Ten Pillars of Financial Independence

Personal_Finance / Debt & Loans Jan 21, 2014 - 02:40 PM GMTBy: Don_Miller

Young folks can usually digest a difficult message more easily when it comes from someone who is not: (a) their parent; (b) their teacher; nor (c) anyone else whose lectures they are sick of hearing. In that spirit, we're starting out 2014 with 10 ways people of any age can safeguard their financial independence. Please feel free to pass it along to anyone in your life who could use a nudge in the right direction from someone other than Mom and Dad.

Young folks can usually digest a difficult message more easily when it comes from someone who is not: (a) their parent; (b) their teacher; nor (c) anyone else whose lectures they are sick of hearing. In that spirit, we're starting out 2014 with 10 ways people of any age can safeguard their financial independence. Please feel free to pass it along to anyone in your life who could use a nudge in the right direction from someone other than Mom and Dad.

Wealth is not gauged by how much money you make, but rather how much you keep. Accumulating wealth, regardless of your age, gives you options and independence. It's sad when people toil in jobs they hate because they need the money. Anyone in that position finds their employer controls their time and, sad to say, much of their happiness (or lack thereof).

We all want to be free to enjoy our lives in the manner we choose. Those who manage to achieve this state of nirvana have internalized these 10 pillars.

Pillar #1: Do Not Make Debt a Way of Life

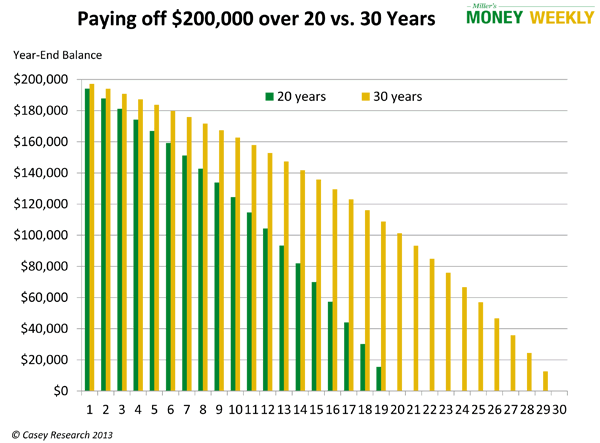

Debt is enemy number one of financial independence. Let's take a look at the most common form of debt, a home mortgage.

Joe and Suzy are in their late 20s with a young family. They're tired of paying ever-increasing rent and want to buy a home. They sacrifice and save $50,000 for a down payment on a $250,000 home.

Joe and Suzy chose from two mortgages, both charging 5% interest. One is based on a 20-year amortization, and one has a 30-year amortization. How much will the home really cost them?

If they choose the 20-year mortgage, their payments are $1,319.91 per month. If they choose the 30-year mortgage, their payments are $1,073.64 month—$246.27 lower. By choosing the lower payment, they're adding $69,732.00 to the cost of their house. Why did it cost so much more? Because of the rent they paid on the money they borrowed for another decade. Had they been able to make the higher payments, they would have 10 years with no house payments to accumulate wealth for retirement.

If, instead of paying the mortgage, they saved $1,319.91 a month for the next 10 years after they're done with the home loan and earned 5% interest on their savings, they'd end up with $204,958.63 in savings at the end of the tenth year.

Therefore, their choices are to sacrifice a bit now so that in 30 years they have a home paid for and $204,958.63 in the bank, or a slightly smaller house payment and a home paid for without a good start on their nest egg. Many of the choices you make 10-20 years ahead of retirement can pay off very well when you want to retire.

I'm a firm believer in paying for your home as soon as possible. Unfortunately, beginning with a starter home and moving up to McMansion after McMansion has become commonplace; this habit can make it practically impossible to pay off your home in a timely fashion.

Pillar #2: Saving and Wealth Accumulation Are Different

Some of the happiest folks at our 50th high school class reunion still lived in modest homes in nice neighborhoods which they had bought in their 20s and 30s. These homes had been paid off for years, and they managed to accumulate a lot of wealth when they no longer had to make house payments.

On the other hand, those who bought McMansions were trying to sell and downsize in a down market. They needed equity from their homes to enjoy financial independence in their golden years.

Financial independence and happiness comes to those who live within their means and make wealth accumulation a major priority. Financial independence is relative, and your attitude plays a big role. For some, financial independence means living in a doublewide in a 55-plus community; for others, it means million-dollar homes and five-star travel. My wife and I have friends in both camps, and it makes no difference: they have all put themselves in a position to enjoy a lifestyle they can afford without major financial worry.

Pillar #3: Never Go into Debt to Buy a Toy

This is a personal favorite. Whatever your toy of choice—a boat, motorhome, four-wheeler, you name it—if you want it badly enough, save the money to buy it. Interest rates on toys are exorbitant because they depreciate so rapidly. I have too many friends who borrowed thousands of dollars for a boat, made extra payments, and still had to write a check to the loan company when they sold it. I get it! It's damn tempting, but just don't do it.

Pillar #4: Consider the True Cost, Not the Monthly Payment

This is tough when you have the hots to buy something. If you cannot purchase something outright, its true cost includes the price of renting someone else's money, plus the depreciation.

Thinking in terms of monthly payments can keep a person in economic slavery for life. We've all seen folks get a nice raise and immediately buy more cool stuff because they now can afford more monthly payments. This is nothing more than a treadmill of earning income and making payments, with little chance of real wealth accumulation.

We're investors in Lending Club and see hundreds of loan applications from people who've finally realized that financial independence requires accumulation of wealth, not stuff. They borrow money to consolidate their debt, cut up their credit cards, and try to get back on track. This can easily take 5-10 years for folks with massive debt. If they finally get it at 50, they may have to set retirement back a full decade or more.

Pillar #5: Wants Are Not Needs

Wealth accumulation and financial independence must trump the "need" for stuff. Throw off the economic shackles! Financial freedom is attainable if you free yourself from stuff.

Pillar #6: You Are Responsible for Your Own Behavior

If you've ever been the parent of a teenage driver, at one point or another that teenager likely received a speeding ticket. The commonsense solution: make the teenager pay the ticket and any increase in the insurance. He who creates the problem should create the solution.

Pillar #7: Behavior Has Both Short- and Long-Term Consequences

By our 50th class reunion, we'd lost many classmates to lung cancer. These were the same kids who'd laugh as they lit up a cigarette and call them "cancer sticks." They were quite right. Incredibly, many of them, knowing the risk, smoked right up until the end; they didn't change their behavior and suffered the consequences.

It's not like big spenders don't know the consequences of not saving; they've heard the message before. Yet they continue the same behavior and end up with a predictable result: little to show for their efforts at the end of their working career. Some people justify their behavior by thinking they can live on Social Security post-retirement. The few I know who are in that situation are not financially independent; they're back working at lower-paying jobs they can ill afford to lose.

Pillar #8: No One Owes You Squat!

If you think anything is owed to you, prepare yourself for a rude awakening. Yes, that means you are responsible for your own retirement, health care, and everything else you need. While you may have a pension or guaranteed healthcare plan today, check the promises made by the government or your employer. Many of those promises are impossible to keep.

Too many people retired counting on their pensions—public and private. These folks kept up their end of the bargain, but that makes little difference when there's no money to pay them. Future generations need to learn from those mistakes.

Some friends recently told us their children got jobs at the police and fire departments. They were pleased because they thought they could work hard, earn a decent living, and have a nice pension waiting for them in a few decades. Ask anyone who worked for the City of Detroit what they think about that plan.

Don't spend your money thinking you can count on others to support you in your old age. They might, but you'll lose your independence and probably not be happy. Too many people in this situation have never learned to save; they allowed someone else to do it for them. Save more than the minimum. You will never regret it.

Pillar #9: Something for Nothing Teaches a Bad Lesson

We've all heard stories of people winning millions in the lottery and quickly going broke. Ever heard of "Sudden Wealth Syndrome?" There is such a thing, and it's completely related to a huge (often unearned) windfall.

Why do seemingly intelligent people who suddenly have a lot of money blow it? Their first reaction is to look at all the cool stuff they can buy. If you win $10 million and buy a $2 million home, you still have $8 million left. Then again, if you also bought a $1 million boat you still have $7 million left, much more than you ever had before. That rationale soon leads people right down the drain, and the money is gone.

Pillar #10: Live off the Interest and Never Touch the Principal

I saved the most important pillar for last.

In the case of lottery winners going bust, it's almost always the same: If you won $10 million and invested it wisely, you could easily net $500,000 a year while your portfolio grew ahead of inflation. In most cases, the income from their winnings could provide a phenomenal lifestyle. And they could pass along the money and sound financial principles to their children.

I recall Johnny Carson discussing having a lot of money with Bert Reynolds. Carson commented, "Having money means you never have to worry about money." While that contains some truth, it's an oversimplification. You also don't have to worry about all the things you have to do to earn money. That's what causes stress and takes years off of our lives.

Having money is important, but it's only part of the puzzle. Understanding what money means, what it can do for you, and prioritizing wealth accumulation are also critical pieces.

If I have to make a choice between leaving my children and grandchildren with money or the basic principles of growing and maintaining wealth, I'd choose the education every time. It will make them hell-bent on keeping the money they earn and educating the next generation to do the same.

If you're of a like mind and want to give the gift of a financial education, click here to share a premium subscription to Miller's Money Forever with a loved one. Call it a belated holiday gift—no wrapping required.

© 2014 Copyright Casey Research - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Casey Research Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.