Global Ageing Population Financial and Economic Crisis Brewing

Economics / Demographics Oct 05, 2009 - 07:48 PM GMTBy: John_Mauldin

We all know that a large wave of Baby Boomers in the US are approaching retirement. But what about the rest of the world? And what happens when those retirees need to spend out of savings? There is more than just a credit crisis and a government deficit crisis in our future. A rising level of retirrees to workers is happening even as I write. And the US is not, for once, the center of the problem. As this week's writer of your Outside the Box Niels Jensen explains, we cannot all export our way out of the problem. There is a global adjustment that must happen and when it does, it will have serious consequences for all. This week's letter is guaranteed to make you think. Set aside a few minutes to do so.

We all know that a large wave of Baby Boomers in the US are approaching retirement. But what about the rest of the world? And what happens when those retirees need to spend out of savings? There is more than just a credit crisis and a government deficit crisis in our future. A rising level of retirrees to workers is happening even as I write. And the US is not, for once, the center of the problem. As this week's writer of your Outside the Box Niels Jensen explains, we cannot all export our way out of the problem. There is a global adjustment that must happen and when it does, it will have serious consequences for all. This week's letter is guaranteed to make you think. Set aside a few minutes to do so.

Niels Jensen is the Senior Partner of Absolute Return Partners based in London. I have worked closely with Niels for years and have found him to be one of the more savvy observers of the markets I know. You can see more of his work at www.arpllp.com and contact them at info@arpllp.com.

John Mauldin, Editor

Outside the Box

A Country for Old Men and a Bit of Samba

The Absolute Return Letter October 2009

The Man Card

"Excuse me Sir, can I see your Man Card?" The stone-faced look of the security guard at Dallas Fort Worth Airport gave nothing away and, after two days of celebrating John Mauldin's 60th, my brain was probably operating somewhat below full capacity. "I need to see your Man Card Sir". Couldn't he just go away, I thought to myself, not really sure how to deal with the situation. Suddenly his face cracked wide open and in the broadest possible Texas drawl he said: "With those pink socks on Sir, I need to make sure you are a man". Welcome to Dallas!

The highlight of the weekend was a two hour roundtable discussion on Saturday afternoon where John had asked 15 of his friends and business associates to share with the group what their fears and hopes were for the next 15-20 years. I duly noted that the issues on the minds of our American friends are not at all dissimilar to what we worry about in Europe – our children's welfare, unemployment, immigration, racism, the impact of technology and the aging of our society to mention but a few.

This month's letter is about demographics and is the second in our series about major trends defining the future of the world we live in. Last month I wrote about the energy outlook, and I had an unusually high number of emails commenting on the letter. Many of them made the point that the world is in better shape than I seem to think, even if oil supplies are dwindling, as natural gas reserves are ample. We just need to switch source. Whilst I don't disagree that natural gas seems the way forward, one should not underestimate the task ahead of us. About 2/3 of all oil is used for transportation purposes and it is an enormous task to reduce our oil dependency. It will take many, many years and cost gigantic sums of money.

It is the banks, Stupid!

Back to this month's topic - in the financial press, there has been no shortage of attempts to apportion blame for the credit crisis. Disregarding the more obvious finger-pointing (it is the banks, stupid!), there seems to be a growing acknowledgement that large imbalances in the global economy are to blame for the current mess.

Put differently, a large number of countries - mainly Anglo-Saxon in origin but also the majority of our Eastern European friends - became credit junkies and spent beyond their means, year-in year-out. Conversely countries with large current account surpluses (e.g. China, Japan and Germany) were only too happy to deliver the drug to the intoxicated.

It is therefore too simplistic to suggest that only the deficit countries are to blame. The suppliers of credit must accept that they carry no small part of the responsibility, just like the drug dealers do when supplying junkies. In the past, I have been critical of Ms. Merkel of Germany when she stated publicly that Germany should continue to do what Germany does best, and that is to export goods of high quality. The obvious point here is that if Germany pursues such a strategy, the world will be no more balanced ten years from now than it is today, and a crisis similar to the one we have just been through could happen again.

It should therefore be obvious that not only should the deficit nations become more disciplined (i.e. save more and spend less), but the large surplus nations should actually put measures in place to ensure that their citizens save less and spend more. In practice, however, that is easier said than done. Demographic forces have a much bigger say on spending and savings patterns than generally acknowledged.

The Life Cycle Hypothesis

My story begins with Franco Modigliani. In 1985 he was awarded the Nobel Memorial Prize in Economic Sciences for his life cycle hypothesis which (somewhat simplified) states that spending and savings patterns are predictable and largely a function of demographics. When you are in your 20s and 30s, savings are low as much of your income is spent on establishing a family, buying and furnishing your home, putting the children through education, etc. Then comes a phase, from your early to mid 40s until just before you reach retirement age, where your savings grow significantly. The outgoings are smaller during this phase of your life as the kids have left home, and you focus on accumulating wealth to pay for your retirement. Eventually, when you retire, your savings rate turns negative as you begin to live on your life savings1.

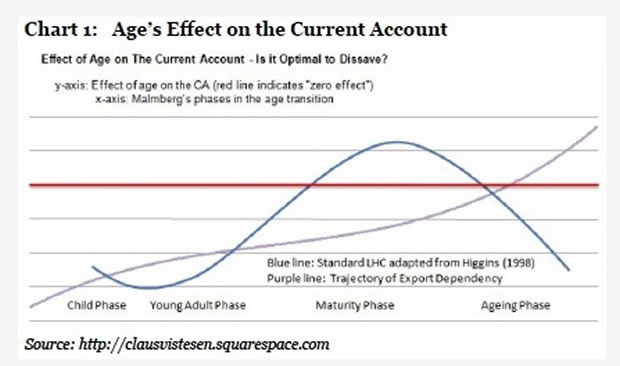

Empirical evidence has since shown that this is generally true both for the individual and for society at large. Obviously, you don't win the Nobel Prize for pointing out something that can hardly be classified as original thinking, but Modigliani's claim to fame was to demonstrate the effect this pattern has on the general economy as the population ages. Let me introduce you to a chart constructed by fellow Dane Claus Vistesen who is an economist and active blogger. He has made a solid attempt to graphically illustrate the consequences of Modigliani's work (chart 1).

The blue line represents the current account – it is in surplus when above the red line and in deficit when below. As you can see, when a country's population is relatively young, the country should (all other things being equal) run a current account deficit. As the population grows older, and the savings rate rises for the reasons described above, the deficit turns into a surplus until such time that the elderly begin to dominate the young at which point the surplus turns into a deficit yet again.

Our export dependency

Why is all this important? Well, take another look at chart 1, but focus on the purple line instead, which represents the country's export dependency. Translated into plain English, Modigliani's work implies that a country with an ageing population must grow its exports aggressively in order not to build up an unsustainably large current account deficit. Unfortunately, as you can see from the shape of the curve, it is not a linear function. The problem gets progressively worse as the population ages.

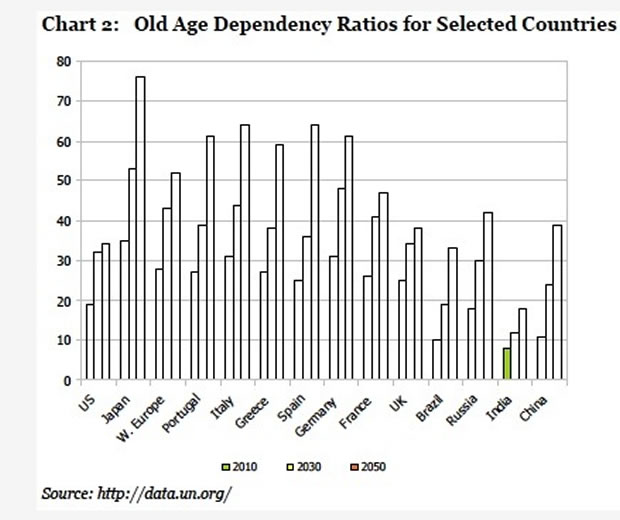

Now, with most OECD countries fast approaching the danger zone where an uncomfortably large part of the population consists of old-age pensioners, how do we get out of this pickle? We can't all export our way out of the problem. Somebody needs to buy our products. I will get back to answering this question later, but let's take a quick look at the so-called dependency ratio first. If the ratio is, say, 30, it means that there are 30 people at the age of 65 or older for every 100 people between the age of 15 and 64 (which defines the working population).

Obviously, the higher the dependency ratio, the fewer working people there are to pay for the elderly. At some point the cost of supporting the elderly will reach a level which spells economic disaster, and some of the more exposed countries may quite simply be forced to abandon their welfare standards to cope. More about this later -let's get some data points on the table. In chart 2 below, I have tried to keep things relatively simple. I have assumed, for example, that the fertility rate will remain unchanged going forward. This may or may not be a reasonable assumption. Only time can tell.

A walk in the park

The first thing that struck me when I produced this chart was how relatively benign the US outlook is. I read an awful lot of US centric macro economic research (my wife thinks too much!) and, more often than not, there is a reference to the bleak future for America given the fact that baby boomers in large numbers will be retiring over the next two decades. However, when you compare the US numbers (a dependency ratio of 19 today growing to 34 by 2050) to most other developed nations, the US demographic challenge suddenly looks like a walk in the park.

No other country is aging as quickly as Japan. Saddled with a large number of old age pensioners already (the dependency ratio is currently 35), the ratio will grow to an astonishing 76 over the next four decades. The Japanese economy has struggled to drag itself out of a slow growth environment for the past twenty years (give or take). The problems in Japan are well publicised and are often blamed on failed policy measures. I just wonder how big a role demographics have actually played in all of this and whether the Japanese mire is a sign of things to come for the rest of us?

Europe is toasted

The outlook for Europe doesn't make for pretty reading either. In fact, you can argue that we are worse off than Japan given our lower savings, and it raises some serious questions about the sustainability of our entire welfare model. The IMF has calculated that the cost of age-related spending in the average advanced G20 country will cause public debt-to-GDP to grow to over 400%, with Spain and Greece reaching over 600% unless the existing welfare model is cut back. For comparison, Japan has the highest public debt-to-GDP ratio today at about 225%.

As our business partner, John Mauldin, always reminds us, what cannot happen, will not. We may have to prohibit the use of condoms (not advisable for other reasons), import more labour from countries with higher birth rates (immensely unpopular) or simply reduce old-age benefits. The latter carries its own set of challenges as the political influence of the elderly is on the rise, and it won't exactly become any easier over the next 20 years to pass draconian legislation to reduce old-age benefits. Frankly, I have no idea how we will find a way out of this pickle. But find a way we will.

BRICs versus PIGS

As far as emerging economies are concerned, the outlook is considerably brighter (note the big difference between the BRICs and the PIGS in chart 2) but perhaps not as straightforward as you may think. Most investors seem to buy into the idea that, over the next few decades, emerging markets will offer better investment opportunities than more mature markets, as their economies are likely to grow much faster, and you don't yet pay for the faster growth through higher P/E ratios. Whilst we wrestle with depressing issues such as how to pay for the credit crisis and how not to bankrupt ourselves as we age, emerging economies should benefit from a growing labour force. In fact, as you can see from chart 3, in the next few years less developed countries, which tend to have very young populations, will actually outgrow more developed countries in terms of the size of the working population relative to the total population (which is good for economic growth).

The growing number of workers should, according to Modigliani, be followed by stronger economic growth and rising savings. If these savings can be invested into new productivity enhancing investments, emerging economies should enjoy much higher living standards in the years to come. You may raise a hand here and say "STOP – didn't you just argue that countries with young populations should run current account deficits and hence low savings rates?" It is indeed correct that 'young' countries should, according to Modigliani's hypothesis, not be able to generate savings rates at the magnitude we have seen coming out of South East Asia in recent years.

Cheating is omnipresent

But Modigliani didn't take cheating into account. Virtually every country in Asia has artificially depressed its currency in recent years in order to export itself to prosperity. This cannot, and will not, go on forever. As living standards rise in these countries, and domestic demand fuels economic growth, expect their currencies to appreciate against the old world currencies.

At the same time, one should not ignore the fact that not all emerging economies have young populations. I have included the four BRIC countries in chart 2 in order to make this point clear. As you can see, by the middle of the century, China and Russia will actually both have a higher dependency ratio than the United Kingdom, whereas Brazil and in particular India should continue to benefit from relatively young populations.

At the same time, one should not ignore the fact that not all emerging economies have young populations. I have included the four BRIC countries in chart 2 in order to make this point clear. As you can see, by the middle of the century, China and Russia will actually both have a higher dependency ratio than the United Kingdom, whereas Brazil and in particular India should continue to benefit from relatively young populations.

In a recent research paper2, BCA Research analysed a number of emerging economies and found that, broadly speaking, they can be divided into 3 categories – those where the working population is peaking just about now, those that will peak in the next 7-10 years and finally those where the peak is still 15-20 years away (chart 4).

It is clear from BCA Research's work that some countries are in much better shape demographically than others. Most interestingly, China, which everybody (well, almost everybody) raves and rants about, does not look particularly attractive. Obviously you cannot judge the investment appeal based only on demographics, but if you add to that China's fragile banking system and a construction boom which has left most new buildings half empty and led the Chinese authorities to block local access to hedge fund manager Hugh Hendry's website, because he had the audacity to point out the insanity of many of the construction projects in China, then the Chinese investment story loses some of its glamour.

Too much of a good thing

A great growth story like China will always attract plenty of capital but, in the case of China, you can actually argue that too much capital has been attracted. As I was taught at university, economic growth loses its momentum if capital spending outgrows labour because of the diminishing return on capital. BCA has illustrated this graphically (chart 5), and it is obvious that China is attracting too much capital for its own good. You want to invest where capital is scarce, not plentiful.

You are therefore likely to earn a higher return on investment by investing elsewhere in the universe of emerging economies. One such country is Brazil which does not attract nearly the amount of capital that China does. I have been keeping an eye on Brazil for some time now as I am intrigued about their fledgling oil industry, and the more I learn about this country, the more excited I get. The story has not gotten any worse in recent days after the International Olympic Committee's decision to award the 2016 summer games to Rio de Janeiro. But that is an entirely different story which I may write more about another day.

Going back to the question I raised earlier, how do we get out of this pickle? As already stated, we cannot all become exporters as we grow older and domestic demand begins to fade. The only way out, if we want to maintain economic growth, is for the younger and more dynamic emerging economies to become net importers. This will require a sea change in policy, and attitude, in those countries. Most importantly, it will require the exchange rate cheating to stop once and for all. There is no alternative, unless you are prepared to accept negative GDP growth year-in year-out. And that is no fun.

Niels C. Jensen

Footnotes:

1 See http://www.princeton.edu/~deaton/downloads/romelecture.pdf for more information on Modigliani's work.

2 'Demographics, Investments and Growth: Where are the opportunities?', BCA Research, August 2009.

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.