The Longer the US Sino-Tariff Wars Go On, the Harder It Will Be to Undo the Damage

Economics / Protectionism Jun 20, 2019 - 02:37 PM GMTBy: Dan_Steinbock

Compared to pre-2008 crisis levels, world economic growth has plummeted by half and is at risk of a long-term, hard-to-reverse stagnation. Returning to global integration and multilateral reconciliation could dramatically change the scenario

Compared to pre-2008 crisis levels, world economic growth has plummeted by half and is at risk of a long-term, hard-to-reverse stagnation. Returning to global integration and multilateral reconciliation could dramatically change the scenario

Since spring 2017, the US-led tariff wars have effectively undermined the global recovery. In the past years, global economy has navigated across several scenarios. Now it is approaching the edge.

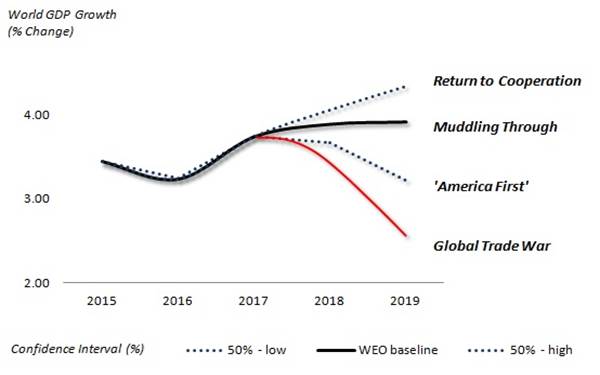

I have been following four generic scenarios on the prospects of global economic growth since the U.S. 2016 election. The first two scenarios represent variants of “recoupling." In these cases, global integration prevails, despite tensions. In the next two scenarios, global integration will fail, either in part and regionally or fully and globally.

What should worry us all is that, during the past few years, real global growth prospects have slowly but surely moved from the ideal and preferable scenarios toward the worst and darkest.

The Return to Cooperation Scenario

In this scenario, U.S. and China achieve a trade agreement. Both agree to phase out additional tariffs, renounce trade threats and establish working groups to defuse other friction areas in intellectual property rights, social and political issues, and military matters. Global growth prospects could – in the best scenario – even exceed the old OECD/IMF baselines at more than 4%.

This was always the least likely scenario to materialize. Today, its degree of probability is minimal. Yet, it is important to remember that, during the first Trump-Xi meeting, many observers saw the scenario still as possible, even probable.

The Muddling Through Scenario

In this scenario, the tariff’s economic impact would have been limited to 0.4% of Chinese GDP and 0.8% of U.S. GDP, respectively. U.S. and China develop a path to a trade agreement during the truce, but other friction areas, – particularly in advanced technology, result in new skirmishes.

Uncertainty decreases but fluctuates. Global economic prospects barely improve. Markets witness rallies and plunges. Global recovery fails. Global growth prospects remain close to 3.5%-3.9%.

Only half a year ago, this scenario was still seen as a viable one. Today, it feels like a bygone world.

The America First Scenario

In this scenario, the import-value stakes would be 10-fold relative to the start of the trade war, amounting to more than $0.5 trillion, with soaring collateral damage. In China, it could shave off 0.4% and in the U.S., 0.8% of the 2019 GDP, respectively. Neither the U.S. nor China would agree to phase out additional tariffs. Talks would linger, fail or lead to new friction. Uncertainty increases, volatility returns. Global prospects decline further. Markets linger.

In this scenario, global prospects would dampen as world GDP growth in 2019 would sink to 3% or worse.

The Global Trade War Scenario

In this scenario, all bets are off. U.S. and China fail to agree on a trade compromise. Additional tariffs are enacted and new trade threats declared. The White House escalates attacks against Chinese industries, in intellectual property rights, social and political issues, and military modernization. Volatility soars. Real GDP growth in the U.S. takes a severe hit. Chinese growth erodes.

Eventually, risks to global outlook overshadow world GDP growth, which could linger at 2%-2.5% or worse. World trade and investment plunges. Migration crises abound. The number of globally displaced, which has exceeded World War II figures since the mid-2010s, soars to record highs. A series of new geopolitical conflicts prove harder to contain.

Toward the Edge

So where are we today vis-à-vis these scenarios? A simple answer: Moving closer to the edge.

After trade frictions and the Trump tariffs undermined the global recovery momentum, the IMF finally woke up predicting global economic activity to slow notably. In early June, the World Bank estimated the world economy would only expand by 2.6%. The IMF has affirmed that the trade wars could wipe $455 billion off global GDP in 2020.

Worse, President Trump increased tariffs on $200 billion worth of Chinese goods exported to the U.S., and introduced an effective ban on American companies doing business with Chinese telecom giant Huawei in early May.

In brief, the status quo is shifting from the America First toward the Global Trade War scenario (see the red line in the Figure).

Figure Trade War Scenarios: Risks to Global Economic Outlook

Sources: Difference Group (WEO/IMF growth data)

In effect, multilateral banks’ estimates still downplay effective collateral damage. If the Trump administration will continue to expand trade wars and geopolitical ploys in multiple regions, their models ignore the impending adverse feedback of such measures - as evidenced by Morgan Stanley’s business conditions index that just took the worst one-month hit in its history.

To understand how much expectations have been revised, let’s recall that before the 2008 global crisis global growth rate was around 4% to 4.3%. The current growth rate has almost halved from its pre-crisis level.

In relative terms, something similar occurred in the 1970s, which saw the end of three “glorious decades” of solid growth in major advanced economies.

What we are witnessing now is a potentially fatal fall into secular stagnation. In part, it is structural, resulting from maturing economies and aging populations. But in part, it is self-induced and the effect of misguided trade policies and unilateral geopolitical aggression. In the absence of tariff wars and geopolitical destabilization, global growth rate could now be closer to 3.5%.

The longer it takes to achieve multilateral reconciliation, the more likely it is that falling secular long-term growth rates will prove harder to reverse.

Dr. Dan Steinbock is the founder of Difference Group and has served at the India, China and America Institute (US), Shanghai Institute for International Studies (China) and the EU Center (Singapore). For more, see http://www.differencegroup.net/

© 2019 Copyright Dan Steinbock - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Dan Steinbock Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.