Banking System Collpase, on the Edge of The Precipice, Basel III

Politics / Credit Crisis 2010 Sep 22, 2010 - 03:42 AM GMTBy: Matthias_Chang

The Global Too Big To Fail Banks are so precarious that literally anything can trigger a collapse in the coming months.

The Global Too Big To Fail Banks are so precarious that literally anything can trigger a collapse in the coming months.

I have read recent commentaries on Basel III posted to various renowned websites and financial publication, but they missed (or deliberately misled) the underlying message of the proposals, the implementation of which will be delayed till 2017 and some till 2019.

Basel III is pure spin and its timing was to assuage the deep-seated fears that there are no solutions in sight to save the fiat money system and fractional reserve banking.

Basel III is pure spin and its timing was to assuage the deep-seated fears that there are no solutions in sight to save the fiat money system and fractional reserve banking.

THE PROBLEM

The major global banks are all under-capitalised and this was all too apparent when Lehman Bros. collapsed. Banks were borrowing so much and so recklessly to play at the global casino that when the bets went sour, they were staring at a black-hole in the $trillions. In fact the banks are all insolvent.

The problem was compounded when the central bankers (all are corrupt without exception) and regulators turned a blind eye to how bankers defined what constituted “capital” so as to circumvent the need to maintain the capital ratio.

THE BASEL III SOLUTION

At its 12 September 2010 meeting, the Group of Governors and Heads of Supervision, the oversight body of the Basel Committee on Banking Supervision, announced a substantial strengthening of existing capital requirements and fully endorsed the agreements it reached on 26 July 2010.

These capital reforms, together with the introduction of a global liquidity standard, deliver on the core of the global financial reform agenda and will be presented to the Seoul G20 Leaders summit in November.

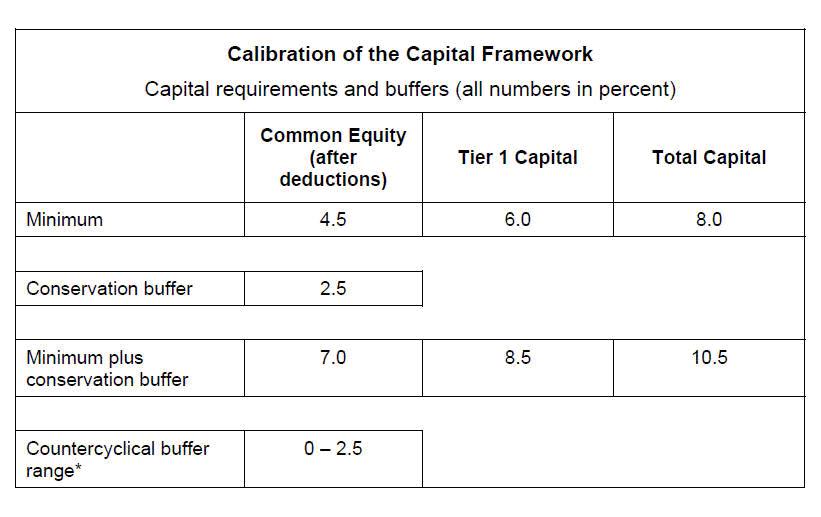

The Committee’s package of reforms will increase the minimum common equity requirement from 2% to 4.5%.

In addition, banks will be required to hold a capital conservation buffer of 2.5% to withstand future periods of stress bringing the total common equity requirements to 7%.

This reinforces the stronger definition of capital agreed by Governors and Heads of Supervision in July and the higher capital requirements for trading, derivative and securitisation activities to be introduced at the end of 2011.

Increased capital requirements

Under the agreements reached, the minimum requirement for common equity, the highest form of loss absorbing capital, will be raised from the current 2% level, before the application of regulatory adjustments, to 4.5% after the application of stricter adjustments.

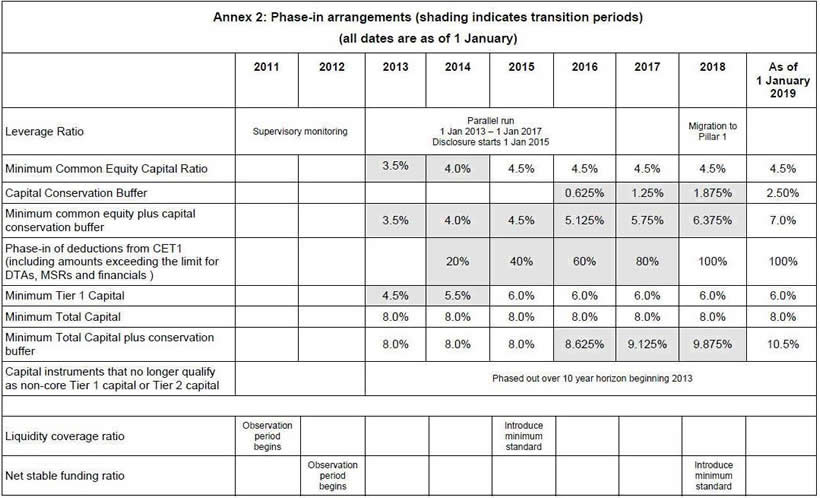

This will be phased in by 1 January 2015.

The Tier 1 capital requirement, which includes common equity and other qualifying financial instruments based on stricter criteria, will increase from 4% to 6% over the same period.

The Group of Governors and Heads of Supervision also agreed that the capital conservation buffer above the regulatory minimum requirement be calibrated at 2.5% and be met with common equity, after the application of deductions.

The purpose of the conservation buffer is to ensure that banks maintain a buffer of capital that can be used to absorb losses during periods of financial and economic stress.

While banks are allowed to draw on the buffer during such periods of stress, the closer their regulatory capital ratios approach the minimum requirement, the greater the constraints on earnings distributions.

This framework will reinforce the objective of sound supervision and bank governance and address the collective action problem that has prevented some banks from curtailing distributions such as discretionary bonuses and high dividends, even in the face of deteriorating capital positions.

A countercyclical buffer within a range of 0% - 2.5% of common equity or other fully loss absorbing capital will be implemented according to national circumstances.

The purpose of the countercyclical buffer is to achieve the broader macroprudential goal of protecting the banking sector from periods of excess aggregate credit growth.

For any given country, this buffer will only be in effect when there is excess credit growth that is resulting in a system wide build up of risk.

The countercyclical buffer, when in effect, would be introduced as an extension of the conservation buffer range.

These capital requirements are supplemented by a non-risk-based leverage ratio that will serve as a backstop to the risk-based measures described above.

In July, Governors and Heads of Supervision agreed to test a minimum Tier 1 leverage ratio of 3% during the parallel run period.

Based on the results of the parallel run period, any final adjustments would be carried out in the first half of 2017 with a view to migrating to a Pillar 1 treatment on 1 January 2018 based on appropriate review and calibration.

Systemically important banks should have loss absorbing capacity beyond the standards announced today and work continues on this issue in the Financial Stability Board and relevant Basel Committee work streams. [1]

THE LOOPHOLE & ADMISSION OF INSOLVENCY

Since the onset of the crisis, banks have already undertaken substantial efforts to raise their capital levels.

However, preliminary results of the Committee’s comprehensive quantitative impact study show that as of the end of 2009, large banks will need, in the aggregate, a significant amount of additional capital to meet these new requirements.

Smaller banks, which are particularly important for lending to the SME sector, for the most part already meet these higher standards.

The Governors and Heads of Supervision also agreed on transitional arrangements for implementing the new standards.

These will help ensure that the banking sector can meet the higher capital standards through reasonable earnings retention and capital raising, while still supporting lending to the economy.

THE IRON CLAD CONFIRMATION THAT BANKS ARE IN DEEP SHITS

Please read all the passages which I have highlighted in bold in the above paragraphs. If the banks were at all material times adequately capitalised and the central bankers in collusion with these banksters and fraudsters were prevented from manipulations, there would not be any need for Basel III regulations.

In saying this, I am not in anyway conceding that even with these new requirements, the banks will be adequately capitalised.

The simple truth is that as long as the derivative casino is still running and banks are allowed to continue their off balance sheet activities, nothing will be resolved.

The 2 tables below tell the whole story:

Source: Basel iii Compliance Professionals Association (B iii CPA)

How can the ultimate capital requirement of 8 percent be adequate when leverage under Basel III is still allowed at the astronomical rate of 33:1?

In the second table, and it is a no brainer to conclude that the banking crisis (if we are lucky) may be “resolved” by 2015 but it is most likely that it can be only resolved by 2017/2018 .

This is an express admission that all banks would require such a long transition period to comply with the new requirements!

The stark reality is that the Too Big To Fail Banks do not have the ability and or the means to raise capital at this critical juncture.

To use an analogy, the banking patient will be in Intensive Care until 2017, which is rather optimistic for the projection implies that the patient may be able to recover.

It is my view that Basel III is pure spin and is intended to convey the impression that the central bankers and regulators have things under control. This is a big lie!

I have said in my earlier article that the FED through QEI purchased toxic assets from the banks and part of the monies were used to shore up the reserves and part to purchase treasuries (to give an illusion of better quality assets in banks’ balance sheet).

There are so much more, $trillions more of toxic waste that no amount of QE (quantitative easing) can remove them. This situation does not even take into consideration the toxic waste in SPVs – the off balance sheet mumbo jumbos. The FED and Accounting Bodies have suspended accounting and regulatory rules that have enabled the banks to hide such toxic waste in SPVs and not having to account for them in the banks’ balance sheet.

LIFE SUPPORT

QEI has merely enable the Too Big To Fail Banks to continue some form of banking activities thus deceiving the public that they are solvent and prevent a bank run.

But the central bankers cannot have the cake and eat it as well. In trying to shore up public confidence in banks with the introduction of Basel III, they have inadvertently let the cat out of the bag and as the above two tables show, the banks are all insolvent.

Additionally, whatever reserves that have been accumulated are insufficient to stimulate further lending, because the banks have reached their limits under the fractional reserve system. This is the reason for the contraction of credit and not as one commentator has postulated that Basel III would “contract credit”.

Two burdens are weighing down on the banks:

1) inadequate capital to meet liabilities (borrowings); and

2) inadequate reserves under fractional reserve banking.

This is a big mess!

THE CONFIDENCE GAME

At this moment, I cannot give a precise time-line as to how long the FED and the global central banks can prolong the confidence game, hoodwinking the public and sovereign creditors that all is well.

When confidence in banks evaporates for whatever reasons, the consequences will be ugly and there will be massive social upheavals across the globe.

The first indication that the game is up is when US treasuries are increasingly purchased by the FED to make up for the shortfalls by foreign creditors and to finance the ballooning US deficits.

All of a sudden, some entities may start to get real nervous and unload the treasuries, and the FED steps in to shore up treasuries. Then, the tipping point is reached and Hell breaks loose!

China is also part of this confidence game.

But, contrary to IMF and other renowned economists who are betting on China’s and Asia’s so-called economic strengths, I take the view that when US treasuries collapse, faith in all fiat monies will likewise evaporate and there will be massive capital flight to commodities, especially gold, silver and oil.

Asian stock markets will be devastated and there will be volatile gyrations in currency values.

Therefore, it is utter lunacy and recklessness for the Malaysian central bank (Bank Negara) and the government to even consider allowing the ringgit to be traded.

When confidence in dollar assets vaporises, China will be caught right in the middle. The third and final phase of the Global Financial Tsunami will devastate Asian economies and with it, the greatest depression in history will ensue.

Time Line?

Between now and anytime in 2011.

At the latest, 2012.

God help us.

Matthias Chang is a frequent contributor to Global Research. Global Research Articles by Matthias Chang

© Copyright Matthias Chang , Global Research, 2010

Disclaimer: The views expressed in this article are the sole responsibility of the author and do not necessarily reflect those of the Centre for Research on Globalization. The contents of this article are of sole responsibility of the author(s). The Centre for Research on Globalization will not be responsible or liable for any inaccurate or incorrect statements contained in this article.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.