Socialization of the G7 Banking System and Food Crisis Horror Story

Interest-Rates / Credit Crisis 2008 May 09, 2008 - 10:39 AM GMTBy: Ty_Andros

In today's missive we are going to cover the creeping socialization of the G7 banking system and the second act of the horror show known as biofuels. Slowly but surely, the central banks of the G7 are taking over the short term funding needs of the money center and investment banking industries. The march is set to accelerate as the income streams dive as outlined in the Tedbits 2008 Outlook (Wolf Wave at www.TraderView.com ).

In today's missive we are going to cover the creeping socialization of the G7 banking system and the second act of the horror show known as biofuels. Slowly but surely, the central banks of the G7 are taking over the short term funding needs of the money center and investment banking industries. The march is set to accelerate as the income streams dive as outlined in the Tedbits 2008 Outlook (Wolf Wave at www.TraderView.com ).

In the second piece we will be covering the unfolding debacle known as biofuels versus food, and the impacts about to unfold in the grain markets. They are set to be quite dramatic. There is no escape from the math. The food price and availability crisis is about to get a whole lot worse .

Confusion reigns supreme as the forces of darkness, embodied by the mainstream press and public servants, are set to blow the public to and fro in a gigantic game of Pin the Tail on the Donkey and the politics of FEAR (false evidence appearing real). The mobs are set and ready to lynch the bad guys. Unfortunately, the bad guys are their elected leaders.

Markets are active, creating huge opportunities for the prepared investor. “Volatility is Opportunity ” and there is going to be a lot more of it. The macro themes that have brought us to this juncture are still in place and set to continue. Countertrend pops are rotating from sector to sector and throwing the dumbest among us off the bandwagon. Don't be fooled by the headlines. The solons of Wall Street are DESPERATE and the misinformation they are doling out is extraordinary. The death of paper castles continues.

Two big headlines used to fool you this week were 1 st quarter GDP and the monthly payroll report . Both reports were “messaged” to create false impressions for the headlines. These illusions are by public servants and the media meant to keep the public docile, peaceful and MIS-INFORMED!

In the case of the employment report, John Williams of www.shadowstats.com reports that if the distortions that are plainly seen in the birth/death estimates are removed unemployment shrank by an incredible 277,000 workers. Continuing claims soared above the 3,000,000 mark. In the case of the GDP numbers, John reports that many of the component numbers appeared to be plucked out of thin air. These numbers ran contrary to other economic reports compiled by the same department of the government. Insert the numbers from the other reports and the GDP DECLINED by approximately 2.7%.

The Pinocchio —er, Bush administration and the current gang of 545 in Congress are certainly as immoral, incompetent, and dishonest as any in history and the public is too stupid to see the truth.

Socialization of the G7 Banking System

The rescue of Bear Stearns was a seminal event as it indicated the length to which the financial and political authorities will act to insure the financial system. As this newsletter has said from the very beginning: THEY WILL PRINT THE MONEY. They will do whatever it takes. The central banks may try to hide the fact that they are taking the crappy paper and lending against it but that is the bottom line. The securitized markets for CDO's, CLO's, MBS etc. are severely impaired and the G7 central banks have substituted themselves in one form or another as funders of last resort. As lending conditions for more traditional bonds and stocks have begun to ease banks have rushed to market hundreds of billions of dollars in long-term obligations to bolster their balance sheets. The banks are impairing the future earnings of their shareholders in exchange for guaranteed locked-in funds for up to 10 years. They are paying top dollar for non- callable debt provisions, as the public will no longer fund them.

The rescue of Bear Stearns was a seminal event as it indicated the length to which the financial and political authorities will act to insure the financial system. As this newsletter has said from the very beginning: THEY WILL PRINT THE MONEY. They will do whatever it takes. The central banks may try to hide the fact that they are taking the crappy paper and lending against it but that is the bottom line. The securitized markets for CDO's, CLO's, MBS etc. are severely impaired and the G7 central banks have substituted themselves in one form or another as funders of last resort. As lending conditions for more traditional bonds and stocks have begun to ease banks have rushed to market hundreds of billions of dollars in long-term obligations to bolster their balance sheets. The banks are impairing the future earnings of their shareholders in exchange for guaranteed locked-in funds for up to 10 years. They are paying top dollar for non- callable debt provisions, as the public will no longer fund them.

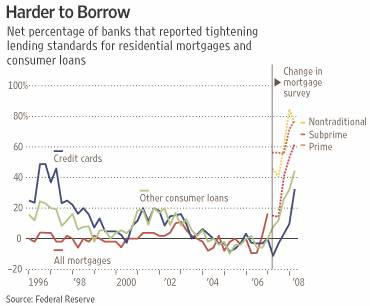

Last Friday the Federal Reserve expanded the term auction and funding facilities they have created so far, increasing them by 50 to 100%. At the same time, the Fed widened the definition of crappy paper they will take to include auto, credit card and student loans. There are sub prime elements in all categories of lending. The lending market for student loans has virtually disappeared, and is constricting for autos and unsecured credit card debt. Take a look at the above chart showing the new funding structures which have been implemented to replace those that have disappeared for the banking and financial system

The Bank of England has created a $100 billion dollar facility of its own to backstop the banks. The European Central Bank has not lowered rates but they have created facilities to swap impaired crappy paper assets for government issued bonds in amounts exceeding $500 billion dollars . Banks can no longer fund themselves through the short-term asset backed money markets.

This had to be done to “Protect the Public” from the irresponsibility of the INSOLVENT banking sectors in which they reside. Anything other then this course of action would have resulted in a deflationary depression and widespread bank failures.

The G7 central banks in question would like to believe this is only going to last for a short while (1 month to a year), but I believe 5 years from now they will still be around and bigger then ever. Interest rates are profoundly NEGATIVE throughout the world . Nominally they are positive after true inflation they are paying people to borrow money.

In the developed world where growth is at a standstill and income is declining, they can never be normalized again until the “crack up boom” runs its course over the next several decades. The real economy is about to get a kick in the pants as bankers on all levels of the banking system raise lending standards for EVERYBODY. Take a look at this chart of tightening lending standards:

There is no corner of the lending industry which is not toughening up borrowing requirements. This is a picture of the credit crunch rolling into the real economy. Bernanke is urging Congress to bail out homeowners and Congress is begging Bernanke to start buying securitized student loans. More reflationary policies loom in the near future. The helicopters are in flight looking for pockets of instability into which to drop money. Last week's helicopter drop by the Fed was a quick reversal of the HAWKISH Fed statement. Do you believe anything they say? I hope you don't. Just look at their actions and you will know the truth. They are printing the money out of thin air!

There is no corner of the lending industry which is not toughening up borrowing requirements. This is a picture of the credit crunch rolling into the real economy. Bernanke is urging Congress to bail out homeowners and Congress is begging Bernanke to start buying securitized student loans. More reflationary policies loom in the near future. The helicopters are in flight looking for pockets of instability into which to drop money. Last week's helicopter drop by the Fed was a quick reversal of the HAWKISH Fed statement. Do you believe anything they say? I hope you don't. Just look at their actions and you will know the truth. They are printing the money out of thin air!

In the emerging world, where growth and wealth generation is robust, these negative interest rates are overstimulating their economies. The currency pegs will fall sooner or later.

There is a dirty little secret no one is talking about. Private direct investment into the United States has come to a standstill. The external current account and budget deficits are now being financed by foreign central banks almost exclusively . The US is living on the grace of foreign central bankers. They are rightly defending the value of their foreign reserves denominated in dollars and they have trillions and trillions of them to defend.

Yields will have to rise and the dollar will have to fall further to create the incentive of higher returns so foreign direct investment will resume. The return on investment in the US has fallen to the point where VERY FEW will send investment dollars here . Investment returns must rise to the point where greed will overcome fear in the minds of foreign private investors. The dollar may correct higher but a move lower is more probable. As a note to the future you can expect the dollar index to decline to 50 in the coming years.

Fannie Mae just announced another multi-billion dollar loss and announced another $6 billion dollar round of capital raising. You can expect them and Freddie Mac to have to raise 50 to 100 billion before it is over as their solvency rests on accounting FICTIONS. The solvency of the G7 banking system rests on accounting FICTIONS as well. Recent reports about HUGE pension fund losses in SIV's, conduits and securitized debt known as CLO's, MBS, CLO's, etc. are now just beginning to surface. You will not believe the funding problems surfacing in the state and municipal governments as boom time budgets are challenged by the unfolding bust in the G7 economies.

The reflation of the banking system and economies has just begun. As G7 central bankers work to preserve their financial and banking systems, support the deficit spending and declining revenues through FIAT currency and credit creation you can expect inflation to run away to the upside. Bottom line: Any investment consisting of paper is extremely hazardous to your investing health….

Horror Story

If you think the prices of wheat and rice were overdone you haven't seen anything yet. Whenever public servants dream up some scheme to protect you the result is predictable: the problem is never solved and the cost is always multiples of what was projected. Vast new industries which are not economically justified become PERMANENT beneficiaries of government and taxpayer subsidies. There are permanent distortions of supply and demand, and that is where we are at in the US and EU. In the original Fingers of Instability in March 2007 (See Tedbits archives at www.Traderview.com ) we wrote about ethanol and the dangers to worldwide food supplies at that time. IT HAS ALL COME TRUE. Corn was priced in the mid $3 dollar range and now is above $6.

Biofuels and corn based ethanol have caused food prices to increase 30 to 100% depending on which food item you are looking at. The US and EU mandated biofuels use has already cost everyone plenty, but recently passed energy bills and pending farm legislation guarantee the future costs are about to skyrocket.

Biofuels and corn based ethanol have caused food prices to increase 30 to 100% depending on which food item you are looking at. The US and EU mandated biofuels use has already cost everyone plenty, but recently passed energy bills and pending farm legislation guarantee the future costs are about to skyrocket.

The EU commissioner in charge of agricultural subsidies and biofuels was interviewed in a recent Financial Times article and was asked whether a change of policy would be considered. His answer: Let me make it very simple for you. NO! This man obviously understands who his masters are and they are not the public. It is the elite insiders profiting from the policies.

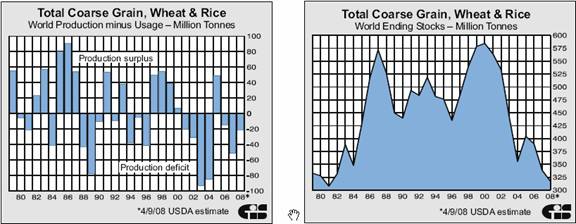

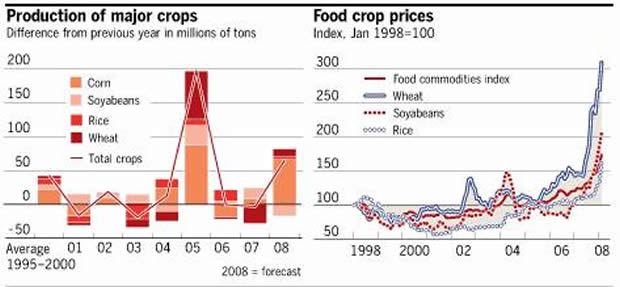

The world has consumed more coarse grains (wheat, rice, corn and soybeans) then it has produced for 7 of the last 8 years. The scattered recovery of grain production this year is also going to be in deficit. Take a look at these charts courtesy of Bill Gary ( www.cis-okc.com , P.S. Bill writes some of the best commentary on the agriculture market anywhere and has been doing so for 3 decades. I urge you to subscribe. I know I do):

Lowest supplies since 1982. What do you think demand has done since then? Moved sideways? Hardly. A bubble? No. There are virtually no reserves of any of the coarse grains anywhere in the world. And public servants are making things exponentially worse. Tariffs, import and export restrictions and price controls are all combining to make sure that the producer's increases in incomes necessary to fuel more production is ABSENT. Their costs have now gone up massively and their income DID NOT. Do you think they are going to increase costs and production when they have no chance of additional income? Unfortunately for economically challenged public servants the answer is NO.

When the planting intentions for corn and soybeans where released in early April there were not enough acres allocated to corn to meet the needs of the U.S. for ethanol, exports and food use in the coming year. China is also drawing down reserves quickly and supplies are tight. In addition there was not enough “OLD CROP” corn to get to the new crop due to record exports. Prices needed to rise in order to meet the requirements--almost 2,000,000 million additional acres for use in the coming year and ration use till the new crop arrived. Everything had to go perfect for the requirements to be met. Prices have risen, but Mother Nature has not cooperated.

Look at this explanation of the problems in the Corn Belt by Kent Lachner, a longtime former resident of Iowa and multi-decade farmer, now retired:

“This spring is very troubling with unrelenting adverse weather conditions. It is cold and wet with the soil temperatures hovering around 48 degrees now on the first of May and well below the needed corn germination temperature of 56 degrees. Two factors determine planting time: soil temperatures and moisture. Large operations need to begin planting probably a little too early, gambling that it will warm up IF we can even get into the fields.

Light sandy loam soils have seen minimal fieldwork while medium to heavy soils have yet to even begin, and the forecast here is possible snow and up to another inch of rain. This causes farmers sleep disorders! There is a limit as to what even large equipment can do when it is wet. Too often, it is tempting to “mud it in” and pay potential yields later due to severe compaction problems. Compaction absolutely causes shallow root systems that are vulnerable to earlier heat stress midsummer and difficulty holding adequate rain when it does occur.

Delayed planting, which has already occurred, invites late pollination usually in the brunt of the summer heat. This most often is a yield cutter. Late planting (after May 11 th depending on the soil type) will cut into yields at about 2% a day and increasing dramatically more after a week to ten days. This cascades into the corn crop being much more vulnerable to hot pollination time and early to normal fall freeze that cuts the test weight of the corn.

The next 8 days are EXTREMELY critical. A good week and most of the crop can be planted in the best of conditions. Driving around wet spots is not ideal and that is already guaranteed to be the case. No work has been done in heavier soils that are the best producing ground. Intended corn acres are down from about 91 million to 87 million, and the yields are already in jeopardy coming out of the gate. Any heat stress, lack of moisture later or early frost will only assure decreased yields. I do not expect to enjoy a bumper crop but would be grateful if it was even normal, which I am pessimistic with at this juncture. Mother Nature will have to be 100% kind (not likely) here on out to expect a normal crop this year”

Thank you , Kent , for these valuable insights into the unfolding problems. Rotating into soybeans is not an easy task as the press would have you believe as the farmers already have their corn seeds and fertilizer and they are very expensive. It's not really easy to load up the seed and fertilizer and go back to the seed distributors and exchange them for soybean seeds. In fact, it is VERY DIFFICULT to do so.

Thank you , Kent , for these valuable insights into the unfolding problems. Rotating into soybeans is not an easy task as the press would have you believe as the farmers already have their corn seeds and fertilizer and they are very expensive. It's not really easy to load up the seed and fertilizer and go back to the seed distributors and exchange them for soybean seeds. In fact, it is VERY DIFFICULT to do so.

The corn crop is still mostly unplanted due to wet and cold conditions throughout the Corn Belt . The forecast for the next week is for more of the same. If it materializes our worse fears about runaway grain prices will be front and center. Not only will there not be an additional 2,000,000 acres planted but the previous intentions are not going to be met: probably by a large margin .

Analysts contend that this will rotate into soybeans and create surpluses, but you cannot count on this, as US exports have been record large due to export tariffs in Argentina . Socialist President Christina Kirschner is trying to confiscate the earnings of farmers exporting soybeans by imposing an export tax of 44% so they have refused to export them.

Above is a picture of an emerging socialist dictator doing what all dictators do, exploding in rage as people refuse to be controlled and robbed by them (thank you Dennis at www.thegartmanletter.com for the photo) of their production and labor. She will control them at the end of a gun before this crisis has past. Rule by force as is done by governments around the globe. Argentina has gone from a basket case courtesy of the IMF (International monetary fund) five years ago into the hands of a populous dictatorship. Talk about fearsome masters—this country has had them in spades.

Myanmar has just suffered a typhoon and its sizable amounts of export rice have been literally BLOWN away. Kazakhstan , which formally was one of the largest exporters of wheat has now become a hoarder and exports have STOPPED. Russia has imposed 40% tariffs on wheat exports. Ukraine has wheat export quotas and Vietnam has stopped rice exports. Egypt , Syria , India and many others are distorting their markets in one government mandated way or another, disrupting food production and international distribution. Price controls, export controls, taxes and tariffs, introducing government distortion upon government distortion so the price mechanisms of the marketplace DON'T WORK. THIS SHORT-CIRCUITS THE PRICES THAT SPUR MORE PRODUCTION AND ALEVIATE SHORTAGES. So they won't be alleviated!

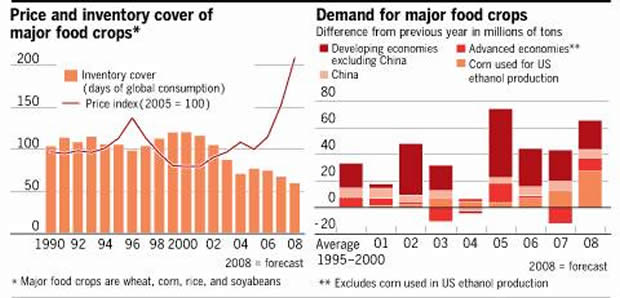

Worldwide inventories of all major food grains have declined now for almost a decade while demand has relentlessly rocketed forward as illustrated in this chart in a recent Financial Times :

If the emerging world just eats two more meals a week demand moves off the charts and they are going to do so as they have the money.

Because of biofuels, each planting year is like a game of musical chairs. When the music stops one grain or another does not have the acres necessary to meet current demand so it moves farther into deficit and inventories are reduced. Just in time inventory techniques are now a thing of the past, as if you wait too long you DO NOT get your grain supplies. Skyrocketing prices—like wheat last year when it tripled and rice recently—are only a harbinger of things to come as one critical crop or another goes through shortages. And when crops are plentiful, look for governments to quickly rebuild reserves to avoid future problems. When corn is expensive, industrial users switch to beans or wheat, when wheat is expensive users switch to corn or beans. Reserves never can accumulate due to substitution.

Rotating grain and food shortages will be a fixture now and for years to come. One of the greatest bull markets in history is front and center. Can you imagine the United States running out of corn? I believe it could happen this summer! But whatever happens, rice and wheat were no anomalies. You will see this happen over and over again in the coming years.

In conclusion: The pain at the checkout counter is set to increase. Your food bills are set to SKYROCKET all along the food chain, creating huge opportunities for prepared investors. No matter what CNBS tells you, nothing has changed in the commodity and natural resource sectors, and paper is not going to make a comeback anytime soon, especially U.S. denominated paper. Corrective activity happens, so learn to control risk better. If biofuels are cut back oil will go to 200 dollars in a heartbeat as it will fall into deficit. Biofuels have become a small but significant portion of global energy use, but in the big picture eliminating them will cause oil to fall into DEEP deficit of production versus rising demand. There is no excess production capacity in oil to substitute for the absence of the biofuels.

Commodities and oil were a dollar story for three decades as capacity was abundant. It is no longer so. Currencies don't float– they just sink at different rates: don't forget this. Commodities and natural resources are SCARCE and new production is far, far away. Supply is constrained and demand is increasing. Commodities ARE NOT a dollar story ANYMORE. The dollar does have an influence but it is steadily disappearing. Commodities and natural resources are rising against all currencies. Bubbles do not have supply constraints; in bubbles supply is abundant and overflowing like housing stocks and NASDAQ. And I don't mean a 90-day supply. Crude oil has to go high enough to make sure we have crude oil in 5 years or more.

Commodities and oil were a dollar story for three decades as capacity was abundant. It is no longer so. Currencies don't float– they just sink at different rates: don't forget this. Commodities and natural resources are SCARCE and new production is far, far away. Supply is constrained and demand is increasing. Commodities ARE NOT a dollar story ANYMORE. The dollar does have an influence but it is steadily disappearing. Commodities and natural resources are rising against all currencies. Bubbles do not have supply constraints; in bubbles supply is abundant and overflowing like housing stocks and NASDAQ. And I don't mean a 90-day supply. Crude oil has to go high enough to make sure we have crude oil in 5 years or more.

Volatility is opportunity and it is abundant as the public is not accustomed to trading commodities and the ETF's are poorly designed (just like about everything coming out of WALL STREET ). Stock brokers do not understand risk control so their customers buy highs and sell lows. Crude is headed quickly to $130 dollars a barrel; take a look at this little crude chart, this pattern signals/projects the move which is $10 dollars higher:

Next week we are doing a commentary on the oil market and it is a frightening picture of public servant and government malfeasance. So get your portfolio ready to capture the opportunity from this epic move that is unfolding. This will push many other markets in big moves and remember: For a prepared investor “Volatility is Opportunity ” so as the boy scouts say “Be Prepared”.

Thank you for reading Tedbits if you enjoyed it send it to a friend and subscribe its free at www.TraderView.com don't miss the next edition of Tedbits.

If you enjoyed this edition of Tedbits then subscribe – it's free , and we ask you to send it to a friend and visit our archives for additional insights from previous editions, lively thoughts, and our guest commentaries. Tedbits is a weekly publication.

By Ty Andros

TraderView

Copyright © 2008 Ty Andros

Hi, my name is Ty Andros and I would like the chance to show you how to capture the opportunities discussed in this commentary. Click here and I will prepare a complimentary, no-obligation, custom-tailored set of portfolio recommendations designed to specifically meet your investment needs . Thank you. Ty can be reached at: tyandros@TraderView.com or at +1.312.338.7800

Tedbits is authored by Theodore "Ty" Andros , and is registered with TraderView, a registered CTA (Commodity Trading Advisor) and Global Asset Advisors (Introducing Broker). TraderView is a managed futures and alternative investment boutique. Mr. Andros began his commodity career in the early 1980's and became a managed futures specialist beginning in 1985. Mr. Andros duties include marketing, sales, and portfolio selection and monitoring, customer relations and all aspects required in building a successful managed futures and alternative investment brokerage service. Mr. Andros attended the University of San Di ego , and the University of Miami , majoring in Marketing, Economics and Business Administration. He began his career as a broker in 1983, and has worked his way to the creation of TraderView. Mr. Andros is active in Economic analysis and brings this information and analysis to his clients on a regular basis, creating investment portfolios designed to capture these unfolding opportunities as the emerge. Ty prides himself on his personal preparation for the markets as they unfold and his ability to take this information and build professionally managed portfolios. Developing a loyal clientele.

Disclaimer - This report may include information obtained from sources believed to be reliable and accurate as of the date of this publication, but no independent verification has been made to ensure its accuracy or completeness. Opinions expressed are subject to change without notice. This report is not a request to engage in any transaction involving the purchase or sale of futures contracts or options on futures. There is a substantial risk of loss associated with trading futures, foreign exchange, and options on futures. This letter is not intended as investment advice, and its use in any respect is entirely the responsibility of the user. Past performance is never a guarantee of future results.

Ty Andros Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.