Fundemental Change as Global Economy Heads For Recession

Economics / Recession 2008 - 2010 Aug 15, 2008 - 02:01 AM GMTBy: Mike_Shedlock

The global economy is slowing rapidly. Let's take a look at some striking examples.

The global economy is slowing rapidly. Let's take a look at some striking examples.

Germany, France, Spain, Italy

Bloomberg is reporting German, French Economies Shrink as Spending, Investment Falter .

- Germany and France, the euro area's two largest economies, contracted in the second quarter as faltering sales undermined investment by companies and soaring costs eroded consumer spending power.

- German gross domestic product fell a seasonally adjusted 0.5 percent from the first quarter.

- French GDP declined 0.3 percent, reversing a 0.4 percent gain in the previous three-month period.

- Spain's economy grew at the slowest pace since a 1993 recession in the second quarter as the country's once-booming construction industry slumped.

- Italy's economy, the third-biggest in the euro region, unexpectedly shrank in the April-June period, edging closer to a fourth recession in a decade.

- An index measuring the economic climate in the euro region dropped to the lowest since 1993, the Munich-based Ifo institute said yesterday. Measures of both current conditions and expectations declined, according to institute's quarterly World Economic Survey.

A recession looms in Japan as the Japanese Economy Shrinks 2.4% .

- Japan's economy contracted last quarter, bringing the country to the brink of its first recession in six years, as exports fell and consumers spent less.

- Gross domestic product shrank an annualized 2.4 percent in the three months ended June 30 after expanding 3.2 percent in the first quarter, the Cabinet Office said today in Tokyo. The Nikkei 225 Stock Average fell the most in a month.

- Exports fell the most since the 2001-2002 recession, robbing Japan of the engine that drove its longest postwar expansion, while record fuel and food prices deterred spending at home.

In Australia, the Reserve Bank is "shocked" by the severity of the slowdown .

- The RBA predicts that Australia's annual rate of jobs growth, at present 2.3%, will slow to three-quarters of 1% almost straight away. The forecast implies a jump in unemployment from 4.3% to 6% by the end of next year.

- Westpac chief economist Bill Evans said the Reserve Bank seemed to be "shocked" by the severity of the slowdown that it had helped engineer.

- Associate Professor Steve Keen from the University of Western Sydney says Brace yourselves for recession in this interview with Phillip Lasker.

In an unexpected move New Zealand cuts rates on fears of drawn-out recession .

- Alan Bollard, governor of the Reserve Bank of New Zealand, cut the rate from 8.25 per cent to 8 per cent - still the highest in the industrialised world after Iceland - despite rising inflation, forecast to peak at 5 per cent by September.

- Economists said the New Zealand authorities were acting aggressively and taking a gamble in looking through the worsening inflation picture and cutting rates to prevent the economy weakening further.

- The move surprised many as it contradicts the Reserve Bank's mandate, which states that achieving and maintaining price stability are the sole objectives of monetary policy. The central bank's stated inflation target band is 1 to 3 per cent.

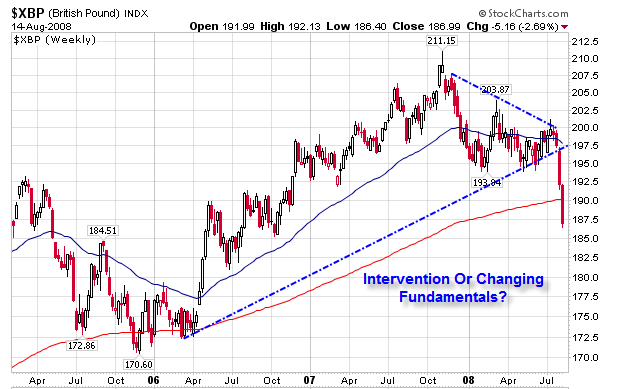

Bloomberg is reporting Pound Near 22-Month Low on Growing Case for Interest-Rate Cut .

- The U.K. pound traded near its lowest level in 22 months against the dollar after the Bank of England cut its economic-growth forecast yesterday, signaling it may reduce interest rates.

- Bank of England Governor Mervyn King said yesterday he saw a "chill in the economic air" after unemployment climbed in July by the most in almost 16 years. The pound has lost 5.8 percent against the dollar in the past 10 days, more than any other major currency except the South African rand and Australian dollar. The pound fell yesterday by the most in nine months.

- "The central bank has effectively opened the door for an interest-rate cut, possibly as soon as next month," Lee Ferridge, a foreign-exchange strategist in London at State Street Global Markets, a unit of the world's largest money manager for institutions, wrote in an e-mailed note to clients today. "Sterling has obviously reacted significantly to this."

Perfectly Obvious

Lee Ferridge, a foreign-exchange strategist in London at State Street Global Markets wrote in an e-mailed note to clients today: " Sterling has obviously reacted significantly to this. "

Indeed it is perfectly obvious why the Sterling has reacted to the news. It is equally perfectly obvious why the Euro has reacted. And it is perfectly obvious why the Australian dollar is reacting as well.

Currency Intervention vs. Fundamentals

On Monday, a post of mine, Currency Intervention And Other Conspiracies , stirred up a ruckus from those who see manipulation as the reason for the rise in the dollar. One person accused me of "yellow journalism" for not seeing manipulation as the "cause" of this rally.

I have exchanged friendly emails with others, most notably James Turk, a person I highly regard, about the Forex markets.

From James Turk:

I use the term "ignited" the rally. I agree the dollar was oversold, and a rally can occur at any time. But usually a market doesn't rally unless there is some news event or some fundamental change that causes the market to reverse course.

The Fundamental Change

That is a reasonable statement from James Turk, even more so if one changes "But usually a market doesn't rally ..." to something like " But usually a market doesn't have a sustainable rally unless there is some news event or some fundamental change that causes the market to reverse course. "

I believe James would accept that and would also add there can be short term technical rallies at any time without any news, based on market players entering and exiting position at or near support/resistance points.

The key point in this is that often times a " fundamental change " is only obvious in hindsight, with the market reacting in advance. In my opinion, that is what James Turk missed in Mystery Solved when he proposed on August 7th " There has not been any news exceptionally favorable to the dollar. .... So what happened to cause the dollar to rally over the past three weeks? In a word, intervention. "

The fundamental change is now, in my opinion, perfectly obvious: The economies in Germany, France, Spain, Italy, Australia, New Zealand, Japan, and the U.K. are all crumbling much faster than anyone expected.

Furthermore, New Zealand, Australia, and most importantly the EU are all going violate price stability mandates to make the implied rate cuts that are coming! That is an enormous fundamental change given that interest rate differentials, and the expected rate of change of interest rate differentials are two of the biggest factors behinds trends, and reversals thereof, in the Forex markets.

Read that last sentence again, carefully: Rate differentials, and the expected rate of change of interest rate differentials are two of the biggest factors behinds trends, and reversals thereof, in the Forex markets.

Falling oil prices are yet another reason for the dollar to rally given that falling oil prices will help balance of trade.

In a market that trades $1 trillion a day, a onetime intervention of 10 billion Euros is simply not enough to cause a rally, at least beyond a day or two. Japan intervened to the tune of $300 billion over the course of about seven months and all it saw was a sustained move opposite to what Japan was hoping to produce.

British Pound vs. US Dollar

Euro vs. US Dollar

Fundamentals Now Perfectly Clear In Hindsight

Look at the fundamentals again.

The US dollar rallied because it was damn good and ready to rally. Those with their eyes open spotted fundamental reasons in advance. Those who did not, blamed intervention.

The Implications Looking Ahead

It is quite possible that oil prices have peaked, and if so, CPI comparisons year over year are going to be easy looking forward, even if energy prices merely stabilize here. And if energy prices continue to drop, the CPI is going to be falling or even negative, soon enough.

Oil at 150 is yesterday's news. Everyone knows about peak oil and China. But China is slowing and the entire world is headed for recession.

Those focused on the CPI and prices have it wrong for two reasons. The first is the lagging effect as described above, but the far more important reason is the credit markets themselves.

It is credit markets and the global economy that are going to determine where interest rates go. Japan, the UK, EU, Australia, and New Zealand are all on the verge of recession, and slowing at a huge pace. So from my perspective lower yields on treasuries are coming, not just in the US but also in the UK, EU, Australia, Canada, and new Zealand, all on account of that slowing global economy.

This is very dollar supportive on the margin given that many market participants expected the Eurozone and the commodity exporting countries would decouple from the US. That decoupling theory has been blown out of the water and Trichet's change in stance (as opposed to currency intervention), using Turk's word, may have ignited a dollar rally.

However, unbeknown to most, the fundamentals had already changed. That is after all, what caused Trichet to be open towards rate cuts.

With a weakening global economy, default risk is rising everywhere. Unsurprisingly, the cost of raising capital is also rising. One implication is that junk bond yields and yields on preferred stock of even the highest grades are going to soar. And soaring corporate bond spreads are never good for the equity markets in general, at least over the long haul. A second implication is that treasury yields are poised to fall, not only in a flight to safety scenario, but also because the savings rate in the US can be expected to rise, and with that, internal demand for treasuries in the US will rise.

This is of course exactly what one should expect in deflation, with deflation being properly defined as a net contraction in credit and money. Credit, especially credit marked to market (and the latter has a long, long way to go), is contracting rapidly.

Those focused on prices and the rear view mirror of the CPI are simply focused on the wrong things when it comes to treasury yields. The important things to focus on are the deflationary forces of sinking asset prices, the effect that bank writeoffs will have on future bank lending, and the lagging effects of the CPI itself.

The overall implication is that treasury yields are likely to go lower. And when they do, expect to see still more shouts of intervention and manipulation, especially from market participants who do not understand what inflation and deflation really are.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2008 Mike Shedlock, All Rights Reserved

Mike Shedlock Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.