Revisiting Bernanke’s QE2 October 2010 Speech

Interest-Rates / Quantitative Easing Jun 11, 2011 - 06:19 AM GMTBy: Asha_Bangalore

The Fed will complete the QE2 purchase plan of $600 billion securities as of June 2011, which is not too far ahead. But there is no assurance that self-sustained economic growth adequate to bring down the unemployment and stabilize the housing market will occur. In fact, the nature of recent economic reports inclusive of the ISM manufacturing survey, auto sales, retail sales excluding auto and gasoline, soft payroll growth, elevated unemployment rate, decelerating factory production, and continued slump in the housing market suggest that economy still needs watching over and support after nearly eight quarters of economic growth.

The Fed will complete the QE2 purchase plan of $600 billion securities as of June 2011, which is not too far ahead. But there is no assurance that self-sustained economic growth adequate to bring down the unemployment and stabilize the housing market will occur. In fact, the nature of recent economic reports inclusive of the ISM manufacturing survey, auto sales, retail sales excluding auto and gasoline, soft payroll growth, elevated unemployment rate, decelerating factory production, and continued slump in the housing market suggest that economy still needs watching over and support after nearly eight quarters of economic growth.

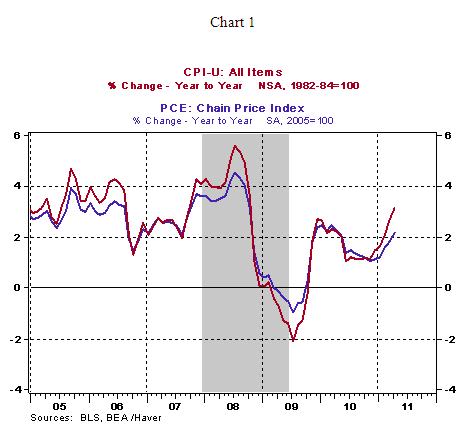

On October 15, 2010, prior to the commencement of QE2, Bernanke's speech (Monetary Policy Objectives and Tools in a Low-Inflation Environment) addressed monetary policy considerations in a "low-inflation environment." It is quite useful to revisit the details of this speech. Inflation readings have changed since this event and appear to have bottomed out in the final months of 2010. The personal consumption expenditure price index is hovering close to the preferred level, while the all items Consumer Price Index has crossed the threshold consistent with price stability (about 2.0%, see Chart 1).

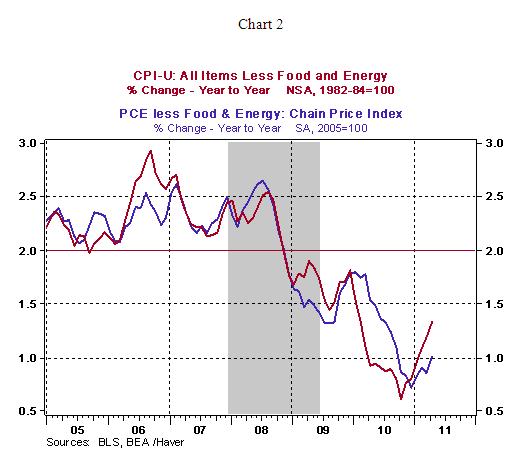

The core CPI and core personal expenditure price index, which exclude food and energy, show a muted gain which is considerably lower than the level consistent with price stability (around 2%, see Chart 2).

The following is an excerpt from the October 2010 speech (emphasis added):

Further policy accommodation is certainly possible even with the overnight interest rate at zero, but nonconventional policies have costs and limitations that must be taken into account in judging whether and how aggressively they should be used.

For example, a means of providing additional monetary stimulus, if warranted, would be to expand the Federal Reserve's holdings of longer-term securities. Empirical evidence suggests that our previous program of securities purchases was successful in bringing down longer-term interest rates and thereby supporting the economic recovery. A similar program conducted by the Bank of England also appears to have had benefits.

However, possible costs must be weighed against the potential benefits of nonconventional policies. One disadvantage of asset purchases relative to conventional monetary policy is that we have much less experience in judging the economic effects of this policy instrument, which makes it challenging to determine the appropriate quantity and pace of purchases and to communicate this policy response to the public. These factors have dictated that the FOMC proceed with some caution in deciding whether to engage in further purchases of longer-term securities.

Another concern associated with additional securities purchases is that substantial further expansion of the balance sheet could reduce public confidence in the Fed's ability to execute a smooth exit from its accommodative policies at the appropriate time. Even if unjustified, such a reduction in confidence might lead to an undesired increase in inflation expectations, to a level above the Committee's inflation objective.

In addition to the differences of opinions held by hawkish Fed Presidents (Fed Presidents Plosser, Fisher, Bullard and Hoenig), the legitimate concerns Bernanke listed in the October 2010 speech are likely to keep the Chairman in a watch-and-wait mode until ample evidence is available to convince members of the FOMC that additional financial accommodation may be necessary.

Asha Bangalore — Senior Vice President and Economist

http://www.northerntrust.com

Asha Bangalore is Vice President and Economist at The Northern Trust Company, Chicago. Prior to joining the bank in 1994, she was Consultant to savings and loan institutions and commercial banks at Financial & Economic Strategies Corporation, Chicago.

Copyright © 2011 Asha Bangalore

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.