9 Ways to Retire Rich

Personal_Finance / Pensions & Retirement Oct 14, 2014 - 03:32 PM GMTBy: Don_Miller

“In theory there is no difference between theory and practice. In practice there is.”—Yogi Berra

“In theory there is no difference between theory and practice. In practice there is.”—Yogi Berra

It’s October, AKA the major league baseball postseason. As a lifelong baseball fan, I take the wisdom of Yogi Berra seriously. And when it comes to planning for the autumn of life, Yogi is spot on.

It seems as though every day an article titled “5 Tips for Retirement Saving” or something similar hits my inbox. I scan for the author’s name, and I’m amazed by how often it’s distinctly contemporary—Jennifer, Brandon, or another name of that vintage. Jennifer’s title is something like “staff writer,” and I immediately picture a fresh-faced young person with a newly minted journalism degree. After work, maybe she jumps in her starter BMW and heads to a local watering hole with her friends to gripe about student loan repayments.

“Jennifer” means well. After all, she’s just doing her job. She recommends setting financial goals, getting out of debt, living within your means, and saving from a young age. I won’t argue with those recommendations. Jennifer’s grandparents probably did just that. If you can pull off following that advice to a T, chances are you’ll accumulate a good deal of wealth.

However, once Jennifer has tried to put her advice to practice for a couple of decades, she might understand that it’s neither simple nor easy, despite how it might sound. Most people know what they should do, but it’s often tough and painful to execute in real life.

During my 74 years I’ve met a lot of successful and rich retired friends who sure didn’t go about it Jennifer’s way. How many baby boomers do you know who married young, raised a family, put their children through school, and consistently saved in their 20s, 30s or even 40s? There are a few, but many—if not most—young families lived through a decade or more of “Why is there is so much month left at the end of the money?”

Several times a month a 50- or 60-year-old Miller’s Money subscriber writes in asking for help with how to accomplish a last-ditch push to save. Truth be told, most of my friends never got serious about retirement until after they’d raised children. It doesn’t mean they were right; it’s just the way it was. Should they have started earlier? Of course. But they didn’t. Some didn’t know how, some were overwhelmed by day-to-day expenses, and some overspent on stuff, stuff, and more stuff. Many got serious in the nick of time, but they did it.

Retiring Rich When You’re Under the Wire

Whatever your age, fretting about what you didn’t do is futile. Start making the needed changes today.

The best place to begin is to define “rich.” For our team, rich means having enough money to choose whether or not to work and enough money that you control your time. Rich means you live comfortably according to your personal standards. If you’ve lived a middle-class lifestyle, a rich retirement means you can maintain that same lifestyle without worry.

Ten days out of high school, I was on a train to Parris Island, South Carolina. One of the best teachers I ever had was SSgt. Thomas R. Phebus. He was an archetype—the ideal combination of common sense and straight talk. I’m going to take a page out of his book and share some straight talk on how to make a rich retirement your reality.

The 9-Step Program

#1—Saving money is a *****! When I entered the work force, every major company and most government agencies offered some sort of pension plan. The bottom line: come work for us at age 25, stay for 40 years, retire at 65, and we’ll continue to pay you until you die, normally another 20 years or so.

Pension plans are no longer the norm. Corporate America just couldn’t do it. Some filed for bankruptcy and broke their promises. Either way, in the private sector, 401(k)s are the new norm. They’re optional—no one makes you contribute.

Now local governments are filing for bankruptcy, many unable to fulfill their pension promises. No matter whom you work for—a big or small corporation, a government agency, or yourself—if you want to retire, be damn sure you’re saving… no matter what you’ve been promised.

#2—Plan to work your tail off. I don’t know anyone who’s accumulated even modest wealth working 40 hours a week. If you want to work for 40 years and pay for 60-plus years of life, chances are you’ll have to do more than that.

When you work, you trade your time, talent, and expertise for money. When you retire, you trade your money for time. In theory, you can work 60 hours a week, live off two-thirds of your income (40 hours’ worth), and invest the remaining one-third (20 hours’ worth). However, if you start saving early, perhaps saving income equal to 10 hours of work will be enough. Your savings will have more time to accumulate and compound, and you’ve bought yourself extra leisure time along the way.

If both spouses are working hard outside the home, which is the norm today, work toward living off of one paycheck and investing the other (or using it to pay off debts and then start investing). Many of our retired friends did just that.

#3—Don’t complain when others have more. Someone always will.

This one saddens me. We have a few friends who chose to work 40 hours a week for most of their working lives. They felt it was important to spend more time at home with their families, and there’s nothing wrong with that choice. Still, it’s a trade-off.

I look at it as though they enjoyed mini slices of retirement time when they were young. If that’s your choice, don’t begrudge others who chose a different path and worked and/or saved more. They don’t owe you anything.

#4—Get out of debt and stay that way. Virtually every wealthy friend I have only started to build wealth after eliminating debt, including home mortgages. Some theory-loving pundits suggest taking out a low-interest mortgage and investing the money with the hope of earning more than the mortgage interest. Oh really? Most people’s investments don’t perform that well.

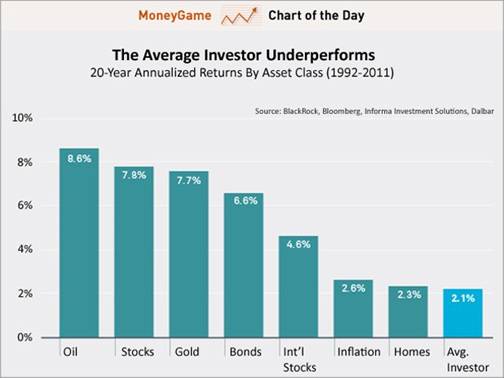

The chart below highlights how poorly the average investor stacks up:

Sure, some beat the odds, but even professional fund managers struggle to do so. As of mid-2013, 59.58% of large-cap funds, 68.88% of mid-cap funds, and 64.27% of small-cap funds underperformed their respective benchmark indices, according to Aye M. Soe, McGraw Hill financial director.

If the big boys have a hard time and the average investor earns just 2.1%, one better secure a darn low mortgage rate before borrowing to invest.

One of the top ways to blow your nest egg is to stop working while you still have a mortgage. Downsize if you have to. Your personal home is not an investment; it’s part of the cost of living.

#5—Get smart while you get out of debt. Commit some of your time to financial education long before you plan to retire. Part of the reason the average investor earns just 2.1% is that many, if not most, haven’t taken the time to learn. If you want to out-earn the average investor, start by investing in education.

Understanding the markets is an ongoing process. The investment world is constantly changing, and if your interests lie elsewhere, it can be a challenge to keep up. A little commonsense scheduling goes a long way, though. Record your favorite programs and watch or listen at night when you’re tired. Then find an hour a day when you are fresh and devote it to more focused study. An hour-long television show has 15-20 minutes of commercials. You can bank that much study time by hitting fast forward.

#6—Set realistic objectives. Get some professional help and a thorough financial checkup so you can set sane targets. With those in place, you can build a realistic plan. The sooner you go through this exercise, the less painful it will be to make any necessary lifestyle adjustments.

#7—Get a grip on your expenses. Investments appreciate (at least that’s the plan). Cars, televisions, and most other stuff depreciate.

Some years ago I read that around 90% of top-of-the-line Lexuses and Mercedes were financed. I live in a community where most of the homes have three-car garages. I shake my head as I drive down the street in my Toyota and see three luxury cars in a garage. I wonder how many of them are financed. It’s easy to have well over $150,000 invested in rapidly depreciating automobiles. With so many long-term auto loans available today, it’s also easy to owe more than the car is worth fairly quickly. Once you get on that treadmill, it’s hard to get off.

All cars are not created equal. I’ve owned my share of luxury autos and can share from personal experience that a routine oil change can cost 10 times more than it does with a Toyota or the like. Is the added prestige of a luxury automobile really worth the extra cost?

#8—Put yourself first. Another common way to blow your nest egg is to spend too much money on others. Your family should not expect you to support them in adulthood, pay for your grandchildren’s college education, or help with major purchases. Take care of yourself and your spouse before anyone else. In time, your family will come to appreciate your self-sufficiency. If not, too bad.

#9—Take advantage of free money. I cannot fathom why such a large percentage of workers with 401(k)s do not maximize their contributions. In addition to the tax benefits, many employers match a percentage of those contributions; it’s free money.

If your employer doesn’t offer a 401(k), maximize your IRA contributions. And if you’re over age 50, don’t forget the catch-up provisions that allow you to save even more. This is low-hanging fruit, so run and grab as much of it as you can.

Retiring rich requires a series of choices; they are often difficult. A comfortable retirement is not a foregone conclusion, even if you lived comfortably in your working years. Since WWII, we have enjoyed one of the most productive economies the world has ever seen, yet many seniors are broke. When you reach retirement age, you don’t have to be one of them.

Start mapping your own path to a rich retirement by reading Miller’s Money Weekly, our free weekly e-letter where my team and I cover pressing money matters and share unique investment insights for seniors, savers and other income investors—all in plain English. Click here to receive your complimentary copy every Thursday. Follow us on Twitter ;@millersmoney.

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Casey Research Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.