Effects of Malaysia Credit Squeeze on the Housing and Stock Market

Stock-Markets / Credit Crisis 2013 Aug 11, 2013 - 01:23 PM GMTBy: Sam_Chee_Kong

Malaysia’s current Household debt problem is not the result of our government’s recent policies to encourage private expenditure. In actuality the current debt problem has been accumulated from the past 15 years. The history of Malaysia’s Household debt can be traced back to 1997 where the household debt to GDP was only 39% then. This was also the year Malaysia is engulfed by the Asian Financial crisis.

Malaysia’s current Household debt problem is not the result of our government’s recent policies to encourage private expenditure. In actuality the current debt problem has been accumulated from the past 15 years. The history of Malaysia’s Household debt can be traced back to 1997 where the household debt to GDP was only 39% then. This was also the year Malaysia is engulfed by the Asian Financial crisis.

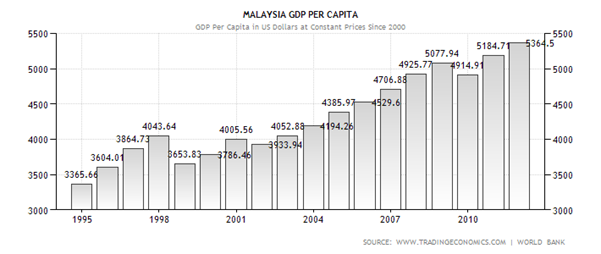

Since then Malaysia embarked on an expansionary fiscal and monetary policy which led to an expansion of credit and also the proliferation public projects so as to extract its economy out of the recession. During the Asian Financial Crisis in 1999 Malaysia’s GDP per capita felled to $3653.83 compared to $4043.64 recorded in 1998. However since then as the expansionary policies worked its way into the economy, Malaysia’s GDP per capita risen as a result. This can be shown by the following graph on Malaysia’s GDP per capita since 1995.

To encourage the private sector to spend, lending procedures are relaxed and interest rates are held low. As a result of the increases in both private and public expenditure, Malaysia’s GDP recorded a fourfold increase in 2012. In 1999, Malaysia’s GDP was valued at $72.175 billion and has since risen to $303.53 in 2012. This can be shown by the following chart.

However, the credit expansion brought about by our government earlier has led to a further increase in the household debt. As of 2010 Malaysia’s household to GDP debt has reached 78% where more than 55% of the loan concentration is in the mortgage market and 23% into the automotive market. And in 2012 the ratio went up to 83% which represents an increase of 13% from 2011.

Our next question is what contributed to our record Household Debt?

- False Expectation of improved economic conditions brought about by our Government. We have mentioned many times in our previous articles that our Government has been painting a false picture on the real condition of our economy. With the aid of the media we are led to believed that our economy is growing at a healthy pace (GDP growth of 4.1%), our stock market is resilient, our housing market is healthy and sustainable (no bubble yet) due to the increasing rural to urban migration of the workforce and so on.

- The easy availability of credit in the past and the lack of supervisory on the part of Bank Negara had led to an enormous build-up of the private sector debt. We shall present again the following chart which we have already mentioned in our last article titled ‘Is our GDP growth a Hoax?’

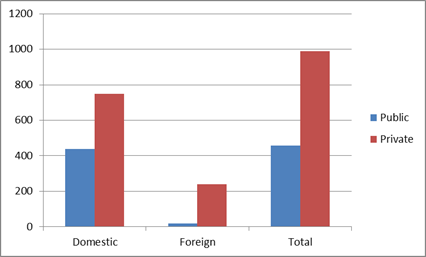

The following is the chart for the total debts by the private and Government sector as of 2011.

Debt |

Domestic |

Foreign |

Total |

Public |

438 |

18 |

456 |

Private |

749 |

239 |

988 |

Given the GDP of RM 860 billion we can then proceed to calculate the Debt/GDP ratio of both the public and private sector. The table below summarizes the ratio of domestic and foreign debts held by the public and private sector.

Debt |

Domestic |

Foreign |

Total |

Public |

51% |

2% |

53% |

Private |

87% |

28% |

115% |

From the above we can conclude that at the present moment the private sector poses a greater risk to financial default than the public sector. This is due to the fact that the private sector is much more exposed to any downside risk, arising not only from size of the debt (87%) but also its exposure to foreign debt (28%). Large exposure to foreign debt is risky because it is subjected to movements in foreign currency (US$ in this case) or external systemic market risk.

The movement of the US dollar creates currency risk or what we called ‘Foreign Exchange Exposure’ in Treasury terms. Foreign Exchange Exposure refers to the risk associated to a decline in a country’s currency. Currency depreciation can have the effect of reducing a company’s profits due to increased cost in imports or loss due to the higher repayments of loans denominated in US dollar.

How big a loss associated with currency movement depends on our Ringgit. On the negative node our country is currently running a ‘Twin Deficits’. Twin Deficits refers to a situation when we are having two economic problems at the same time (Budget Deficit + Balance of Trade Deficit). Twin deficits are known to create havoc in an economy by accelerating the decline of a country’s currency and in this case the Ringgit. So, obviously the risk of default in our private sector has certainly increased due to the problems coming in from multiple fronts.

- A boom in the Housing and Stock Market. The boom in the housing and stock market for the past couple of years has increase the risk appetite of investors. Somehow they reckoned they have found a way to make money without putting much work. To them making money can be as easy as sitting in the stock market and pressing some buttons or flipping some real estates. Hence this led to many of them holding to a portfolio of 3 to 4 houses which risked being wipe-out should there be a serious downturn in the real estate market.

- A strong response from the private sector especially from the business community to increase their exposure to debt due to the expectation of better times ahead.

Problem with ARMs Mortgage

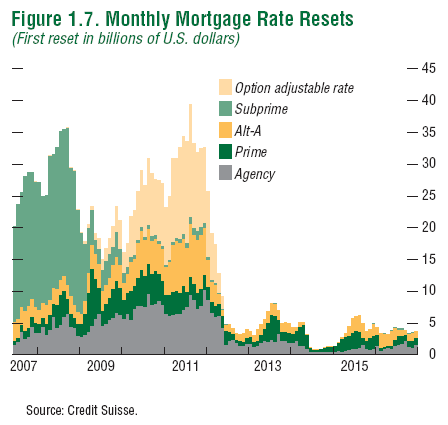

Another problem we are facing is that about 80% of the loans given to the housing market are in the ARMs (Adjustable Rate Mortgages) category which is also known as ‘teaser loan’ in the U.S. To lure prospective borrowers, banks offered very low initial repayments (such as BLR – 2 to 4%) during the first 3-5 years. Once that duration expires or resets then borrowers will have to start paying higher mortgages. That’s where the nightmare comes in.

For example, a RM 200,000 loan with tenure of 20 years, the initial repayment can be as low as RM 800 a month. When the 3-5 years period expires, the loan will be automatically resets to higher interest rates, probably (BLR + 0%) and repayment will be more than RM 1000 per month. One thing to remember is that ARMs is one of the major contributors to the U.S Housing meltdown. The following is the U.S Monthly Mortgage Rate Resets.

As can be seen above, the U.S housing crisis is yet to be over as the mortgage resets will continue beyond the year 2015. As for Malaysia our total housing loans has risen to MYR 222.2 billion from about MYR 25 billion in 1996.

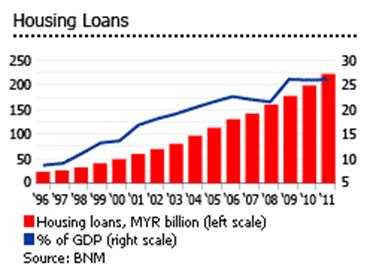

Below is the chart for the housing loans to GDP as from 1996 to 2011.

It shows that the outstanding housing loans has been on the rise since 1996 and reached MYR 222.2 billion in 2011 or around 26.1% of GDP, up 11.8% from a year earlier.

An oversupply of Housing?

According to C.H. Williams Talhar & Wong, there is an oversupply of high-end condominiums in Malaysia especially in Kuala Lumpur, Johor Bahru, Kota Kinabalu, Kuching and Penang. The following chart shows the relationship between the housing approval and oversupply.

The over-supply of high-end condominiums remains a concern while a further 2,300 units of high-end condominiums will be completed in 2012, half located in the Kuala Lumpur City Centre (KLCC).

In total, around 54,557 properties were unsold at end-2011, down 2.3% on the previous year, and down 34.9% from the 2004 peak of 83,811 units. There was a 62.3% decline in house launches during the year to Q4 2011. It clearly shows that the housing market is already softening since the end of 2011. Moreover, we also received reports from real estate agents complaining that high-end properties (over MYR 1 million) are very sticky or difficult to sell.

Bank Negara Malaysia’s new measures

We are certainly living in interesting times. Fundamentally, our economy is weak. Our exports are plunging, our trade balances and deficits are negative and the only things that are going up are our companies bankruptcy that is on record territory, stock market, consumer spending, inflation, private and public debts. It seems like things are moving in opposite directions. Positive economic indicators are moving down while negative economic indicators such as inflation and household debts are moving up.

In view of our credit expansion problems, Bank Negara Malaysia (Central Bank of Malaysia) is implementing the following measures to curb the excessive debt incurred on the private sector namely the Household and Housing sector with immediate effect (06/07/2013).

- Reducing tenure of housing loans from 45 to 35 years

- Limiting tenure of personal loans to the maximum of 10 years.

- Prohibition of offering pre-approved personal financing products.

Before we address the effects of the above measures, we would like to digest what Bank Negara hoped to achieve with the above measures. In short, Bank Negara is trying to reduce the banking sector’s exposure to real estate and personal loans. In trying to do so, it is employing a strategy known as ‘shortening of maturities’. This can be literally translated in plain English as ‘the government is more concerned with short term instability than promoting long term growth’. In part, these measures we believe are also directed towards resolving our big budget deficits and Government Debt to GDP problem. Again these problems are due to our excesses in the past few years of credit expansion.

So how will the Government going to fix this problem? Our Government hoped that by reducing the credit, it will help reduce domestic consumption on consumer goods and real estate and at the same time try to expand the exports. This in time will helped reduce the trade balance due to the increase in exports and decrease in imports. By this our Government hoped to help built a sounder economy with a better income foundation and lesser debts.

However along the way a lot of people are going to get hurt due to the credit squeeze but there is no other choice if we want a transition to a better and more sustainable economy. Hopefully, more resources will be directed towards the more efficient part of the economy such as building more plants, better infrastructure, modernising production facilities or anything that can help the economy to make real products which can be used for domestic consumption or exports which will in turn earn foreign exchange. Our next question is will it work?

Will it work?

It appears that Bank Negara is definitely worried on the banking sector’s exposure to real estate. Any big downturn in real estate prices will definitely have profound effects on the economy. Among them are unemployment resulted from the construction related business and also the growth of NPLs in the banking sector. Below are the problems that may arise as a result of the latest measures.

Limitations to Monetary Policy – Long Lag

Central Banks have always been prudent in their approach towards the economy and that is the main problem. Sometime they waited too long before they act or when the problem is evidently long in its tooth. The slow response may be due to the problems associated with monetary policy implementation and they are the long-lag response and genie out of the bottle response. Monetary policy such as increasing the interest rate to counter inflationary pressure might take 6-9 months to work its way into the economy. If they waited until the inflationary effect is visible to us then it is already too late because the inflationary effect has already accelerated too much and the interest rate increase will have not much effect in contracting the economy.

Similarly to what is happening in Malaysia. Bank Negara should have taken action many months ago to stem the borrowing to the private sector and not waited until the problem becomes obvious. Now when they starting to take action, the genie is already out of the bottle and it is all but one hell of a difficult task to stuff the genie back into the bottle. The above measures will only have effects on new loans, how about the old ones?

Problem with our Shadow Banking System

This I would like to point out that as in many other countries we also have two different banking systems. One is called the formal banking where their operations are regulated by Bank Negara and the other one is the informal banking which is unregulated by Bank Negara. The informal banking system or Shadow Banking System consists of lending from private money lender and credit companies, inter-company loans, corporate bonds and loans by investment companies

Due to the current credit squeeze those who are unable to qualify for loans in the formal banks will turn to the informal banks. There are already a lot of evidence of individuals and SMEs and even developers are getting loans from the informal banks where maturities are short and interest rates are high. The problem is we do not know how large our informal banks are and what type of portfolios they are holding. Another problem is we do not know what sort of linkage or relationship between the formal and informal banks. If they are linked and if our real estate market were to collapse then the resulted decline in real estate prices will be serious, due to the following.

- There will be force sell of real estate financed by the informal banks. This self-reinforce selling will further depress the prices of real estate. This is the last thing our Government wants because when the informal banks start to liquidate their assets to raise cash then it will cause further downward pressure on the market

- Informal banks may have got their funding from the formal banks. So any credit squeeze will certainly have effect on the operations of the informal banks which might force them to shorten the maturities, recall or totally freeze their loan operations.

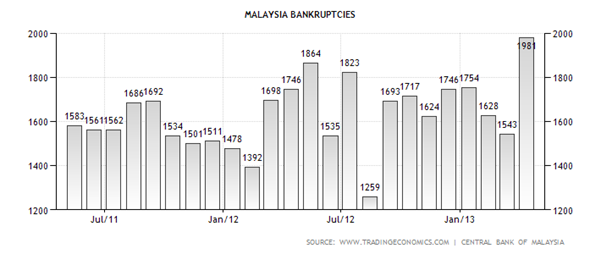

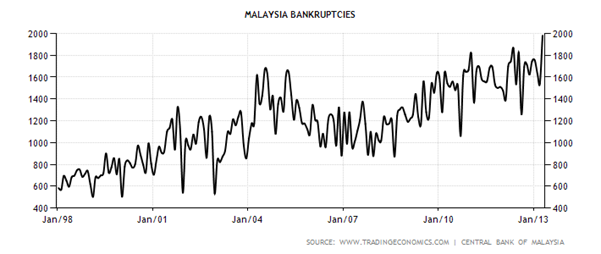

Without funds to finance their operations, many businesses may have to cease their operations. With the expected softening of the real estate market developers who have been snapping up land to build up their land banks will find it difficult to stay afloat. This can be shown with the following chart on bankruptcies in Malaysia from April 2011 to May 2013.

As from the two charts above, Malaysia recorded an increase in company bankruptcy. Total company bankruptcies reached a high of 1981 companies in April 2013. This is the highest ever number of bankruptcies recorded since January 1998. In view of the credit crunch we expect to see much more bankruptcies in the month ahead.

Hence, such risk is real and is already happening. Credit squeeze means there will be lack of funds available to individuals and companies and hence liquidity. Since liquidity is the lifeline of both the housing and stock market, a lack of it will definitely have profound effects on them. Lacked of liquidity will cause seizing up of transactions because of the negative expectations on the economy will make people and businesses lee willing to spend, which eventually will drive prices down. Even before the implementation of the credit squeeze the housing market has already shown signs of weakness.

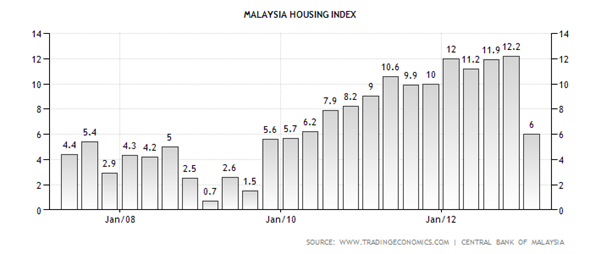

The Housing index refers to the residential construction activity during a period of time. As indicated by the housing index below, our residential construction activity has declined to 6% in the first quarter of 2013 from 12.2% recorded in the last quarter of 2012. It represents more than a 50% drop on a quarter to quarter basis. At 6% it brings us back to the level recorded in the early 2010 when our economy is just started to recover from the Global Financial Crisis in 2008. This big drop in housing activity certainly worries the authorities and which might be attributed to the over-leveraged consumers and also the peaking of the housing prices.

Housing prices in Tier-1 cities in Malaysia namely Kuala Lumpur, Penang and Johor Bahru has seen an unprecedented rise due to the easy availability of credit that resulted in a speculative frenzy. Any investment that is buoyed by easy credit especially housing and the stock market will eventually end up in a bubble. Despite numerous denials by our authorities the housing market in Malaysia has long been in a bubble.

As for the Stock Market we are saying it again. Sell and walk away. From the chart the market has been on the Distribution phase since 05/05/2013. We have drawn two lines that represent the distribution area and we will expect the market to breakdown from the lower line in the coming weeks. By then you will see an extremely volatile market.

Due to the credit contraction we are expecting a continuation of decline into the next few months. Any rebound will be another bear trap and we are seeing a much lower index in the next few weeks and month. In short we are BEARISH.

by Sam Chee Kong

cheekongsam@yahoo.com

© 2013 Copyright Sam Chee Kong - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.