Zero Interest Rates, Plunging Bond Yields, Slumping Oil Price, Stocks Santa Rally?

Stock-Markets / Financial Markets Dec 21, 2008 - 11:09 AM GMT

“Americans have always been able to handle austerity and even adversity. Prosperity [greed!] is what is doing us in,” said James Reston , former New York Times journalist and Pulitzer Prize winner.

“Americans have always been able to handle austerity and even adversity. Prosperity [greed!] is what is doing us in,” said James Reston , former New York Times journalist and Pulitzer Prize winner.

Another chapter in dealing with the current credit and economic adversity was written on Tuesday when the US Federal Reserve announced a no-holds-barred set of measures in a determined attempt to fix the broken credit machine, revive economic activity and stem the deflationary tide.

The Federal Open Market Committee's (FOMC) policy statement noted: “The Fed will employ all available tools to promote the resumption of sustainable economic growth … In particular, the Committee anticipates that weak economic conditions are likely to warrant exceptionally low levels of the Fed funds rate for some time.”

Although the FOMC slashed the Fed funds rate to a target range of 0 to 0.25% – the lowest the central bank's key rate has been on record – the Fed was actually simply aligning its target rate with the effective rate, thereby pushing the US into an era of Zirp – a zero-interest-rate policy like that used by Japan for six years in its own fight against deflation.

The Fed's communiqué also said: “The focus of the Committee's policy going forward will be to support the functioning of financial markets and stimulate the economy through open market operations and other measures that sustain the size of the Federal Reserve's balance sheet at a high level.” The statement discussed specific actions that would move the Fed further towards a quantitative easing approach to monetary policy.

Source: Daryl Cagle

President-elect Barack Obama told reporters the fact that the Fed had no more room to cut rates underscored the case for a big fiscal stimulus. “We are running out of the traditional ammunition that's used in a recession, which is to lower interest rates,” he said according to the Financial Times . Word circulated that Obama may ask Congress next year to approve a stimulus plan of about $850 million.

Investors' concerns about the outlook for the global economy deepened on the back of the Fed's announcement, as seen from government bond yields plunging to record lows and a sharp sell-off in oil prices (despite the announcement of the largest supply cut in Opec's history). Furthermore, the dollar also tumbled on worries about the US's public debt expansion and the potential inflationary implications of the “printing press”, although a relief rally did take place on Friday. (Also see my post “ Greenback slumped on the canvas ”.)

As far as stock markets are concerned, investors have again been shrugging off bad news – a pattern seen since the poor manufacturing and payrolls data of more than two weeks ago. “The newspapers may be giving us a parade of bad news, but the stock market is beginning to march to a different drummer,” said venerable newsletter writer Richard Russell ( Dow Theory Letters ). This is evidenced from the MSCI World Index (+2.4%), S&P 500 Index (+0.9%) and the MSCI Emerging Markets Index (+5.5%) all improving for a second week running.

The scamster Bernard Madoff's Ponzi scheme also vied for a place in the history books, causing more billions to evaporate to money heaven – yet another example of how greed clouded the minds of people during the halcyon days. (Click here to track the fallout from the fraud.)

Bill King ( The King Report ), never one to mince his words, commented as follows: “Madoff allegedly engaged in a scheme that is similar to what the US government has been perpetrating for years – giving people benefits now and promising future benefits, even though the benefits are mathematically impossible to pay, by using new cash flows from taxpayers.”

On the bailout front, the White House gave Detroit their Christmas wish, announcing that General Motors (GM) and Chrysler will receive $13.4 billion in emergency government loans in exchange for substantially restructuring their businesses, according to Bloomberg . “Another $4 billion will be available to GM in February provided Congress releases the second half of the $700 billion TARP fund originally set up to bail out financial institutions.”

Some cheer has also been seen in the credit markets, with the TED spread (i.e. three-month dollar LIBOR less three-month Treasury Bills) declining by 43 basis points to 1.48% – the lowest level since the Lehman bankruptcy in September. Although this measure is moving in the right direction, credit spreads need to narrow further to indicate that confidence is returning and liquidity is starting to move freely again.

The cost of buying credit insurance for US and European companies also eased as shown by the narrower spreads for both the CDX (North America, investment grade) Index (down from 263 to 213) and the Markit iTraxx Europe Index (down from 214 to 191). High-yield credit indices also improved.

There is also some encouragement from the weekly average rates for US 30-year fixed mortgages having declined to 4.94% from 6.30% at the beginning of November, according to Zillow.com .

Next, a tag cloud from the dozens of articles I have read during the past week. This is a way of visualizing word frequencies at a glance. The key words include the usual suspects such as “bank”, “economy”, “Fed”, “market”, “prices” and “rate”.

Regarding the outlook for the stock market, the Wall Street Journal's MarketBeat blog reported legendary money manager Jeremy Grantham as predicting that beaten-down equities will rally until spring, at which time the bear market will resume.

“While he said that equities in the last couple of months had reached a level of cheapness than had not been seen in years, he still expects more pain to come. Those who can invest with a seven-year time horizon should do well, saying that ‘we've popped all of the bigger bubbles', but he expects ‘we'll overrun on the downside'.

“He says that the market will likely continue to rally into the spring, and it ‘will be big enough to convince about three-quarters of the players that [the bear market] is all over'. However, he doesn't believe it is over – expecting a ‘good rally and a different kind of decline, on the sheer grinding of bad news'. He expects something similar to 1974, where the market takes a step forward and a couple steps back, and is fed ‘a diet of ugly earnings'.”

From across the pond, David Fuller ( Fullermoney ) added: “… markets had fallen sufficiently so that one could nibble on weakness, taking a long-term view. My guess is that China has not only bottomed but is also leading the way back up. However the case is not proven, and will not be until we see base formations for China and most other markets, plus breaks above the 200-day moving averages, which have also turned up. At that point, the next bull market should be well under way.”

The S&P 500 could fall to as low as 600 in 2009 and “alternative assets” like commodities and currencies will provide no shelter for investors, said Gary Shilling in an interview on Tech Ticker (hat tip: Clusterstock ). “Having been appropriately bearish heading into this year, Shilling sees ‘few good places to hide' in 2009. His ‘S&P 600' prediction, a 33% drop from current levels, is based on a view that S&P earnings will be $40 per share next year (versus the consensus of $83) and the index will trade at a P/E multiple of 15. (Here's the math: $40 EPS x 15 P/E = 600.)”

Jeffrey Hirsch ( Stock Trader's Almanac ) draws our attention to the so-called Santa Claus Rally. This is the trading period from the day after Christmas to the close of the second trading day of the New Year. During this period stocks historically tended to advance, but when recording a loss, it was frequently a sign of trouble ahead.

In my opinion, stock markets are still caught between the actions of central banks pulling out all stops to stabilize the financial and economic situation on the one hand, and a worsening economic and corporate picture on the other. The major US indices seem locked in a short-term trading range, having fallen back below their 50-day moving averages.

The CBOE Volatility Index ( VIX) has declined from more than 80 in October and November to 44.9 on Friday. It is not uncommon for short-term volatility to be at extreme levels at bottom turning points, and for stocks to improve as the “storm” grows quieter. It nevertheless remains too early to tell whether a secular stock market low has been recorded on November 20 and, failing further technical and fundamental evidence, I remain distrustful of rallies. In short, we are in a wait-and-see mode. (Also see my post “ Stock markets: is this it? ”.)

Economy

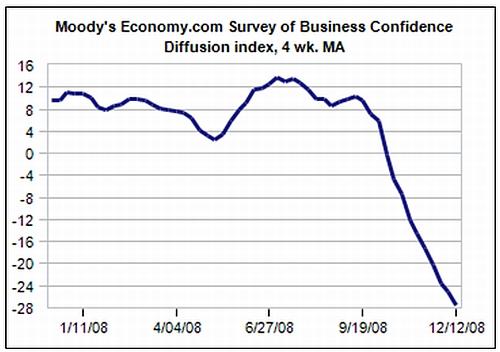

“Global business confidence continues to slide, falling to another new record low last week. Sentiment is equally negative in North America, South America and Europe, and while Asian business confidence is not quite as dark, it is weakening rapidly,” said the latest Survey of Business Confidence of the World conducted by Moody's Economy.com . The Survey results indicate that the entire global economy is mired in recession.

Economic reports released in the US during the past week confirmed a world of “depression economics” (to coin Nobel Prize winner Paul Krugman's phrase). According to Briefing.com, industrial production declined by 0.6% in November, housing starts plummeted by 18.9% (marking the largest decline since March 1984), building permits hit a record low, and weekly initial jobless claims held near a 26-year high. Furthermore, the seasonally unadjusted CPI fell 1.9% in November, the largest drop since the 1930s.

Elsewhere in the world, data releases compounded anxiety about a severe global recession, as seen from the following:

• Germany's Ifo Business Climate Index fell to a record low in December. The outcome reflects the ongoing stresses in the financial markets and weaker global and domestic economic activity, which have weighed on business sentiment. The downward trend in the Ifo suggests that economic activity in Germany will be very weak in the fourth quarter and prospects going forward remain bleak.

• BBC News reports that France will enter recession in the first quarter of 2009, according to Insee, the country's national statistics agency. France is the Eurozone's second biggest economy, and would be the latest major world economy to enter recession.

• The Bank of England's Monetary Policy Committee voted unanimously in favour of the decision to cut the main repo rate by 100 basis points to 2% at the December monetary policy meeting. However, the minutes revealed that the central bank had considered an even more aggressive interest rate cut, heightening expectations that the UK could follow the US in adopting a quantitative easing policy.

• Confidence among Japanese businesses capitulated during the fourth quarter, with the Tankan Survey Index for large manufacturers recording its biggest decline in more than three decades. Business sentiment in Japan is now at its lowest level in more than six years.

• The Bank of Japan followed the lead of the Fed and moved to a near-zero interest rate environment at its December monetary policy meeting. The central bank cut its overnight call rate target by 20 basis points to 0.10%.

• China's industrial production growth rose only 5.5% year-on-year in November, the slowest gain since 1999 and steeply slower than the 17% growth reported in March, said RGE . Electricity production fell 9.6% – more than in October, which had marked the first fall in a decade.

Source: Financial Times , December 16, 2008.

Summarizing the economic situation, Nouriel Roubini, professor at New York University and chairman of RGE , said in an article in Forbes : “The outlook for the US and the global economy is now very bleak and getting worse as the global economy experiences its worst recession in decades. In the US, recession started last December and will last at least 24 months until next December – the longest and deepest US recession since World War II, with the cumulative fall in gross domestic product possibly exceeding 5%.”

Week's economic reports

Click here for the week's economy in pictures, courtesy of Jake of EconomPic Data .

| Date | Time (ET) | Statistic | For | Actual | Briefing Forecast | Market Expects | Prior |

| Dec 15 | 8:30 AM | NY Empire State Index | Dec | -25.8 | -28.0 | -27.0 | -25.4 |

| Dec 15 | 9:00 AM | Net Foreign Purchases | Oct | $1.5B | NA | NA | $65.4B |

| Dec 15 | 9:15 AM | Capacity Utilization | Nov | 75.4% | 75.8% | 75.6% | 76.0% |

| Dec 15 | 9:15 AM | Industrial Production | Nov | -0.6% | -0.6% | -0.8% | 1.5% |

| Dec 16 | 8:30 AM | Building Permits | Nov | - | 700K | 700K | 708K |

| Dec 16 | 8:30 AM | Core CPI | Nov | 0.0% | 0.0% | 0.1% | -0.1% |

| Dec 16 | 8:30 AM | CPI | Nov | -1.7% | -1.5% | -1.3% | -1.0% |

| Dec 16 | 8:30 AM | Housing Starts | Nov | - | 725K | 730K | 791K |

| Dec 16 | 8:30 AM | Building Permits | Nov | 616K | 700K | 700K | 730K |

| Dec 16 | 8:30 AM | Housing Starts | Nov | 625K | 725K | 730K | 771K |

| Dec 16 | 2:15 PM | FOMC Policy Statement | - | - | - | - | - |

| Dec 17 | 10:35 AM | Crude Inventories | 12/13 | 525K | NA | NA | 392K |

| Dec 18 | 8:30 AM | Initial Claims | 12/13 | 554K | 550K | 558K | 575K |

| Dec 18 | 10:00 AM | Leading Indicators | Nov | -0.4% | -0.5% | -0.4% | -0.9% |

| Dec 18 | 10:00 AM | Philadelphia Fed | Dec | -32.9 | -35.0 | -40.5 | -39.3 |

Source: Yahoo Finance , December 19, 2008.

Next week's US economic highlights, courtesy of Northern Trust , include the following:

1. Real GDP (December 23): The final estimate of third-quarter Real GDP is expected to be left at -0.5%. Consensus : -0.5%.

2. Existing Sales (December 23): Consensus : 4.90 million versus 4.89 million in October.

3. New Home Sales (December 23): Consensus : 420,000 versus 433,000 in October.

4. Durable Goods Orders (December 24): Consensus : -3.0% versus -6.2% in October.

5. Personal Income and Spending (December 24): Consensus : Personal income +0.0% versus +0.3% in October; Consumer spending: -0.7% versus -1.0% in October.

Click here for a summary of Wachovia's weekly economic and financial commentary.

Markets

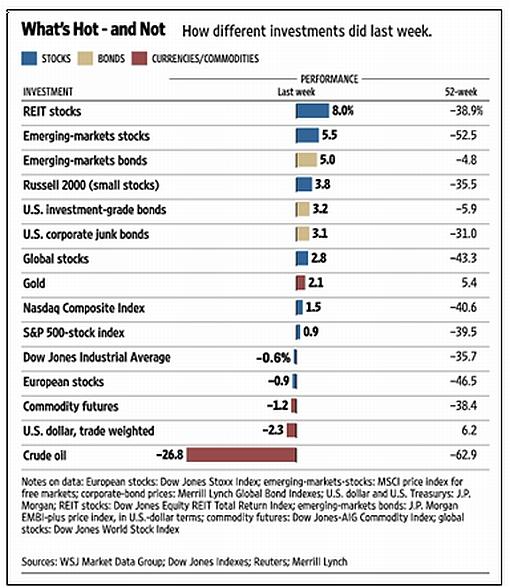

The performance chart obtained from the Wall Street Journal Online shows how different global markets performed during the past week.

Source: Wall Street Journal Online , December 19, 2008.

{kind=link}

This week I am giving the customary review of the various asset class movements a skip as family time calls, especially as we have just moved into a new house (located in the scenic Stellenbosch winelands region – about 35 minutes from Cape Town).

On a different note, Madoff's jeer at the investing public, keeps reminding me of the old adage: “If something sounds too good to be true, that must be because it is too good to be true.” Let's hope that the news items and words from the investment wise below will assist in bringing cheer to our portfolios during 2009.

Thank you for your friendship and support in making Investment Postcards such a fulfilling experience. Here's wishing you a great festive season full of fun, laughter and joy. May you have a wonderful 2009.

Source: Daryl Cagle

Krishna Guha (Financial Times): Fed slashes rates to near

“The Federal Reserve moved deeper into uncharted waters on Tuesday, heralding further unconventional measures to support the economy as it slashed interest rates from 1% to virtually zero.

“In a historic statement, the US central bank said it would target a record low interest rate, expressed as a range of between zero and 0.25%. It said it expected to keep rates at ultra-low levels ‘for some time' and vowed to use ‘all available tools to promote the resumption of sustainable growth and to preserve price stability'.

“The Fed said it ‘stands ready' to step up its planned purchases of securities issued by Fannie Mae and Freddie Mac, the mortgage giants now under government control. It also said it was ‘evaluating the potential benefits of purchasing longer-term Treasury securities'.

“The aggression of the statement caught the markets by surprise. Mohamed El-Erian, chief executive at Pimco, the bond fund manager, said it was ‘an incredibly strong public declaration that the Fed will throw everything it has in attempting to stabilize the financial and economic situation'.

“The US central bank laid out a strategy that aims to drive down actual borrowing costs for households and companies. It seeks to do so by supporting demand for such loans, reducing the risk spreads on them. At the same time, it wants to keep government bond yields low.

“This means expanded credit and outright asset purchase programs, likely to be funded, at least for now, by expanding reserves and therefore the money supply. Jan Hatzius, chief US economist at Goldman Sachs, called this ‘quantitative easing'. But a senior Fed official said its policy was different from the quantitative easing pursued in post-bubble Japan. The Fed policy is driven by its credit operations whereas Japan targeted bank reserves.

“The Fed said the outlook for economic activity had ‘weakened further' and acknowledged that ‘inflationary pressures have diminished appreciably'.

“The decision to set a range for interest rates reflects an admission that the US central bank cannot tightly control the actual rate that prevails in the market in current conditions.

“Barack Obama, president-elect, told reporters that the fact that the Fed had no more room to cut rates underscored the case for a big fiscal stimulus. ‘We are running out of the traditional ammunition that's used in a recession, which is to lower interest rates,' he said.”

Source: Krishna Guha, Financial Times , December 17, 2008.

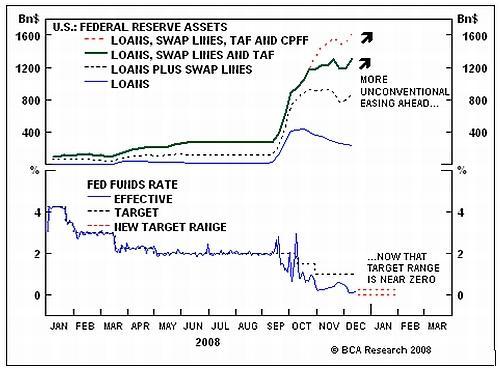

BCA Research: US monetary policy – unconventional easing underway

“The FOMC clearly crossed over the line into quantitative-easing territory by cutting the Fed funds target rate virtually to zero, promising to hold it low for a long period, and committing to large purchases of mortgage-related assets and possibly long-term Treasurys.

“In the statement that followed, the FOMC shifted emphasis away from the target rate as the Fed's primary means of implementing monetary easing in favor of aggressively expanding its balance sheet to drive private sector borrowing rates lower.

“Early clues to its latest thinking were provided late last month upon the launch of its agency and MBS purchase programs and Term Asset-Backed Liquidity Facility (TALF). At that time, it promised to increase the size, the scope and the term of its liquidity facilities as necessary to get credit markets moving again. These comments were echoed in the FOMC statement, which confirms the Fed is prepared to do whatever it takes to restore order to the financial system and head off a potentially damaging bout of deflation.

“The Fed will drive agency and agency-backed MBS yields lower, and will keep Treasurys well bid. If investment-grade corporate bond yields do not fall in the coming months, the Fed could add new facilities to support this market as well.”

Source: BCA Research , December 17, 2008.

Nouriel Roubini (Forbes): Helicopter Ben goes ZIRP!

“The Fed decision to cut the Fed Funds range to 0% to 0.25% has formalized the fact that, over the last month, the Fed had already moved to a zero-interest-rate policy, or ZIRP, and started a policy of quantitative easing (QE) as its balance sheet has surged over the last few months from $800 billion to over $2 trillion.

“The Fed is now undertaking even more unorthodox policy actions. These actions are occurring while the US and the global economy are at risk of a protracted bout of ‘stag-deflation' (stagnation and deflation).

“While it is now fashionable to talk about such deflationary risks (and the latest US Consumer Price Index figures confirm that we are entering into deflation), some of us were worrying about the coming deflation well before the mainstream – concerned with short-run and unsustainable increases in commodity prices – discovered the deflationary risks in the global economy.

“It was clear to those who saw, early on, the risks of a severe US and global recession, that deflationary rather than inflationary pressures would emerge alongside a slack in goods, labor and commodity markets. Welcome to the world of stag-deflation or, as Paul Krugman would put it, the world of ‘depression economics'.

So what is the outlook for 2009? And what is the likely policy response to the risks of a global stag-deflation?

“The outlook for the US and the global economy is now very bleak and getting worse as the global economy experiences its worst recession in decades. In the US, recession started last December and will last at least 24 months until next December – the longest and deepest US recession since World War II, with the cumulative fall in gross domestic product possibly exceeding 5%.”

Click here for the full article.

Source: Nouriel Roubini, Forbes , December 18, 2008.

John Authers (Financial Times): The Fed's morning after

“Markets expect the Bank of Japan to cut interest rats to zero; the Fed's decision has drastically undercut the dollar, oil prices continue to fall despite low rates, a week dollar and a cut in output.”

Click here for the article.

Source: John Authers, Financial Times , December 17, 2008.

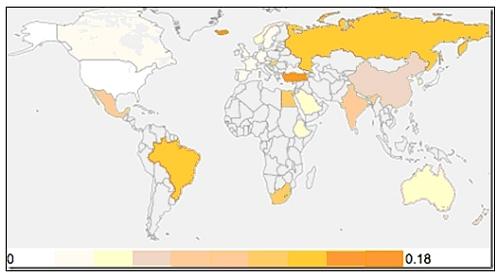

Paul Kedrosky (Infectious Greed): ZIRP-ishness around the world

“A quick-and-dirty chart of ZIRP-ishness – the degree to which countries' nominal interest rates are approaching zero – around the world. Note: The whiter the country the more ZIRP-ish it is, while the more orange you are the further that country's rate is from zero. Finally, gray means no rate data currently in the dataset.

“It is interesting how, for the most part, ZIRP neatly breaks down into the BRIC/emerging markets versus the rest of the world.”

Source: Paul Kedrosky, Infectious Greed , December 18, 2008.

Bloomberg: Obama may seek a stimulus plan exceeding $850 billion

“Barack Obama may ask Congress next year to approve a stimulus plan of around $850 billion, an amount that has grown as the US economy sinks deeper into recession, an adviser to the president-elect said.

“Obama's transition team believes the amount, about 6% of the US's $14 trillion economy, is needed to reverse rising unemployment, said the adviser, who spoke on condition of anonymity. The sum would exceed initial estimates by House Speaker Nancy Pelosi and Senate Majority Leader Harry Reid, as well as surpassing what some economists and the International Monetary Fund say is required.

“The latest proposal is circulating in Congress as Obama's advisers work with lawmakers to craft a package aimed at improving roads, bridges and other parts of the US's crumbling infrastructure. The plan probably will also include state aid for unemployment and health-care programs and incentives such as tax credits to promote renewable energy production, lawmakers have said.

“The president-elect wants to create as many as 2.5 million jobs over the next two years. As unemployment has increased, estimates of what is needed to pull the nation out of the slump have continued to grow, with some economists calling for a $1 trillion spending program.

“They include Kenneth Rogoff, a Harvard University professor who was an adviser to Republican presidential candidate John McCain, and Joseph Stiglitz, a Nobel Prize winner who served in President Bill Clinton's White House.

“UBS AG economists calculate a global stimulus of 1.5% of gross domestic product has so far been lined up for next year. The IMF has called for packages of at least 2% of GDP to stem the economic crisis that's sweeping the globe.”

Source: Lorraine Woellert, Bloomberg , December 18, 2008.

Bloomberg: $1 trillion stimulus

“Stimulus competition grows as companies vie for funds; Caterpillar wants a piece of the highway projects; GE is pushing to build an electric ‘smart grid'; Daimler AG hopes to build new buses for mass transit systems; Obama promises huge infrastructure investment.”

Source: Bloomberg (via YouTube ), December 18, 2009.

Bloomberg: GM and Chrysler will get $13.4 billion in loans

“General Motors and Chrysler will get $13.4 billion in emergency government loans in exchange for substantially restructuring their businesses, President George W. Bush announced.

“Another $4 billion will be available to GM in February provided Congress releases the second half of the $700 billion Troubled Asset Relief Program fund originally set up to bail out financial institutions. The automakers have until March 31 to meet the conditions of the loans, including demonstrating they have a plan to become profitable, or be forced to repay.

“Winning the assistance is a reprieve for GM, the biggest US automaker, and No. 3 Chrysler after they said they would run out of operating funds as soon as this month. Bush is stepping in after Senate Republicans' refusal last week to take up a House- approved rescue raised the prospect that the companies would fail, costing millions of jobs.

“‘These are not ordinary circumstances,' Bush said at the White House today. ‘In the midst of a financial crisis and a recession, allowing the US auto industry to collapse is not a responsible course of action.'

“The cost of letting automakers fail would lead to a 1% reduction in the growth of the US economy and mean about 1.1 million workers would lose their jobs, including those in the auto supply business and among dealers, the White House said in a fact sheet.

“President-elect Barack Obama endorsed the plan, calling it a ‘necessary step' to avoid a major blow to the economy.

“‘The auto companies must not squander this chance to reform bad management practices and begin the long-term restructuring that is absolutely required to save this critical industry,' Obama said in a statement.

“The United Auto Workers are ‘disappointed' that Bush added ‘unfair conditions singling out workers', the union's president, Ronald Gettelfinger, said in a statement. ‘We will work with the Obama administration and the new Congress to ensure that these unfair conditions are removed,' Gettelfinger said.

“The package is intended for GM and Chrysler initially. Ford Motor Co., the second-biggest US automaker, has said it can continue operating without aid for now.”

Source: Roger Runningen and John Hughes, Bloomberg , December 19, 2008.

Bloomberg: Fed becoming lender of last resort – interview with Merrill Lynch chief economist David Rosenberg

Source: Bloomberg (via YouTube ), December 17, 2008.

CNN Money: Economy rescue - adding up the dollars

“The government is engaged in an unprecedented - and expensive - effort to rescue the economy. Here are all the elements of the bailouts.”

Source: CNN Money , December 15, 2008.

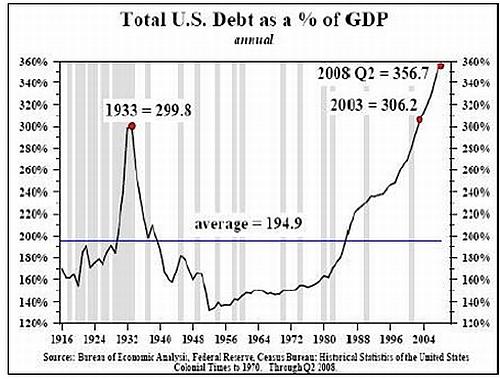

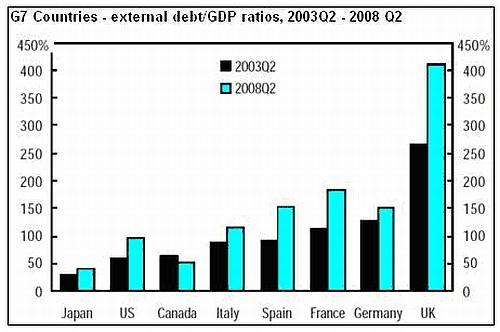

FT Alphaville: Welcome to debt central

“US total debt to GDP is beginning to worry a number of market commentators – even those previously convinced it wasn't a problem. Most recently, Dennis Gartman of the Gartman Letter, has turned jittery on the issue:

“‘We have never been given to wailing and gnashing our teeth over the US' growing debt, for during our nearly six decades of life and three and one half decades of trading in markets, we've seen the nation's debt grow even as the quality of life and wealth of the country grew faster. But now, even we are becoming concerned; now even we see potential disaster looming; now even we are depressed … Now even we are considering that double hemlock!'

“As can be seen in the chart below, the figure has certainly ballooned somewhat substantially of late.

“But Americans shouldn't feel too lonely. There's at least one other G7 country that can rival the States in the debt to GDP rankings. Have you guess which one it is? Some clues: Land of the Great British Krona, home to Team GB … Yes – it's the grand old United K. Just take a look at this chart from the Spectator.

“And that's not even total debt, just external.”

Source: Izabella Kaminska, FT Alphaville , December 12, 2008.

CEP News: Leading nations' GDP poised to decline in 2009

“US, Japan and euro zone GDPs are expected to decline in 2009, according to the Institute of International Finance (IIF) global economic forecast.

“The IIF forecast is calling for the US economy to decline by 1.3% after rising 1.2% this year, while the euro area economies are projected to decline by 0.9% in 2008 and 1.5% in 2009. Japan's economy is expected to fall by 1.2% after a flat performance this year.

“IIF Managing Director Charles Dallara said, ‘we now face extraordinary challenges. The extent of the declines in the major economies in the current quarter and in the next quarter or two may be substantial, with the US and the euro area likely to see falls in real GDP in the fourth quarter of this year of respectively 5% and 3%.'

“The IIF is also predicting the downturn in the major economies to impact the leading emerging-market economies. They project the growth in emerging markets to average 5.9% in 2008 and 3.1% in 2009. Weak growth is anticipated to hit central, eastern and southern Europe with growth of just 0.3% for 2009, while the IIF is forecasting growth in South America to come in at 1% next year.

“Overall, global economies are poised to grow 2.0% in 2008 and fall 0.4% in 2009.”

Source: Steve Stecyk, CEP News , December 18, 2008.

The Times: IMF fears unrest without action on economy

“Violent unrest may be sparked around the world by a prolonged global slump unless governments act with greater urgency to jump-start stalled economies, the head of the International Monetary Fund said on Monday.

“Dominique Strauss-Kahn sounded a stark warning over the consequences of what he argued was weak and uncertain government reaction to the economic crisis. He used a hard-hitting speech in Madrid to single out eurozone nations over what he attacked as an inadequate response.

“The broadside from the IMF's managing director came as fears over a protracted global recession, and political fallout, mounted after China said that its factories' output registered the weakest growth in almost a decade last month.”

Source: Gary Duncan, The Times , December 16, 2008.

George Magnus (Financial Times): Five ways to start the world economic recovery

“After the Minsky Moment – where euphoria tips into crisis, named after Hyman Minsky – the capitulation of economic activity has been rapid and severe. The outlook is as dark as the doomsayers assert. The only thing that stands between today's dire economic prospects and a lost decade similar to Japan's in the 1990s is the competence and authority of macroeconomic policy. We have a long way to go, but for five reasons, even doomsayers can start to feel the force, so to speak.

“First, governments have already acted decisively to preserve the integrity of the formal banking system, while the so-called shadow banking system is collapsing. Over $8,000 billion of programmes to stem the collapse in credit and housing have been announced but it is too soon to declare victory. To strengthen banks in the recession and sustain lending, European banks will need a further $100 billion to $150 billion of capital, while US banks, including regional banks, should quickly be allocated most of the unspent Tarp money of $350 billion.

“Second, governments must continue to facilitate the enormous task of sustaining credit flows and restructuring debt. Bankruptcies are inevitable but additional direct lending programmes, asset purchases and government guarantees are needed to keep liquidity flowing to good corporate and residential borrowers, especially while bank balance sheets are constrained by the need to soak up bad assets that were previously held off-balance sheet. Equity-for-debt swaps will be required for companies with excessive debt.”

Click here for the full article.

Source: George Magnus, Financial Times , December 18, 2008.

Did you enjoy this post? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail.

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2008 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Prieur du Plessis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.