Fed Shortsighted QE Policy Fuels the Continuing Gold Price Rise

Commodities / Gold and Silver 2010 Dec 20, 2010 - 03:22 PM GMT

“Washington doesn't agree on much these days, with one glaring exception: that the U.S. is facing a long-term fiscal crisis. The federal government's debt is now $13.8 trillion and is projected to hit $20 trillion by the end of the coming decade-when it will be the highest level as a share of the economy that the U.S. has seen in 50 years. In September the International Monetary Fund warned that the U.S. is moving dangerously close to a point at which spooked markets will send interest rates on new borrowing to devastatingly high levels. As it is, the government is on course to spend $1 trillion per year on interest costs alone-about a quarter of all federal spending. ‘We are accumulating debt burdens that will rival a third-world nation within 10 years,’ says David Walker, former chairman of the nonpartisan Congressional Budget Office. ‘Once you end up losing the confidence of the markets, things happen very suddenly-and very dramatically. We've seen that in Greece, we've seen it in Ireland, and we must not see it happen in the United States.’" - Michael Crowley, The New York Times

“Washington doesn't agree on much these days, with one glaring exception: that the U.S. is facing a long-term fiscal crisis. The federal government's debt is now $13.8 trillion and is projected to hit $20 trillion by the end of the coming decade-when it will be the highest level as a share of the economy that the U.S. has seen in 50 years. In September the International Monetary Fund warned that the U.S. is moving dangerously close to a point at which spooked markets will send interest rates on new borrowing to devastatingly high levels. As it is, the government is on course to spend $1 trillion per year on interest costs alone-about a quarter of all federal spending. ‘We are accumulating debt burdens that will rival a third-world nation within 10 years,’ says David Walker, former chairman of the nonpartisan Congressional Budget Office. ‘Once you end up losing the confidence of the markets, things happen very suddenly-and very dramatically. We've seen that in Greece, we've seen it in Ireland, and we must not see it happen in the United States.’" - Michael Crowley, The New York Times

|

Fed Open Market Committee meeting room |

The Federal Reserve's recent shift to the direct purchase of long-term Treasuries carries far-reaching implications for domestic economic stability, potentially causing systemic fractures that could dwarf any short-term benefits to economic growth. While the Fed’s goal is to avoid the scenario described in the quote above, it has created undeniable moral hazard, simultaneously fueling irrational, unpredictable and unsustainable distortions in the market. The Fed is at risk of causing the very end it seeks to prevent. If investor confidence in the bond market is permanently eroded by these policies, the United States could follow the path of Ireland and Greece and, as a result, elevate gold ownership from intelligent diversification to practical necessity.

In late 2008, in the wake of the financial crisis, the Federal Reserve elected to embark on an unprecedented (in the United States) stimulus plan known as Quantitative Easing (QE). At first, the Fed focused its purchases on Mortgage Backed Securities (MBS) in an effort to directly reduce mortgage rates and in hopes of reviving the housing market. In March 2009, the Fed expanded QE, allocating an additional $1.15 trillion in bond purchases. This time, instead of continuing to purchase only MBS, the Fed allocated $300 billion directly to the purchase of long-term Treasuries. At the time, this decision was buried in the rubble of the bailouts, and passed with little notice or worry to its significance.How a rational, freely trading bond market operates

On November 3, 2010, the Federal Reserve approved a second round of Quantitative Easing, dubbed in the market as “QE2”. In QE2 the Fed will directly purchase $600 billion worth of long-term Treasury Bonds, while reinvesting an additional $250-$300 billion by rolling over maturing assets. The Fed also decided against a specific end date to these operations, leaving open the possibility of additional future purchases. In contrast to QE1, which focused on Mortgage Backed Securities, QE2 constitutes a direct intervention in the US Treasury market. This difference is significant.

To understand how intervention in the bond market can have such far-reaching consequences, it’s worth a brief discussion on how a rational, freely trading bond market would operate. When an individual investor buys a 10-yr Treasury note, he is essentially agreeing to lend the US Government his money for ten years, and the government, in turn, agrees to give him more back than he gave them in the first place. The difference the government has to pay is a reflection of the perceived risk associated with lending the government a certain amount of money for a certain length of time. That risk is quantified by the interest rate. In a free market, if the interest rate offered to the market didn’t adequately compensate investors for the risk they felt they were taking on, the government would be unable to sell bonds at that rate. Due to a lack of demand, the US Treasury would have to offer higher interest rates until that risk/yield relationship came into balance and demand returned. This basic interaction of the risk/yield relationship and demand establishes a fair market valuation on an ongoing basis.

|

Timothy Geithner, US Secretary of the Treasury Ben Bernanke, Chairman of the Federal Reserve |

Now, consider the impact of direct Fed purchases: The presence of a ready buyer for any Treasury auction forces the yield the US government has to offer to attract buyers of its debt to remain artificially low. Essentially the government need not offer what would otherwise be the real market rate to sell its bonds. Since the Federal Reserve cares little for what interest rate it receives, especially because its goal is to drive the rate down, it skews the natural impact that demand, or lack thereof, has on setting a fair market rate. As this process continues over and over, the risk/yield relationship becomes increasingly distorted. The theory that the Fed adheres to is that this distortion is a net positive, in that it will bring down long-term rates, thereby stimulating the economy by rejuvenating credit markets. Of course, that conclusion is predicated on the hope that the economic growth garnered will fuel increased confidence (lower risk) for the market, thereby preventing a rate explosion after the Fed steps aside. In this perfect scenario, the end achieved would be a rebirth of economic growth, with no functional compromise to the stability of the Treasury market.

It is a slippery slope though, where any number of risks could give way to a whole new set of problems. If, on one hand, the Federal Reserve’s methods prove ineffective or too costly and it is forced to remove its support, the market will naturally recalibrate. Given the litany of fiscal and economic risks associated with our destructively high debt-to-GDP ratios, existing interest payment obligations, and stagnant growth (partially the result of the failure of these policies), the interest rate the government would need to offer to attract buyers of its debt, especially its long-term debt, would soar. This is, in a nutshell, what happened in Ireland and Greece. Interest payments on our debt would go from expensive to oppressive, and could dwarf all other government expenditures. A literal snowball effect would ensue and the scenarios described in the quote at the outset of this article would become a reality. Solutions would include higher taxes and reduced spending, ushering in a prolonged period of low economic growth, just like the austerity measures have caused in Ireland and Greece.

"We’ll do it until it works"

Granted, this is exactly what the Fed seeks to prevent. The greater likelihood is that the Fed will resist stepping away from the Treasury market altogether, employing a “We’ll do it until it works” attitude. But even if the recovery were to suddenly blossom, the Fed would likely continue the quantitative easing program, fearing economic growth may not be sustainable on its own momentum. The last thing the Fed would want is for the US to immediately slide back into a recession upon the discontinuation of its Treasury purchases. This attitude could easily lead to a permanent continuation of Fed open market operations.

The longer the Fed directly purchases Treasuries, the more distorted the market will become, and the more the economy will come to depend on Fed intervention. By skewing the risk/yield relationship, the Fed might ultimately undermine free market demand and eventually position itself as the primary buyer of US Treasuries. In the end, it is unknown whether this policy would even prevent the snowball effect described in the first scenario above and masthead quote. By fueling further distortions, and ultimately undermining the legitimacy of the Treasury market, the transition back to equilibrium might prove only to be substantially more painful.

Regardless of the course of action taken, the Fed and US Government are placing a risky bet on the success of these policies. Other countries have tried to paper over their financial problems, as the United States is now, only to ultimately have the free market expose their financial fractures. This was the fate of Ireland and Greece. For those countries, bailouts eventually prevented the market from imposing an oppressive borrowing rate and helped forestall an outright default. But if the United States were to follow this path, the most important question of all needs to be asked: If the lender of last resort is no longer able to borrow money, who stands ready to bail it out?

The Federal Reserve’s actions over the past two years suggest a sort of hubris, reflecting an apparent belief that its interventions are somehow immune to any negative consequences. To the point, during his interview on “60 Minutes”, Ben Bernanke was asked how confident he was that his policies would yield results and how sure he is in his ability to control the situation. “100 percent,” was his answer.

Paradigm shift in gold’s relevance

Despite the dollar’s role as the world’s reserve currency, the lethal combination of a discredited Treasury market and an ineffective Federal Reserve could cause economic instability and significant erosion in the value of the dollar, potentially igniting runaway inflation. This gives compelling cause to the belief that there is an ongoing paradigm shift in gold’s relevance, both for the individual investor and, within the international monetary system. Consider some of the events and trends seen in the gold market since the initial Fed involvement in the Treasury market in March 2009 (the initial $300bln QE injection mentioned earlier):

1. The price of gold has appreciated dramatically – On March 18, 2009 gold closed at $895 per ounce. The next day (the date the Fed announced it would purchase Treasuries directly) it jumped $60. Following the November 3, 2010 announcement of QE2, gold jumped $90 in four days, ultimately reaching an all-time high of $1430. Gold is currently trading at the $1400 level, up 56% from the first announcement of direct Treasury purchases by the Fed – less than two years ago.

2. World Bank chief Robert Zoellick said in an article in the Financial Times that leading economies should consider “employing gold as an international reference point of market expectations about inflation, deflation and future currency values.” Zoellick said a return to some sort of currency link to gold would be “practical and feasible, not radical.” Zeollick’s comments were made three days after the announcement of QE2.

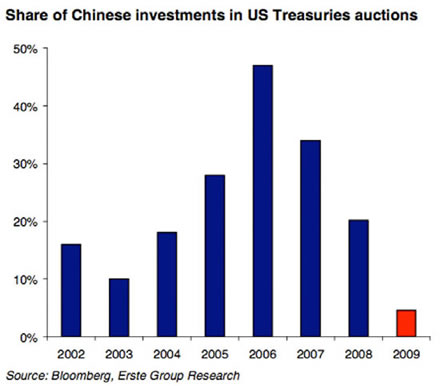

3. The dollar’s role as the world reserve currency is in question. “The dollar has proved not to be a stable store of value, which is a requisite for a stable reserve currency,’ the U.N. World Economic and Social Survey 2010 said. ‘A new global reserve system could be created, one that no longer relies on the United States dollar as the single major reserve currency.’” (Reuters) Countries have already begun to move away from US Treasuries in favor of gold, with China being the prime example. In the last six years, China has increased its official gold holdings 76%, from 454 metric tons to 1054 metric tons, vaulting them to the 5th largest gold holder in the world. Meanwhile, they’ve drastically curtailed their purchases of US Treasuries, as seen in the graph below:

4. In the 3rd Quarter filing with the SEC, three of the largest and closely followed hedge funds, Soros Fund Management LLC, Paulson & Co. and Touradji Capital Management LP listed investments in gold as their biggest holdings. David Einhorn of Greenlight Capital made headlines in July 2010 when he transferred his entire position in GLD, the gold paper ETF, to physical gold bullion.

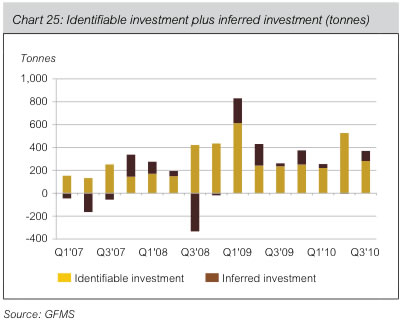

5. Gold investment demand has exploded in the last two years. The large spike in demand in the second quarter of 2009 (seen in the graph below) was in direct response to QE1. It should also be noted in conjunction with this point that, by the end of 2009, combined ownership of gold ETFs, gold stocks, and physical metal still only represented less than 1% of all invested assets globally.

The gold market has already been profoundly impacted by the early stages of Quantitative Easing. As global investors and countries alike embrace the yellow metal in response to these policies, one can only project what will happen to the price of gold, and its overall role in the international monetary system. At a minimum, it will take some time to unwind what the Fed has already committed to in QE2. Add to it the potential for expanded operations in the future and it’s quite possible that we “ain’t seen nothing yet” in the gold market.

Jonathan Kosares graduated ***** Laude with a degree in Finance from the University of Notre Dame. He has authored numerous articles on the gold market and is the moderator for the USAGOLD Video Series.

December’s Top Gold Articles

December, 2010by Randy Strauss

Editor’s Note: As the USAGOLD sitemaster, Randy Strauss selects articles and opinion pieces daily for our News & Views page, one of our most popular web pages. On occasion, he offers his own analysis on the news of the day -- all of which makes for some interesting reading. Editing and posting the breaking news puts him in a position uniquely suited for choosing the month’s top articles on gold and related subject matter. Here are his selections for December and his own views.

A vindication of Asians' faith in the value of gold

By N Balakrishnan, The National; December 9, 2010

China and India, whose central banks have been buying tonnes of gold in the open market, can hardly complain if their citizens do the same. Centuries of gold accumulation in Asia means that China and India now possess more gold than is likely to be mined in the future... This also means that if the world were ever to switch to a form of gold standard -- and this is no longer a fringe idea, with even the president of the World Bank suggesting it -- Asian countries, and certainly their citizens, would be in a strong position to adapt to the new gold standard. Chalk up one more point for the Asian economies.

COMMENT: We'll be shedding more light on World Bank president Robert Zoellick's "gold standard" endorsement in our final article. That particular event came early in this news cycle, but in true 'Top Ten' fashion we're saving the best (more or less) for last. In the meanwhile, to flesh out this Asian gold appetite just a bit more, Bloomberg has reported that imports of gold into China for the first 10 months of 2010 have reached 209 tonnes as compared to 45 tonnes for all of 2009. This is remarkable not only because it comes augments China's position as the world's top producer of newly mined gold, but because China is typically as tight-lipped about its gold-trade figures as it is about its reserves. One gets the distinct impression that China is proud of the feat and is poised to continue. Shen Xiangrong, chairman of the Shanghai Gold Exchange, said 70 percent to 80 percent of the imports in the first 10 months were made into mini-gold bars, which Chinese investors like to hold. "The expectation for higher inflation has fueled great interest among investors to hold physical gold, which led to higher imports," the gold exchange's Shen said. China is expected to have mine output of 340 tonnes this year, yet Shen says nothing of its fate, leaving one to imagine that it may very likely be destined to join the 454 tonnes of gold that were quietly accumulated and then suddenly added during the past year to China's original 600 tonnes of official gold reserves, bringing the publicly acknowledged total now to 1,054 tonnes (... and still likely being accumulated quietly in the background.)

All about gold with John Hathaway, Peter Munk, & James Grant

By Charlie Rose, Video Interview; December 6, 2010

PETER MUNK: Listen to me, Charlie, one point. ... Even then, let me tell you, what happened over the past five years, in frightening rich people in the fortunes that have been lost from bank stocks to European real estate to any asset class, I know many of these people, from Arab sheikhs to Latin-American billionaires who poured hundreds of millions in the past few years into gold and they doubled their money. Even if the economy becomes euphoric globally, which I don't think is a likely scenario, these guys have been so frightened and they have been so traumatized by all the other things that I think it will take years and years of that euphoric scenario for those people to give up gold. ...... But as every day goes by there are more and more new factors entering into this, and that is what supports gold and that is why gold is a really, really good investment right now.

COMMENT: James Grant and John Hathaway each made articulate points, but in my viewing of this interview, it was the delivery of these words by Peter Munk that resonated most powerfully.

Gold climbs as investors look for safe haven investments in midst of Korean conflict

By The Associated Press; November 23, 2010

Even a rising dollar couldn't stop gold and silver prices from climbing Tuesday as investors bid up the precious metals in light of economic woes in Europe and military conflict in the Koreas. "Any time you have conflict and war, gold is always a safe haven play you can go to," said Spencer Patton, founder and chief investment officer for hedge fund Steel Vine Investments LLC. "On a day when it should be lower, it really was strongly higher, which is just a great sign for gold going forward." Gold for December delivery rose $19.80 to close at $1,377.60 an ounce... The spike was largely driven by escalating tensions between North and South Korea, Patton said. The countries exchanged artillery fire Tuesday after the North shelled an island near their disputed sea border, killing at least two South Korean marines, setting dozens of buildings ablaze and sending civilians fleeing for shelter. The clash, which put South Korea's military on high alert, was one of the rivals' most dramatic confrontations since the Korean War ended.

COMMENT: Events such as this recent Korean military flare-up surely contribute to the daily list of new factors supportive of the overall gold investment scenario that Peter Munk was recently talking about.

Gold tipped to hit at least $1800 next year

By Atholl Simpson, CityWire.uk; November 30, 2010

"Without any major crisis I expect gold to reach between $1600-1800 in 2011, with a major crisis it is anybody's guess," said Donora.

"...for the first time since the 1970s US investors are investing around 5-10% of their portfolio either in precious metals or into commodities themselves." He described these investors as the last of the 'baby boom generation' and said they are looking for long-term investments to ensure their future. The result, he thinks, is that the gold which is being bought by this pool of investors is coming out of the market and is unlikely to return unless the dollar regains a lot of its credibility in the long term. "It is being allocated, not lent, and it does not tend to return to the market."

COMMENT: The key point here is that the more that gold is allocated into accounts conveying 'full (physical) ownership' and the less of it being lent around in a daisy chain of 'fractionalized ownership', the greater becomes the distinction between gold's relevance and value as a tangible asset -- as opposed to the financial system's nebulous realm of derivatives and counterparty liabilities. It may seem like an elementary point to make, but it is on the basis of this important distinction that the full and fair market valuation for gold metal is to be found, whereas the market in artificial gold investments may naturally trade at a valuation discount according to the perceived risk.

FOMC: Fed to continue expanding its holdings of Treasury securities

FOMC Press Release; December 14, 2010

Information received since the Federal Open Market Committee met in November confirms that the economic recovery is continuing, though at a rate that has been insufficient to bring down unemployment. ... To promote a stronger pace of economic recovery and to help ensure that inflation, over time, is at levels consistent with its mandate, the Committee decided today to continue expanding its holdings of securities as announced in November. The Committee will maintain its existing policy of reinvesting principal payments from its securities holdings. In addition, the Committee intends to purchase $600 billion of longer-term Treasury securities by the end of the second quarter of 2011, a pace of about $75 billion per month. The Committee will regularly review the pace of its securities purchases and the overall size of the asset-purchase program in light of incoming information and will adjust the program as needed to best foster maximum employment and price stability.

The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels for the federal funds rate for an extended period.

COMMENT: First of all, here we receive official confirmation of the December 5th interview on CBS' 60 Minutes in which Federal Reserve chairman Ben Bernanke signaled that the central bank might indeed expand its $600 billion bond purchase program to address the high unemployment rate. The second point I would like to make is based on inflation data released by the Labor Department released earlier this same day as the FOMC meeting. Reuters reported the following:

"The producer price index, a measure of business costs, rose 0.8 percent last month, above forecasts for a 0.6 percent gain in a Reuters poll. Compared to the same month a year earlier, the PPI climbed a robust 3.5 percent. Core producer prices -- which are favored by Federal Reserve policymakers because they exclude food and energy prices that are considered more erratic -- rose 0.3 percent, above estimates for a 0.2 percent increase. The yearly gain was 1.2 percent. ... The report highlighted the dissonance between the inflation measures used by policy officials and the everyday experience of businesses and consumers. Gasoline costs jumped 4.7 percent while the price of fruit soared 13.6 percent."

When policy makers at the Fed finally wake up and smell the price of coffee, they may have to deal with no eggs and cold bacon due to heightened costs for food and energy as resulting from these additional and upwardly adjustable measures of quantitative easing, which are being driven mainly by political concern about unemployment figures more so than by any assessments of general price stability. Further to this point about rising prices, a government report released the previous Friday along with trade deficit data for the month of November revealed that import prices rose by 1.3%, the largest monthly advance in a year.

[Gold sets new record high!] Jim Rogers: Fed understates inflation

By Steven C. Johnson and Frank Tang, Reuters; December 7, 2010

U.S. government inflation data is "a sham" and is causing the Federal Reserve to vastly understate price pressures in the economy, influential U.S. investor Jim Rogers told the Reuters 2011 Investment Outlook Summit, and he criticized the Fed's $600 billion bond-buying program. Rogers, who rose to prominence after co-founding the now defunct Quantum Fund with billionaire investor George Soros some four decades ago, said he was betting against U.S. Treasuries. ... "Everybody in this room knows prices are going up for everything," Rogers told the Reuters Summit. "If the world economy gets better, commodities are going to go up in price because there are shortages. If the world economy does not get better, you should own commodities, because (central banks) are going to print more money," he said. "Real assets are the way to protect yourself." Rogers also said the price of gold will rise eventually above $2,000 an ounce. The price of spot gold on Tuesday hit a record high of $1,430.95 an ounce.

COMMENT: On this record-setting day, Reuters reported the peak spot price as given above in dollar terms, whereas in euros it was reported as reaching an intraday record high at €1,072.03 per ounce. Bloomberg reported the peak for the February COMEX gold futures contract at $1,432.50 during morning trade, whereas they had the price of gold for immediate delivery reaching $1,431.25 on the day.

Obama commission says US debt is greatest threat to security

By Richard Blackden, Telegraph.uk; December 2, 2010

America's worst financial crisis since the Great Depression helped swell the deficit, and the report's release came on the same day the Federal Reserve was forced to disclose who received the more than $3 trillion in emergency financial aid it supplied between December 2007 and July 2010. The US central bank was stipulated to disclose the banks and companies that tapped six of its emergency loan programmes established because of the passing of the Dodd-Frank Act, the financial reform bill that was signed into law last summer. In total, the information discloses more than 21,000 transactions between the Fed and a host of banks and companies. Senator Bernie Sanders, an independent from Vermont, has said it was "incomprehensible" that the general public did not know who the Fed lent to during the crisis.

COMMENT: Let's focus on that concluding sentiment briefly. If an increase in political heat comes to jeopardize the Fed's ability to provide a lender of last resort safety net for dollar-denominated operations by the commercial banking sector, particularly insofar as much of this 'last resort' lending was necessarily extended to foreign banks as a direct consequence of the dollar's international reserve currency status, then this is yet another element that will erode the dollar's unique prominence in international banking usage. In the not-too-distant future we should anticipate most bilateral trade invoicing and financing to be denominated in the domestic currencies of the counterparty countries involved specifically in the underlying transaction. Any future default or bailout scenario, therefore, would be handled similarly as localized bilateral affairs rather than touching off a global meltdown. And as for the appropriate array of assets to hold among central banking reserves, gold would logically emerge as the one prevailing international choice -- serving as a universal cross-currency translator of benchmark value for dealings between any given pair of trading partners. Surplus foreign currency would find recourse with greater regularity to an active global gold market than to the counterparty's sovereign debt market (the exhaustive use of which has been the Achilles' heel of the present systemically vulnerable and dysfunctional international monetary architecture.)

... on The Role of Gold in the New Financial Architecture

DIFC Press Centre; December 9, 2010

In short, the size of the dollar liquidity necessary to finance global trade and capital movements will, in the near future, outweigh the size and the capability of the US economy to sustain it. Hence in a multipolar world where the economies of China and Euroland have a size on par with that of the US, the international role of the dollar would come increasingly under strain. Furthermore, the significant role played by other countries, such as Brazil, the GCC, Korea, South Africa, on the world stage will lead to a more decentralized network of financial centers unlikely to be revolving only around the US dollar.

This situation needs to be addressed by considering an alternative source of international liquidity. Specifically it suggests creating a "Hard SDR". The SDR is issued by the IMF and used in transactions among central banks. ... The Hard SDR, especially in these testing times when investors' confidence in paper assets is irremediably dented, should be pegged to a basket with a significant weight attributed to gold. Gold has represented historically a hedge against traumatic events such as inflation outbursts or major financial breakdown. In particular, Dr Nasser Saidi suggests: "International liquidity should be supplied on a large scale by an international currency such as the SDR, whose value should be tied to a basket of major currencies and gold, with the weight of the latter set at 20-25%."

COMMENT: The last significant shift to occur in the international monetary architecture was the 1999 inauguration of the European Central Bank, at which time the gold component for ECB's reserves were initiated at a more modest fraction of total reserves (15 percent on a floating MTM price basis) than the figure being proposed in this current report. The management and mark-to-market accounting of its gold reserves have been the one indisputable success story of the Eurosystem throughout the past decade. It is not surprising, therefore, that this principally firm gold foundation employed by the Eurosystem has been seminal in shaping key discussions as the international monetary officials struggle to retrofit the IMF's old dollar-based system, which was shattered when the subprime crisis first rocked the global financial markets nearly three years ago. And to be sure, the subsequent shift in the focal point of the ongoing crisis to the sovereign debt woes now plaguing the Eurosystem does not impugn the quality or desirability of the gold reserves component, but rather presents an appeal for wider, if not universal, application of gold reserves to their international peers.

China should consider increasing gold reserves to boost trade in the yuan

By Bloomberg News; December 2, 2010

China should consider adding to its gold reserves as a long-term strategy to pave the way for the yuan's internationalization, central bank adviser Xia Bin wrote in the China Business News today. ... China is allowing greater use of its currency for cross-border transactions to reduce reliance on the dollar, after Premier Wen Jiabao said in March he is "worried" about holdings of assets denominated in the greenback. The country must revise its foreign-reserves management principle, Xia wrote. China is the world's largest producer and second-biggest user of gold and has a world-record $2.65 trillion in foreign-exchange reserves. [The metal accounts for only 1.6 percent of the nation's reserves held by the People's Bank of China, according to the World Gold Council.] The country increased gold reserves by 454 tons to 1,054 tons since 2003, the State Administration of Foreign Exchange said last April. Building gold as the basis of solvency has been used through history, PBOC adviser Xia wrote. Having a corresponding amount of solvency is a necessary precondition and indispensible safeguard in the long-term strategy for the internationalization of the yuan, Xia wrote. China should raise its gold holdings and the 1,054 tons of reserves are inadequate compared with the 8,133 tons held by the U.S. and 3,408 tons by Germany, Meng Qingfa, a researcher at the China Chamber of International Commerce said on Oct. 27.

COMMENT: Although I we touched on China in our first article, that was more from a retail perspective, whereas this article demonstrates the potential heavyweight China could be if it entered the market more assertively in the context of rebalancing the official sector reserves. The luxury of time for non-disruptive accumulation may indeed be running out now that the president of the World Bank has openly lifted the lid on the merits of a more substantial role for gold within the global economy.

Betting on the Gold Standard? Odds are still long

By NPR; November 13, 2010

When the price of gold tipped $1,400 a troy ounce this week, the news fit right into a frenzy over the metal ignited by the World Bank president on Monday. In a Financial Times column, Robert Zoellick wrote that the global economy should consider using the price of gold as an "international reference point of market expectations about inflation, deflation and future currency values."

His statement was immediately taken, in some quarters at least, as a call for a return to the gold standard. Although he later clarified his point, the fire had been lit. And Zoellick, for the moment, became a hero for a small group that believes the U.S. should return to the gold standard. At the same time, he drew ire from mainstream economists tired of having the discussion in the first place.

COMMENT: Concluding our previous Top Ten, the notion of a $10,000/oz gold price was floated by Kenneth Rogoff, an event that we said was notable especially in light of the caliber and credentials of the spokesman (i.e., Professor of economics and Public Policy at Harvard University, and formerly the chief economist at the IMF). And here again the same theme applies. Returning briefly to the Charlie Rose interview featured earlier, Zoellick's remarks were brought up as a discussion point, and James Grant summarized it as follows: "Robert Zoellick wrote a piece, as you know, for a newspaper, 'The Financial Times,' and in it... mentioned perhaps that we might think about gold as a monetary unit... he had the temerity, the unimagined audacity to mention gold. Now, Robert Zoellick is an establishmentarian, born and bred. His resume could not be improved upon. Goldman Sachs, Fannie Mae, the World Bank -- And yet he mentioned this. So the mention of it by a man of his caliber, or his station in the establishment, is extraordinary." To which John Hathaway added, "[I]t's amazing. To come from a man with that background is an interesting shift in the establishment view. I mean, that was a leak in the dike, let's say, of the otherwise impervious view that gold is something... -- that should not play an official role." Reuters echoed that sentiment, putting a finer point on it in their report of Zoellick's comments, stating:

Leading economies should consider adopting a modified global gold standard to guide currency rates, World Bank president Robert Zoellick said on Monday in a surprise proposal before a potentially acrimonious G20 summit. ... While his opinion article in the Financial Times did not represent either U.S. or World Bank policy, it may reflect a greater openness in Washington than in the last two decades to some form of international currency cooperation. "The dollar is losing its relevance especially with the emergence of Asia economies, so a more neutral benchmark may be required. Gold, amid all the recent uncertainty, is proving its worth," said ANZ's senior commodity analyst Mark Pervan.

Zoellick later went on to describe gold as being "the elephant in the room" that policymakers needed to acknowledge. With few exceptions, policymakers have remained silent on the matter, but the markets certainly took notice, and gold has remained relatively buoyant ever since.

Short & Sweet

by Peter A. Grant, Senior Metals Analyst

There were several primary themes moving markets over the past month:

QE2

- The Fed launched into its second round of quantitative easing in November – dubbed QE2. The Fed plans to purchase an additional $600 bln in assets through the end of June 2011.

- US yields near 3-mo. highs as bond market seems inclined to hold Fed's feet to the fire over QE2.

- St. Louis Fed's Bullard says QE2 will be adjusted based on data. Might not need full $600 bln in new asset purchases.Boston Fed's Rosengren expects the central bank to buy the entire $600 bln of Treasuries. If necessary "we should take more action.”

- Me thinks the Fed is seeking to confuse on QE2, much like they did in the lead-up to 03 Nov announcement. Keeps market on its heels.

- Bernanke defends QE2, saying it could result in creation of 700k jobs over next 2 years. Where are the jobs from the much larger QE1?

- Fed's Bullard worries about disinflation in wake of below expectations PPI & CPI, but maintains full deployment of QE2 is data dependent.

- Is anyone surprised Bernanke has turned to the alleged job-creating potential of QE2 in attempt to quiet recent criticism from politicians?

- Bernanke hints that if surplus countries stimulated domestic demand, US might not need über easy monetary policy.

- FOMC Minutes show Fed’s growth forecasts revised significantly lower. Unemployment expectations revised higher.

- So what does the Fed do if dollar gains resulting from eurozone deterioration derail its quest for inflation? Ramp up the QE2?

- In wake of payrolls miss, I'm envisioning Bernanke on the horn with the DC Office Max, getting a quote on more paper & ink for his presses.

- Bernanke on 60-Minutes: "We’re not very far from the level where the economy is not self-sustaining,” said the man buying $600+ bln in US Treasuries.

- With US economic recovery "very close to the border" of sustainable and unsustainable, Bernanke hints more stimulus may be needed.

- Bernanke says, "we're not printing money, just look at the money supply.” I am, and I see a rise in M2 to an all-time high of $8.8 Trillion.

- 8 million+ jobs lost, trillions in bailouts, stimulus, QE & Bernanke concedes, "We've only gotten about a million of them back so far."

- Wondering what makes Bernanke think more QE is going to result in a different outcome. What was Einstein's definition of insanity?

Summary: One has to wonder what might be prompting the Fed to think they will get results different than those achieved with the much larger QE1 program. Fed Chairman Bernanke indicated in a 60-Minutes interview that more stimulus may be needed. Is QE3 in the queue? To be followed by QE4, QE5…? Clearly Mr. Bernanke is setting the stage for further devaluation of the dollar in his quest to manufacture inflation. That should in turn continue to have a positive influence on the price of gold, as prudent investors seek to preserve their wealth. This topic is discussed in greater detail in this month’s feature article.

US consumer confidence has edged higher in recent months, reaching 54.1 in November. While that's certainly better than the mid-twenty readings from early last year, it's only a modest improvement from last Christmas, and still way off the recent 111.9 peak in July of 2007. Perhaps consumers are merely feigning confidence and turning to their credit cards to provide a little holiday cheer in the wake of two pretty crummy Christmases in a row, as evidenced by the recent expansions in consumer credit after 19 consecutive monthly contractions. However, with a sluggish economy and unemployment still stubbornly high around 10%, there is little to warrant full-fledged jolliness.

EU Sovereign Debt Crisis

- Eurostat confirms latest upward revision in Greece's 2009 budget deficit at 15.4% of GDP, up from 13.6%.

- Austria threatened to withhold its contribution to Greek bailout package, claiming Greece hasn't met commitments to EU on public finances.

- No resolution to Ireland debt issues prompts collapse in euro to 7-wk lows.

- ECB's Honohan expects Ireland to take a large EU/IMF loan.

- Irish PM Cowen confirms bailout talks are under way. Looking for best possible deal "to improve the situation" and "provide certainty."

- Irish bailout announced. Spreads jump and euro tumbles, suggesting the market has not been mollified. Focus shifts to Portugal next.

- EU's Rehn on Ireland bailout: "It is likely unfortunately to imply tax increases." Without its low corporate tax structure, the Irish economy would really be in trouble.

- Bailout plunges Ireland into political turmoil. A little something extra to go along with their financial turmoil.

- Europe deeply fears contagion, which means everyone will get bailed-out, no matter the cause.

- Spanish yields soar on weak auction. Spread with German bunds reach record wide. Indicative of contagion.

- Ireland reveals 4-year austerity plan. Cuts include €2.5 bln to welfare. Corporate tax spared…for now. VAT hiked to 22% in 2013 and 23% in 2014.

- EU member nations pressure Portugal to seek a bailout in hopes of preventing contagion to Spain...because that worked so well with Ireland.

- ECB's Axel Weber assures eurozone rescue fund is sufficient. Governments "will do everything to keep the [euro] alive."

- ECB's Weber says the worst of worst cases is Portugal and Spain require bailouts too, but says the "euro will not fail because of a difference of €145 billion."

- Spain's PM Zapatero calls out those betting against his country. Says "absolutely" no bailout. He may not be so 'absolute' if Portugal caves.

- Eurozone rescue plan sends bondholders running. Spreads blow out. Borrowing costs in periphery soar and euro tumbles.

- Der Speigel says German households still have an estimated 13 billion Deutsche Marks stashed.

- German exporters fear a return of the Deutsche Mark, as safe-haven appeal would likely drive up costs of their products. That would probably result in higher unemployment too.

- European company borrowing costs rise as contagion worries hit the corporate debt market.

- Some feel that printing euros may be the EU’s last hope to halt the crisis. Kick the can just like America!

- Trichet says special liquidity measures will be extended at least until 12 Apr. -- Can we please have some American-style QE after that?

- Spain and Italy, seen as at-risk of contagion, press for ECB to act. QE is what they desire.

- Europe is treading an all-too familiar path: Attempting to resolve a debt crisis by borrowing more.

- Europe needs a debt-restructuring mechanism, but it’s simply easier for politicians to just issue more debt.

- Subdued demand at German 2-yr Schatz auction. Bid cover was just 1.1. Bundesbank kept €995M for open market operations, or auction may have failed.

- Eurogroup chief Junker accused Germans of "simple" thinking and of being "unEuropean" for dismissing the notion of eurobonds.

- Fitch cut Ireland's sovereign debt rating 3 levels to BBB+ on "additional fiscal costs of restructuring and supporting the banking system."

- ECB projects debt to "rise across the Eurozone in 2011," and almost everywhere in 2012, except Germany and Italy.

- ECB predicts mean debt/GDP ratio in eurozone of 87.8% in 2012 with Belgium, Ireland, Greece & Italy all over 100%.

- Banca D'Italia governor Draghi worries about the fine line the ECB is walking: "We could easily cross the line and lose everything we have."

- Germany's Merkel rules out expansion of rescue fund and eurobonds, but warns "If the euro fails, Europe fails. That's very serious." Front-runner for understatement of the year.

- Italy’s PM Silvio Berlusconi calls no-confidence vote “madness.” Warns that vote will hurl Italy into the midst of the EU financial crisis.

Summary: The lull in the EU sovereign debt crisis since Greece took its bailout in May was a short one. In November, Ireland had a bailout thrust upon it by the EU, which in fact did little to assuage contagion worries. Borrowing costs rose throughout the periphery of Europe as the market fixed its sights on Portugal next and the EU tried to insulate Spain -- its fourth largest economy – from the threat. It is widely believed that Spain is too big to bail out, but the risks extend even further, to Belgium, Austria and Italy. Talk about the potential for a complete collapse of the union continues to circulate, which is weighing on the single currency. That will continue to drive gold demand in Europe, but a falling euro also thwarts US efforts to devalue the greenback, which may force the Fed to extend its QE program beyond June of 2011.

The pace of residential foreclosures slowed in November, but it wasn't because the housing market had fundamentally improved. Instead many banks put a hold on foreclosures amid swirling concerns over faulty paperwork and procedures. In fact, new home sales plunged by 8.1% in October to just 283K, down 80% from the peak of the housing boom. Zillow, an online real estate database, projects that home values will be off $1.7 trillion in 2010, worse than the $1.05 trillion loss recorded in 2009. Zillow estimates that $9 trillion in residential home equity will have been wiped out since the housing market peaked in 2006.

Fed Bailout Data Dump

- Fed releases data on the beneficiaries of its $3.3 trillion in crisis aid.

- Fed programs saw some 21,000 transactions. The Fed followed "sound risk management practices." They incurred no credit losses and expect no losses. – Yeah, thanks to mark-to-fantasy valuations.

- Fed bought hundreds of billions of dollars worth of MBS from foreign banks. Deutsche Bank and Credit Suisse were top two beneficiaries.

- Fed helped prop up ten other central banks during the financial crisis. ECB borrowed money from the Fed 271 times for a gross rolling total of $8 trillion.

Summary: As part of the Dodd–Frank Wall Street Reform and Consumer Protection Act, the Fed was obligated to reveal the details of the $3.3 trillion in emergency aid it doled out in 2008 and 2009. Along with bailouts of the usual suspects, it was revealed that the Fed also bailed out foreign banks, corporations and even other central banks. It is now abundantly clear that the Fed is the lender of last resort to the world…which begs the question: Who bails out the lender of last resort to the world? This is a disturbing confirmation that the world calls on the Fed to provide global liquidity in the form of dollars when all hell is breaking loose. It’s easy; a couple keystrokes on a Fed computer terminal and voilà, trillions appear from out of nowhere!

- China’s Efforts to Curb Inflation

- China’s gold imports soar almost fivefold on inflation concern.

- China raised bank reserve requirements another 50bp, 6th hike this year. Talk of a rate hike persists.

- China CPI +1.1% m/m in Nov, up to +5.1% y/y pace, heightening markets anticipation of a PBoC rate hike.

- China is likely to continue increasing its gold position, which is presently a mere 1.6% of FX reserves.

- China raised bank reserve requirement by 50bp (effective 29 Nov), 5th such hike this year. Markets have been pricing in a rate hike.

- Chairman of China's sovereign wealth fund says China should not increase holdings of US Treasuries. - No problem. The Fed will pick up the slack.

- CIC chairman Lau says repercussions of a large sell-off of US Treasuries by Asian holders of US debt would be "inconceivable."

- China's fight against inflation – balanced against growth risks and risks of falling stocks – is a cautionary tale the Fed should heed.

- Stocks weighed by worries of further tightening by China; either more hikes to the reserve ratio or a rise in the benchmark lending rate.

- Jing Ulrich of JPM cites 47% rise in China's money supply since 2009 as a contributing factor to Chinese inflation. – Yep, that would sure do it.

Summary: Hot money inflows have become increasingly problematic in China, contributing to an uncomfortable 5.1% y/y inflation rate. China has focused on quantitative measures thus far in an effort to reign in price risks, but may ultimately have to resort to interest rate hikes. China and the world are understandably concerned that slowing the last major economic engine firing on all cylinders will have negative repercussions globally. Inflation will lead to ever increasing demand for gold within China as the PRC simultaneously continues to diversify out of paper assets into the yellow metal.

This Ed Stein cartoon initially ran around Christmas last year. If the five gold rings were a 'budget buster' then, Santa will have to scrutinize his budget even more carefully this year with gold up about 28% since last December.

Random

- FDIC Chairman Sheila Bair warns in Washington Post op-ed that debt could be 185% of GDP by 2035.

- BoJ's Morimoto indicates expanding the central bank's asset buying fund is a policy option being considered.

- WTO chief warns that currency wars could result in "1930s-style protectionism."

- Kiwi under pressure after S&P cut New Zealand outlook to negative on widening current account deficit & banking system credit risks.

- DPRK warns joint US/ROK military exercises to begin Sunday will bring Korean peninsula to "brink of war." China lodges protest as well.

Peter Grant spent the majority of his career as a global markets analyst. He began trading IMM currency futures at the Chicago Mercantile Exchange in the mid-1980's. Pete spent twelve years with S&P - MMS, where he became the Senior Managing FX Strategist. The financial press frequently reported his personal market insights, risk evaluations and forecasts. Prior to joining USAGOLD, Mr. Grant served as VP of Operations and Chief Metals Trader for a Denver based investment management firm.

For a free subscription to our newsletters, please click here.

By Michael J. Kosares

Michael J. Kosares , founder and president

USAGOLD - Centennial Precious Metals, Denver

Michael Kosares has over 30 years experience in the gold business, and is the author of The ABCs of Gold Investing: How to Protect and Build Your Wealth with Gold, and numerous magazine and internet articles and essays. He is frequently interviewed in the financial press and is well-known for his on-going commentary on the gold market and its economic, political and financial underpinnings.

Disclaimer: Opinions expressed in commentary e do not constitute an offer to buy or sell, or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. Centennial Precious Metals, Inc. recommends the purchase of physical precious metals for asset preservation purposes, not speculation. Utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such USAGOLD - Centennial Precious Metals does not warrant or guarantee the accuracy, timeliness or completeness of the information found here.

Michael J. Kosares Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.