The Geography of Global Economic Recession

Economics / Recession 2008 - 2010 Jun 03, 2009 - 03:12 AM GMTBy: STRATFOR

Peter Zeihan writes: The global recession is the biggest development in the global system in the year to date. In the United States, it has become almost dogma that the recession is the worst since the Great Depression. But this is only one of a wealth of misperceptions about whom the downturn is hurting most, and why.

Peter Zeihan writes: The global recession is the biggest development in the global system in the year to date. In the United States, it has become almost dogma that the recession is the worst since the Great Depression. But this is only one of a wealth of misperceptions about whom the downturn is hurting most, and why.

Let’s begin with some simple numbers.

As one can see in the chart, the U.S. recession at this point is only the worst since 1982, not the 1930s, and it pales in comparison to what is occurring in the rest of the world. (Figures for China have not been included, in part because of the unreliability of Chinese statistics, but also because the country’s financial system is so radically different from the rest of the world as to make such comparisons misleading. For more, read the China section below.)

But didn’t the recession begin in the United States? That it did, but the American system is far more stable, durable and flexible than most of the other global economies, in large part thanks to the country’s geography. To understand how place shapes economics, we need to take a giant step back from the gloom and doom of the current moment and examine the long-term picture of why different regions follow different economic paths.

The United States and the Free Market

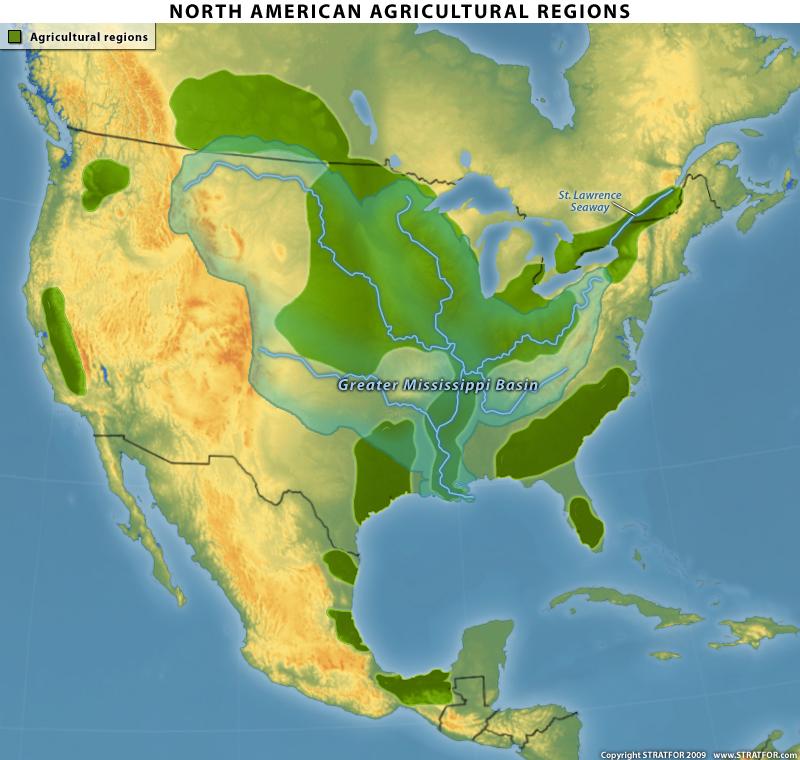

The most important aspect of the United States is not simply its sheer size, but the size of its usable land. Russia and China may both be similar-sized in absolute terms, but the vast majority of Russian and Chinese land is useless for agriculture, habitation or development. In contrast, courtesy of the Midwest, the United States boasts the world’s largest contiguous mass of arable land — and that mass does not include the hardly inconsequential chunks of usable territory on both the West and East coasts.

Second is the American maritime transport system. The Mississippi River, linked as it is to the Red, Missouri, Ohio and Tennessee rivers, comprises the largest interconnected network of navigable rivers in the world. In the San Francisco Bay, Chesapeake Bay and Long Island Sound/New York Bay, the United States has three of the world’s largest and best natural harbors. The series of barrier islands a few miles off the shores of Texas and the East Coast form a water-based highway — an Intercoastal Waterway — that shields American coastal shipping from all but the worst that the elements can throw at ships and ports.

The real beauty is that the two overlap with near perfect symmetry. The Intercoastal Waterway and most of the bays link up with agricultural regions and their own local river systems (such as the series of rivers that descend from the Appalachians to the East Coast), while the Greater Mississippi river network is the circulatory system of the Midwest. Even without the addition of canals, it is possible for ships to reach nearly any part of the Midwest from nearly any part of the Gulf or East coasts. The result is not just a massive ability to grow a massive amount of crops — and not just the ability to easily and cheaply move the crops to local, regional and global markets — but also the ability to use that same transport network for any other economic purpose without having to worry about food supplies.

The implications of such a confluence are deep and sustained. Where most countries need to scrape together capital to build roads and rail to establish the very foundation of an economy, transport capability, geography granted the United States a near-perfect system at no cost. That frees up U.S. capital for other pursuits and almost condemns the United States to be capital-rich. Any additional infrastructure the United States constructs is icing on the cake. (The cake itself is free — and, incidentally, the United States had so much free capital that it was able to go on to build one of the best road-and-rail networks anyway, resulting in even greater economic advantages over competitors.)

Third, geography has also ensured that the United States has very little local competition. To the north, Canada is both much colder and much more mountainous than the United States. Canada’s only navigable maritime network — the Great Lakes-St. Lawrence Seaway —is shared with the United States, and most of its usable land is hard by the American border. Often this makes it more economically advantageous for Canadian provinces to integrate with their neighbor to the south than with their co-nationals to the east and west.

Similarly, Mexico has only small chunks of land, separated by deserts and mountains, that are useful for much more than subsistence agriculture; most of Mexican territory is either too dry, too tropical or too mountainous. And Mexico completely lacks any meaningful river system for maritime transport. Add in a largely desert border, and Mexico as a country is not a meaningful threat to American security (which hardly means that there are not serious and ongoing concerns in the American-Mexican relationship).

With geography empowering the United States and hindering Canada and Mexico, the United States does not need to maintain a large standing military force to counter either. The Canadian border is almost completely unguarded, and the Mexican border is no more than a fence in most locations — a far cry from the sort of military standoffs that have marked more adversarial borders in human history. Not only are Canada and Mexico not major threats, but the U.S. transport network allows the United States the luxury of being able to quickly move a smaller force to deal with occasional problems rather than requiring it to station large static forces on its borders.

Like the transport network, this also helps the U.S. focus its resources on other things.

Taken together, the integrated transport network, large tracts of usable land and lack of a need for a standing military have one critical implication: The U.S. government tends to take a hands-off approach to economic management, because geography has not cursed the United States with any endemic problems. This may mean that the United States — and especially its government — comes across as disorganized, but it shifts massive amounts of labor and capital to the private sector, which for the most part allows resources to flow to wherever they will achieve the most efficient and productive results.

Laissez-faire capitalism has its flaws. Inequality and social stress are just two of many less-than-desirable side effects. The side effects most relevant to the current situation are, of course, the speculative bubbles that cause recessions when they pop. But in terms of long-term economic efficiency and growth, a free capital system is unrivaled. For the United States, the end result has proved clear: The United States has exited each decade since post-Civil War Reconstruction more powerful than it was when it entered it. While there are many forces in the modern world that threaten various aspects of U.S. economic standing, there is not one that actually threatens the U.S. base geographic advantages.

Is the United States in recession? Of course. Will it be forever? Of course not. So long as U.S. geographic advantages remain intact, it takes no small amount of paranoia and pessimism to envision anything but long-term economic expansion for such a chunk of territory. In fact, there are a number of factors hinting that the United States may even be on the cusp of recovery.

Russia and the State

If in economic terms the United States has everything going for it geographically, then Russia is just the opposite. The Russian steppe lies deep in the interior of the Eurasian landmass, and as such is subject to climatic conditions much more hostile to human habitation and agriculture than is the American Midwest. Even in those blessed good years when crops are abundant in Russia, it has no river network to allow for easy transport of products.

Russia has no good warm-water ports to facilitate international trade (and has spent much of its history seeking access to one). Russia does have long rivers, but they are not interconnected as the Mississippi is with its tributaries, instead flowing north to the Arctic Ocean, which can support no more than a token population. The one exception is the Volga, which is critical to Western Russian commerce but flows to the Caspian, a storm-wracked and landlocked sea whose delta freezes in the winter (along with the entire Volga itself). Developing such unforgiving lands requires a massive outlay of funds simply to build the road and rail networks necessary to achieve the most basic of economic development. The cost is so extreme that Russia’s first ever intercontinental road was not completed until the 21st century, and it is little more than a two-lane path for much of its length. Between the lack of ports and the relatively low population densities, little of Russia’s transport system beyond the St. Petersburg/Moscow corridor approaches anything that hints of economic rationality.

Russia has no good warm-water ports to facilitate international trade (and has spent much of its history seeking access to one). Russia does have long rivers, but they are not interconnected as the Mississippi is with its tributaries, instead flowing north to the Arctic Ocean, which can support no more than a token population. The one exception is the Volga, which is critical to Western Russian commerce but flows to the Caspian, a storm-wracked and landlocked sea whose delta freezes in the winter (along with the entire Volga itself). Developing such unforgiving lands requires a massive outlay of funds simply to build the road and rail networks necessary to achieve the most basic of economic development. The cost is so extreme that Russia’s first ever intercontinental road was not completed until the 21st century, and it is little more than a two-lane path for much of its length. Between the lack of ports and the relatively low population densities, little of Russia’s transport system beyond the St. Petersburg/Moscow corridor approaches anything that hints of economic rationality.

Russia also has no meaningful external borders. It sits on the eastern end of the North European Plain, which stretches all the way to Normandy, France, and Russia’s connections to the Asian steppe flow deep into China. Because Russia lacks a decent internal transport network that can rapidly move armies from place to place, geography forces Russia to defend itself following two strategies. First, it requires massive standing armies on all of its borders. Second, it dictates that Russia continually push its boundaries outward to buffer its core against external threats.

Both strategies compromise Russian economic development even further. The large standing armies are a continual drain on state coffers and the country’s labor pool; their cost was a critical economic factor in the Soviet fall. The expansionist strategy not only absorbs large populations that do not wish to be part of the Russian state and so must constantly be policed — the core rationale for Russia’s robust security services — but also inflates Russia’s infrastructure development costs by increasing the amount of relatively useless territory Moscow is responsible for.

Russia’s labor and capital resources are woefully inadequate to overcome the state’s needs and vulnerabilities, which are legion. These endemic problems force Russia toward central planning; the full harnessing of all economic resources available is required if Russia is to achieve even a modicum of security and stability. One of the many results of this is severe economic inefficiency and a general dearth of an internal consumer market. Because capital and other resources can be flung forcefully at problems, however, active management can achieve specific national goals more readily than a hands-off, American-style model. This often gives the impression of significant progress in areas the Kremlin chooses to highlight.

But such achievements are largely limited to wherever the state happens to be directing its attention. In all other sectors, the lack of attention results in atrophy or criminalization. This is particularly true in modern Russia, where the ruling elite comprises just a handful of people, starkly limiting the amount of planning and oversight possible. And unless management is perfect in perception and execution, any mistakes are quickly magnified into national catastrophes. It is therefore no surprise to STRATFOR that the Russian economy has now fallen the furthest of any major economy during the current recession.

China and Separatism

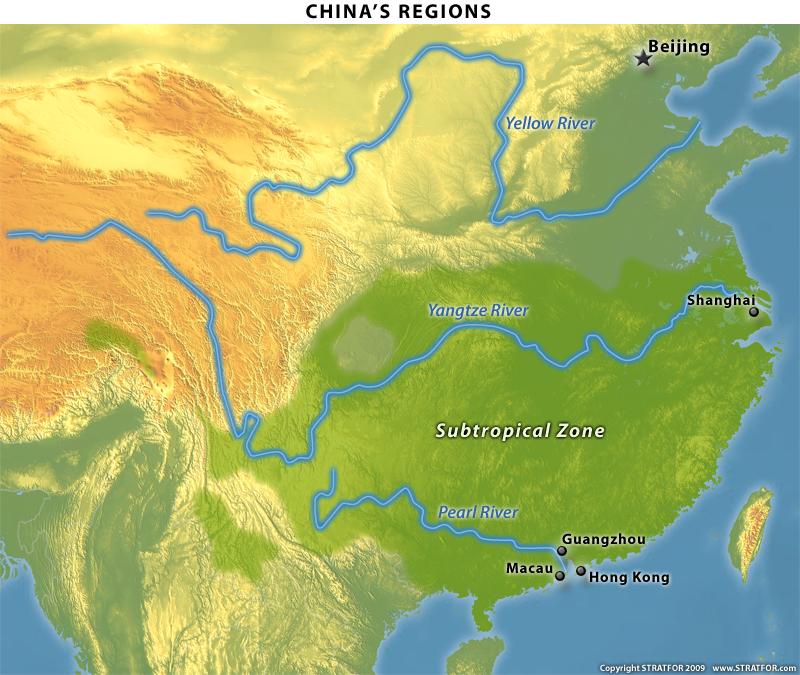

China also faces significant hurdles, albeit none as daunting as Russia’s challenges. China’s core is the farmland of the Yellow River basin in the north of the country, a river that is not readily navigable and is remarkably flood prone. Simply avoiding periodic starvation requires a high level of state planning and coordination. (Wrestling a large river is not the easiest thing one can do.) Additionally, the southern half of the country has a subtropical climate, riddling it with diseases that the southerners are resistant to but the northerners are not. This compromises the north’s political control of the south.

Central control is also threatened by China’s maritime geography. China boasts two other rivers, but they do not link to each other or the Yellow naturally. And China’s best ports are at the mouths of these two rivers: Shanghai at the mouth of the Yangtze and Hong Kong/Macau/Guangzhou at the mouth of the Pearl. The Yellow boasts no significant ocean port. The end result is that other regional centers can and do develop economic means independent of Beijing.

With geography complicating northern rule and supporting southern economic independence, Beijing’s age-old problem has been trying to keep China in one piece. Beijing has to underwrite massive (and expensive) development programs to stitch the country together with a common infrastructure, the most visible of which is the Grand Canal that links the Yellow and Yangtze rivers. The cost of such linkages instantly guarantees that while China may have a shot at being unified, it will always be capital-poor.

Beijing also has to provide its autonomy-minded regions with an economic incentive to remain part of Greater China, and “simple” infrastructure will not cut it. Modern China has turned to a state-centered finance model for this. Under the model, all of the scarce capital that is available is funneled to the state, which divvies it out via a handful of large state banks. These state banks then grant loans to various firms and local governments at below the cost of raising the capital. This provides a powerful economic stimulus that achieves maximum employment and growth — think of what you could do with a near-endless supply of loans at below 0 percent interest — but comes at the cost of encouraging projects that are loss-making, as no one is ever called to account for failures. (They can just get a new loan.) The resultant growth is rapid, but it is also unsustainable. It is no wonder, then, that the central government has chosen to keep its $2 trillion of currency reserves in dollar-based assets; the rate of return is greater, the value holds over a long period, and Beijing doesn’t have to worry about the United States seceding.

Because the domestic market is considerably limited by the poor-capital nature of the country, most producers choose to tap export markets to generate income. In times of plenty this works fairly well, but when Chinese goods are not needed, the entire Chinese system can seize up. Lack of exports reduces capital availability, which constrains loan availability. This in turn not only damages the ability of firms to employ China’s legions of citizens, but it also removes the primary reason the disparate Chinese regions pay homage to Beijing. China’s geography hardwires in a series of economic challenges that weaken the coherence of the state and make China dependent upon uninterrupted access to foreign markets to maintain state unity. As a result, China has not been a unified entity for the vast majority of its history, but instead a cauldron of competing regions that cleave along many different fault lines: coastal versus interior, Han versus minority, north versus south.

China’s survival technique for the current recession is simple. Because exports, which account for roughly half of China’s economic activity, have sunk by half, Beijing is throwing the equivalent of the financial kitchen sink at the problem. China has force-fed more loans through the banks in the first four months of 2009 than it did in the entirety of 2008. The long-term result could well bury China beneath a mountain of bad loans — a similar strategy resulted in Japan’s 1991 crash, from which Tokyo has yet to recover. But for now it is holding the country together. The bottom line remains, however: China’s recovery is completely dependent upon external demand for its production, and the most it can do on its own is tread water.

Discordant Europe

Europe faces an imbroglio somewhat similar to China’s.

Europe has a number of rivers that are easily navigable, providing a wealth of trade and development opportunities. But none of them interlinks with the others, retarding political unification. Europe has even more good harbors than the United States, but they are not evenly spread throughout the Continent, making some states capital-rich and others capital-poor. Europe boasts one huge piece of arable land on the North European Plain, but it is long and thin, and so occupied by no fewer than seven distinct ethnic groups.

These groups have constantly struggled — as have the various groups up and down Europe’s seemingly endless list of river valleys — but none has been able to emerge dominant, due to the webwork of mountains and peninsulas that make it nigh impossible to fully root out any particular group. And Europe’s wealth of islands close to the Continent, with Great Britain being only the most obvious, guarantee constant intervention to ensure that mainland Europe never unifies under a single power.

Every part of Europe has a radically different geography than the other parts, and thus the economic models the Europeans have adopted have little in common. The United Kingdom, with few immediate security threats and decent rivers and ports, has an almost American-style laissez-faire system. France, with three unconnected rivers lying wholly in its own territory, is a somewhat self-contained world, making economic nationalism its credo. Not only do the rivers in Germany not connect, but Berlin has to share them with other states. The Jutland Peninsula interrupts the coastline of Germany, which finds its sea access limited by the Danes, the Swedes and the British. Germany must plan in great detail to maximize its resource use to build an infrastructure that can compensate for its geographic deficiencies and link together its good — but disparate — geographic blessings. The result is a state that somewhat favors free enterprise, but within the limits framed by national needs.

And the list of differences goes on: Spain has long coasts and is arid; Austria is landlocked and quite wet; most of Greece is almost too mountainous to build on; it doesn’t get flatter than the Netherlands; tiny Estonia faces frozen seas in the winter; mammoth Italy has never even seen an icebreaker. Even if there were a supranational authority in Europe that could tax or regulate the banking sector or plan transnational responses, the propriety of any singular policy would be questionable at best.

Such stark regional differences give rise to such variant policies that many European states have a severe (and understandable) trust deficit when it comes to any hint of anything supranational. We are not simply taking about the European Union here, but rather a general distrust of anything cross-border in nature. One of the many outcomes of this is a preference for using local banks rather than stock exchanges for raising capital. After all, local banks tend to use local capital and are subject to local regulations, while stock exchanges tend to be internationalized in all respects. Spain, Italy, Sweden, Greece and Austria get more than 90 percent of their financing from banks, the United Kingdom 84 percent and Germany 76 percent — while for the United States it is only 40 percent.

And this has proved unfortunate in the extreme for today’s Europe. The current recession has its roots in a financial crisis that has most dramatically impacted banks, and European banks have proved far from immune. Until Europe’s banks recover, Europe will remain mired in recession. And since there cannot be a Pan-European solution, Europe’s recession could well prove to be the worst of all this time around.

By Peter Zeihan

This analysis was just a fraction of what our Members enjoy, Click Here to start your Free Membership Trial Today! If a friend forwarded this email to you, click here to join our mailing list for FREE intelligence and other special offers. Please feel free to distribute this Intelligence Report to friends or repost to your Web site linking to www.stratfor.com .

© Copyright 2009 Stratfor. All rights reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis.

STRATFOR Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.