How the Fed Could Become Insolvent

Interest-Rates / Central Banks Jan 05, 2011 - 02:00 AM GMTBy: Casey_Research

Terry Coxon, Editor, The Casey Report writes: You've seen the proof in real time. Once-dominant industrial companies, e.g., General Motors, can run out of money. The biggest banks, e.g., Bank of America, can run out of money. Even sovereign governments, e.g., Greece, can run out of money. Yes, all those organizations are still limping along, but only after being rescued by other giant institutions, such as the U.S. government, the less unhealthy European governments, the European Central Bank, and the International Monetary Fund.

Terry Coxon, Editor, The Casey Report writes: You've seen the proof in real time. Once-dominant industrial companies, e.g., General Motors, can run out of money. The biggest banks, e.g., Bank of America, can run out of money. Even sovereign governments, e.g., Greece, can run out of money. Yes, all those organizations are still limping along, but only after being rescued by other giant institutions, such as the U.S. government, the less unhealthy European governments, the European Central Bank, and the International Monetary Fund.

So far, it's been easy to get rescued. The people who run giant institutions seem to shudder at the thought of other giant institutions being shown up as anything less than indestructible. Of course, the rescues weaken the rescuers and push them toward the day when they, too, may join the ranks of the desperate.

By now it's clear that neither big, Bigger, nor BIGGEST implies unlimited resources. But how about central banks? In a world of fiat money, a central bank can always print more of its own currency. So unless it takes on debt or other obligations denominated in something other than its own currency, it's impossible for a central bank to become formally insolvent. Nonetheless, it can become functionally insolvent, void of any ability to command resources or influence markets. That's what happened in Zimbabwe, with a hyperinflation.

As of today, we're nowhere near such a catastrophe. But there is another way, long before hyperinflation destroys its currency, for a central bank to become functionally insolvent. It's a trap into which our own Federal Reserve System has already stuck its foot and now seems to be getting ready to stick its neck.

The Federal Reserve has come a long way since it was conjured by Congress in 1913. From the beginning, it was authorized to issue Federal Reserve notes with the status of legal tender and to issue demand deposits, redeemable in Federal Reserve notes or other "lawful money," to member banks. But there were constraints. Among them was a requirement for the Federal Reserve to hold a gold reserve equal to 35% of the deposits it owed to member banks plus 40% of the total Federal Reserve notes outstanding. In addition, being legal tender, Federal Reserve notes were redeemable in gold. Those restraining factors didn't last.

The 1933 prohibition on gold ownership by U.S. citizens weakened the constraint of gold redeemability, but not by much, since foreigners (whom governments normally treat better than their own citizens) could still redeem dollars for gold. Next, in 1944, in conjunction with the Bretton Woods agreement, the gold reserve requirements were lowered to 25%. In the late 1960s, through a series of steps, the requirements for a gold reserve were eliminated altogether. Then, in 1971, the U.S. government told all foreigners, "If you haven't redeemed your dollars for gold already, it's too late, ha-ha-ha." The era of Central Bankers Gone Wild had arrived.

The Federal Reserve was not long in using its new license. In the 37 years that followed the abandonment of the last tie to gold, successive waves of printing reduced the dollar's purchasing power by 81%. That was mischief enough, but nothing like the danger the Fed embraced in the fall of 2008. Determined to rescue the country's largest banks from their subprime lending and derivative investing blunders, the Federal Reserve in effect swapped more than $1 trillion in newly created cash for the low-quality loans and debt securities that commercial banks wanted badly to be rid of.

For the banks, the swap was like waking up on Christmas morning and finding that Santa had taken out the trash and left a big sack of money in its place. But the exchange gave the Fed a new problem - how to keep all the new cash that banks were sitting on from fueling a doubling in the public's money supply (M1) and the unprecedented rates of price inflation that such a doubling would cause. The solution was to give commercial banks an incentive to keep sitting on the excess reserves rather than lending or investing them. The incentive the Fed offered was to pay interest on the reserve that commercial banks keep on deposit at Federal Reserve banks, so that the money would stay there.

The Federal Reserve is now paying interest on nearly $1 trillion in deposited reserves. The interest rate is only 0.25% per year, but with open market interest rates so low, it's more than banks can earn elsewhere, so it's enough to keep the excess reserves sequestered. And at that low interest rate, the expense is easy for the Fed to manage, only about $2.5 billion per year.

But what happens when interest rates start rising from today's abnormally and artificially low levels? To prevent an explosion, roughly a doubling, in the M1 money supply, the Fed will need to raise the rate it pays banks on their deposits, so the Fed's interest expense will start growing.

Could it grow into a problem?

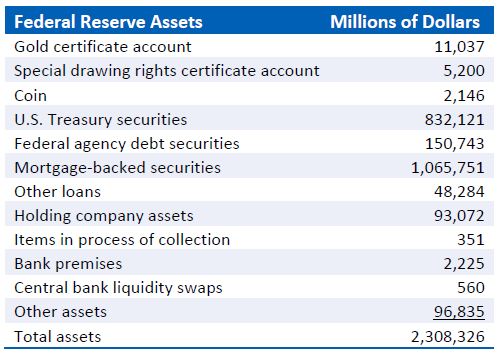

Below is a summary of the asset side of the Federal Reserve's balance sheet. Those are the assets that generate income for the Fed, income that currently runs about $65 billion per year. Most of the income-earning assets - chiefly the Treasury securities, agency securities, and mortgage-backed securities - have long maturities (short-term T-bills make up only a small portion of the total).

Given the composition of the Fed's assets, when interest rates start rising, the immediate effect on the Fed's income will be negligible. But the Fed's interest expense will respond immediately, because the interest it is paying is interest on deposits that commercial banks are free to withdraw without notice. That's not a healthy combination. Short-term rates would only need to rise above 6.5% for the cost of keeping the $1 trillion sequestered to exceed all of the Fed's income. The Federal Reserve would be operating at a loss.

A rate of 6.5% is higher than the historical average for short-term rates, but it's not extraordinary. The fed funds rate was higher than that for most of the 20 years from 1969 to 1989. (It peaked at 19% in 1981.) And it will move back up to the 6.5% neighborhood when, as I expect, the rate of price inflation picks up substantially.

And the crossover rate, at which the Federal Reserve starts losing money, may be about to come down. The Fed is about to begin round 2 of "quantitative easing," in which it creates still more reserves to buy still more long-term Treasury bonds. Suppose that QE2, regardless of what details are initially announced, adds up to a purchase of another $1 trillion of 30-year T-bonds, at the current yield of 3.9%. That will add $39 billion per year to the Fed's income. But it will double the effect that any rise in short-term rates has on the Fed's interest expense. The net effect would be to lower the crossover fed funds rate, at which the Federal Reserve starts operating at a loss, to 5.3%.

When the Fed does start operating at a loss, it won't be broke, but its hands will be tied. It won't have the latitude to influence markets that it had just a few years ago. Its choices for covering its operating loss will be:

- Sell assets to cover the loss. It has plenty of assets to sell, but selling them would put upward pressure on interest rates.

- Print the money to cover the loss but continue to pay interest at a sufficiently high rate to keep the new reserves sequestered. That, of course, would add to the rate at which the Fed would be losing money.

- Print the money to cover the loss and simply let the new reserves have their inflationary effect. But that, too, would add to future operating losses, since higher inflation means higher interest rates, which means higher interest expense for the Fed.

If short-term rates bob up to the 5% to 7% neighborhood and stay there, all this will happen in slow motion. Mr. Bernanke and company can still hope to find a way out. But the higher rates go, the less real hope there will be. Even without QE2, if the fed funds rate returns to its historic peak of 19% (price inflation running at a similar rate would get it there), the Federal Reserve will be losing $125 billion per year. In that case, things would move rapidly. Then we would find out what happens when the last lifeguard has swum out so far that he hasn't the strength to get back to shore.

[Every month, the editors of The Casey Report analyze big-picture trends to find the best crisis investment opportunities for subscribers. And one of their current favorites is betting on rising interest rates – a no-brainer for savvy investors. Read more here.]

© 2010 Copyright Casey Research - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.