High Risk 125% and 100% Mortgages Disappearing

Personal_Finance / Mortgages Feb 22, 2008 - 05:33 AM GMTBy: MoneyFacts

By the close of play yesterday four of the six lenders that were offering 125% loan to value mortgages had announced that they were to withdraw these higher risk home loans. Alliance and Leicester, Coventry BS, Godiva Mortgages and Abbey are all set to pull these deals this week. Julia Harris analyst at moneyfacts.co.uk investigates:

By the close of play yesterday four of the six lenders that were offering 125% loan to value mortgages had announced that they were to withdraw these higher risk home loans. Alliance and Leicester, Coventry BS, Godiva Mortgages and Abbey are all set to pull these deals this week. Julia Harris analyst at moneyfacts.co.uk investigates:

“The only two lenders left in the 125% market are Northern Rock who have already priced themselves out of the market and Birmingham Midshires Solutions who lend solely through intermediaries. “But it’s not just 125% deals that are being pulled, 100% deals are also becoming more expensive and much harder to find.

“In November 2007 41 of the 123 prime mortgage lenders were offering mortgages at 100% LTV or more. Since then almost one third of those lenders have withdrawn their products from the market leaving only 28 providers. Those that still operate in this market include those that only lend 100% or more to professionals or as part of specialist arrangements such as the shared ownership scheme.

“This is yet another example of lenders continuing to tighten their belts even further in what has become a vastly different mortgage market from this time last year.

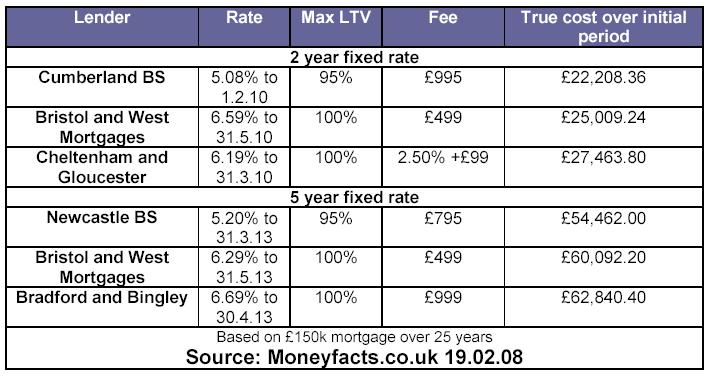

“Prospective first-time buyers are those that are going to be most affected by this move. Not only are there fewer options for those without a deposit but they will also find themselves having to pay a larger premium for the added risk that the lender is taking on. The table below highlights the additional costs of a 100% mortgage compared to a situation where you are in a position to provide a 5% deposit.

“With house prices starting to cool and some commentators predicting a further drop as the year unfolds, perhaps it is time to make the most of the current high savings rates and save for that deposit.

Moneyfacts.co.uk is the UK's leading independent provider of personal finance information. For the last 20 years, Moneyfacts' information has been the key driver behind many personal finance decisions, from the Treasury to the high street.

www.moneyfacts.co.uk - The Money Search Engine

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.