Europe Is in for a Long Recession

Economics / Double Dip Recession Nov 22, 2011 - 03:04 AM GMTBy: Paul_L_Kasriel

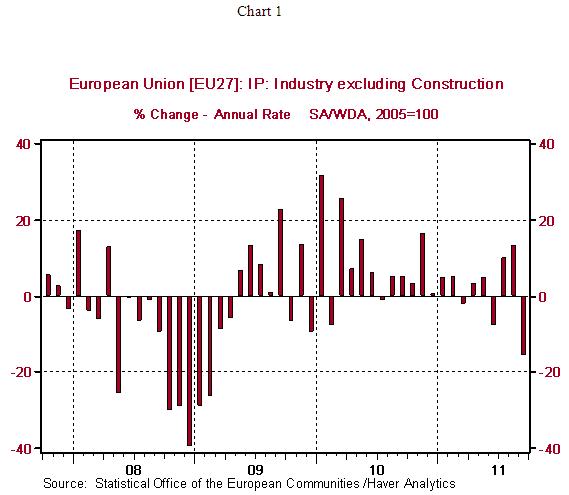

Collectively, the 27 sovereign nations that make up the European Union (EU) most likely entered a recession this quarter. Chart 1 shows that EU industrial production contracted at an annualized rate of 15.5% in September vs. August, a near certain sign of a recession. Given that the EU represents the largest economy in the world, a recession there is no small beer for the rest of the world.

Collectively, the 27 sovereign nations that make up the European Union (EU) most likely entered a recession this quarter. Chart 1 shows that EU industrial production contracted at an annualized rate of 15.5% in September vs. August, a near certain sign of a recession. Given that the EU represents the largest economy in the world, a recession there is no small beer for the rest of the world.

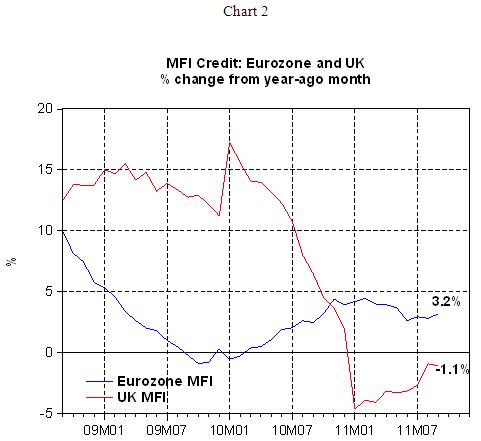

The Greek tragedy morphed into an Italian comedy. Now, it has become a French farce. The plot behind all of these theater forms is how an economy struggles when deprived of adequate bank credit. Chart 2 shows the recent behavior of monetary financial institution (MFI) credit in the eurozone and the UK economies, economies that account for the bulk of EU GDP. Although eurozone MFI credit is growing, its growth is much slower than it was prior to the global recession. UK MFI is contracting. With all the problems associated with European sovereign debt, EU banks will be cutting back on their already miserly lending in anticipation of sovereign-debt write-downs. Hence EU MFI credit growth will slow more or contract, prolonging the EU recession.

Of course, the European Central Bank (ECB) could step in to create some of the credit that EU MFIs otherwise would be creating under normal circumstances. But the ECB fears that quantitative easing would somehow sully its Bundesbankian reputation. How ironic that the ECB, a central bank ostensibly sympathetic to an Austrian approach to monetary policy, would not try to maintain a normal amount of credit creation when MFIs were unable to do so. Europeans, get ready to join your Japanese brethren for a lost decade. It did not have to happen for the Japanese and it does not have to happen for the Europeans. But given the intransigence of Japanese and European central bankers (with the exception of British central bankers), it will..

Paul Kasriel is the recipient of the 2006 Lawrence R. Klein Award for Blue Chip Forecasting Accuracy

by Paul Kasriel

The Northern Trust Company

Economic Research Department - Daily Global Commentary

Copyright © 2011 Paul Kasriel

Paul joined the economic research unit of The Northern Trust Company in 1986 as Vice President and Economist, being named Senior Vice President and Director of Economic Research in 2000. His economic and interest rate forecasts are used both internally and by clients. The accuracy of the Economic Research Department's forecasts has consistently been highly-ranked in the Blue Chip survey of about 50 forecasters over the years. To that point, Paul received the prestigious 2006 Lawrence R. Klein Award for having the most accurate economic forecast among the Blue Chip survey participants for the years 2002 through 2005.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

Paul L. Kasriel Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.