Stock Market Investment Success Through the “Investment Rule of 72”

InvestorEducation / Learning to Invest Oct 21, 2016 - 05:14 PM GMT

The issue of successful stock market investment affects us all. Even if we are not directly engaged in the industry, all of us will need some form of pension to fund our retirement. Whether we like it or not most of our retirement funds will find their way into the financial markets. For this very reason, the issue of pensions has moved politically centre stage; in particular the investment strategies used to administer pension funds. Due to mismanagement, mainly over the last decade, many retirement portfolios have become under-funded at best, or, at worst, totally bust. This situation is a direct result of the managed funds having been speculated rather than invested. Many cynics will say that the whole investment environment today has more of the characteristics of a casino than of a professional market of equities and, therefore, they doubt that one can ever achieve a faithful and fair return on capital. However, this view is erroneous. This essay sets out to explain how to achieve superior pension investment returns through a simple yet powerful investment rule: “the rule of 72. This rule is based on investment and not speculation yet if you faithfully apply it your returns, over time, will be spectacular. Many believe that such degree of return is only possible through “speculative activity”. They are wrong and I will explain.

The issue of successful stock market investment affects us all. Even if we are not directly engaged in the industry, all of us will need some form of pension to fund our retirement. Whether we like it or not most of our retirement funds will find their way into the financial markets. For this very reason, the issue of pensions has moved politically centre stage; in particular the investment strategies used to administer pension funds. Due to mismanagement, mainly over the last decade, many retirement portfolios have become under-funded at best, or, at worst, totally bust. This situation is a direct result of the managed funds having been speculated rather than invested. Many cynics will say that the whole investment environment today has more of the characteristics of a casino than of a professional market of equities and, therefore, they doubt that one can ever achieve a faithful and fair return on capital. However, this view is erroneous. This essay sets out to explain how to achieve superior pension investment returns through a simple yet powerful investment rule: “the rule of 72. This rule is based on investment and not speculation yet if you faithfully apply it your returns, over time, will be spectacular. Many believe that such degree of return is only possible through “speculative activity”. They are wrong and I will explain.

Benjamin Graham, the father of security analysis, and mentor of Warren Buffett, long believed in the stock market as a means to achieve financial freedom. The wealth he accumulated and the school of successful investment gurus he educated are testament to his insight and genius. The key to his formula has always been one simple concept: VALUE. His central message never changed and in a financial community which bores easily, his conservative investment style became "classical" and then "old fashioned". Graham ultimately derided the fads and trends that engulfed Wall Street and he eventually gave up trading and managing funds. However, his "baton" of value was spectacularly taken up by his acolyte, Warren Buffett, who went on to become the most successful investor of all time.

Buffett, like Graham, believes the policy of investing does not require high qualities of insight or forethought, as long as some simple rules are applied. In essence these simple rules are:

1. Safety of Capital

2. Adequacy of Return

An operation that does not seek both of the above is not an investment but a speculation.

Now in today's complex, volatile, media-driven and fast-moving market environment how does one actually apply these simple rules? The essential thing to realise is that when you buy an equity, you are purchasing part of a business. Investment is most intelligent when it is most business like.

For over the two decades, for pension purposes, I have been educating clients on how to achieve excellent pension returns through passive saving into the S & P 500. This strategy ensures safety of capital and good return because ones hard earned money is spread over 500 companies (thus ensuring spread of risk) that pay good dividends (thus gaining good return).

The rule of 72.

The 'Rule of 72' is a simplified way to determine how many years an investment will take to double, given a fixed annual rate of interest. Thus by dividing 72 by the annual rate of return, investors can get a rough estimate of how long it will take for the initial investment to “double” itself.

Our target annual rate of return is 10%. (This is the rate the S & P has grown, on average, over the last 30 years). This average annual return objective when married to the “miracle” of compounding turns a consistent savings fund into an excellent retirement nest egg. Let me demonstrate.

When you divide 10 into 72 you get 7.2 . This means that it will take 7 years (approx.) for ones fund to double:

Year 1. 1000 X 1.10 = 1100

Year 2. 1100 X 1.10 = 1210

Year 3. 1210 X 1.10 = 1331

Year 4. 1131 X 1.10 = 1464

Year 5. 1464 X 1.10 = 1611

Year 6. 1611 X 1.10 = 1771

Year 7. 1771 X 1.10 = 1949

The average “pension investment” cycle is about 40 years (25-65 = 40), therefore if you focus on achieving an annual investment target of 10% you can get 6 “doublings” (approx.) of your investment over the 40 year period. Thus through the “magic” of compounding an “investment pot” of 20,000 Euro or a fund developed through dollar cost average saving (see addendum 3), can grow into a handsome pension fund of 1.24 million Euro after 6 such “doublings”.

Year 1-7. 20,000 X 2 = 40,000

Year 8-14. 40,000 X 2 = 80,000

Year 15-21. 80,000 X 2 = 160,000

Year 22-28. 160,000 X 2 = 320,000

Year 29- 36. 320,000 X 2 = 640,000

Year 37- 42. 640,000 X 2 = 1,240,000

(Rounded up)

Conclusion

Despite appearing to be a complex matter, the path to investment success can be quite simple, if you have a proven strategy.

By applying our earnings growth and dividend investment approach through our S & P savings strategy the average investor, using discipline and patience, to achieve financial independence over time.

However, time is of the essence.

Addendum 1.

Investing: Compounding & The Power Of Starting Saving Early:

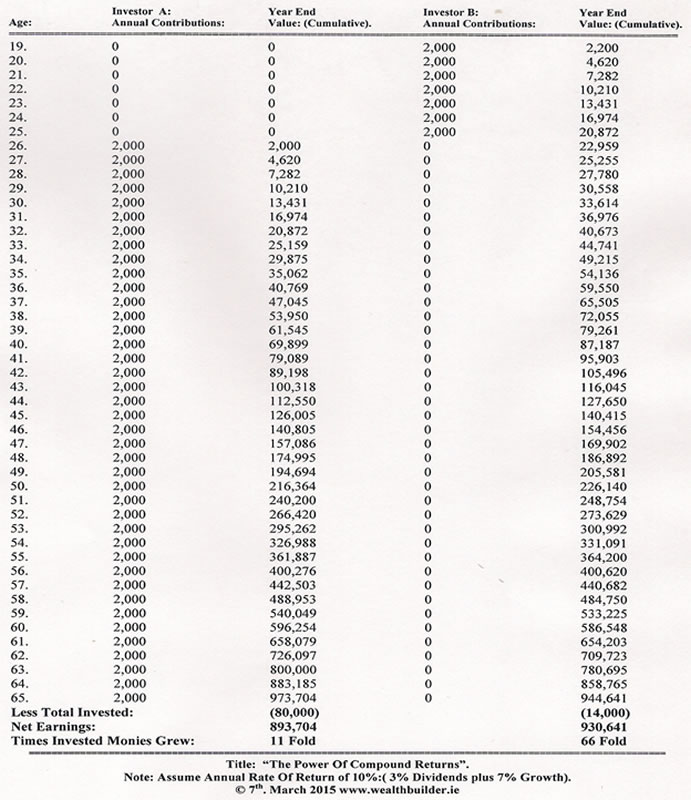

In order to emphasize the power of compounding, I am including this extraordinary study, courtesy of Market Logic, of Ft. Lauderdale, FL 33306. In this study we assume that investor (B) opens Personal Pension Plan at age 19. For seven consecutive periods he puts $2,000 in his fund at an average growth rate of 10% (7% interest plus growth). After seven years this fellow makes NO MORE contributions -- he's finished. A second investor (A) makes no contributions until age 26 (this is the age when investor B was finished with his contributions). Then A continues faithfully to contribute $2,000 every year until he's 65 (at the same theoretical 10% rate).

Now study the incredible results. B, who made his contributions earlier and who made only seven contributions, ends up with MORE money than A, who made 40 contributions but at a LATER TIME. The difference in the two is that B had seven more early years of compounding than A. Those seven early years were worth more than all of A's 33 additional contributions.

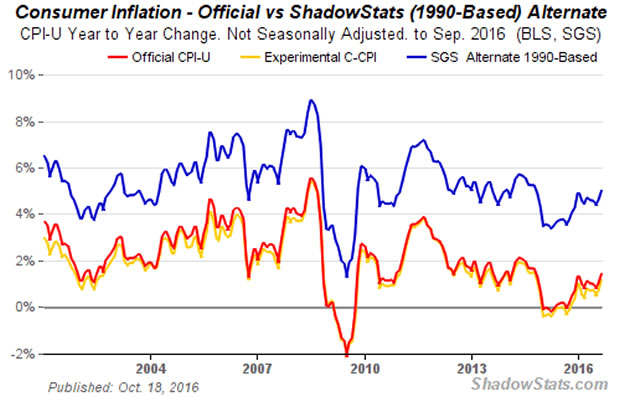

Addendum 2. True rate of inflation

Source: ShadowStats.Com

Note: with an average inflation rate of 6% per annum general price levels, using the rule of 72, will double every 12 years, equating to 3.5 doublings over our rounded up 42 working years. This means that a basket of goods that costs 20,000 Euro today will have a “nominal value” of 240,000 Euro at our sample retirement age. In other words those who work but do not have an “inflation proof” form of income are going to end up the “paupers” of the future and I am afraid that this is going to be the norm for the majority in the western world.

Addendum 3.

Dollar-Cost Averaging

Dollar-cost averaging is carried out simply by investing a fixed dollar amount into your investment instrument at pre-determined intervals. The amount of money invested at each interval remains the same over time, but the number of shares purchased varies based on the market value of the shares at the time of a purchase. When the markets are up, you buy fewer shares per dollar invested due to the higher cost per share. When the markets are down, the situation is reversed and you purchase a greater of number of shares per dollar invested. It's a strategic way to invest because you buy more shares when the cost is low, so you get an average cost per share over time, meaning you don't have to invest the time and effort to monitor market movements and strategically time your investments.

Christopher Quiqley

B.Sc., M.M.I.I. Grad., M.A.

http://www.wealthbuilder.ie

Mr. Quigley was born in 1958 in Dublin, Ireland. He holds a Bachelor Degree in Accounting and Management from Trinity College Dublin and is a graduate of the Marketing Institute of Ireland. He commenced investing in the stock market in 1989 in Belmont, California where he lived for 6 years. He has developed the Wealthbuilder investment and trading course over the last two decades as a result of research, study and experience. This system marries fundamental analysis with technical analysis and focuses on momentum, value and pension strategies.

Since 2007 Mr. Quigley has written over 80 articles which have been published on popular web sites based in California, New York, London and Dublin.

Mr. Quigley is now lives in Dublin, Ireland and Tampa Bay, Florida.

© 2016 Copyright Christopher M. Quigley - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors before engaging in any trading activities.

Christopher M. Quigley Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.