A No-win Situation for the Fed

Interest-Rates / Central Banks Mar 02, 2011 - 07:27 AM GMTBy: Clif_Droke

A situation is developing the global markets which threatens to undo the recovery of the past two years. The price spikes in fuel and especially agriculture prices is the Achilles’ heel of the recovery and may well serve as its death knell before the year is through.

A situation is developing the global markets which threatens to undo the recovery of the past two years. The price spikes in fuel and especially agriculture prices is the Achilles’ heel of the recovery and may well serve as its death knell before the year is through.

The surge in commodity prices since last summer is garnering headline attention as fears of a surge in consumer price inflation increase. Agricultural prices have jumped in recent months and grocery store prices are forecast to increase across the board by summer. Developing countries have born the brunt of the commodities surge, with the poorest countries paying an estimated 20 percent more for food in 2010 than in 2009. Wheat prices at the Chicago Board of Trade are up by more than 75 percent in the past year; corn prices have gained almost 90 percent.

The central banks of both China and the U.S. have taken a big share of blame for the global food price inflation. Many experts have accused the U.S. Federal Reserve of stimulating an inflationary outbreak by embarking on its $600 billion Treasury security purchase plan. China’s own $586 billion stimulus plan has had arguably a greater impact on food price inflation in that country considering that China’s economy is only a third the size of the U.S. economy. The Fed’s quantitative easing initiative, which is expected to continue until June, clearly has had a benign impact on equity prices and arguably has helped corporations shore up their balance sheets and raise cash levels to their current highs. It has, however, had a rather malignant spillover effect in another area of the financial market.

One spillover effect of the Fed’s Treasury purchasing program can be seen in the huge amounts of money that have been funneled into commodities. Oil and agricultural commodity prices in particular have been beneficiaries of the Fed’s QE campaign. This has increased prices for a broad array of consumer goods as well as boosting transportation costs.

The biggest victims of the concerted central bank stimulus campaigns have been the poor in the emerging nations. Rising food prices in the Middle East region have already led to a revolution and one dictator has already toppled as a result. Moreover, global food prices have pushed 44 million people into extreme poverty, according to the World Bank.

The turbulence in the Middle East is making matters worse by spiking the oil price even more. The Kress 120-year “revolutionary cycle” is in its final descending phase and this is why we can expect to see more revolutionary activity between now and 2014. The strong deflationary undercurrents that accompany this cycle are responsible for creating the economic chaos which is the dominant factor behind political revolt and popular uprisings. With the Middle East a revolutionary powder keg, the oil price has never been more vulnerable to factors other than those of the financial market.

Fed chief Bernanke has the unenviable task of balancing a domestic economy plagued by low consumer demand against his loose money policy. In the first two years following the credit crisis, Bernanke’s loose monetary policy served him well. Commodity prices were depressed along with equity prices and this gave the Fed plenty of room to re-inflate with worrying about immediate-term consequences. Two years of steadily rising commodity prices have eroded the Fed’s cushion, however, and the end game is surely in sight. Any additional commodity rice increases will threaten the global market recovery and will exert profound pressure against the Asian and emerging market economies. It won’t do any favors for the still weak U.S. economy, either.

Mr. Bernanke has expressed his determination to continue the second quantitative easing (QE2) campaign, which commenced in November 2010, until June this year. This means at least three more months of potential spillover into the commodity price uptrend. Hedge funds are taking full advantage of this copious increase in liquidity and what we’re seeing here is essentially Act 2 of the drama that unfolded in the months before the credit crash in 2008. At that time, a fund-driven rally in the oil price put tremendous pressure on the already weakened financial market and added fuel to the credit fire. The oil market eventually succumbed to that raging inferno, but not before causing tremendous economic damage.

The situation that appears to be repeating here is the same theme we saw in the months leading up to the credit crisis. Oil and gas stocks accounted for much of the stock market’s gains during 2007 and although the market did effectively ignore the rising crude oil price for a while, the relentless rally in oil eventually turned out to be the proverbial straw that broke the camel’s back.

Chairman Bernanke’s conundrum is truly of the catch-22 variety: either he’ll be forced to ease off the monetary accelerator to prevent prices from rising too much, in which case the forces of long wave deflation (i.e. the long-term Kress cycles) will push hard against the financial system and eventually create another systemic crisis. Or if he decides to keep pumping the increase in commodity prices (particularly oil) will put all kinds of pressure on the still fragile economic recovery. Under this scenario, there would most likely be a sharp spike in retail prices across the board, particularly for gasoline. This in turn would be followed by a deflationary crash.

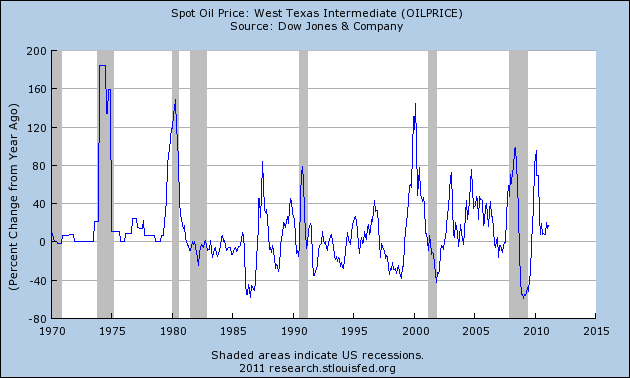

You may wonder how a fuel price spike would create deflation? The reason is that higher oil prices eventually result in reduced consumer spending, which in turn puts downward pressure on prices, i.e. deflation. Another point worth mentioning is that in the last 40 years, with the exception of 1986, year-over-year rises in oil prices of 80% or more have always been followed by recession (see chart below). So no matter which way Mr. Bernanke turns, he is confronted with the specter of deflation.

Deflation likely won’t be a concern until later this year or early next year, particularly after the 6-year cycle peaks in October. For now we’ll continue to look for opportunities on the relative strength and momentum front among individual mining stocks and ETFs. But we need to be aware that the days of easy profits and extremely low volatility are likely over. For the rest of 2011 investors would do well to assume a market environment similar to that of 2007, which had its ups and downs but was characterized by increasing turbulence as the year progressed.

Until lately, the gold price hadn’t benefited from the Fed’s second QE campaign quite as much as oil and agricultural prices. It has nonetheless managed to catch up to the oil price recently. There are two components behind the gold price uptrend that are especially significant from an interim standpoint, namely the fear component and the currency component. Fear has been a major factor behind gold’s surge in recent years, particularly following the credit crisis. A weak dollar has also helped fuel the gold bull market, and to that end the Fed’s loose money policy has benefited gold in a residual fashion.

Yet the Fed’s easing program has also hindered gold’s progress since last November. The easy money fueled a surge higher in stock prices, which resulted in a diminution of investors’ fears. This in turn led to a temporarily diminished demand for gold investments. With market volatility on the rise once again in response to Middle East troubles, fear is returning to the market and will help gold gain additional traction.

Cycles: Over the years I've been asked by many readers what I consider to be the best books on stock market cycles that I can recommend. While there are many excellent works out there on the subject of technical and fundamental analysis, chart reading, etc., precious few have addressed the subject of market cycles. Of the relatively few books on cycles that are available, most don't even merit mentioning. I've read only one book in the genre that I can recommend - The K Wave by David Knox Barker - but even that one doesn't deal directly with stock market cycles but instead with the economic long wave. I'm pleased to announce, however, that after nearly 10 years of research and one year of writing, I've completed a book on the subject that I believe will meet the critical demands of most cycle students. It's entitled, The Stock Market Cycles, and is available for sale at http://clifdroke.com/books/Stock_Market.html

By Clif Droke

www.clifdroke.com

Clif Droke is the editor of the daily Gold & Silver Stock Report. Published daily since 2002, the report provides forecasts and analysis of the leading gold, silver, uranium and energy stocks from a short-term technical standpoint. He is also the author of numerous books, including 'How to Read Chart Patterns for Greater Profits.' For more information visit www.clifdroke.com

Clif Droke Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.