Long-Term Economic Forecast: Slow Growth And Deflation

Economics / Recession 2008 - 2010 Mar 17, 2009 - 04:07 AM GMTBy: John_Mauldin

This week I am really delighted to be able to give you a condensed version of Gary Shilling's latest INSIGHT newsletter for your Outside the Box. Each month I really look forward to getting Gary's latest thoughts on the economy and investing. Last year in his forecast issue he suggested 13 investment ideas, all of which were profitable by the end of the year. It is not unusual for Gary to give us over 75 charts and tables in his monthly letters along with his commentary, which makes his thinking unusually clear and accessible.

This week I am really delighted to be able to give you a condensed version of Gary Shilling's latest INSIGHT newsletter for your Outside the Box. Each month I really look forward to getting Gary's latest thoughts on the economy and investing. Last year in his forecast issue he suggested 13 investment ideas, all of which were profitable by the end of the year. It is not unusual for Gary to give us over 75 charts and tables in his monthly letters along with his commentary, which makes his thinking unusually clear and accessible.

Gary was among the first to point out the problems with the subprime market and predict the housing and credit crises. You can learn more about his letter at http://www.agaryshilling.com. If you want to subscribe (for $275), you can call 888-346-7444. Tell them that you read about it in Outside the Box and you will get not only his recent 2009 forecast issue with the year's investment themes, but an extra issue with his 2010 forecast (of course, that one will not come out for a year. Gary is good but not that good!) I trust you are enjoying your week. And enjoy this week's Outside the Box....

And if you have cable and get Fox Business News, I will be on Happy Hour tomorrow Tuesday the 17th at 5 pm Eastern. Have a great week.

John Mauldin, Editor

Outside the Box

Long-Term Outlook: Slow Growth And Deflation

by Gary Shilling

From 1982 until 2000, the U.S. economy enjoyed rapid growth with real GDP rising at a 3.6% average annual rate. Furthermore, this 18-year expansion, which cumulated to an 89% rise in inflation-adjusted economic activity, was interrupted by only one recession, the relatively mild 1990-1991 downturn, which depressed real GDP by only 1.3% from peak to trough.

Extended Expansion

From a fundamental standpoint, the growth spurt ended in 2000 as shown by basic measures of the economy's health. The stock market, that most fundamental measure of business fitness and sentiment, essentially reached its peak with the dot com blow-off in 2000 and has been trending down ever since (Chart 1). The same is true of employment, goods production and household net worth in relation to disposable (after-tax) income.

Nevertheless, the gigantic policy ease in Washington in response to the stock market collapse and 9/11 gave the illusion that all was well and that the growth trend had resumed. The Fed rapidly cut its target rate from 6.5% to 1% and held it there for 12 months to provide more-than ample monetary stimulus. Meanwhile, federal tax rebates and repeated tax cuts generated oceans of fiscal stimulus.

As a result, the speculative investment climate spawned by the dot com nonsense survived. It simply shifted from stocks to housing (Chart 2), commodities, foreign currencies, emerging market equities and debt, hedge funds and private equity. Investors still believed they deserved double-digit returns each and every year, and if stocks no longer did the job, other investment vehicles would. Thus persisted what we earlier dubbed the Great Disconnect between the real world of goods and services and the speculative world of financial assets.

Not Sustainable

Even before these final speculative binges, the forces driving the economy in its long expansion were unsustainable, as we've been stressing for years in Insight. These forces included the decline in the consumer saving rate and jump in consumer debt, the vast leveraging of the financial sector, increasingly freer trade and loose financial regulation, all of which are now being reversed.

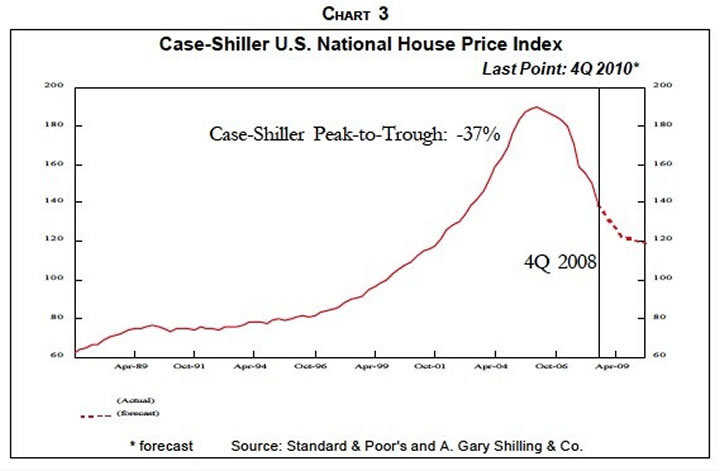

In the 1980s and 1990s, American consumers were more than willing to cut their saving rate because they believed stock portfolios would continue to grow rapidly and take care of all their financial needs. Then, when stocks collapsed in 2000-2002, house appreciation (Chart 3) seamlessly took over to continue the push down the household saving rate from 12% in the early 1980s to zero. Americans saw their houses as continually-filling piggybanks because, they believed, home price appreciation would continue indefinitely. They tapped that equity freely with home equity loans and cash-out refinancing.

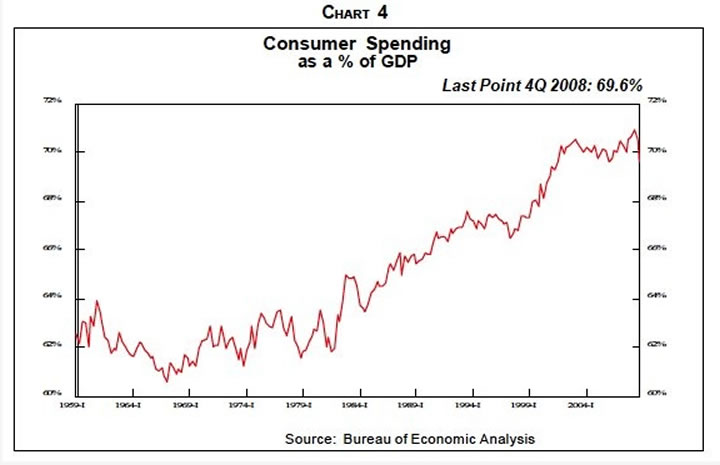

The flip side of saving less is borrowing more, as evidenced by the leap in all consumer debt and debt service, both in relation to disposable (after-tax) income and relative to assets. In relation to GDP, the cumulative outside financing of the household as well as the financial sector leaped for three decades, measuring the immense leveraging in these two areas. Not surprising, amidst this consumer borrowing and spending binge, consumer spending's share of GDP leaped from 62% in the early 1980s to 71% at its peak in the second quarter of 2008 (Chart 4).

The Tide Turns

Now, however, consumers have run out of borrowing power. As of the third quarter 2008, homeowners with mortgages had on average 25% equity in their abodes after all mortgage debt was removed and that number will probably drop to the 10%-15% range with the further decline in house prices we are forecasting (Chart 3). At that bottom, after a 37% peak-to-trough collapse, almost 25 million homeowners, or nearly half the 51 million with mortgages, will be under water, with their mortgages bigger than their house values. In total, the gap will be about $1 trillion.

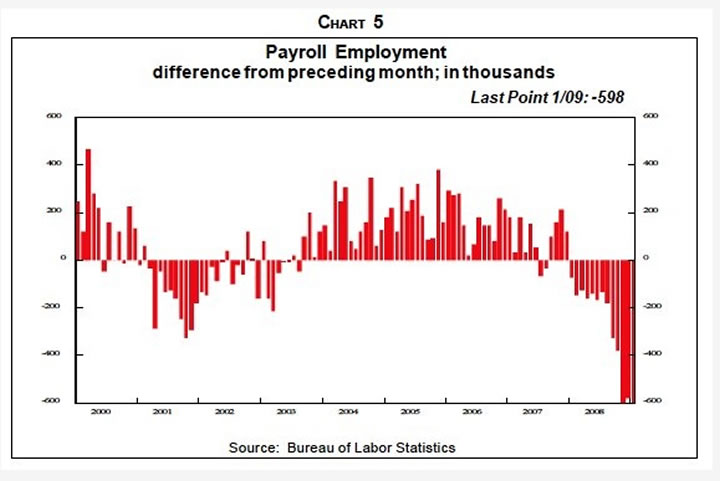

The nosedive in stocks has also discouraged consumer spending as have mounting layoffs (Chart 5), maxed out credit cards and tighter lending standards and weak consumer confidence. Rising medical costs are also a drag on consumers as their co-pays and deductibles mount. For decades, credit card issuers and other lenders encouraged consumers to indulge in instant gratification. Buy now, pay later. But now, habits are changing. Debit cards are becoming popular since they deduct charges directly from the user's checking account and, therefore, don't increase indebtedness. Layaway plans are back in style after nearly disappearing.

Financially Unprepared

Between low saving levels in recent years and weak stock prices, few Americans are prepared financially for retirement. About 54% of 401(k) assets are invested in stocks, which fell 39% last year as measured by the S&P 500 index. And except for Treasurys, almost all other investments suffered huge losses in 2008. Around 50 million Americans have 401(k) plans, with $2.5 trillion in assets, and in the 12 months after the stock market peak in October 2007, over $1 trillion in stock value was wiped out in 401(k)s and other defined contribution plans. Another $1 trillion in IRAs was lost.

After 401(k)s were initiated in 1978, those containing stock assets appreciated in the long 1982-2000 bull market, which convinced many that they didn't need to save, as mentioned earlier. In 1983, 33% of working-age households were financially unprepared for retirement, but the number rose to 40% in 1998 as a result of lower saving and more borrowing, and to 44% in 2006 as the 2000-2002 bear market also depressed retirement funds. Obviously, with the subsequent collapse in house and stock prices, many more -- over 50% -- are unprepared. In 2007, in defined contribution accounts administered by Vanguard, the median account balance for 55-64 year-olds was just $60,740 and only 10% of participants contributed the maximum amount.

Economic Effects

As households increase their saving rate, their spending growth will slow, a distinct contrast from the decline of the saving rate from 12% in the early 1980s to zero recently. That decline, which averaged about a half-percentage point per year, meant that consumer spending grew an average of around a half-percentage point faster than disposable income annually. For the next decade, we're forecasting a one percentage point rise in the saving rate annually. That still would not return it to the early 1980s level of 12% even though the demographics for saving have gone from the worst to the best in the interim. Applying a 1.5 multiplier to account for the total destimulating effects as those dollars are saved, not spent, this means a reduction of about one percentage point in real GDP growth, from 3.6% per annum in the 1982-2000 years to 2.6%.

Although the stock bulls may salivate over the prospect that increased saving will mean more equity purchases, we believe that most of the money will go to debt repayment--the flip side of a saving spree. Note that if the saving rate rises one percentage point per year for 10 years, the cumulative increase in saving will total about $5.5 trillion. That will go a long way in offsetting federal deficits and debt.

So will the deflation that we'll explore later. Incomes may grow on average in real or inflation-adjusted terms, but shrink in current dollars. But debts are denominated in current dollars and therefore will grow in relation to incomes and the ability to service them. This will be the reverse of inflation, which reduced the value of debts in real terms and makes it easier to service them as incomes rise with inflation.

Foreign Effects

The effects, then, of a consumer switch from a 25-year borrowing-and-spending binge to a saving spree will be profound for the U.S. economy. Even more so for the foreign economies that have depended for growth on American consumers to buy the excess goods and services for which they have no other ready markets.

In 2007, U.S. consumers accounted for 18.2% of global GDP, and that share has jumped from 14.9% in 1980 and 16.8% in 1990. Furthermore, the shares of American consumer spending on durable and nondurable goods accounted for by imports from Central and South America and from the Pacific Rim have leaped since the early 1990s.

A clear result of the upward trend in consumers' share of GDP (Chart 4) and declining saving rate for a quarter-century has been the downtrend in the foreign trade and current account balances. We can't overemphasize the importance of the profligate U.S. consumer in fueling economic growth in the rest of the world, as we've discussed in many past Insights. We have also published our analysis of Asian exports. The intra-Asian trade was much bigger than the direct exports to the U.S., but when we accounted for the components produced in, say, Taiwan that were sent for subassembly to Thailand, then to Malaysia for final assembly with the finished product destined for the U.S., over half of Asian exports ended up in America.

Export-Dependent China

In late 2007, most forecasters disagreed with us and said China's economy would continue to grow at double-digit rates, and even support the U.S. economy if it softened. However, in "The Chinese Middle Class: 110 Million Is Not Enough" (Nov. 2007 Insight), we explained that China was not yet far enough along the road to industrialization to have a big enough middle class of free spenders to sustain economic growth if exports fell with U.S. consumer spending, as we were predicting.

As we noted in that report, in China, it takes $5,000 or more in per capita income to have meaningful discretionary spending. The 110 million who fit that category are a lot of people, but only 8% of China's population. In India, the middle and upper income classes are even smaller, 5%. In contrast, in the U.S. it takes $26,000 or more to have middle-class spending power, and 80% of Americans qualify. So we wrote in that report that all the cell phones and PCs being bought by Chinese was not the result of domestic economic strength, but merely the recycling of export revenues and direct foreign investment funds. And we went on to forecast that U.S. consumers would retrench, resulting in a nosedive in Chinese exports and a deep recessionary slump in China's growth.

Well, as they say, the rest is history. It now seems likely that China's earlier double-digit growth rates will slip to the 5%-6% range that would probably constitute a major recession, and probably lower. About 8% growth is needed to accommodate the vast numbers who continually flood from the countryside to the cities in search of work and better lives. Of those who went back to their villages to celebrate the recent lunar new year, 20 million didn't return because their factory jobs had vanished along with Chinese exports. Worker unrest us mounting and just as civil disturbances have ended many past Chinese dynasties, the Mao Dynasty's days may be numbered, as we've discussed in past Insights.

No Winners

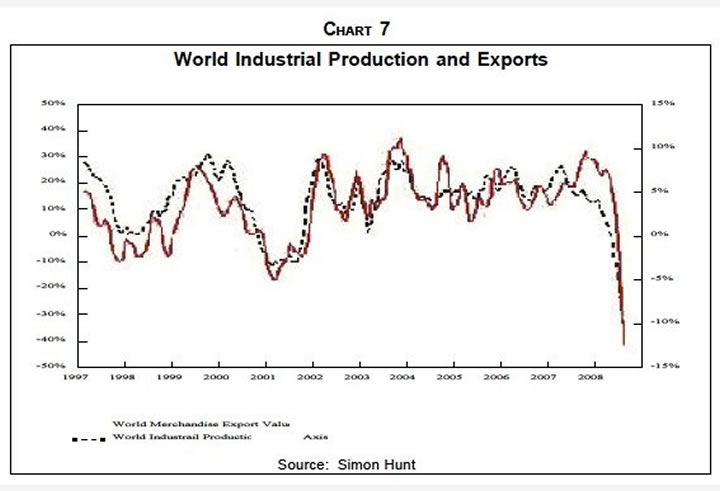

With subdued U.S. consumer spending in the years ahead and the resulting weakness in American imports, economic growth abroad will be even weaker than in the U.S. Note that in previous U.S. recessions, the current account and trade balances tend to rise as imports weaken with economic activity, but exports fall less as economic growth abroad persists. That's been true of late, even though most would prefer strengthening balances from strong U.S. exports, not weaker imports. In any event, falling economies overseas are already weakening U.S. exports (Chart 6) and subdued global growth in the years ahead will probably limit the improvement in the U.S. current account and trade balances. Notice the close link between world industrial production and merchandise exports (Chart 7).

First And Last Resort

Now, with American consumers embarking on a saving spree, the U.S. will no longer be the buyer of first and last resort for the globe's excess goods and services. Furthermore, with slower global growth for years ahead, virtually every country will promote exports to spur domestic activity. Already, China has stopped allowing her yuan to rise in order to gain a bigger share of a declining pool of global exports.

Financial Deleveraging

There's no question that the financial sector is deleveraging, and its embarrassed leaders, pressured by regulators and everyone else, will no doubt continue this process for years to come. Securitization, off-balance sheet financing, derivatives and other financial vehicles that both stimulated and distorted economic activity are disappearing.

Big banks are reducing exposure to volatile proprietary trading and emphasizing safer asset management. Hence, Morgan Stanley's interest in buying Smith Barney, the brokerage unit of cash-hungry Citigroup. Furthermore, banks are cutting their financing of hedge funds by concentrating on the likely survivors in the ongoing shake-out and cutting off the rest. This will hasten the demise of many less-successful as well as smaller shops that are also at risk of investor withdrawals.

Banks are retrenching from lending to the point that corporate borrowers are turning to the bond market instead for funding. Despite government bailouts, writedowns continue to erode bank capital. Many still hold some of the leveraged loans they made to fund private equity leveraged buyouts back in the boom days. Lenders normally recover 80% on those loans when borrowers default since they rank high in the recovery pecking order. But recent bankruptcies indicate 25% recovery rates. Earlier, Japanese banks were flush with cash, but sharply lower earnings outlooks suggest they no longer will be able to provide capital to international markets.

As banks retreat to their core competencies, they're selling non-essential units. Faced with lasting fear spawned by huge losses and pressed by regulators, these institutions are retreating to basic banking 101. That's spread lending in which deposits are lent with a market-determined interest rate spread that covers costs plus a modest profit. Banks are also consolidating in response to gigantic losses and bleak outlooks. France's BNP Paribas bought the Belgium and Luxembourg assets of Fortis. Spain's Santander is acquiring full control of Sovereign Bancorp based in Wyomissing, Pa. Large consolidated financial institutions don't tend to be big risk-takers, and often lack the entrepreneurial spirit that promotes productivity and economic growth. Also, with fewer institutions, there are fewer counterparts to share risks, and that also dampens activity.

Eastern Europe

Overseas, Western banks largely financed the rapid economic growth in the former Iron Curtain countries in Europe after the Soviet Union collapsed in 1991. In addition, many companies in those lands financed their domestic businesses by borrowing Swiss francs, euros and other hard currencies at lower rates than in their own inflation-prone countries. Individuals entered the same carry trade to fund their home mortgages.

Now, however, lenders are retreating as they delever. Exports to Western Europe, another important source of growth, are falling. Eastern European borrowers need to repay $400 billion owed to Western banks this year, much of it denominated in foreign currencies. Eurozone banks have outstanding loans to Central and Eastern Europe totaling $1.3 trillion. EU leaders, led by German Chancellor Merkel, recently rejected a $240 billion bailout of Eastern Europe proposed by Hungary.

Like Asia 1997-1998

The dependence of Central and Eastern Europe on foreign financing is painfully similar to that is Asia in the 1990s that led to the 1997-1998 financial and economic collapse--except it probably will be worse this time since banks are delevering this time and weren't back then. Also, these European countries were more leveraged in 2008 than their Asian counterparts a decade ago. This can be seen in their foreign debts in relation to GDP (Chart 8) and in their current account deficit/GDP (Chart 9) as well as in their currency declines.

Asian lands reacted to the 1997-1998 crisis by cutting foreign borrowing and building foreign currency reserves. Ironically, however, they still didn't escape the current global recession and financial crisis. They're no longer as dependent on inflows of foreign capital, but this time are highly dependent on exports, which are plummeting as U.S. consumers retrench.

Commodity Crisis

The collapse of the commodity bubble will also subdue global economic growth in future years. Sure, commodity consumers benefit from lower prices as producers lose. But the share of total spending on commodity imports by consumers, especially developed lands, is tiny while they account for the bulk of exports for producers, notably developing countries.

Budget Signals

The new Obama federal budget points clearly to more government regulation and involvement in the economy. Going well beyond dealing with the deepening recession and financial crisis, the President wants $630 billion to move toward national health insurance. Businesses that emit carbon dioxide and other greenhouse gases would have to purchase permits. Another $20 billion would go for clean energy technology. The government would essentially take over student loans while eliminating private lenders, and make them entitlements with no annual limits on loan totals.

Obama also plans to increase taxes in higher-income households and capital gains and estate while redistributing money to lower-income people, even those who don't pay taxes. This reflects his populist views on the campaign trail, but with considerably more edge. The President's budget document states, "Prudent investments in education, clean energy, health care and infrastructure were sacrificed for huge tax cuts for the wealthy and well-connected. In the face of these trade-offs, Washington has ignored the squeeze on middle-class families that is making it harder for them to get ahead. There's nothing wrong with making money, but there is something wrong when we allow the playing field to be tilted so far in the favor of so few." The President's budget message also attacks "a legacy of misplaced priorities...and irresponsible policy choice in Washington."

Corporations, the energy industry, hedge funds and large farmers would also pay higher taxes while families with annual incomes under $200,000 and especially the working poor would get government checks.

The budget calls for more enforcement money for the FDA to step up drug safety rules, more for the EPA to crack down on industrial polluters, additional funds to protect endangered species and land and water conservation and to protect wildlife from climate change. More money is also requested to enforce fair housing laws and better disclosure of mortgage terms and to reverse "years of erosion in funding for labor law enforcement agencies." Employers that don't offer retirement plans will be forced to open IRAs for employees. There's also additional funds requested for enforcing workplace safety rules.

Stress Tests

Major banks are being stress-tested to determine their volatility under adverse conditions. To date, Fannie and Freddie are in conservatorship and controlled by the government. The remaining major investment banks, Goldman Sachs and Morgan Stanley are bank holding companies with Federal Reserve regulation. Is it a big surprise that Litton Loan Servicing, owned by Goldman, recently changed its strategy on mortgage modification to reduce borrowers' monthly payments to 31% of income from 38%, the industry standard?

Citigroup and BofA are, for all intents and purposes, wards of the state while the media and Washington spar over whether they will be formally owned by the government. Those two banks recently agreed to suspend mortgage foreclosures until the Treasury sets up its rescue program.

AIG is 85% owned by the Fed, which probably wishes it owned nothing of that bottomless money pit that has already absorbed $150 billion in government money. Recently, the government initiated its fourth plan to rescue AIG,which just reported a $62 billion loss in the fourth quarter. The firm is so troubled that Washington has completely backed away from its role as a stern lender that forced AIG to pay high interest rates on what it assumed would be short-term loans. Now the government is relaxing loan terms by wiping out interest in hopes of preserving some value for AIG. And it will be more involved as it splits AIG into two pieces and gets preferred shares in each entity.

Auto Bailout Payback

Beyond the financial sector, the ongoing bailout of U.S. auto producers is leading to more government intervention in that industry. As usual, he who pays the piper calls the tune. The government has already pumped $17.4 billion into GM and Chrysler, and they say they may need $21.6 billion more. GM also proposes a $4.5 billion credit insurance program for the auto parts makers. Furthermore, GMAC may need more than the $5 billion sunk into it by the Treasury last December.

Bonuses

Of all the signs of opulence carried over from the bubble years, corporate jets and big executive bonuses seem to bother Washington the most. BofA is selling three of its seven jets, a helicopter that was owned by Merrill Lynch and one of two of its New York corporate apartments. Obama wants firms that accept "extraordinary assistance" from the government to cap annual pay at $500,000, disclose pay to shareholders for a non-binding vote, claw back bonuses of corporate officials who provide misleading information, eliminate golden parachutes for those terminated and adopt board policies for luxuries such as entertainment and jets.

This reaction to big bonuses in firms that are taking huge writeoffs, losing big money and requiring massive government bailouts was predictable. From 2002 to 2008, the five largest Wall Street firms paid $190 billion in bonuses while earning $76 billion in profits. Last year, they had a combined net loss of $25 billion but paid bonuses of $26 billion.

The Trouble With More Regulation

Increased regulation may be the natural reaction to financial and economic woes, but it is fraught with problems. It's a reaction to crises and, therefore, comes too late to prevent them. And it often amounts to fighting the last war since the next set of problems will be outside the purview of these new regulations. That's almost guaranteed to be the case since fixed rules only invite all those well-paid bright guys and gals on Wall Street and elsewhere to figure ways around them.

Furthermore, government regulators have never, as far as we know, stopped big bubbles or caught big crooks. Consider the dot com and then the housing blowoffs, both of which occurred while the SEC, the Fed, other regulators, Congress, etc. sat on their hands. Think about Enron, WorldCom and Bernie Madoff, all of whom went on their merry ways until their self-induced collapses, completely free of regulatory interference.

Most importantly, government regulation and involvement in the economy is almost certain to prove inefficient. Risk-taking has been excessive, but government bureaucrats are likely to eliminate much of it, to the detriment of entrepreneurial activity, financial innovation and economic growth. Fannie, Freddie and government-controlled banks are now being directed by the government to modify mortgages to accommodate distressed homeowners. That may implement government policy, but leads to bad business decisions.

Confusion

Furthermore, if financial regulation changes massively, it probably will create confusion and uncertainty to the detriment of adequate financing, spending and investment. Some academics believe that the Great Depression was prolonged because the New Deal measures were so disruptive that banks and other financial firms as well as individual investors, consumers and businessmen were too scared to do anything. Recently, Tadao Noda, a Bank of Japan policy board member, said, "We are in a position where the central bank needs to interfere in financial markets, but if we do too much, the market functioning in turn may be hurt." In any event, major problems inexorably lead to greater government involvement. The Bush Administration was staunchly deregulatory in philosophy but forced to intervene in the financial crisis. The 20th century saw tremendous growth in government involvement in all aspects of the economy and financial markets as a result of three tremendous traumas--World Wars I and II and the Great Depression.

Protectionism

Recessions spawn economic nationalism, protectionism, and the deeper the slump, the stronger are those tendencies. It's ever so easy to blame foreigners for domestic woes and take actions to protect the home turf while repelling the invaders. The beneficial effects of free trade are considerable but diffuse while the loss of one's job to imports is very specific. And politicians find protectionism to be a convenient vote-getter since foreigners don't vote in domestic elections.

U.S. Leadership

Sadly, the U.S. appears to be among the leaders for protection of goods and services against foreign competition. The auto loan program last year under the Bush Administration largely excluded foreign transplants. Obama advocates a super-competitive economy, which requires highly productive workers. Yet the recent fiscal stimulus law restricted H-1B visas, granted to foreigners with advanced education and skills, for employees of firms that receive TARP (bank bailout) money.

Some in Congress worried that tax credits for renewable energy should be confined to American-produced equipment. And recall that during the presidential campaign, Obama called for renegotiating the North American Free Trade Agreement. Furthermore, the President's emphasis on health care, education and renewable energy turns attention inward, toward self-sufficiency and away from a global focus.

Outside the U.S., protectionism is being promoted by labor unrest. In England, workers at a French-owned oil refinery struck because Total awarded a construction contract to an Italian firm that planned to use its own staff from abroad rather than local workers. Rioters on the French Caribbean island of Guadeloupe protested high prices for food and other necessities for a month recently. High unemployment rates, especially among younger workers, have precipitated riots in Latvia, Lithuania, Greece, Russia and Bulgaria as well as France.

Competitive Devaluations

Good old-fashioned competitive devaluations to spur exports and retard imports, a mainstay of the 1930s, are making a comeback. Kazakhstan recently devalued, in part because of devaluations of her trading partners. As noted earlier, China stopped allowing her yuan to appreciate, in part because her labor costs are being undercut by countries like Vietnam and Bangladesh.

With the understanding that protectionism helped make the Great Depression "Great," country leaders still publicly espouse free trade and reject protectionism. And they express confidence that global organizations like the WTO, IMF and World Bank will forestall protectionism and economic nationalism, and they engage in endless meetings to promote free trade as well as global standards and cooperation for handling the deepening financial crisis. But almost nothing happens, as shown by the recent EU refusal to bail out Eastern Europe.

Stealth Protectionism

In any event, protectionism is returning by stealth. U.S. steelmakers plan to file anti-dumping suits against foreign producers, a strategy they have employed successfully for decades, and India recently proposed increased steel tariffs. In the first half of 2008, WTO antidumping investigations were up 30% from a year earlier. Bank bailouts have been aimed at protecting local institutions, as discussed earlier, and the Japanese government is buying stocks of Japan-based corporations to help company balance sheets, but also giving them a competitive advantage over the subsidiaries of foreign outfits.

Like America, France is aiding its own auto producers, not transplants, and has created a sovereign wealth fund to keep "national champions" out of foreign ownership. Since last November, Russia has introduced 28 import duty and export subsidies affecting steel, oil and other products as well as imposed special road tolls on trucks from the EU, Switzerland and Turkmenistan. Russia's tariff on imported cars recently rose 5 to 10 percentage points, curtailing shipments of used cars from Japan to the Russian Far East.

Meanwhile, Argentina has imposed new obstacles to imported shoes and auto parts. The EU again is giving export refunds to dairy farmers, to the detriment of New Zealand, slapped anti-dumping charges on Chinese nuts and bolts, and threatens duties on U.S. biodiesel imports in retaliation for America's export subsidies. Not to be outdone, the U.S. plans retaliatory tariffs on Italian water and French cheese in reaction to EU restrictions on U.S. chicken and beef imports in the hormones war.

Ecuador lifted tariffs across the board recently, with the levy on imported meat rising to 85.5% from 25%. Indonesia is using special import licenses to limit the inflow of clothing, shoes and electronics and also is curtailing toy imports by allowing them to enter through only a few of its ports. And there's the old standby, health and safety standards that Japan relies on consistently to keep out unwanted products.

Deflation

Long-time Insight readers know that we have been forecasting chronic deflation to start with the next major global recession. Well, that recession is here. As discussed in our Nov. 2008 Insight, deflation results when the overall supply of goods and services exceeds demand, and can result from supply leaping or from demand dropping. We've been forecasting chronic good deflation of excess supply because of today's convergence of many significant productivity-soaked technologies such as semiconductors, computers, the Internet, telecom and biotech that should hype output. Ditto for the globalization of production and the other deflationary forces we've been discussing since we wrote two books on deflation in the late 1990s, Deflation: Why it's coming, whether it's good or bad, and how it will affect your investments, business and personal affairs (1998) and Deflation: How to survive and thrive in the coming wave of deflation (1999). As a result of rapid productivity growth, fewer and fewer man-hours are needed to produce goods and services. Estimates are that 65% of jobs lost in manufacturing between 2000 and 2006 were due to productivity growth with only 35% due to outsourcing overseas.

Similar conditions held in the late 1800s when the American Industrial Revolution came into full flower after the Civil War. Value added in manufacturing leaped, and at the same time, real GNP grew 4.32% per year from 1869 to 1898, an unrivaled rate for a period that long, and consumption per consumer jumped 2.33% per year. Yet wholesale prices dropped 50% between 1870 and 1896, a 2.6% annual rate of decline. Good deflation also existed in the Roaring '20s when the driving new technologies were electrification of factories and homes and mass-produced automobiles.

The 1930s

In contrast, bad deflation reigned in the 1930s as the Great Depression pushed demand well below supply. As in the 1839-1843 depression, the money supply, prices, banks and real goods and services all nosedived. Employment dropped along with prices in the Great Depression and the unemployment rate rose to 25%. That depression was truly global.

We've consistently predicted the good deflation of excess supply, but in our two Deflation books and subsequent reports, we said clearly that the bad deflation of deficient demand could occur--due to severe and widespread financial crises or due to global protectionism. Both are clear threats, as explained earlier in this report.

Furthermore, with slower global economic growth in the years ahead due to the U.S. consumer saving spree, worldwide financial deleveragings, low commodity prices, increased government regulation and protectionism, excess global capacity will probably be a chronic problem. So deflation in the years ahead is likely to be a combination of good and bad.

Supply will be ample due to new tech, globalization and other factors we've explored over the years such as no big global wars (we hope), continual inflation worries by central bankers, continuing restructuring, and cost-cutting mass retailing. But demand will be weak, as discussed earlier. The chronic 1% to 2% deflation from excess supply that we forecast earlier still seems likely, but now we're adding 1% due to weak demand for a total of 2% to 3% annual declines in aggregate price indices for years to come.

2009 Seems Easy

For four reasons, the deflation that started several months ago (Chart 10) is quite likely to persist along with the recession, or at least until early 2010. First, the collapse in commodity prices continues and past declines are still working their way through the system. Crude oil prices have collapsed from $147 per barrel to around $40. Steel semi-finished billet prices were $1,200 a metric ton last summer but now is $350. Iron ore costs per metric ton dropped from $200 early last year to $80. It takes time for steel prices to work through to final consumer goods prices such as for washing machines.

Second, producers, importers, wholesalers and retailers were caught flat-footed by the sudden nosedive in consumer spending late last year and continue to unload surplus goods by slashing prices. All the giveaway bargains at Christmas still didn't entice enough consumers to open their wallets. Spring apparel, ordered before consumer retrenchment, is clearly in excess and being marked down before it's put on the racks. Retailers from Saks on down continue to chop prices. Branded food product manufacturers are willing to promote their wares alongside the private-label goods that supermarkets shoppers increasingly favor.

Wage Cuts

Third, wages are actually being cut for the first time since the 1930s. Previously, labor costs were controlled by layoffs, which still dominate. Benefits have also been trimmed in recent years by switching from defined contribution pensions to 401(k)s and increasing employee contributions to health care costs. Most workers are less sensitive to benefits than to salaries and wages, but the deepening recession and mounting layoffs (Chart 5) are making them more amenable to wage cuts.

So is the growing use of this approach. In a recent poll, 13% of companies plan layoffs in the next 12 months, but 4% expect to reduce salaries and 8% will cut workweeks.

So it just isn't the CEO who is taking the symbolic pay cut to deal with tough times. We argued in our Deflation books that cutting pay rather than staff is more humane, better for morale and better for keeping the organization together and ready for a business rebound. Now increasing numbers of employers agree with us.

A final reason to expect deflation in coming quarters in the U.S. is the surplus of aggregate supply over demand. Notice that the supply-demand gap is an excellent forerunner of inflation six months later. And deflation this year is spreading globally. Japan is once again flirting with falling prices, Thailand's CPI in January fell year over year for the first time in a decade. In Europe, inflation rates are rapidly approaching zero.

Prices In Recovery

The real test of deflation will come when the economy recovers--in early 2010 or later, we believe. Inflation rates normally fall in recessions, but then revive when the economy resumes growth. This time, inflation rates started low, so declines into negative territory are normal, especially given the severity of the recession and the collapse in energy and other commodity prices. If we're right, however, aggregate price indices like the CPI and PPI will continue to drop in economic recovery and verify the arrival of chronic deflation.

Few agree with us. They've never seen anything but inflation in their business careers or lifetimes, so they think that's the way God made the world. Few can remember much about the 1930s, the last time deflation reigned. Furthermore, we all tend to have inflation biases. When we pay higher prices, it's because of the inflation devil, but lower prices are a result of our smart shopping and bargaining skills. Furthermore, we don't calculate the quality-adjusted price declines that result from technological improvements. This is especially true since many of those items, like TVs, are bought so infrequently that we have no idea what we paid for the last one. But we sure remember the cost of gasoline on the last fill-up a week ago.

Too Much Money?

The main reason most expect inflation to resume, however, is because of all the money that's being pumped out by the Fed and other central banks as well as the Treasury to finance the mushrooming federal deficit. When the economy revives, they fear, all this liquidity will turn into inflationary excess demand.

At present, the Fed's generosity isn't getting outside the banks into loans that create money.

When cyclical economic recovery finally does arrive in 2010 or later, it will probably be sluggish and lenders will still likely be cautious, as discussed earlier. Furthermore, any meaningful increase in loans will probably continue to be more than offset by the continual destruction of liquidity as writedowns, chargeoffs, elimination of derivatives, etc. persists for years. Derivatives represent liquidity. You can't use them at the grocery store, but at least until recently, they were interchangeable from money in many uses.

In Sum

The deepening recession and spreading financial crisis is the beginning of the unwinding of about three decades of financial leverage and spending excesses. The process will probably take many years to complete as U.S. consumers mount a decade-long saving spree, the world's financial institutions delever, commodity prices remain weak, government regulation intensifies and protectionism threatens, if not dominates. Sluggish economic growth and deflation are the likely results.

A. Gary Shilling's INSIGHT - March 2009

Telephone: 973-467-0070

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.