Gold Price is Going Higher Whether or Not FED Tapers

Commodities / Gold and Silver 2013 Aug 29, 2013 - 11:21 AM GMTBy: Jason_Hamlin

The Federal Reserve is in a very tough position. Despite unprecedented amounts of stimulus, GDP growth is anemic, unemployment remains historically high, durable goods orders have plunged and rising rates are harming the housing rebound. If this is all that can be accomplished with record low rates and trillions in quantitative easing, the underlying health of the economy must be magnitudes worse than believed.

The Federal Reserve is in a very tough position. Despite unprecedented amounts of stimulus, GDP growth is anemic, unemployment remains historically high, durable goods orders have plunged and rising rates are harming the housing rebound. If this is all that can be accomplished with record low rates and trillions in quantitative easing, the underlying health of the economy must be magnitudes worse than believed.

Most analysts are expecting the FED to taper in September, significantly reducing their $85 billion per month in asset purchases. While it is easy to throw around dollar amounts such as $85 billion, we should put this number into context. $85 billion per month is over $1 trillion per year and is equivalent to over 20 million new jobs paying $50,000 per year. It is enough to end world hunger 30 times over or send every high school student to a four-year college.

Yet, despite spending this unfathomable amount of money on quantitative easing, the economy only grew at 1.7% during the second quarter. Can you imagine the condition of the economy today if the FED was not buying $85 billion in bonds per month?

Interest rates would skyrocket, the stock market would collapse, the housing market would collapse, credit markets would freeze up, unemployment would skyrocket and foreign nations would very well accelerate their dumping of U.S. debt.

Sound dramatic? I am not the only one that holds such views. The Federal Reserve essentially hoisted a trial balloon earlier this year by discussing the possibility of tapering to the media. What transpired was an immediate and severe sell-off in the stock market at only the hint of the possibility of future tapering. Imagine the impact when the FED actually confirms the beginning of tapering!

Employment Data Suggests More QE is Needed, Not Less

The FED has a dual mandate of maximum employment and price stability. They have discussed not tapering until official unemployment drops to 6.5%, but it still remains at 7.4%. And even this historically high number of 7.4% does not paint the total picture of the employment situation in the United States.

The better measure of unemployment, U6, is hovering around 14%. If we use a more honest measurement, such as the one calculated by Shadowstats to include long-term discouraged workers that conveniently get defined out of existence in government models, unemployment is at an all-time high around 23%!

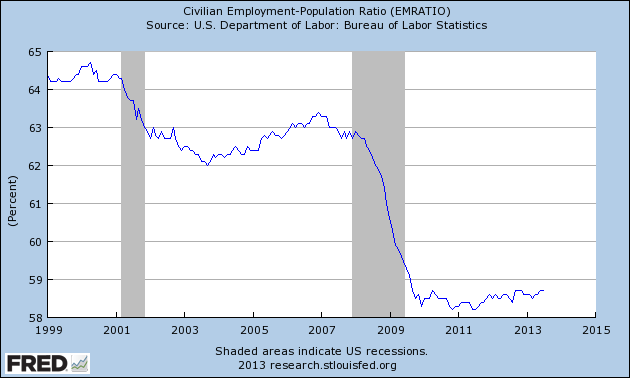

Another good way to get an accurate understanding of the health of the jobs market is to look at the civilian employment-population ratio. In very simple terms, it tells us what percent of working-age Americans have a job. It was around 65% in the year 2000. Following the bursting of the dotcom bubble in 2001, the ratio dropped three points to 62%. When the 2008 financial crisis hit and the recession took hold (grey area in chart below), the rate dropped sharply from 63% to below 59%. This drop was nearly twice as severe as the one that followed the 2001 dotcom recession. But here is the real kicker… the employment-population ratio has remained below 59% for 4 years now and has failed to recover at all, following the 2008/2009 recession.

This is the first time in modern history that there hasn’t been a strong bounce back in the employment market following a recession and it is an ominous sign for the future. Simply put, there has been no real recovery in the labor market.

Official Measures of Inflation Remain at Historically Low Levels

While you may not feel it when shopping for groceries, pumping gas or buying health insurance, official indicators are showing that both headline and core CPI remain below 2%. This is not the type of inflation that would compel the FED and policymakers to back off stimulus programs. In fact, this level of inflation is technically lower than desired, suggesting that there is room to increase stimulus efforts without causing runaway inflation.

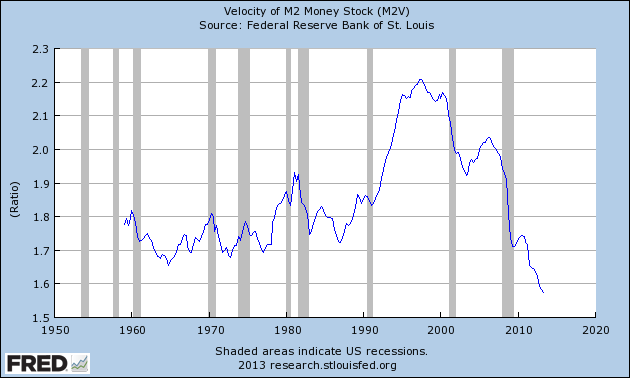

This is contrary to what many gold investors had expected following the trillions in bailouts and money printing in 2009. The main reason all of this new money has not yet translated into high inflation has to do with the velocity of money. This term is used to describe the pace at which money is circulating through the economy and being used to buy goods and services.

The chart below shows that the velocity of money has fallen to the lowest level ever on record. It went into free fall during the latest recession and has continued dropping towards the 1.5 level as banks park assets with the FED in order to collect interest on excess reserves. Corporations are also sitting on record amounts of cash, as their hiring and spending has slowed in the face of a tepid economic recovery.

So, with both of the FED’s mandates pointing towards the need for more quantitative easing, not less, why are so many investors and analysts convinced that the FED will begin tapering next month?

Perhaps it is because of the subtle hints the FED has been dropping or maybe central bankers want investors to believe the story of an improving economy that no longer needs stimulus. Whatever the reason, it is a delicate balancing act needed to keep confidence high and prevent the house of cards from collapsing. Investors are getting used to it now, but not long ago the idea of a centrally-planned economy hinging on the words and whims of a bearded banker would have been hard to foresee. Sure, Greenspan and others had incredible sway in the markets, but there was still a sense that the main driver was the underlying fundamentals, not the amount of stimulus the FED would inject during any given month.

While the majority are bracing for significant tapering next month, my analysis of the situation suggests the exact opposite. I believe there is very little chance of tapering in September or even by year end. I have always suspected that QE3 was actually “QE to Infinity,” so I would not be surprised to see an increase in bond buying or the announcement of a new stimulus program meant to keep the lights on a while longer.

What are the Implications for Gold Investors?

A substantial portion of the recent decline in precious metals was driven by forecasts for an end or significant tapering to FED bond buying. This forecast was slowly baked into gold and silver prices during the first half of 2013, leading to multi-year lows amidst the worst correction of the entire 12-year bull market. But was the sell-off justified?

The recent price action suggests the correction was severely overdone. And while the move over the last two months has been impressive, the real fireworks will begin when the FED concludes their September meeting without an announcement of tapering. Even more explosive would be news that the FED plans to increase their quantitative easing efforts in order to push rates back down, increase borrowing and spur hiring in the job market.

But even if the FED does decide to taper this year, it will only be a token amount aimed at pleasing opponents of QE and those rightfully concerned about the expanding balance sheet of the FED and deepening national debt levels. Would the FED buying $70 billion per month instead of $85 billion per month be cause to turn bearish on precious metals or equities in general? What about $65 billion? No matter the number, it is still an incredibly large and absurd amount of economic stimulus required years into the supposed recovery.

Some may view any degree of tapering as proof of a strengthening economy and foreshadowing of a rebound in the velocity of money. In such conditions, inflation indicators are likely to spike higher and spread fear that all of the money printed in the past 5 years will finally begin flowing into the markets. This scenario would also be bullish for precious metals, leading me to believe that prices are headed higher whether or not the Federal Reserve decides to taper.

Summary and Conclusion

I believe that investors have incorrectly assumed the FED will announce significant tapering in September. This concern has spread through the markets over the past several months and is now baked into gold prices. However, if my hypothesis is correct and the FED does not taper in September as expected, look for a continued upward revision to gold and silver prices. In the short term, this upward trajectory will likely be accelerated by increasing tensions in the Middle East and the potential of a new war with Syria.

While I advocate holding physical metals in your possession first and foremost, the value currently being offered by mining stocks is hard to ignore. If mining equities continue their recent leveraged performance to the underlying metals, we will see some very explosive moves in quality companies with high grades and low costs. They will benefit not only from higher gold prices and recent programs to reduce cash costs, but from a newfound bullishness in equities overall following the realization that the FED will not be taking away the easy-money punch bowl anytime soon.

After an uneventful and sometimes painful two years for precious metals investors, there is now very little downside risk and huge upside potential. A return to previous highs would mean a 35% gain for gold, 100% gain for silver and tripling or quadrupling of the share price for many mining stocks.

To view the Gold Stock Bull portfolio, receive our highly-rated newsletter and get regular updates on the stocks that we believe will generate the greatest gains during this next upleg, click here to sign up for the Premium Membership.

By Jason Hamlin

Jason Hamlin is the founder of Gold Stock Bull and publishes a monthly contrarian newsletter that contains in-depth research into the markets with a focus on finding undervalued gold and silver mining companies. The Premium Membership includes the newsletter, real-time access to the model portfolio and email trade alerts whenever Jason is buying or selling. You can try it for just $35/month by clicking here.

Copyright © 2013 Gold Stock Bull - All Rights Reserved

All ideas, opinions, and/or forecasts, expressed or implied herein, are for informational purposes only and should not be construed as a recommendation to invest, trade, and/or speculate in the markets. Any investments, trades, and/or speculations made in light of the ideas, opinions, and/or forecasts, expressed or implied herein, are committed at your own risk, financial or otherwise. The information on this site has been prepared without regard to any particular investor’s investment objectives, financial situation, and needs. Accordingly, investors should not act on any information on this site without obtaining specific advice from their financial advisor. Past performance is no guarantee of future results.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.