Systemic Global Economic Crisis At the Crossroads of Three Roads of Global Chaos

Economics / Global Debt Crisis Jan 20, 2011 - 06:41 AM GMTBy: Global_Research

This GEAB issue marks the fifth anniversary of the publication of the Global Europe Anticipation Bulletin. In January 2006, on the occasion of the first issue, the LEAP/E2020 team indicated that a period of four to seven years was opening up which would be characterized by the “Fall of the Dollar Wall”, an event similar to the fall of the Berlin Wall which resulted, in the following years, in the collapse of the communist bloc then that of the USSR. Today, in this GEAB issue, which presents our thirty-two anticipations for 2011, we believe that the coming year will be a pivotal year in the roll out of this process between 2010 and 2013. It will be, in any case, a ruthless year because it will mark the entry into the terminal phase of the world before the crisis (1).

This GEAB issue marks the fifth anniversary of the publication of the Global Europe Anticipation Bulletin. In January 2006, on the occasion of the first issue, the LEAP/E2020 team indicated that a period of four to seven years was opening up which would be characterized by the “Fall of the Dollar Wall”, an event similar to the fall of the Berlin Wall which resulted, in the following years, in the collapse of the communist bloc then that of the USSR. Today, in this GEAB issue, which presents our thirty-two anticipations for 2011, we believe that the coming year will be a pivotal year in the roll out of this process between 2010 and 2013. It will be, in any case, a ruthless year because it will mark the entry into the terminal phase of the world before the crisis (1).

Since September 2008, when the evidence of the global and systemic nature of the crisis became clear to all, the United States, and behind it the Western countries, were content with palliative measures that have merely hidden the undermining effects of the crisis on the foundations of the present-day international system. 2011 will, according to our team, mark the crucial moment when, on the one hand, these palliative measures see their anesthetic effect fade away whilst, in contrast, the consequences of systemic dislocation in recent years will dramatically surge to the forefront (2).

In summary, 2011 will be marked by a series of violent shocks that will explode the faulty safety devices put in place since 2008 (3) and will carry off, one by one, the “pillars” on which the “Dollar Wall” has rested for decades. Only the countries, communities, organizations and individuals which, over the last three years, have actually undertaken to learn the lessons from the current crisis to distance themselves as quickly as possible from the pre-crisis patterns, values and behavior will get through this year unscathed; the others will be carried away in the procession of monetary, financial, economic, social and political difficulties that 2011 holds.

Thus, as we believe that 2011 will, globally, be the most chaotic year since 2006, the date of the beginning of our work on the crisis, in this GEAB issue our team has focused on 32 anticipations for 2011, which also include a number of recommendations to deal with future shocks. Thus, this GEAB issue offers a kind of map forecasting financial, monetary, political, economic and social shocks for the next twelve months.

If our team believes that 2011 will be the worst year since 2006, the beginning of our anticipation work on the systemic crisis, it’s because it’s at the crossroads of three paths to global chaos. Absent fundamental treatment of the causes of the crisis, since 2008 the world has only gone back to take a better jump forward.

A bloodless international system

In fact, since the mid-2000s at least, all the major global players, at their head of course the United States and its cortege of Western countries, do no more than give out information, or gesticulate. In reality, all bets are off: The crisis ball rolls and everyone holds their breath so it doesn’t fall on their square. But gradually the increasing risks and issues of the crisis have changed the casino’s roulette wheel into Russian roulette. For LEAP/E2020, the whole world has begun to play Russian roulette (6), or rather its 2011 version, “American Roulette” with five bullets in the barrel.

The inflation induced by US, British and Japanese Quantitative Easing and similar stimulus measures of the Europeans and Chinese will be one of the destabilizing factors in 2011 (14). We will come back to this in more detail in this issue. But what is now clear with respect to what is happening in Tunisia (15), is that this global context, especially the rise in food and energy prices, now leads on to radical social and political shocks (16). The other reality that the Tunisian case reveals is the impotence of the French, Italian or American “godfathers” to prevent the collapse of a “friendly regime” (17).

Impotence of the major global geopolitical players

On one side we haves a moribund West with, on the one hand, the United States, for whom 2011 will show that its leadership is no more than fiction (see this issue) and which is trying to freeze the entire international system in its configuration of the early 2000s (18), and on the other hand we have Euroland, “sovereign” in the pipeline, which is currently mainly focused on adapting to its new environment (19) and new status as an emerging geopolitical entity (20), and which, therefore, has neither the energy nor the vision necessary to influence world events (21).

And on the other side are the BRIC countries (with China and Russia in particular) who are, at the moment, proving to be incapable of taking control of all or part of the international system and whose only action is therefore limited to quietly undermine what remains of the foundations of the pre-crisis order (22).

Ultimately, impotence is widespread (23) at the international community level, increasing not only the risk of major shocks, but also the significance of the consequences of these shocks. The world of 2008 was taken by surprise by the violent impact of the crisis, but paradoxically the international system was better equipped to respond being organized around an undisputed leader (24). In 2011, this is no longer the case: not only is there no undisputed leader, but the system is bloodless as we have seen above. And the situation is aggravated further by the fact that the societies of many countries in the world are on the verge of socio-economic break-up.

Societies on the edge of socio-economic break-up

But amongst the emerging powers too, the violent transition which constitutes the crisis is leading societies towards situations of break-up: in China, the need to control expanding financial bubbles is hampered by the desire to improve the lot of whole sectors of society such as the need for employment for tens of millions of casual workers; in Russia, the weakness of the social security system fits badly with the enrichment of the elite, just as in Algeria shaken by riots. In Turkey, Brazil and India, everywhere the rapid change these countries are seeing is triggering riots, protests and terrorist attacks. For reasons that are sometimes contradictory, growth for some, penury for others, across the globe our diverse societies tackle 2011 in a context of strong tensions and socio-economic break-up, which have the making of political time bombs.

It’s its position at the crossroads of three paths which thus makes 2011 a ruthless year. And ruthless it will be for the States (and local authorities) which have chosen not to draw hard conclusions from the three years of crisis which have gone before and / or who have contented themselves with cosmetic changes not altering their fundamental imbalances at all. It will also be so for businesses (and States (27)) who believed that the improvement in 2010 was a sign of a return to “normal” of the global economy. And finally it will be so for investors who have not understood that yesterday’s investments (securities, currencies,...) couldn’t be those of tomorrow (in any case for several years). History is usually a “good girl”. She often gives a warning shot before sweeping away the past. This time, it gave the warning shot in 2008. We estimate that in 2011, it will do the sweeping. Only players who have undertaken, even painstakingly, even partially, to adapt to the new conditions generated by the crisis will be able to hang on; for the others, chaos is at the end of the road.

Notes:

(1) Or of the world that we have known since 1945 to repeat our 2006 description.

(2) The recent decision by the US Department of Labor to extend the inclusion of the measure of long-term unemployment in the US employment statistics to five years instead of the maximum of two years until now, is a good indicator of the entry into a new stage of the crisis, a step that has seen the disappearance of the “practices” of the world before. As a matter of fact, the US government cites “the unprecedented rise” of long-term unemployment to justify this decision. Source: The Hill, 12/28/2010

(3) These measures (monetary, financial, economic, budgetary, strategic) are now closely linked. That’s why they will be carried away in a series of successive shocks.

(4) Source: The Independent, 01/13/2011

(5) It’s even worse because it was international aid that brought cholera to the island, causing thousands of deaths.

(6) Moreover Timothy Geithner, US Treasury Secretary, little known for his overactive imagination, has just indicated that “the US government could once again have to do exceptional things”, referring to the bank bailout in 2008. Source: MarketWatch, 01/13/2011

(7) Moreover, India and Iran are in the course of establishing a system of exchange “gold for oil” to try and avoid supply disruptions. Source: Times of India, 01/08/2011

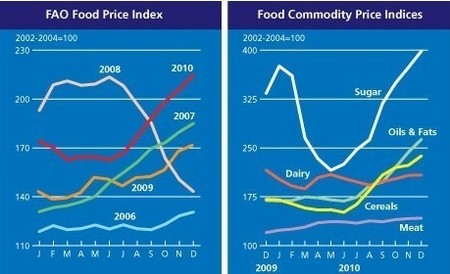

(8) In January 2011 the FAO food price index (at 215) has just exceeded its previous record set in May 2008 (at 214).

(9) Wall Street banks are currently unloading their US Treasury bonds as fast as possible (unseen since 2004). Their official explanation is “the remarkable improvement in the US economy which no longer requires us to seek refuge in Treasury Bonds”. Of course, you are free to believe it, like Bloomberg ’s journalist on 01/10/2011.

(10) Thus Euroland is already taking big steps forward along the path described in the GEAB N°50 with a discount in the case of refinancing the debts of a member state, whilst Japanese and US debt are now about to enter the storm. Sources: Bloomberg, 01/07/2011; Telegraph, 01/05/2011

(11) We believe that, in general, global banks’ balance sheets contain at least 50% ghost assets which in the coming year will require to be discounted by between 20% to 40% due to the return of the global recession combined with austerity, the rise in defaults on household, business, community and state loans, currency wars and a pickup in the fall of real estate prices. The American, European, Chinese, Japanese and others “stress-tests” can still continue to try and reassure markets with “Care Bears” scenarios except that this year it’s “Alien against Predator ” which is on the banks’ agenda. Source: Forbes, 01/12/2011

(12) Each of these real estate markets will fall sharply again in 2011 in the case of those which have already started falling in recent years, or in the case of China, which will begin its sharp deflation amid economic slowdown and monetary tightening.

(13) The Japanese economy is, moreover, one of the first victims of this currency war, with 76% of the CEOs of 110 major Japanese companies surveyed by Kyodo News now reported being pessimistic about Japanese growth in 2011 following the rise in the yen. Source: JapanTimes, 01/04/2011

(14) Here are several instructive examples put together by the excellent John Rubino. Source: DollarCollapse, 01/08/2011

(15) By way of reminder, in the GEAB N°48 we had classified Tunisia in the category of countries “with significant risks” in 2011.

(16) No doubt, moreover, that the Tunisian example is generating a round of reassessment amongst the rating agencies and the “experts in geopolitics”, who, as usual, didn’t see anything coming. The Tunisian case also illustrates the fact that it’s now the satellite countries of the West in general and the US in particular, who are on the way to shocks in 2011 and in the years to come. And it confirms what we regularly repeat: a crisis accelerates all the historical processes. The Ben Ali regime, twenty-three years old, collapsed in a few weeks. When political obsolescence is involved everything changes quickly. Now it's all the pro-Western Arab regimes which are obsolete in the light of events in Tunisia.

(17) No doubt this « Western godfather » paralysis will be carefully analyzed in Rabat, Cairo, Jeddah and Amman, for example.

(18) A configuration that was all the more favorable because it was without a counterweight to their influence.

(19) We will return in more detail in this GEAB issue, but seen from China we are not mistaken. Source: Xinhua, 01/02/2011

(20) Little by little Europeans are discovering that they are dependent on centres of power other than Washington. Beijing, Moscow, Brazilia, New Dehli,… Source: La Tribune, 01/05/2011; Libération, 12/24/2010; El Pais, 01/05/2011

(21) All Japan's energy is focused on its desperate attempt to resist the attraction of China. As for other Western countries, they are not able to significantly influence global trends.

(22) The US Dollar’s place in the global system is a part of these last foundations that the BRIC countries are actively eroding day after day.

(23) As regards deficit, the US case is textbook. Beyond the speeches, everything continues as before the crisis with a deficit swelling exponentially. However, even the IMF is now ringing the alarm. Source: Reuters, 01/08/2011

(24) Moreover, even the Wall Street Journal on 01/12/2011, echoing the Davos Forum, is concerned over the lack of international coordination, which is in itself a major risk to the global economy.

(25) Millions of Americans are discovering food banks for the first time in their lives, whilst in California, as in many other states, the education system is disintegrating fast. In Illinois, studies on the state deficit are now comparing it to the Titanic. 2010 broke the record for real estate foreclosures. Sources: Alternet, 12/27/2010; CNN, 01/08/2011; IGPA-Illinois, 01/2011; LADailyNews, 01/13/2011

(26) Ireland, which is facing, purely and simply, a reconstruction of its economy, is a good example of situations to come. But even Germany, with remarkable current economic results however can’t escape this development as shown by the funding crisis for cultural activities. Whilst in the United Kingdom, millions of retirees are seeing their incomes cut for the third year running. Sources : Irish Times, 12/31/2010; Deutsche Welle, 01/03/2011; Telegraph, 01/13/2011

(27) In this regard, US leaders confirm that they are rushing straight into the wall of public debt, failing to anticipate the problems. Indeed, the recent statement by Ben Bernanke, the Fed chairman, that the Fed will not help the States (30% fall in 2009 tax revenues according to the Washington Post on 01/05/2011) and the cities collapsing under their debts, just as Congress decides to stop issuing “Build America Bonds” which enabled States to avoid bankruptcy these last few years, shows a Washington blindness only equal to that which Washington demonstrated in 2007/2008 in the face of the mounting consequences of the “subprime” crisis. Sources: Bloomberg, 01/07/2011; WashingtonBlog, 01/13/2011

Global Europe Anticipation Bulletin

Global Research Articles by Global Europe Anticipation Bulletin

© Copyright Global Europe Anticipation Bulletin -, Global Research, 2011

Disclaimer: The views expressed in this article are the sole responsibility of the author and do not necessarily reflect those of the Centre for Research on Globalization. The contents of this article are of sole responsibility of the author(s). The Centre for Research on Globalization will not be responsible or liable for any inaccurate or incorrect statements contained in this article.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.