not mention credit losses, toxic paper, derivatives, etc.). JPMorgan (JPM) and Bank of America (BAC) later made similar comments.

Global stock markets surged over the past four days as investors adopted a more positive view of the prospects for the beleaguered financial sector and shrugged aside gloom about the economy. Citigroup (C) on Tuesday said it had turned a profit from operations for January and February (BUT did not mention credit losses, toxic paper, derivatives, etc.). JPMorgan (JPM) and Bank of America (BAC) later made similar comments.

A positive shift in investor sentiment, together with the possibility of the suspension of mark-to-market accounting and the reinstitution of the uptick rule, resulted in the best week for equities since November.

Arriving in time for my 54 th birthday today, the reversal of fortune is illustrated by the strong gains of the MSCI World Index (+9.8%) and the MSCI Emerging Markets Index (+8.8%) since Tuesday. Although stashed (or “panic”) cash was deployed, the top-performing stocks were the most pummeled ones of the past few months, indicating significant short-covering.

Extremely oversold markets bounced off levels last seen 12 years ago in the case of the S&P 500 Index and the FTSE Eurofirst 300 Index, and 26 years ago as far as the Nikkei 225 Average is concerned. Talking about being oversold, the Dow Jones Industrial Index has been down for 13 of the past 16 months.

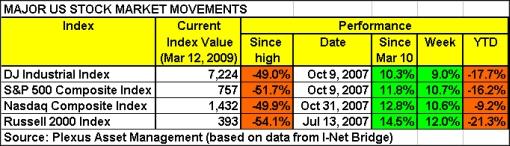

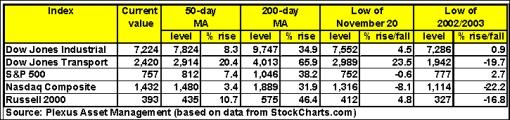

As shown in the table below, the major US indices gained strongly during the week, recording only the second up-week out of ten in 2009.

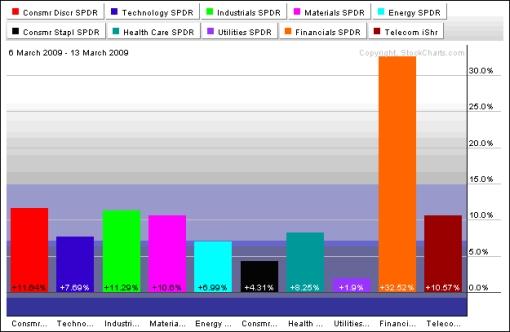

As far as exchange-traded funds (ETF) are concerned, John Nyaradi ( Wall Street Sector Selector ) reports that the battered financial sector last week rose like the legendary Phoenix with the Financial Select Sector SPDR (XLF) surging by 32.5%. ETFs like iShares Regional Banks (IAT) (+31.1%) and SPDR S&P Homebuilders (XHB) (+19.8%) also recorded handsome gains. Interestingly, the broad financial sector was the only main US economic sector to beat the top-performing broad index ETF, the Russell 2000 (IWM), which added “only” 11.9% on the week.

Source: StockCharts.com

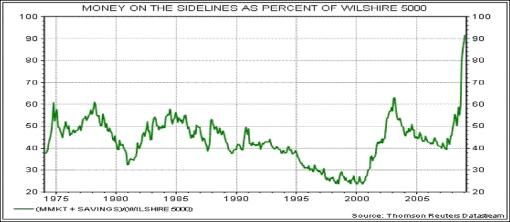

The fact that government bonds had not been sold off during the equity rally indicates that some “side-lined” cash was deployed to fund the buy orders. The amount of cash hoarded over the past few months as a result of precautionary savings and deleveraging is enormous, as seen from the fact that money-market and savings accounts constitute more than 90% of the market capitalization of the Wilshire 5000 Index. (Hat tip: Todd Sullivan, Value Plays .)

Still on the topic of government bonds, according to CEP News , Chinese Premier Wen Jiabao said on Friday that China was growing “worried” about the safety of US Treasuries and wanted assurances from the United States. “I request the US to maintain its good credit, to honour its promises and to guarantee the safety of China's assets,” he said, voicing concerns over the state of the American economy. This is not good news for the massive issuance of US government bonds that lies ahead.

UK government bond prices surged to record levels as the Bank of England launched its £75 billion program of buying securities to expand the money supply. The yield of the ten-year Gilt plunged by 40 basis points to close at 2.95% after having touched 2.91% earlier - its lowest level ever.

The US dollar lost ground as the rally in global equities kept the greenback in check and was further undermined by Wen Jiabao's comments about China's dollar reserves. However, the announcement by the Swiss National Bank to intervene by devaluing the Swiss franc dominated news in the currency markets. This step was a strong signal of the severity of the global recession and knocked the Swiss franc back by 2.5% against the US dollar and 4.7% against the euro (see chart below) on the week.

Source: StockCharts.com

Commenting on the SNB's decision, Bill King ( The King Report ) said: “This is the dangerous aspect of the game - competitive currency debasement and ‘beggar-thy-neighbor' trade policies. Tariffs and other trade barriers usually result. So trade diminishes but inflation jumps. Once the monetization card is played, the market must commence a watch for extraordinary inflation.”

The SNB's move provided support for the gold price (although still down by 1.3% on the week) as more hedge funds are turning to the yellow metal. David Einhorn of hedge fund Greenlight Capital wrote in a recent letter to his investors (as quoted in the Financial Times ): “Our instinct is that gold will do well either way: deflation will lead to further steps to debase the currency, while inflation speaks for itself.”

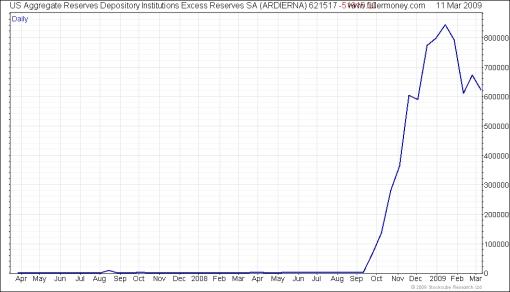

On the credit front, the TED spread (i.e. three-month dollar LIBOR less three-month Treasury Bills) is showing renewed stress as it has widened by 20 basis points since February 10 (also see “ Credit market conditions - an update “). However, a graph of the US Depository Institutions Aggregate Excess Reserves (shown below) makes for interesting reading. Although the level of reserves is still far in excess of the amount banks need to keep on deposit to meet their requirements, the decline in this measure could be indicating a turning point in the recovery of banks. But the speed of the recovery, needless to say, remains unknown.

Source: Fullermoney

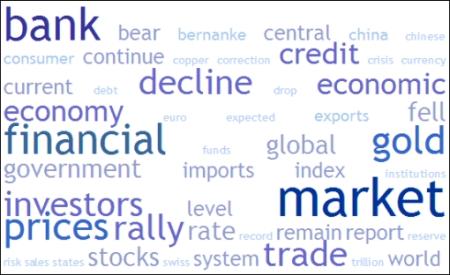

Next, a quick textual analysis of my week's reading. No surprises here as the picture is almost identical to that of last week with key words such as “bank”, “financial” and “market” still featuring prominently. “Gold” seems to be on the ascent.

The stock market “internals”, or market breadth, like the up/down volume spread, the advance/decline spread and new highs/lows have improved dramatically over the past few days and auger well for the nascent rally. Yet, the market still needs to do a considerable amount of work before evidence of a primary bear market low will be demonstrated. As a first step, the indices must clear their respective 50-day moving averages, i.e. the S&P 500 and Dow Industrials need to rise by 7.4% and 8.3% respectively.

I will soon have the privilege to meet face-to-face with Richard Russell ( Dow Theory Letters ) again at the time of his Tribute Dinner in San Diego on April 4, when he will undoubtedly share his market wisdom. Meanwhile, he commented as follows yesterday: “So where are we now? Over the last few weeks the market has become drastically oversold - at the same time investors' sentiment has grown progressively more bearish. Furthermore, since September 2008 we have experienced an amazing twenty-one 90% down-days, which may have exhausted the urge by big investors to sell.

“By the way, yesterday [Thursday] was a 90% up-day, the second of this week. This action strengthens the thesis that this advance has further to go.

“… are we now in a new-born bull market, or is this an upward correction in an oversold bear market? … on the basis of duration and values, I believe we are experiencing a significant upward correction in an ongoing bear market.

“How far might this rally carry? Every movement in the stock market, minor, secondary or primary, is eventually corrected. Upward corrections in bear markets tend to recoup one-third to two-thirds of the ground lost in the preceding down-leg. The bear market will do whatever it has to relieve its oversold condition and at the same time lure the greatest number of investors back into its folds.”

On the topic of rally “targets”, Adam Hewitson of INO.com prepared a few slides dealing specifically with key levels. Click here to access the presentation.

Not putting his faith in further upside potential, Bennet Sedacca ( Atlantic Advisors ) said on Friday: “We are taking profits after the recent 13% move in equities. The macro-economic view is just too negative for me. It never, ever hurts to take a profit. We are back to 0% equities.” Sedacca's price target for the S&P 500 is in the 350-400 range, which is a decline of 47-54% from current levels. He sees the ultimate low only by October 2010.

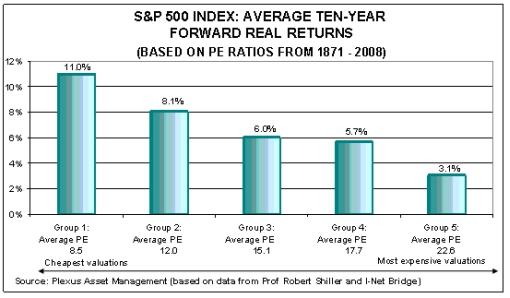

Using rolling ten-year reported earnings, my research (based on Robert Shiller 's CAPE methodology) shows that the “normalized” price-earnings ratio of the S&P 500 Index is currently 12.6. This compares with a long-term average of just more than 15. Based on the historical PE/return patterns, this would imply average ten-year real returns off these levels in the order of 8% (see graph below). Although, at index level, this may not grab one as bargain basement returns, it certainly is starting to point to a broad area within which opportunities should arise for the judicious stock picker.

The debate on whether stock markets are witnessing A bottom or THE bottom will take a while longer to resolve. Taking one step at a time, it is quite conceivable that the rally may last until the release of potentially ugly earnings and guidance announcements in April, by when a clearer picture should emerge on whether the bottom has been reached or yet lower levels are in store.

For more discussion about the direction of stock markets, also see my recent posts “ Stock markets: Relief rally or new bull? “, “ Technical talk: S&P 500 up against resistance levels “, “ Video-o-rama: Stock markets - turnaround time ” and “ Jeremy Grantham: Reinvesting when terrified “. (And do make a point of listening to Donald Coxe's webcast of Friday, which can be accessed from the sidebar of the Investment Postcards site.)

Economy

“Global business confidence … remains very near the record low that has prevailed since last November. Sentiment is eerily weak across the entire globe and all industries. Oddly, US business confidence, while very poor, seems a bit better than anywhere else,” said the latest Survey of Business Confidence of the World conducted by Moody's Economy.com . “Most worrisome is the recent collapse in pricing power; a record over one-third of respondents now say they are cutting prices for their goods and services.”

Source: Moody's Economy.com , March 9, 2009.

European Central Bank member Jürgen Stark said the world economy is in its deepest slump since the Second World War and that it was difficult to predict when it would end, as reported by CEP News .

Also, analysts at JPMorgan note (via the Financial Times ) that 30 out of the 35 countries they cover saw activity contracting at the end of last year, with those economies most linked to global trade flows, rather than those at the root of the financial crisis, hit hardest.

Grim trade data from China also spooked economists. The country's trade surplus plunged to $4.8 billion in February, about an eighth of the amount in the previous month, as exports tumbled by 25.7% from a year earlier and imports fell by 24.1%. According to CEP News , Premier Wen Jiabao was quick to add that China remained firm in its commitment to deliver an annual 8% growth rate for 2009 and had “adequate ammunition” to “introduce new stimulus policies”.

Grim trade data from China also spooked economists. The country's trade surplus plunged to $4.8 billion in February, about an eighth of the amount in the previous month, as exports tumbled by 25.7% from a year earlier and imports fell by 24.1%. According to CEP News , Premier Wen Jiabao was quick to add that China remained firm in its commitment to deliver an annual 8% growth rate for 2009 and had “adequate ammunition” to “introduce new stimulus policies”.

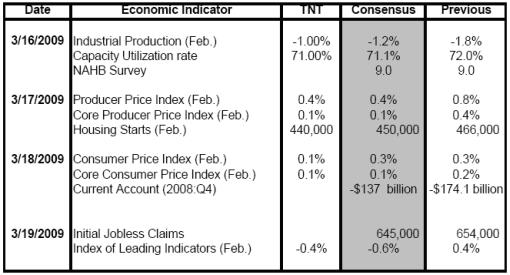

A snapshot of the week's US economic data is provided below. (Click on the dates to see Northern Trust 's assessment of the various data releases.)

March 13, 2009

• Despite impressive improvement in nominal terms, real trade deficit will be a drag on Q1 GDP

March 12, 2009

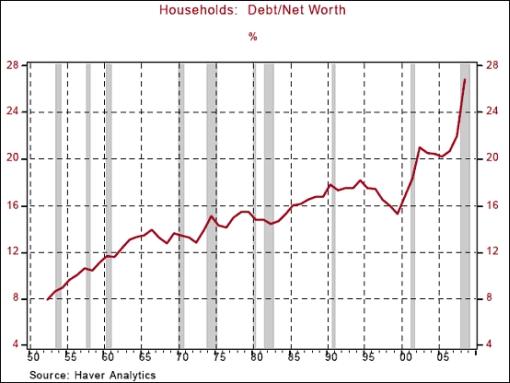

• Household net worth recorded historical plunge

• Consumer spending - less pronounced weakness in Q1

• Inventories-sales ratio holds steady in January

• Labor market remains mired in a recession

March 11, 2009

• Credit market conditions - renewed stress

March 10, 2009

• Bernanke sketched out financial reform agenda to “address systemic risk”

• Wholesale trade report - significant drop in demand

• NFIB Survey shows small business optimism at lowest point since 1980

Commenting on the better-than-expected retail sales data and the issue of whether the US consumer could prove more resilient than feared, Asha Bangalore ( Northern Trust ) said: “The important question is if this pace of gains in retail sales will prevail in an environment where employment conditions are abysmal. The dire employment situation persuades us to forecast weakness in consumer spending in the near term.”

Also jeopardizing the consumer's firepower is a sharp decline in household net worth, falling by $5.1 trillion in the fourth quarter of 2008 for an annual decline of $11.2 trillion - slightly below the mark seen in 2004. “Net worth of households has declined and their debt levels have grown noticeably slowly in 2008. But, the sharp drop in net worth has led to a debt-to-net worth ratio for households that is alarming,” said Bangalore .

Week's economic reports

Click here for the week's economy in pictures, courtesy of Jake of EconomPic Data .

| Date | Time (ET) | Statistic | For | Actual | Briefing Forecast | Market Expects | Prior |

| Mar 10 | 10:00 AM | Wholesale Inventories | Jan | -0.7% | -1.1% | -1.0% | -1.5% |

| Mar 11 | 10:30 AM | Crude Inventories | 03/06 | +749K | NA | NA | -757K |

| Mar 11 | 2:00 PM | Treasury Budget | Feb | -$192.8B | NA | -$205B | -$175.6B |

| Mar 12 | 8:30 AM | Initial Claims | 03/07 | 654K | 640K | 644K | 645K |

| Mar 12 | 8:30 AM | Retail Sales | Feb | -0.1% | -0.3% | -0.5% | 1.8% |

| Mar 12 | 8:30 AM | Retail Sales ex-auto | Feb | 0.7% | -0.1% | -0.1% | 1.6% |

| Mar 12 | 10:00 AM | Business Inventories | Jan | -1.1% | -1.1% | -1.0% | -1.6% |

| Mar 13 | 8:30 AM | Export Prices ex-agriculture | Feb | 0.1% | NA | NA | 0.1% |

| Mar 13 | 8:30 AM | Import Prices ex-oil | Feb | -0.6% | NA | NA | -0.8% |

| Mar 13 | 8:30 AM | Trade Balance | Jan | -$36.0B | -$37.5B | -$38.0B | -$39.9B |

| Mar 13 | 10:00 AM | Michigan Sentiment(preliminary) | Mar | 56.6 | 56.5 | 55.0 | 56.3 |

Source: Yahoo Finance , March 13, 2009.

In addition to interest rate announcements by the Bank of Japan (Tuesday, March 17) and the Federal Open Market Committee (Wednesday, March 18), the US economic highlights for the week include the following:

Source: Northern Trust

Click the links below for the following reports:

• Wachovia's Weekly US Economic & Financial Commentary (March 13, 2009)

• Wachovia's Monthly Economic Outlook (March 2009)

• Wachovia's Global Chartbook (March 2009)

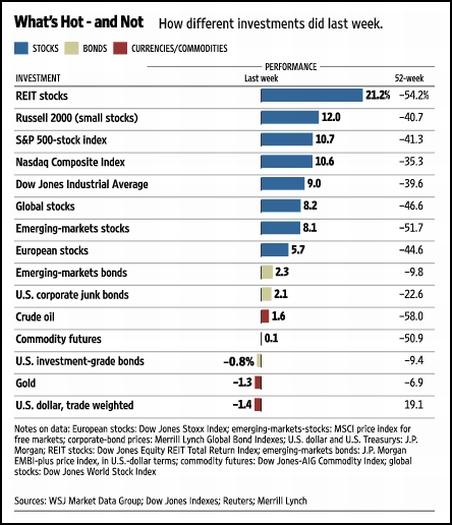

The performance chart obtained from the Wall Street Journal Online shows how different global markets performed during the past week.

Source: Wall Street Journal Online , March 13, 2009.

People calculate too much and think too little,” said Charlie Munger (hat tip: Harry Newton ). It is hoped the “Words from the Wise” reviews will provide Investment Postcards readers with the necessary material to stimulate the thinking process and add structure to their investment decisions.

That's the way it looks from Cape Town (where friends are arriving for my birthday celebrations).

Hat tip: Barry Ritholtz , The Big Picture , March 13, 2009.

Richard Russell (Dow Theory Letters): Amazing facts in the new world

“The true deficit of the federal government is a $65.5 trillion in total obligations. This exceeds the gross domestic product of the entire world.

“Empty houses in the US now number about 14 million or one in nine homes.

“At the forum in Davos, it was revealed the 40% of the world's wealth has been destroyed by the financial crisis so far.

“The International Labor Organization now estimates that global unemployment in 2009 could increase to 198 million or 230 million in the worst case scenario.

“In short, the biggest bubble of them all - that the US dollar is ‘money' - is about to pop. The US dollar is on the path to the fiat currency graveyard, and will soon get there.”

Source: Richard Russell, Dow Theory Letters , March 10, 2009.

CNBC: Warren Buffett - billionaire next door

“Thoughts on the steps needed for economic recovery, with Warren Buffett, Berkshire Hathaway chairman/CEO.”

Source: CNBC , March 9, 2009.

CEP News: Buffett says “everything will be all right”

“Even though the US economy has ‘fallen off a cliff', and unemployment is likely to climb higher, billionaire Warren Buffett remains optimistic about the long term, he told CNBC on Monday.

“‘Everything will be all right', he said. ‘We do have the greatest economic machine that man has ever created.'

“However, Buffett, who runs Berkshire Hathaway, said fear and uncertainty have taken hold of investor behaviour, which now requires strong leadership from President Barack Obama as the US fights an economic war.

‘What is required is a commander in chief that's looked at like a commander in chief in a time of war,' Buffett said, adding that the President needs to restore faith in the financial system, letting American know their money is safe, even in the event of another bank failure.

“‘If you don't trust where you have your money, the world stops,' he told CNBC.

“Buffett said that Americans need to accept that government actions aimed at helping the economy will inevitably help some people who made poor decisions that contributed to the problem in the first place. However, everyone is in the same boat now, he said.

“‘The people that behaved well are no doubt going to find themselves taking care of the people who didn't behave well,' he said.”

Source: CEP News , March 9, 2009.

CEP News: ECB's Stark says global economy in deepest slump since WWII

“European Central Bank member Jürgen Stark said the world economy is in its deepest slump since the Second World War and said that it is difficult to predict when it will end.

“‘The year 2009 will be a very difficult year,' Stark said at the fifth German-Luxembourgish Economic Conference in Luxembourg on Monday. ‘Policy makers need to prevent a further deterioration in economic and financial conditions.'

“However, central banks alone cannot solve the crisis, Stark said, adding that measures to restructure and recapitalize the banking sector are also needed. ‘(This year) will be the year of adjustments in the balance sheets of banks, firms and private households,' Stark said.

“Stark also said that rate reductions alone would not bring an end to the crisis and that rates at too low a level could be counterproductive.

“‘(Low rates) have the potential to weaken the incentives for banks to clean up their balance sheet of troubled assets and monitor their credit risk carefully,' Stark said, echoing comments made previously to a Luxembourg newspaper over the weekend.

“He also said that while the ECB has room to cut its policy rate further, there is a limit to every policy and that the ECB's key policy rate at 1.50% is already ‘very low'.

“Stark added that current measures taken by the central bank, including the expansion of its balance sheet and accepting corporate loans as collateral, are already unconventional and that there are limits regarding these measures as well.”

Source: CEP News , March 9, 2009.

Financial Times: Economic outlook - fears for industrial output

“The worldwide crisis in financial markets and the deepening global economic recession are feeding off each other furiously in spite of governments slashing interest rates and ramping up public spending in their efforts to stave off a prolonged depression.

“Analysts at JPMorgan note that 30 out of the 35 countries they cover saw activity contracting at the end of last year, with those economies most linked to global trade flows, rather than those at the root of the financial crisis, hit hardest.

“Meanwhile, the threat to the health of the banking system from the credit crunch has not abated.

“While banks have been applying more stringent lending criteria to new loans, in the eurozone companies have been able to draw down on existing credit lines so year-on-year growth in corporate lending has remained ‘strikingly robust', according to UBS.

“Nick Davey at UBS says corporate credit remains a major threat to the health of the eurozone banking sector. He says credit lines agreed pre-crisis are likely to have been inadequately priced for the current severe economic recession and that banks will face a significant rise in corporate defaults in 2009.”

Source: Chris Flood, Financial Times , March 8, 2009.

Did you enjoy this post? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2009 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Prieur du Plessis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Comments

|

MIKE BRONZINO

18 Mar 09, 07:28 |

COMMENTS

I LOVE YOUR ANALYSIS IT IS BRILLIANT! |