What Economic Uncertainty Means for the Rare Earth Metals Sector

Commodities / Metals & Mining Oct 12, 2011 - 04:26 AM GMT

The rare earth sector has seen astronomical gains in recent years as Chinese export restrictions, short-sighted U.S. policy and investor interest combined to make front page news. In this exclusive article for The Critical Metals Report, Chris Berry, founder and president of House Mountain Partners, LLC, argues that a "Great Reset" is changing the face of the sector, rewarding explorers far more selectively.

The rare earth sector has seen astronomical gains in recent years as Chinese export restrictions, short-sighted U.S. policy and investor interest combined to make front page news. In this exclusive article for The Critical Metals Report, Chris Berry, founder and president of House Mountain Partners, LLC, argues that a "Great Reset" is changing the face of the sector, rewarding explorers far more selectively.

What Economic Uncertainty Means for the Rare Earth Sector

The competition among non-Chinese junior mining companies to successfully mine rare earth elements (REEs) began as a footrace and evolved into a full-on stampede. That race is now unraveling, thanks to slower global economic growth and the sheer number of exploration companies involved in rare earth exploration. We have seen estimates of over 300 companies involved in this global search, and when you factor in the relatively tiny size of the rare earth market (approximately 130,000 tons produced in 2010, according to the U.S. Geological Survey) we still stand by what we've said all along—there is room here for a few major players and not much else. We believe the rare earth industry is in the beginning stages of a phase we call "The Great Reset." We base this theory on four ideas:

- Everything reverts to the mean. This includes rare earth oxide (REO) prices. While we believe we will see a permanently higher price for select REOs, this is not the case for the entire suite of oxides, and prices cannot continue rising indefinitely. The laws of supply and demand have proven this.

- Demand projections for REOs are being re-evaluated downward due to anemic global economic growth prospects. With a tremendous debt overhang in the United States and Europe and evidence of growth slowing in China (the three biggest economies in the world), lower aggregate demand for finished goods that use REOs is a given. We have seen forecasts for REO demand in 2015 that are higher than they are today, and don't disagree, but the downward revision is indicative of lower demand for most REOs.

- Companies such as Toyota and General Motors are actively researching substitutes for REOs in their products. This type of research has been in progress for some time and we think that these companies would not be spending the R&D dollars if they didn't want to avoid high REO prices.

- Demand projections for "green" or "clean tech" applications such as hybrid electric vehicles, wind turbines and solar cells are not factoring in whether or not manufacturers of these goods can ensure a steady supply of raw materials (specifically REOs) to meet their production forecasts. The rare earth industry is a customer-driven business in that the customer needs REOs of a highly specific type and purity. If a wind turbine manufacturer can't procure a specific purity of neodymium oxide, for example, the wind turbine may get built without neodymium, implying demand destruction. We have seen estimates of the use of up to one ton of neodymium needed to produce one megawatt of generating capacity from a wind turbine. China alone has plans to install 100 gigawatts of generating capacity from wind (up from 12 gigawatts in 2009). When you factor in European and American projections for wind power (not to mention other parts of the world), this begs the question of whether or not there is enough neodymium to go around and if there currently is not, will there be enough to satisfy these growth targets in wind generating capacity? We are well aware of the benefits of neodymium-iron-boron magnets in miniaturization and efficiency, but think that if a product can be manufactured economically without REOs, then the manufacturer will choose that path or abstain from building the product at all.

To be clear—we have not "thrown in the towel" on REOs and the important role they play in certain sectors of the economy. What we are saying is that the role will be different from what many in the sector currently suggest. Like many other facets of life, the rare earth sector is Darwinian in nature and will evolve to equilibrate supply and demand. The gratification that comes along with healthy and growing demand for a product (in this case REOs) will be delayed, to the chagrin of investors and rare earth mining company CEOs alike. This "reset" shapes how we think about the rare earth space now and in the future and in deciding how and where to invest. Below is a price chart of the Bloomberg Rare Earth Mineral Resources Index and its one-year performance.

The One Sector Where Supply and Demand Don't Matter

There is one area of the economy, however, which we think is immune to the vagaries of supply and demand of REOs: the military. While the potential for substitution exists with consumer products, we believe there is no such "wiggle room" when analyzing a country's defense capabilities. The neodymium-iron-boron magnets we mentioned above are critical in actuators of precision-guided bombs and are designed specifically around these magnets. Actuators are responsible for control of the bomb, and this is just one of several products (lasers and radar being two significant other products) that must use rare earths to function optimally. Without the magnets in the bombs, performance is reduced—implying an inferior product—something nobody should be willing to accept. The U.S. Military is responsible for a small overall percentage of REO demand in the United States, but it is significant nonetheless.

The Rare Earth Supply Chain: The Key to It All

So at this point, we believe two things: first, demand for most REOs will decrease in the near term, and second, that it will be exceedingly difficult for the majority of the junior mining companies involved in rare earth exploration to achieve commercial production of REOs. Despite this, the singular crucial issue that put the rare earth story on the front page of every newspaper around the world in the first place still haunts us—Western dependence on a critical resource from a strategic adversary. While a seemingly endless amount has been written about China's control of the supply of REEs, what we think is most important (and most often missed by the pundits) is the fact that China also effectively owns the entire mine-to-magnet supply chain. This is the crucial vulnerability. The mining of rare earths is the easy part. It is the resulting steps where intellectual property is created that really matter. In 2010, the United States Government Accountability Office (GAO) was commissioned to deliver a report on the use of rare earth elements in the Department of Defense supply chain. Regarding military capabilities, the report states (Ed. Note: bold text is ours),

"For example, the M1A2 Abrams tank has a reference and navigation system that uses samarium cobalt (SmCo) permanent magnets. The samarium metal used in these magnets comes from China."

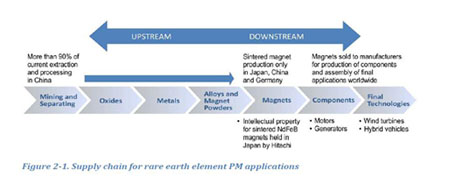

Whether we're discussing heavy rare earth elements (HREEs) or light rare earth elements (LREEs), a particular concern is the fact that the West is realistically years away from having a supply chain built that can diminish foreign dependence on REOs. Viewed that way, reduced demand for certain REOs could be a blessing in disguise in that it can give Western policymakers more time to formulate a viable strategy, though based on recent behavior in Washington DC (i.e., the debt ceiling debate), we're not holding our breath. The chart below shows the supply chain for rare earth permanent magnets used in wind turbines and hybrid vehicle motors, among other products. China is responsible for the entire upstream portion of this chain and has designs through mercantilist export policies on owning the entirety of the downstream portion of the chain as well.

There are myriad issues surrounding China's trade policies and her seeming inability to "play fair" on the world stage. The World Trade Organization recently found that China was in violation of international trade rules for curbing exports of rare earths. The Chinese government is likely to appeal this ruling, effectively kicking the can down the road and prolonging export curbs of rare earths from China indefinitely. Though one could, based on this factor, infer higher prices for REOs, we still believe that slower economic growth and potential for substitution point to lower REO prices going forward.

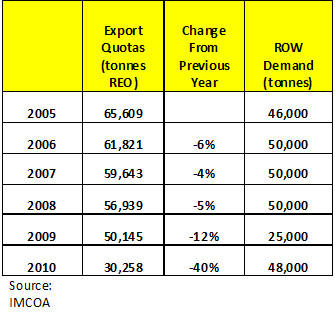

To get a sense of how Chinese export quotas of REOs have decreased in recent years and the resulting increases in prices of REOs, see the charts below:

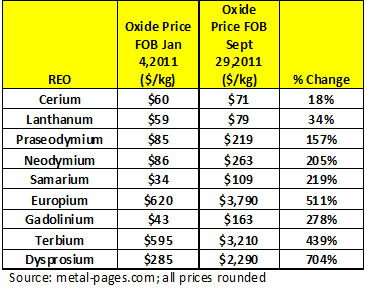

Here are the YTD percentage increases in prices of select REOs. More than anything else, we believe, this makes the case for our thoughts on mean reversion and demand destruction described above:

What to Focus on in the Rare Earth Space Going Forward

There are numerous important factors to consider when undertaking due diligence of a mining opportunity (management capability, grade, tonnage, etc.) that we use in the Discovery Investing Ten-Point Factor Model, but we think that there are three keys one must consider initially before looking further at a given rare earth exploration company as an investment.

Despite the fact that we believe the "easy money" has already been made in this sector, we do believe that opportunities for profit exist. Much has been made in recent months of "critical" or "strategic" metals and what constitutes a metal joining this group. We would certainly include rare earths here and, in fact, take this one step further. We consider rare earths to be "political metals." In the rare earth sector, geopolitics trumps all, and this is the first factor to consider when investing in the junior mining rare earth sector. It should be clear that we have our doubts about permanently increasing demand for REOs. However, due to the significant enhancements REOs provide in military applications, access to a reliable supply of these metals is now on the radar (pardon the pun) of politicians from Brussels, to Ottawa, to Beijing, to Washington DC. In the United States, Sen. Lisa Murkowski (R-Alaska) has been an ardent supporter of rebuilding the U.S. industrial base and supply chain for critical minerals, including rare earths. Rare earth deposits are of strategic significance. A deposit in a safe and stable political jurisdiction is an absolute must.

Second, when comparing rare earth deposits, a decidedly large slant towards HREE mineralization is also a must. After all, the HREEs are truly "rare," and forecast to be in deficit going forward. In our opinion, investing in a large LREE deposit that promises tens of thousands of tons of REO production per year, when the Chinese dominate this portion of the market and are set to do so going forward, is not a wise move. In the price chart we printed above, dysprosium oxide and terbium oxide (two of the most sought-after HREOs) have increased in price by 704% and 439% respectively, year-to-date. We do not expect continued triple-digit gains in these REO prices, but do believe that deposits with a high percentage of HREEs have potential to outperform going forward.

Finally, while the geopolitics and HREE content are important, without a solid understanding of the metallurgy of a deposit, you could quite literally be investing in moose pasture. This is one of the ultimate differences between rare earths and other metals. Separating 17 metals from each other is an enormously difficult task both technically and financially. This is also a competitive advantage the Chinese have over the West—they have "cracked" the metallurgy of their primary rare earth deposits. While we don't expect miracles, we do want to see Western rare earth companies making steady progress into understanding the mysteries of the metallurgy. This is one of the biggest risk factors when analyzing a rare earth exploration company.

The Future Is Never Certain, but There Will Always Be a Place for REOs

It appears to be a rather hazy future for the rare earth sector as slow economic growth, potential for substitution, manufacturers potentially misreading demand for their own products that use REOs and price mean reversion all come together to take some of the "froth" out of this market. We think this is a good thing. Regardless, the big picture issues surrounding the need for REOs in various military and clean tech applications are going to keep the industry front and center, but it will evolve much differently than many expect. The Great Reset will ensure that.

Chris Berry, with a lifelong interest in geopolitics and the financial issues that emerge from these relationships, founded House Mountain Partners in 2010. The firm focuses on the evolving geopolitical relationship between emerging and developed economies, the commodity space and junior mining and resource stocks positioned to benefit from this phenomenon. Chris holds an MBA in finance with an international focus from Fordham University, and a BA in international studies from The Virginia Military Institute.

Want to read more exclusive Critical Metals Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators and learn more about critical metals companies, visit our Critical Metals Report page.

Streetwise - The Gold Report is Copyright © 2011 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

The Gold Report does not render general or specific investment advice and does not endorse or recommend the business, products, services or securities of any industry or company mentioned in this report.

From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Gold Report. These logos are trademarks and are the property of the individual companies.

101 Second St., Suite 110

Petaluma, CA 94952

Tel.: (707) 981-8999

Fax: (707) 981-8998

Email: jluther@streetwisereports.com

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.