House Prices to Drop by 50%, US Still Headed for A Recession Despite Fed Rate Cut

Economics / US Economy Sep 22, 2007 - 03:47 AM GMTBy: John_Mauldin

In this issue:

In this issue:

A Sea Change at the Fed

Transmission Problems

A 50% Drop in Housing Prices

Wildness Lies in Wait

I Still Think Recession

It's Good to Be Home

The term "sea change" has come to mean a profound transformation ever since Will Shakespeare used it in The Tempest. I think this week we witnessed a true sea change in central bank policy, on both sides of the Atlantic. The stock market rejoiced over a 50 basis point cut from the Fed, assuming that it will stimulate growth and avoid anything more than a slowdown. In this week's letter, we ponder several questions. Why did the Fed decide to cut now when the rhetoric of just a few weeks ago was that of inflation fighting? What do they see? Are more rate cuts coming? Will they make any difference? And who is Frederic (Rick) Mishkin and why is he maybe the most important Fed governor you haven't heard of? There's a lot of ground to cover, and it should make for an interesting letter.

But first, I need to acknowledge an anniversary of sorts. Some seven years ago I put this e-letter on the internet, with (maybe) 2,000 names to send it to. Today, it goes out every week to more than 1,000,000 readers and is posted on scores of web sites such as the Market Oracle. I have to confess with being a little (well, a lot) amazed by it all. It has changed my business practice in ways that I could not imagine seven years ago, and all for the better. Someone asked me what I will do when I retire. I told them I would read, write, travel and speak, which is pretty much what I do now, along with a few extra duties here and there.

But it is a great life and I want to thank you for allowing me to come into your home or office, and for recommending this letter to friends, which is the way the readership has grown. And because I want to keep writing for a long time and I want to keep you as a reader, I am going to make available to you a speech on how we can all live longer by Dr. Mike Roizen, who wrote You - The Owner's Manual (and You - On a Diet , and the other monster best-sellers in the series). He also appears on Oprah about six times a year. I am lucky enough to call him both friend and my doctor.

Mike spoke at my Strategic Investment Conference last year, telling us that if we don't like the way our bodies are doing, it is ok. We can get a "do-over." Mike is one of the true experts on aging (or anti-aging) and shared how we could all live a lot longer and healthier. It was a great speech.

Just a small catch. Let me ask a favor. Since all I really know about you is an email address, I really don't know a lot about who reads me and why. I want to know more about my readers and what it is that you want. What type of e-letters do you like? What topics? Want a blog? More Outside the Boxes? Less? If you could take the time to fill out a short (and very anonymous!) survey, when you finish you will be taken to a page where you can listen to Mike's fascinating speech. There is also a place for comments and suggestions.

Thanks. Just click on the link http://www.frontlinethoughts.com/survey.htm when you are ready. And if you want to get Mike's books, you can go to www.amazon.com and pick any of his dozen books.

A Sea Change at the FedAs everyone knows, the Federal Reserve cut both the fed funds rate and the discount rate by 50 basis points this week. The rate cut was clearly telegraphed and only the amount of the cut was a mystery. And for reasons I lay out later on, I think there will be more cuts. But that is not the interesting thing, at least to me. I think the Fed under Bernanke has clearly taken a new direction in determining monetary policy, one that differs with past deliberations.

At Jackson Hole on August 31, Bernanke addressing the problem of moral hazard faced by Central Banks, Bernanke noted: "It is not the responsibility of the Federal Reserve -- nor would it be appropriate -- to protect lenders and investors from the consequences of their financial decisions." He did acknowledge that if the system as a whole was at risk, then a central bank would have to act even in spite of the moral hazard issue.

That was then and this is now. We got rate cuts September 18. Bernanke in his testimony to Congress this week said the Fed cut rates "to try to get out ahead of the situation and try to forestall potential effects of tighter credit conditions on the broader economy. While he gave no hints as to future policy, he did note that the Fed would "keep reassessing our outlook and adjusting policy" as the situation demanded.

Read those words again. "...to try to get out ahead of the situation..." Hello. That is something new. Normally watching the Fed and predicting the next move is about as exciting as watching paint dry. The Fed has always waited until the data suggested (and/or the market demanded) a rate hike or especially a cut. The Fed has been what good friend Paul McCulley calls "opportunistically disinflationary" for the past two-plus decades. They tighten until inflation comes down and only when it is apparent that a recession is in the works, or if there is a crisis like 1987 or 1998 (more on that important distinction later) do they cut rates. They have reacted to the data rather than made forward looking assumptions.

Over time, this has been a good policy, as it dropped inflation down from the mid-teens in 1980 to below 2% a few years ago. There are those who argue (and with some justification) that Greenspan left rates too low for too long and allowed inflation to rise back to an uncomfortable 3%, although it has been tending down of late.

But the point is that inflation is merely tending down. It is not below 2%, and year over year comparisons in the fourth quarter suggest that headline inflation of closer to 3% is quite possible. That being said, the similar comparison numbers for core inflation are not as difficult, but certainly do not suggest - at this time - that we will drop below 2% this year.

Indeed, there may be some concerns that the CPI (Consumer Price Index) number could come under pressure from the housing component. Given that home prices are falling, that may be considered odd by many. But CPI does not measure home prices. It measures something called owner's equivalent rent. And even as house prices rose by 93% in real terms (per Bob Shiller) in the last decade run-up, rent in real terms did not go up all that much, so the cost of a new home was not reflected in the CPI.

Now, we may have the opposite problem. As more and more people cannot get a mortgage coupled with a very precipitous rise in foreclosures, we are seeing more people who need to rent. Rental property availability in many markets is quite tight, which means that rent prices are increasing. If you go to the Bureau of Labor Statistics and look at the housing rent data, it is not too hard to think that the housing component of CPI could easily rise by more than 4% in the fourth quarter given the current trend.

Since the housing component is about 30% of the total CPI, a 4% inflation in housing could be significant. And oil is over $80 and rising. The dollar is falling, meaning that import prices are going to rise. And should we mention that food costs a lot more than this time last year?

Given that the Fed has two mandates, stable prices and full employment, is the Fed abandoning its inflation mandate? Is Bernanke, who argued in academia for explicit inflation targeting, no longer worried about inflation? Is he willing to accept the possibility of 3% inflation? Is inflation getting ready to come back, a la the 1970s? Isn't that what the rise of gold is telling us? And aren't TIPS suggesting the same since the rate cut (a long term 2.64% inflation)?

In general I think the answer is no. I think that the Fed is concerned about other problems, and specifically heading off a recession. And to that topic, we need to turn to a recent speech at Jackson Hole by Fed Governor Fred Mishkin.

Long time readers of this letter should recognize that name. Mishkin was the co-author of a 1996 New York Federal Reserve paper on the predictive power of an inverted yield curve and recessions, which I have written about on several occasions. He was most recently a professor at the Graduate School of Business at Columbia before President Bush nominated him to the Fed Board of Governors which he joined last September, 2006. His resume is long and strong. He is a consummate and well-regarded insider. ( http://www.federalreserve.gov/aboutthefed/bios/board/mishkin.htm )

At Jackson Hole in late August, he essentially argued that central bankers should ease monetary policy quickly and aggressively in response to a big fall in housing prices. "Presenting a paper on the final day of the Fed's Jackson Hole symposium, Mr. Mishkin said policymakers should not wait until output falls, but should 'react immediately to the house price decline when they see it.'

"He said the optimal policy response was both quicker and more aggressive than that suggested by a standard policy rule, in which policymakers respond only to deviations in output and inflation.

"He said simulations show that this approach 'can be very successful at counteracting the real effects' of even a large house price slump, because of the long lags from changes in housing wealth to changes in consumer spending." (Financial Times)

Transmission Problems In a car, the transmission is responsible for taking the power of the engine and transmitting it to wheels. Economists also talk about transmission. How does an opportunity (or problem) in one area affect another seemingly unrelated area? How does a rise in housing prices affect overall consumer spending? What is the mechanism (the transmission) of the Wealth Effect? One obvious answer (among many) would be Mortgage Equity Withdrawals that are possible as home prices double in ten years.

And Mishkin talks about just that transmission in his paper. And he makes it clear that a precipitous drop in home prices would be a negative force. Of course, that is somewhat intuitively obvious. But the interesting thing is that he argues for a pro-active response from the Fed when it becomes clear that housing prices are getting ready to fall. Let's read carefully the following from the closing arguments of his paper. (You can read the speech at http://www.federalreserve.gov/pubs/feds/2007/200740/200740pap.pdf )

"My discussion so far argues against a special emphasis on house prices in the conduct of monetary policy. This argument does not extend to a recommendation that central banks stand by idly when house prices climb steeply. To the contrary, central banks can take steps to reduce the negative consequences for aggregate economic activity of sharp movements in house prices. But rather than try to preemptively deal with the bubble--which I have argued is almost impossible to do--a prudent central bank would be better advised to deal with adverse macroeconomic consequences as they emerge in the wake of any substantial decline in asset prices. One way a central bank can prepare itself to react quickly is to explore various scenarios as a normal part of its business to assess how it might respond to a variety of shocks, including a drop in house prices, to achieve maximum sustainable employment and price stability.

"Indeed, the exploration of different scenarios by the central bank can be thought of as stress testing similar to that regularly conducted by commercial financial institutions and banking supervisors. They see how financial institutions will be affected by particular scenarios and then propose plans to ensure that the banks can withstand the negative effects. By conducting similar exercises, in this case for monetary policy, a central bank can mitigate the effects of a drop in house prices without having to judge that a bubble may be in progress or predict when a bubble might burst.

"One objection to an easing of monetary policy following the collapse of an asset bubble is that it might lead market participants to believe that the central bank will always act to prop up asset prices, a belief that can make a bubble more likely. The central bank can mitigate such an interpretation, however, if it publicly emphasizes that its monetary policy is not directed at stabilizing any particular asset price but is rather focused on achieving price stability and maximum sustainable employment. Making sure that a house-price collapse does not do serious harm to the aggregate economy in no way eliminates sharp declines in house prices and so does not provide insurance against such declines. The same reasoning holds true for stock prices. Indeed, we have seen substantial declines in housing and other asset prices in many countries even when monetary policy has been eased substantially."

A 50% Drop in Housing Prices Dr. Robert Shiller of Yale (of Irrational Exuberance fame) also presented at Jackson Hole. He said housing prices could fall as much as 50% in some areas given how home prices have diverged relative to rents.

Let's put the timing in perspective before we get back to housing. At the time of the Jackson Hole conference (my invitation once again seemed to get lost in the mail), the credit markets were in the process of freezing up. The European Central Bank was injecting hundreds of billions of euros into the economy. The Fed was also opening the monetary door. But as noted here often, the problem is not one of available liquidity, but of confidence.

The subprime problem, which everyone assured us last spring would not spread to other markets, clearly had infected the entire world. What should be a US problem was more of a problem for European banks. We were told that the housing markets were bottoming last winter and then last spring and now it is clear that we are no where close to a bottom. (I wrote about this time last year we would see a crash in the housing market in late 2007 and 2008 and this winter that the subprime problems would spread.)

By the end of August, all this had to be clear to the Fed gathering at Jackson Hole. And when Shiller stands up and starts talking about precipitous housing price drops, everyone evidently paid attention. Mishkin argues for a pro-active response, and the FOMC (the Federal Open Market Committee which sets rates) responded.

Let's run through the scenario that the US economy, and thus the world, faces. It is going to be many months before there is a functioning subprime mortgage market in the sense that mortgages can be packaged and sold to investors. We are first going to have to create transparency in the various banks to allow the commercial paper market to function. No one is going to buy commercial paper from a bank unless they are 100% sure they can get their money back. And you can't be sure unless there is transparency into the books of the lending institutions. And that includes all the SIVs or Special Investment Vehicles that allow banks to move liabilities off their books. Kind of. Sort of. Maybe. As long as there is not a problem. And then they come back.

Jumbo mortgages (over $417,000) are difficult to obtain without paying exorbitantly high rates. The only functioning mortgage markets are for conforming loans that can be sold to Fannie Mae or Freddie Mac or with FHA backing. (As an aside, I expect that $417,000 to be raised, and for government intervention in subprime markets.)

In effect, with what will be tighter standards for loans going forward, we are going to remove 10-15% of the home buyers that were in the market in 2005-6. That is a serious drop in potential demand. That in itself argues for a large drop in housing prices. Couple that with the rest of the housing market problems, and it could get ugly. Gary Shilling suggests a 25% drop. Dr. Roubini thinks 15-20%.

The total housing market value in the US is $20 trillion. Knock of $4 trillion, and you have a serious drop in the wealth of homeowners. For may, that completely wipes out equity built up over the years.

Wildness Lies in Wait "The real trouble with this world of ours is not that it is an unreasonable world, nor even that it is a reasonable one. The commonest kind of trouble is that it is nearly reasonable, but not quite. Life is not an illogicality; yet it is a trap for logicians.

"It looks just a little more mathematical and regular than it is; its exactitude is obvious, but its inexactitude is hidden; its wildness lies in wait." - G. K. Chesterton

All of the subprime mortgages and CDOs that sit on the books of banks throughout the world are the wildness that lies in wait. We can know with some exactitude that there are going to be $100 billion in losses, give or take. What we cannot know is from what hidden glen the losses will spring up. Where is this paper?

And thus the difference between risk and uncertainty. Risk has a price. You can establish the probability of a loss, and price it. Life insurance, as an example, or the likelihood of defaults in subprime mortgages (at least, before they dropped rational lending practices).

But you cannot price uncertainty. And now the markets are uncertain about subprime debt, and uncertain as to where that debt is. And so how do you price the debt? If you are no longer certain about German banks when two of them go belly up, then do you take any German bank paper? French paper? Commercial paper from Countrywide Mortgage?

You are a central banker. You can see the problem, and you can see that a housing led recession or at the very least a serious slowdown is in the near future. The mortgage credit markets are not functioning and may not for some time. Do you wait? Mishkin argues no.

Even though housing is only 5% of the economy, it is a huge part of the Wealth Effect. $4 trillion is not a small sum in the psychology of the consumer. Slower consumer spending, and consumer spending is clearly slowing, is the transmission which takes us from a housing recession to a general recession.

Slower consumer spending should result in lower inflation and lower prices. If you read Mishkin's paper, the Fed is clearly modeling the economy, and just as clearly their models suggests a problem.

And so we get a sea change. We get a Fed that is pro-active instead of reactive. That makes Fed-watching a whole new ball game.

A couple of side points. In 1998, the Fed cut rates 75 basis points in response to the Russian bond crisis and LTCM. When the crisis subsided, they took those cuts away fairly quickly. While I do not think this crisis subsides in a few months, if it does, and inflation even remotely ticks up, they will take the recent cut, and the ones they are going to make in the future, off the table just as quickly.

And I am running out of room, but the Bank of England's response to NorthRock was also a sea change. They in effect guaranteed all bank deposits in Great Britain. This will take some fleshing out on the part of authorities, but it is a big change.

I Still Think Recession Even with a proactive Fed, I think we do not avoid a recession.

I think the Fed did the right thing by cutting rates. I think they will cut them more as the economy continues to slow. We will see a Fed funds rate with a "3 handle" before this process is over (meaning that the Fed funds rate starts with a 3 from the current 4.75%). The Fed did not start down this road with the thought 50 basis points would be enough.

The point is to try and drop rates enough to make mortgages (when that market finally rights itself) low enough that home buyers can afford to buy homes. While that will help some individuals, the more important concern from a central bankers perspective is the total economy. You do not allow the housing market to implode on your watch and do nothing.

And yes, it will help business with lower funding costs and encourage deals and risk taking. Which is what you want when an economy is on the verge of recession.

But home construction, even with lower rates, is not going to turn around fast. At the peak of the market, we were building 2,000,000 new homes a year in the US. As the following chart from the Conference Board shows (thanks to Dennis Gartman), it is not unusual for housing starts to drop below 1,000,000, and this typically precedes a recession.

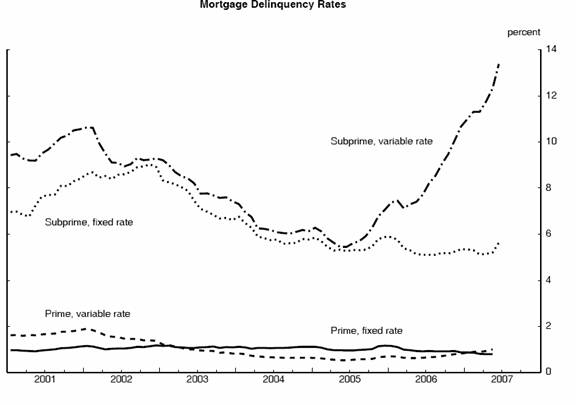

This of course is not helped by all the homes that are coming back onto the market via foreclosures. Mortgage delinquencies are rising, especially in the variable rate subprime market, as the chart below indicates.

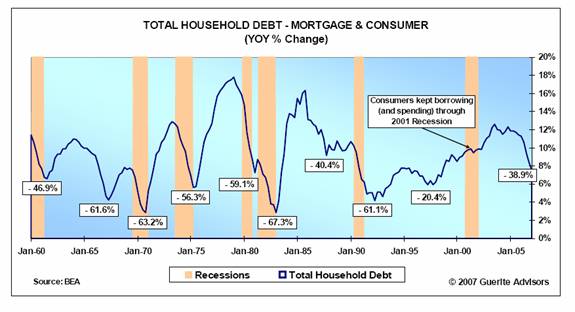

And all this puts pressure on consumer spending. Hugh Moore of Guerite Advisors writes:

"Consumer spending accounts for two-thirds of the U.S. economy. Total Household Debt is particularly important in supporting the growth of consumer spending. This indicator includes mortgage debt due to the important role that Home Equity Withdrawal (HEW) has played in sustaining the growth in consumption since the beginning of the decade.

"As shown in the graph below, each time the year-over-year increase in Total Household Debt has dropped more than 40% below its recent peak, a recession (or in the case of 1967, a mini-recession) has occurred. The mid-1980's slowdown touched this level, but did not exceed it. The current -38.9% level is approaching this boundary and, based on recent credit tightening by financial institutions, is likely to drop significantly below the -40% level.

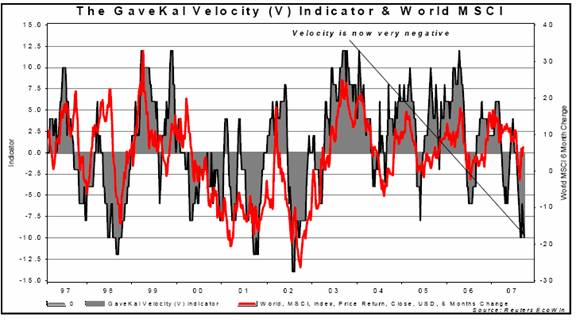

And quickly, a preview from next week's Outside the Box, courtesy of my friends at GaveKal (this actually written by Louis Gave). They track the velocity of money. As they note, central banks are pushing money into the system. But is it going anywhere?

"Which brings us to today. Following the recent central bank actions in the US, Europe and the UK, most commentators seem to expect a sharp acceleration of either inflation, economic activity, or asset prices (or all three). As a result, gold is making new highs, the US$ is plunging to new depths, etc.... But aren't the recent buyers of gold focusing solely on likely changes in the money supply (M), while forgetting why central banks are set to dump money into the system in the first place? Isn't the reason behind the loosening of monetary policies the fact that the velocity of money (V) has been plummeting?

"As in 2001, the question investors should thus ask themselves is whether velocity is set to rebound? If it is, then investors are right to position themselves for an ample liquidity environment (long gold, long commodities, long deep cyclicals).

"But if it isn't, then the investment environment could start getting a lot trickier." (emphasis mine).

We do live in interesting times. Next week I will try and look at the currency markets. The dollar is going to continue to be under pressure.

It's Good to be Home I must admit I do love to travel and see the world. But I have been doing a lot of travel this year, and it feels good to be home for the next three months. I am sure that something will come along and necessitate a trip, but right now re-acquainting myself with my home is a pleasant exercise. And even more fun in my new digs.

As many of you know, I moved my residence this spring to a high rise in an area of downtown Dallas called Uptown, as a personal experiment in urban living. It also puts me rather close to my two older girls. I find that I like it a great deal, at least so far. Being able to walk to restaurants, entertainment, shops and more is quite convenient, and the area is more fun than the suburbs I have haunted all my life. And I leased. I would have to pay almost two and a half times more a month to buy the equivalent space. That suggests there may be a buying opportunity at some point in the future.

I did my bit for the economy this week. I helped my daughter Abigail buy a car in Tulsa, where she goes to school. I must confess to not looking at a smaller car for a long time. I drive larger SUVs and have done so for decades. Abigail is 4'10" on a good day, so she was looking for a smaller car. We ended up with a Nissan Sentra. I was quite impressed with all the features and luxury that you can buy for $17,000. I know Bill King and others hate hedonic adjustments in the CPI, but this was a massively better car than I bought when I was 22, for about a third the nominal dollars, and used at that. Safer, more reliable. Airbags everywhere. 30 MPG. Blue tooth. 100,000 miles before the first tune-up. I used to change my plugs every 6,000 miles.

And best of all? "Dad, I have been looking at jobs in the paper here. There are just none for public relations, and I want to work for a sports team. I think I might move to Dallas when I graduate." Mark Cuban, are you reading? I'll be glad to drop you a resume at the season opener.

Life is so very good, even with all the bumps here and there. Once again, thanks from the bottom of my heart for letting me send you my musings each week. Your support and comments mean a lot, and I do appreciate it.

Your ready for the Mavericks to start playing again analyst

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2007 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.