U.S. Gas Price Redux

Commodities / Gas - Petrol Apr 14, 2012 - 07:50 AM GMTBy: Andy_Sutton

It is truly amazing how much can change in four years. Or, more accurately, how little things change in terms of human behavior. Four years ago the US was mired in the last spike in gasoline prices heading into the summer. Virtually every media outlet was conducting daily interviews, polls, and newsbytes about how Mr. and Mrs. Average were dealing with the high gas prices. Today, we have a new norm, and the wires are rather silent on the high gas prices other than quietly reporting the national averages. We as a country have come to be comfortable with $3.50 gas. Gas is one of those strange commodities too because, unlike so many other things, almost everyone has a pretty good idea of the price they paid for their last tankful.

It is truly amazing how much can change in four years. Or, more accurately, how little things change in terms of human behavior. Four years ago the US was mired in the last spike in gasoline prices heading into the summer. Virtually every media outlet was conducting daily interviews, polls, and newsbytes about how Mr. and Mrs. Average were dealing with the high gas prices. Today, we have a new norm, and the wires are rather silent on the high gas prices other than quietly reporting the national averages. We as a country have come to be comfortable with $3.50 gas. Gas is one of those strange commodities too because, unlike so many other things, almost everyone has a pretty good idea of the price they paid for their last tankful.

What should be even more disconcerting are the misperceptions surrounding this latest increase in prices. There have been many factors blamed so far, such as America’s lack of energy independence, speculation, more expensive summer blends, high gas taxes, and supply and demand. Some groups focus on refining capacity, while others focus on more energy efficient vehicles and higher EPA standards for efficiency. There are also others that argue that there should be national standards for gasoline instead of each state setting its own rules. This, they say, would make the refiner’s job a lot easier.

In a way, they’re all right – and wrong at the same time. The point of this article, however, is not to assign blame, but to present some very relevant information and let you draw your own conclusions. The list of issues is by no means a complete one by any stretch and I’ll say in advance that, in terms of analysis, the data relied upon is provided by the US Energy Department. Aside from the reality of prices, there is really no way to either back check or verify their data.

Analysis – Supply and Demand or ‘Other Factors’?

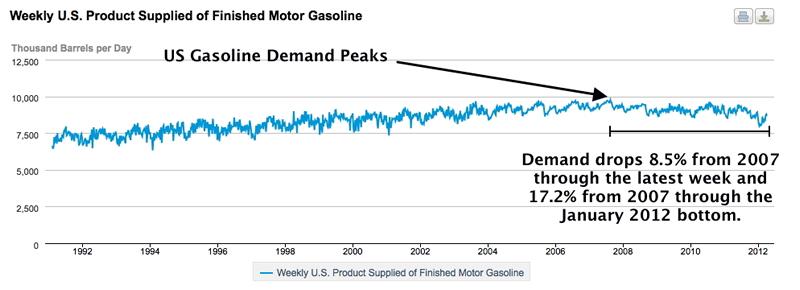

The chart below shows the number of barrels of finished motor gasoline supplied per day in the United States. The data is by the week. Since reaching a peak of 9.688 million barrels per day (mbpd) during the week of 7/27/07, gasoline demand has dropped to 8.861 mbpd during the most recent week for which there is data (4/6/12). Demand bottomed at 8.018 mbpd during the week of 1/27/12. In percentage terms, demand for finished gasoline has dropped 8.5% from the 2007 peak through the present, and 17.2% from the 2007 peak through the January 2012 bottom.

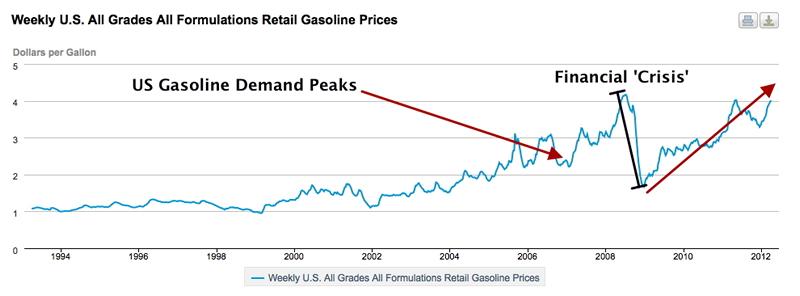

The next chart is basically an overlay covering essentially the same period of time. Prices were all over the place while demand slowly but steadily grew into 2007, peaked at 9.688 mbpd during the week of 7/27/07, and has been trending downward ever since. This pretty much eliminates increasing US demand as the culprit for rising prices. Unfortunately for us the market for gasoline, like most commodities, is now global. This is where the story becomes rather sad.

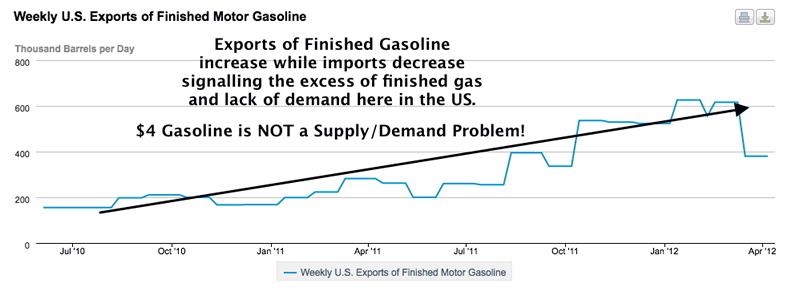

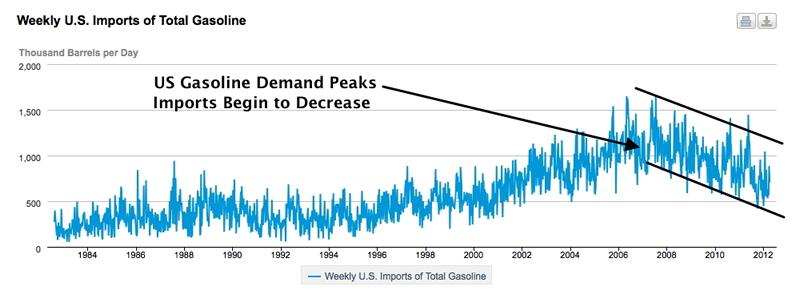

The charts below show the ‘movement’ of gasoline products. Most Americans do not realize that we actually export a good deal of finished gasoline, while simultaneously importing the same. Certainly many of these decisions are made at the corporate level, but as a national policy ‘theme’, it certainly seems silly to import something, use less and less of it domestically, then have enough to export while at the same time consumers are being crushed by near-record level prices.

Many economists cited demand destruction as the reason prices fell after peaking in 2008, and while this may be true, demand certainly didn’t pick up, even when the average price was cut by more than half. Remember, not too long ago, we were paying less than $2/gallon. So the price has more than doubled, while demand continues to fall. Many folks might use this reality to make the case that there is absolutely no sense to economics and that supply and demand ‘laws’ aren’t really laws but theories and cannot be taken seriously.

Rather to the contrary, I believe it is more important to use this situation to impress upon readers that there are numerous factors involved in setting prices, many of which were previously mentioned in this piece. Unfortunately, this is only part of the story; it gets even worse.

Refining Capabilities

Many individuals will be quick to point out that America hasn’t built a refinery in several decades. When we built our last refinery really doesn’t matter at this point. What is important is that the stage is set for America to actually lose refining capacity – and it is already happening.

Earlier this week there was an excellent article in the Financial Times that got some play in the US media, but not nearly enough. It asserted that the East Coast of the US is set to lose roughly half of its refining capacity. Here are some of the details:

-Sunoco has already scuttled two refineries and indicated it will close a third by July of this year if a buyer is not found.

-Sunoco has lost $1 billion over the past three years at its East Coast refineries.

-Conoco-Phillips is trying to sell a refinery in Philadelphia that has been sitting idle since last year.

-More than 3 mbpd of refining capacity has been lost in Western nations since the financial crisis back in 2008.

-Emerging economies have added 4.2 mbpd of refining capacity since the crisis with another 1.8 mbpd coming online this year. This factoid would help to make the argument that we are likely to be importing more gasoline in the years to come instead of becoming more independent.

-Europe’s largest refiner, PetroPlus, has filed for bankruptcy and is currently seeking buyers for five of its plants.

Sunoco’s dilemma with its Marcus Hook refinery in the southeastern corner of Pennsylvania is representative of some of the logistical issues facing domestic refiners. The Marcus Hook refinery relied largely on oil from Nigeria, Norway, and Azerbaijan. Nigerian crude is some of the finest quality in the world and for nearly all of 2011, the price of a barrel of Nigerian Crude (called Qua Iboe) averaged around $114/barrel, more than a barrel of refined gasoline, making the refining of this product a loser. Meanwhile, West Texas Intermediate Crude averaged $95/bbl during 2011, but Sunoco had no cost-effective way to get the oil to PA, since there is no pipeline. And it is a real shame too since Texas’ oil production has actually increased by 25% over the past several years and topped a half billion barrels for the first time since 1998.

The battle over the Keystone XL pipeline would do nothing to help Marcus Hook either since it would connect the Alberta tar sands with Texas. And even if there was a second pipeline shuttled to the East Coast, Marcus Hook and many other refineries in that area are not designed or suitable for refining heavy, sour crude, but rather depend on the higher quality grades such as Qua Iboe for their refining activities.

Many are quick to blame conspiracies amongst the oil companies to fix prices, and while this may be true in some instances, Sunoco’s conundrum is certainly a legitimate one. The only options really would be for Sunoco to eat the loss and keep refining, essentially taking one for the team, or for the government to subsidize continued refining by making up for the loss. Unfortunately, this would have to be done by borrowing even more money from foreigners and/or the federal reserve.

The further loss of refining capacity (for whatever reason) is going to have serious ramifications on prices – unless demand continues to fall, which seems to be the consensus of the IMF among others. And even in the case of falling demand, we’ve already demonstrated that prices can still rise thanks to the complex factors already described.

The economic landscape is changing right before our eyes. The lack of pickup in demand for gasoline and oil in general in the United States is proof positive that the ‘recovery’ so eloquently talked about in the press and by politicians and central bankers is an absolute joke. Higher fuel efficiency and ethanol have been credited with the decrease in overall gas demand by the media, but high unemployment and stagnant consumer spending on a unit basis have certainly taken their toll as well. It is a well-known fact that vibrant, growing, and healthy economies use more oil unless they’ve been set up to use alternatives, which we, by and large, have not.

For several years now, corn-based ethanol has been touted as the magic bullet that will solve the gasoline crisis in America. Unfortunately, that too was a poorly thought out, half-baked solution and as a result, the country is littered with multi-million dollar ethanol plants, many of which have never been used. There is one 20 miles from where I sit and it has never produced a single gallon of ethanol.

The bottom line is that America has been talking for decades about energy independence, but there has never been a coherent plan for achieving it and sadly, that is still the case today. To make matters even worse, paper futures markets make it ridiculously easy for banks and hedge funds to get in on the action too and rake in billions off the backs of consumers the world over. We’ve always been told we should be happy because the Europeans pay twice as much for gas as we do. Even a cursory glance at that continent today should indicate we don’t want any part of the path they’ve taken, with regards to energy or anything else for that matter.

Several years ago, I pointed out that it would be unlikely that a serious economic recovery would occur here in the US due to the issues of peak oil (as well as poor policy decisions), and unfortunately, so far that thesis is intact. Yet that still hasn’t stopped gas prices from hitting $4/gallon and it would be my guess that before too long, Americans will be comfortable with it and anything less will be considered ‘cheap’. Regrettably, other than restructuring our lives to reflect this new reality, there is little we as consumers can do about this one.

By Andy Sutton

http://www.my2centsonline.com

Andy Sutton holds a MBA with Honors in Economics from Moravian College and is a member of Omicron Delta Epsilon International Honor Society in Economics. His firm, Sutton & Associates, LLC currently provides financial planning services to a growing book of clients using a conservative approach aimed at accumulating high quality, income producing assets while providing protection against a falling dollar. For more information visit www.suttonfinance.net

Andy Sutton Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.