Why Getting Valuation Right Is So Important To Retired Dividend Growth Investors

Companies / Pensions & Retirement Dec 10, 2015 - 10:32 AM GMT

Although getting valuation right before you buy a stock is critically important to the long-term oriented retired dividend growth investor, it is not a short-term market timing concept. My point is that short-term market movements are typically volatile and unpredictable. The reason is simple. Over short periods of time, which I define as less than a business cycle (3- 5 years), emotion has a major effect on stock prices.

Although getting valuation right before you buy a stock is critically important to the long-term oriented retired dividend growth investor, it is not a short-term market timing concept. My point is that short-term market movements are typically volatile and unpredictable. The reason is simple. Over short periods of time, which I define as less than a business cycle (3- 5 years), emotion has a major effect on stock prices.

When dealing with common stock investments, the primary emotions that interfere with reason are fear and greed. However, there are also subtle nuances associated with these primary emotional responses. For example, if a stock is running to the upside, investors might feel they are missing out and invest regardless of valuation. Although this is related to greed, it is a milder form. Conversely, if a stock is falling precipitously, panic often sets in motivating investors to sell regardless of fundamental strengths. Panic is related to fear, but it is an extreme form.

This speaks to the reality that between the two primary emotional responses (fear and greed) that investors face, fear is both the most influential and the most dangerous. In my experience, more money has been lost through panic selling than through overpaying. This is especially true when investing in high-quality dividend growth stocks with consistent records of above-average earnings growth. Again, the reason is simple.

When the emotional response kicks in, logic and reason is often disregarded and people can mistakenly buy when they should be selling and/or sell when they should be buying. Sometimes this works out okay in the short run, but in the long run it usually ends up creating poor, and in some cases, disastrous results. If you overpay for a growing business, you face the prospect of earning less than the company’s earnings growth would produce if you were more prudent. However, if the business is truly growing, you might still make money even though it is most likely less than you should have made.

In contrast, if you sell a valuable business for less than it is worth based on fundamental strengths, you turn an unrealized and usually temporary loss into a true, permanent and realized loss. This is just one reason why fear is a more dangerous emotional response than greed.

Valuation - What It Is and How It Works

Fair valuation is a metric that astute fundamental investors focus on to ensure that they are making a prudent investment decision when considering a stock to purchase. However, it is not a metric that is driven by short-term stock price movements. In other words, valuation is not concerned with price momentum in either direction up or down. At its core, valuation relates to a company’s past, present and potential future earnings power in relation to the price you are being asked to pay to buy it.

In this context, fair valuation relates to the earnings yield that an investment in a stock offers based on its current price in relation to the company’s earnings and/or cash flows. A common valuation measurement that many investors rely on is the P/E ratio. However, the P/E ratio metric simply serves as a quick guide for determining earnings yield. Earnings yield can be calculated simply by inverting the P/E ratio to an E/P ratio (earnings divided by price).

When investing in common stocks, astute fundamental investors require an earnings yield of at least 6.5% to 7% or better. Of course, the higher the earnings yield you can purchase a stock for, the better. Importantly, this number is not simply pulled out of a hat. Instead, it relates to the average return that stocks have generated for investors over the long run. A shortcut formula for determining earnings yield is to simply divide the number 1 by a company’s current P/E ratio.

A few simple examples will clarify how this works. A P/E ratio of 15 (the historical norm for the S&P 500) calculates to an earnings yield of 6.67% (1÷15 = 6 .67%). In contrast, a P/E ratio of 20 calculates to an earnings yield of 5% (1÷20 equal 5%), which would be below the 6.5% to 7% required minimum threshold. A high P/E ratio of 30 only calculates to an earnings yield of 3.33% (1÷30 = 3 .33%), which is obviously half of the earnings yield represented by a P/E ratio of 15.

In the real world also known as the stock market, it is not uncommon to see stocks grab momentum and move from fairly valued P/E ratios in the 15 range, to valuations of 20 or 30 times earnings for a short period of time. There are many high-quality dividend growth stocks that are currently trading at such heights with no material improvements in fundamentals to justify their valuations. However, when valuations are not supported by fundamentals, investors are exposed to the potential fickle results that can occur when popularity wanes.

In stock market parlance, valuations not supported by fundamentals are referred to as hot potato stocks. As an investor, you can do well by investing in a hot potato stock as long as you pass the potato on to the next person while it is still hot. You don’t want to be the person getting the hot potato just before it cools off. The problem is that momentum is fragile because investor sentiment can change in a heartbeat. On the other hand, strong fundamentals are substantial because this is where the true value of a business is found.

To summarize the essence of valuation, when you overpay for even a great stock, you are taking more risk than prudence would dictate. Consequently, in reality you are exposing yourself to returns that are lower than the strength of the business would offer at more prudent valuations. In contrast, when you are given the opportunity to purchase a fundamentally strong business below sound valuation, you are simultaneously taking on less risk while generating the potential for returns higher than the growth of the business would offer.

This higher return manifests as the P/E ratio increases to fair valuation levels which serves as natural leverage. To clarify, you originally buy earnings at a lower P/E ratio, then future earnings grow to higher levels and therefore those higher earnings are capitalized at a higher multiple. I call this natural leverage.

Digital Realty Trust Inc: Quintessential Lessons on Valuation

On June 30, 2013 fellow Seeking Alpha author and friend Brad Thomas penned an article on Digital Realty Trust Inc. found here at a time during which its stock price had fallen approximately 22% from highs established one year earlier (July, 2012). Brad’s positive article on Digital Realty (DLR) was mostly met with skepticism and some support. You can read the comment section of the article to validate my previous statement.

However, the primary point I am offering is that Digital Realty was an unpopular stock and there were even hedge funds recommending shorting it. In the short run, some of the negativity was validated as Digital Realty’s stock price dropped another 22% over the next 5 months (November 29, 2013). But most importantly, Digital Realty was in truth undervalued when Brad Thomas originally wrote the article. Thus, it was a sound and attractive investment longer-term, even though it was unpopular in the short run.

I bring this up for a couple of reasons. First of all, Brad’s article stroked my ego because he led his article off with a story that I had previously shared with him. Yes, I am human, and I do have an ego, but I try to keep it under control as best I can. Additionally, I responded with a comment of my own on Brad’s article that is germane to the subject of my article here as follows:

“IMHO, there are a couple of points that are being overlooked in these discussions. First of all, in spite of DLR's recent price swoon, their long term performance as a publically traded REIT is stellar and has soundly outperformed the S&P 500 as follows:

A $10,000 investment on 10/29/2004 is currently (Through yesterday’s close) worth $47,776.48 vs only $14,915.17 for the S&P 500. That’s a 19.6% annual rate of capital appreciation vs only 4.7% for the S&P 500.

DLR’s total cumulative dividends during that time were $12,775.76 versus only $1,578.86 for the S&P 500. This brings their total return plus dividends to 22.8% vs 5.9% for the S&P 500. Moreover, their dividend growth rate has averaged 18.7% per annum. All of this is in spite of the recent price drop.

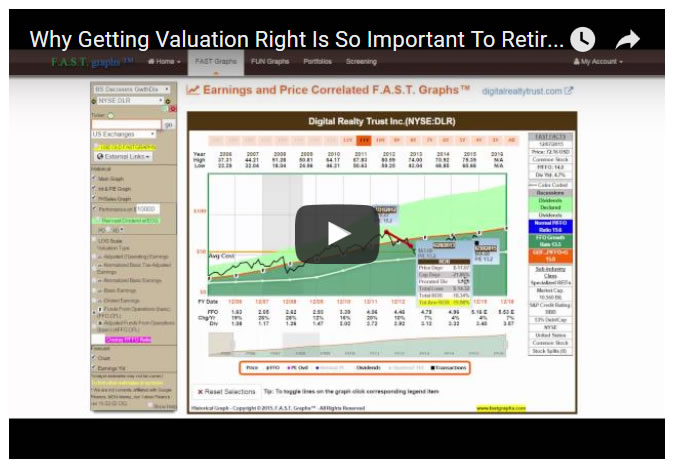

Point number two, a close look at the price and FFO correlated FAST Graph in the article clearly illustrates the price has fallen below the orange and blue valuation lines on several occasions in the past, with each representing an incredible buying opportunity.

Whether it was Graham, J.P. Morgan or both, the point that stock price fluctuates is a given for all stocks. IMHO, and vast experience when price falls but fundamentals remain intact, a bargain is created. If fundamentals and price both fall, there is a big problem. DLR's quarter was very strong, and from what I saw only the announced accounting change was a concern.

Additionally, if there is nothing systemically wrong with DLR's business potential, then time will show DLR to be a great bargain at today's levels as it was every time it occurred in the past. If fundamentals deteriorate, then long term investors will be in trouble. A comprehensive research analysis may shed light on which, and time will tell.

Finally, DLR's strong performance depicted above is consistent with their superb operating record (consistent FFO growth and dividend increases). Again, this quarter was more of the same. Be greedy when others are fearful and fearful when others are greedy. A wise and successful investor advised that, and he also said that if you do not intend to own a stock for at least 10 years, you should not consider owning it for even10 minutes.

My view on the matter,

Chuck”

Bonus: A Short Video Elaborating on Valuation via Digital Realty Trust

If a picture is worth 1000 words, then a short video must be worth many more. Therefore, I offer the following video looking at Digital Reality through the lens of the F.A.S.T. Graphs™ fundamentals analyzer software tool. I chose this example because this REIT has shown several periods where stock price has moved from fair valuation to overvaluation to undervaluation several times. Consequently, I believe the valuation story can be more elegantly presented than it could be with mere pictures and lots of words. I hope you find it illuminating.

Bonus: A Live Fully Functioning F.A.S.T. Graphs™ on DLR

I believe that one of the best ways to learn about something, or how to do it, is by doing it. Therefore, I offer a live fully functioning historical F.A.S.T. Graphs™ on Digital Realty so that you can run through various valuation exercises yourselves, just like I did in the above video. Simply point your mouse on the black price line and a pop-up will appear with the date, price and P/E ratio. Click that spot and then move your mouse to any other future point on the black price line and again the pop-up will appear. Click on that second spot and a comprehensive performance will appear from point A to point B. To erase the calculation, simply click on the second plot and you will be ready to run as many other calculations as you desire.

The purpose of conducting these exercises is to help you understand the effects that both overvaluation and undervaluation has on future performance. Additionally, as you conduct these exercises also pay attention to the orange valuation reference line and the honeydew green dividend line. Notice how more consistent operating results are in comparison to price volatility. As an additional side, you can remove the price line by simply clicking on the word “price” found in the long orange rectangle at the bottom of the graph. This allows you to focus on operating results without your judgment being contaminated by price action. (NOTE: To mirror what I presented in the video, shorten the timeframe to 11 years to screen out the anomalous growth of FFO in the first year.)

Summary and Conclusions

When buying stocks, exercising the discipline to only invest when fair valuation is manifest will significantly improve long-term total returns. Not only will you position yourself for greater capital appreciation, which at current and future yield will also be stronger-in the long run. Of course, this also mitigates a great deal of the risk normally associated with investing in equities.

On the other hand, valuation is not always a perfect short-term market timing tool. Since short-term volatility is greatly influenced by motion, an out-of-favor stock can continue to fall for a period of time, and conversely, a highly popular stock can continue to rise for a period of time. Therefore, astute value investors aware of this possibility are prepared for the possibility of poor short-term performance. However, they invest confidently because they understand that the fundamental strength of a business is more enduring than short-term emotionally- driven price volatility. True value investors trust strong operating results (earnings, dividends, etc.) more than they trust price action.

Disclosure: Long DLR.

By Chuck Carnevale

Charles (Chuck) C. Carnevale is the creator of F.A.S.T. Graphs™. Chuck is also co-founder of an investment management firm. He has been working in the securities industry since 1970: he has been a partner with a private NYSE member firm, the President of a NASD firm, Vice President and Regional Marketing Director for a major AMEX listed company, and an Associate Vice President and Investment Consulting Services Coordinator for a major NYSE member firm. Prior to forming his own investment firm, he was a partner in a 30-year-old established registered investment advisory in Tampa, Florida. Chuck holds a Bachelor of Science in Economics and Finance from the University of Tampa. Chuck is a sought-after public speaker who is very passionate about spreading the critical message of prudence in money management. Chuck is a Veteran of the Vietnam War and was awarded both the Bronze Star and the Vietnam Honor Medal.

© 2015 Copyright Charles (Chuck) C. Carnevale - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Chuck Carnevale Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.