The Shanghai Stock Market Crash and China Gold Demand

Commodities / Gold and Silver 2015 Jul 11, 2015 - 01:01 PM GMT

What it means for the future of the gold market

What it means for the future of the gold market

"At present, up to 12 trillion yuan stays in domestic residents' saving accounts. The launch of individual gold investment, therefore, will allow residents to change currency assets into gold assets. At the macro level, it will expand channels for changing savings into investment, thus adjusting the money supply; in the micro aspect, allowing citizens to trade and keep gold can improve social welfare, benefiting both the country and the population. Moreover, with the dual attributes of common commodity and currency commodity, gold is a desirable instrument for hedging. Therefore, developing gold trade for individuals is practical." – Zhou Xiaochuan, Governor, the People's Bank of China

Shanghai stocks have fallen over 30% since mid-June. The equivalent in U.S. terms would be for the DJIA to fall 6000 points to the 11,000 level – a crash by any definition. Most of the commentary on this important subject has centered around the potential contagion effect for stock markets in the rest of Asia and beyond. There is another aspect to the crash worth considering though, and that has to do with the effect it will have on Chinese gold demand.

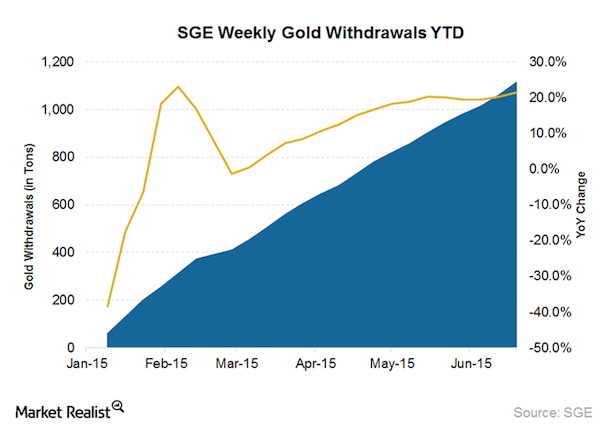

The Chinese people, it is well known, already have a cultural affinity to gold. That attachment just received a shot of adrenaline. Prior to June, trading volumes on the Shanghai Gold Exchange (SGE) were already running 20% higher than the previous year. Now, with crash psychology affecting thinking up and down the spectrum of investors, SGE is reporting volumes off the charts. In early July, Want China Times reported that "SGE posted a record trading volume of 48.33 million grams in a single day in late June." (48.3 metric tonnes, a big number.)

|

Chart courtesy of Market Realist, Shanghai Gold Exchange Withdrawals |

Typically stock market crashes inspire gold demand. In the case of China, where the government and central bank encourage citizen gold ownership as a matter of public policy, that lesson could become enshrined in the national psyche. The important consideration for investors elsewhere around the globe is what effect even stronger gold demand from China will have on the gold price both now and in the future.

Flow of physical metal between buyers and sellers will govern prices in China not paper trades

Ever since 2011 when China's demand began to ratchet up, clients have asked how the price of gold could be stagnant to down under the circumstances. The short answer to that question is that price discovery for gold does not occur in the physical market, but in the multi-trillion dollar leveraged paper trade in London and New York – a volume that dwarfs the physical delivery market. Now China is about to challenge that price discovery mechanism through significant infrastructure changes slated to take effect by the end of the year. This new construct has as its base China's fundamental understanding and goals with respect to gold as summarized by Peoples Bank of China governor Zhou Xiaochuan in our masthead quote above; its affinity for delivered physical ownership, as opposed to paper-based metal; and, the official measures it has undertaken to make inroads into the international gold market's price discovery mechanism.

To gain a better understanding of how China is likely to affect price discovery in the gold market, let's start with something of interest that surfaced as a result of the recent Shanghai crash. Financial Times reported rumors floating the markets that Goldman Sachs was responsible for manipulating stocks downward. Officials denied those rumors and a spokesman for the exchange stated that "foreign investors with access to the futures market via the Qualified Foreign Institutional Investor (QFII) program were only permitted to use futures for hedging operations and are not allowed to make directional bets. All recent trades by QFIIs complied with regulations." Of course if any manipulation of stocks were to occur, it would be executed in the leveraged futures market where bets can be placed at pennies on the dollar.

Up until I read that quote I was unaware of the strict procedures governing foreign trading on the Shanghai Futures Exchange (SHFE), China's only futures trading venue. A further investigation, helped along with some links from Koos Jansen, the Netherlands based expert on China's burgeoning gold market, revealed stringent rules governing trade on the SHFE for domestic participants as well, though not quite as stringent as the rules for foreigners. At the heart of those rules, SHFE imposes strict position limitations and margin requirements on traders in order to keep price speculation (or directional bets to use its term) to a minimum. Futures trading in China, clearly is meant to serve as an adjunct to the physical market instead of the other way around as it is in western gold trading centers. Hedging is maximized. Speculation is minimized. Leverage is controlled within reasonable parameters. (Link SHFE "Operational Manual for Gold Futures Contract Trading")

__________________________________________________________________________________________________

A little USAGOLD history. . . . Pictured are News & Views hard copies from 1999 just before gold began its secular bull market. News & Views first made its appearance at a time when gold-based publications were few and far between. The "Big Breakout" headlined in the November, 1999 issue refers to a price jump from $260 to $330 per ounce. Your editor sees a good many similarities between that period and now. ____________________________________________________________________________________________________ |

An institution wishing to bet against gold would be forced to do so by delivering the physical metal itself in kilo bar form (the standard trading unit) upon settlement – an expensive and cumbersome process likely to discourage excessive speculation or attempts at price manipulation. Gold Forecaster's Julian Phillips, who has analyzed activity in the gold market for a number of years, points out that the seminal changes taking place in the gold market centering around Shanghai "will allow Chinese banks to participate in the gold market on a global basis." It will be a market, he says, "that is not distorted by the banks, their proprietary trading, or control of the gold distribution system globally. China will hold these reins."

Gold as a wealth building asset – East and West

In short, the physical flow of metal – its purchase and sale in real terms – will govern pricing in Shanghai, not leveraged paper trades, as is the case in the West. This emphasis on physical pricing in Shanghai, particularly when the new Shanghai Fix comes into play later this year, could signal the birth of a whole new gold market unlike anything we have experienced since the United States detached the dollar from gold in 1971.

At the moment, there is a strong, steady flow of gold through the London-Zurich-Hong Kong-Shanghai pipeline. Should the supply slow, prices in yuan terms could receive a strong jolt. Don't forget too that the newly structured London fix now includes one Chinese bank with perhaps two others soon to be accepted as members, the situation Julian Phillips touches upon above. These banks will be on the constant lookout for arbitrage opportunities that could be purchased and shipped to their home country. Competition, as they say, is good for the soul, and in this case, it could be curative.

Taking this overview one step further, if the Shanghai stock crash does indeed inspire increased interest in gold among Chinese investors, as it has elsewhere, that buying pressure – in the absence of opposing speculative leverage – will manifest itself in higher yuan gold prices, as the public buys and takes delivery. A higher gold price in yuan terms could translate in due course to a stronger yuan in terms of the dollar, the British pound, the euro, etc.

At the moment, China is not particularly interested in exercising a policy to push the yuan higher (particularly in light of recent events), but that could change at any time. China's stated longer-term aim is a strong and reliable yuan that could be used by other nation states as a reserve currency and store of value. Ultimately higher gold prices in yuan terms would serve that end, act as a balance to its huge paper currency reserves and, in the process, bolster the wealth of the Chinese people. In the meantime, its other stated policy – the building of personal and national gold reserves – will go on as it has in the past.

As for the impact on the Western gold owner, in my view, the developing China gold market lends itself to a significant longer term opportunity for the investor who buys and holds gold coins and bullion as an alternative savings vehicle. China will continue to add a level of official sector support previously absent from the global market. Under the current circumstances, gold ownership makes a great deal of sense even without China's involvement. With it, that sensibility is underscored.

For those new to the China gold market analysis or those looking to catch-up, let me rehash that infrastructure:

• China is the largest producer of gold in the world today and its production is climbing.

• China's citizenry is the largest consumer of gold and that consumption, even without the incentives outlined above, is growing.

• The Shanghai Gold Exchange, as we have reported and monitor here, intends to open its own gold price fix to compete with London by the end of the year.

• One Chinese bank now participates in the London fix and a second is expected to join shortly. Membership to the exclusive London pricing club was formerly reserved to European and American banks only. The inclusion of Chinese banks in and of itself is an important change in the London and New York pricing formulae. China's national strategy with respect to gold though brings a whole new element to the London/New York pricing regime. China sees gold like the majority of our clientele – as a long term savings instrument and hedge against the vagaries of paper currencies.

• Last, rumors continue to float the gold market that China is about to make an announcement with respect to its national gold reserves. Though the largest gold producer in the world, it still remains a net importer. Most gold analysts believe that the bulk of China's mine production has gone into its national coffers as a hedge. China now reports holdings of 1059 tonnes. An announcement of a large increase would likely send shock waves through both the gold and FOREX markets. Its last announcement of an increase in gold reserves from 600 tonnes to 1059 tonnes in 2009 was the first public indication of China's strong interest in gold. It shocked markets and contributed to gold's rise from the $900 per ounce level in April when the announcement was made to more than $1200 by the close of the year.

By Michael J. Kosares

Michael J. Kosares , founder and president

USAGOLD - Centennial Precious Metals, Denver

Michael J. Kosares is the founder of USAGOLD and the author of "The ABCs of Gold Investing - How To Protect and Build Your Wealth With Gold." He has over forty years experience in the physical gold business. He is also the editor of Review & Outlook, the firm's newsletter which is offered free of charge and specializes in issues and opinion of importance to owners of gold coins and bullion. If you would like to register for an e-mail alert when the next issue is published, please visit this link.

Disclaimer: Opinions expressed in commentary e do not constitute an offer to buy or sell, or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. Centennial Precious Metals, Inc. recommends the purchase of physical precious metals for asset preservation purposes, not speculation. Utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such USAGOLD - Centennial Precious Metals does not warrant or guarantee the accuracy, timeliness or completeness of the information found here.

Michael J. Kosares Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.