Buy-to-let Mortgage Product Choice Reaches Post Financial Crisis High

Housing-Market / Buy to Let Feb 25, 2019 - 02:48 PM GMTBy: MoneyFacts

While the tax and rule changes imposed on the buy-to-let (BTL) sector over the last few years have heightened the pressures felt by landlords – and even forced some from the market altogether – research from Moneyfacts.co.uk shows that the number of BTL products currently available is at a post-financial crisis high.

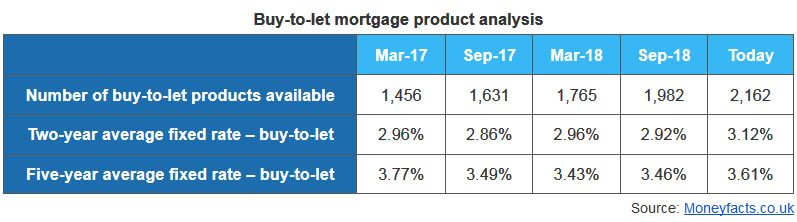

Today, landlords have the choice of 2,162 buy-to-let mortgages, meaning the number of products has not been higher since October 2007, when 3,305 products were available.

Darren Cook, Finance Expert at Moneyfacts.co.uk, said:

“It is encouraging that buy-to-let landlords have more mortgage choice than they have had at any time in almost 12 years. Total product numbers have increased by 397 over the past year and by 706 over the past two years to stand at 2,162 products today.

“Despite ongoing uncertainty in the property market, providers are not shying away from offering landlords a greater choice of products, although it is also evident from our research that heightened competition to try and attract BTL business has not resulted in a fall in interest rates, as has recently happened in the residential mortgage sector. Indeed, the average two-year fixed BTL mortgage rate has increased by 0.20% to 3.12% since September 2018 and the average five-year fixed rate has increased by 0.15% over the same period.

“As there appears to have been no sustained increases in interest SWAP rates since September 2018, a strong argument can be made that the recent increases to BTL mortgages interest rates have been a result of BTL mortgage providers attributing a little more to risk into their product rates due to uncertainty over future economic conditions.

“The disparity in the direction of movement between BTL and residential interest rates may be due to the way these two types of lending are primarily assessed. BTL mortgage providers generally consider the potential rental income and affordability during assessment, whereas residential mortgage providers typically look back at income earned by the borrower and affordability.”

moneyfacts.co.uk is a financial product price comparison site, launched in 2000, which helps consumers compare thousands of financial products, including credit cards, savings, mortgages and many more. Unlike other comparison sites, there is no commercial influence on the way moneyfacts.co.uk ranks products, showing consumers a true picture of the best products based on the criteria they select. The site also provides informative guides and covers the latest consumer finance news, as well as offering a weekly newsletter.

MoneyFacts Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.