What Should We Do If There Is No Fed Monetary Policy Pivot?

Stock-Markets / US Federal Reserve Bank May 17, 2022 - 04:44 PM GMTBy: The_Gold_Report

While investors may have been betting on a Fed pivot, expert Michael Ballanger analyzes where we may find ourselves if they don't.

As a young and very brash “stock salesman” in the early 1980s (Note: Back then, they did not call us “wealth managers” or “investment professionals” or “advisors.”), I discovered a newsletter writer that was the best storyteller I have ever read, and his name was Richard Russell. The author and founder of the 1958 “Dow Theory Letters,” he rose to fame after calling the bottom of the horrendous 1973-1974 bear market in December of the terminal year resulting in a bombardment of catcalls and peer-pressure ridicule. Nobody—and I mean NOBODY—expected that stock prices were going to do anything but continue to crater and that was what made him such a beast.

As we do our collective best to weather this storm of selling pressure in what started as tech stocks but which has now migrated to literally everything, I am reminded of one of the more poignant “Russell-isms.” He said, “In a bear market, he who loses the least, wins.”

“My losses have taught me that I must not begin to advance until I am sure I shall not have to retreat.” — Edwin Lefevre

That phrase is the major portion of the reason that I advised subscribers on January 7th of this year, with the S&P 500 clipping above 4,800, that capital preservation was our primary focus and that volatility would dominate the investment landscape in 2022.

Russell was a firm believer in gold and silver as cornerstone assets for all portfolios but not to the avoidance of stocks and bonds because he educated himself on the language of the market as defined by Charles Dow, which meant that all assets had their “time and place” to shine. For a clueless rookie in an industry fraught with incompetence and graft, his guidance would help me in trying my utmost to deliver a realistic rate of return for clients.

Not always did he get it right but when he was wrong, he owned up to it and explained why. I try to emulate that and cringe when I hear yet another of the many newsletter writers or podcasters that try to weasel their way out of a particularly bad call by blaming “the banksters” or “the Fed” or the “the cartel,” all three of whom have been playing around in our beloved precious metals markets since the Dawn of Creation (of the Fed).

As these markets take each and every sector out behind the woodshed, including commodities, and thrash them mercilessly, I always remember another great Richard Russell quip: “Follow the money.”

It would seem that most Wall Street money-masters have now finally heeded Jerome Powell’s message and like my subscribers and myself, have taken the Fed at its word when it says that “price stability” trumps “maximum full employment” as an executable mandate undertaking. The idea that the Fed will not put its foot anywhere even close to the money-printing accelerator was clearly evident the moment that Fed Chair Powell dropped the word “transitory” from the inflation/Fed policy narrative. However, the much-advertised and even-greater-trumpeted term “Fed pivot” is now at the forefront of everyone that I know and respect.

I will not bother to list the names of the ladies and gentlemen that are all collectively calling for a “Fed pivot” but as we all know, when all of the popular and very successful analysts of astounding intellect and track record agree, the exact opposite is about to unfold. I maintain that this much-publicized “breaking point” of the financial markets to which all the wizards point is much farther out than estimated and far more elusive than any so-called stock market “breaking point.”

“Recency bias” is one of those cognitive dissonances that the youngsters like to flash around but it was in 1975 in my marketing class through my non-Jesuit professor of marketing Jeremy Klein that I first learned of it. He was a great student of the history of marketing as it pertained to consumer behavior but he also knew markets. He told us one morning that “recency bias” was “assuming that your sophomore girlfriend was in love with you every night that you were out with the boys.” (Hint: she was in love just not with you.)

This applies to the market in the same way that everyone who “bought the dip” between March 2009 and November 2021 while laughing off Uncle Jerome’s “transitory” head fake were totally misinterpreting his message to the member banks (and Nancy Pelosi) that the boom was about to be lowered on all “risk assets” and “all margin accounts” and “rumored Twitter takeovers.” We have entered a “secular bear market” and the sooner we all accept that reality, the better off we shall all be.

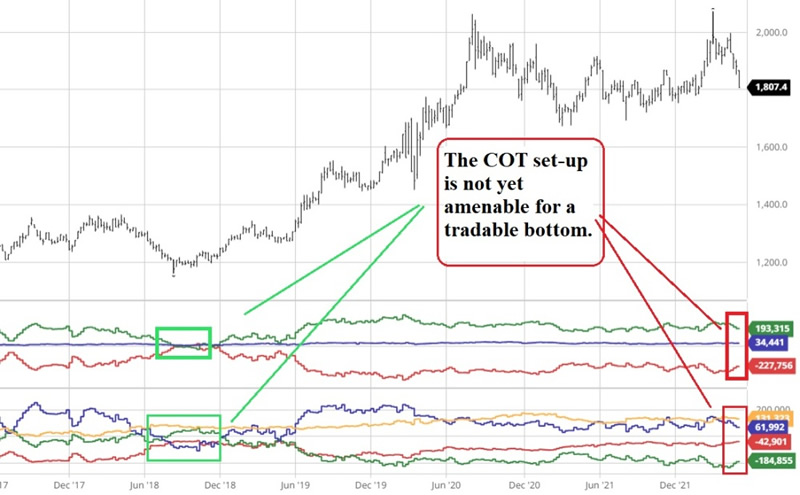

The “real” cost of borrowing is now shrinking thanks to rising bond yields. The commercial traders under the direction of the global central banks have little need to worry about carrying mammoth short positions into the month-end close. Look below at the COT Report for this past week ended Tuesday. The Twitterverse has been positively cavitating all week ling with commentary regarding the Commitment of Traders (or “COT”) Report and how it was a lead-pipe cinch to show a wildly bullish drawdown in the commercial net short position (in futures). Alas, it came in with a net short position of 227,756 contracts which was, to put it mildly, unexciting. At the bottom in December 2015, that number flipped to an actual net long position, albeit briefly, marking a watershed moment for gold and silver traders and investors, while the opposite was the case at the August 2016 top when commercials were obscenely short at north of 350,000 contracts. Conclusion: More downside is probable.

I have a question for all of the readers out there that think markets are poised for a superlative advance based upon the Fed’s ability to “pivot.” It is an easy question.

What if they don’t?

Go back to page one and look at that chart of the SPY: US. That is a seven-year history of Fed intervention/interference/invasion of the “freedom of markets” so pivotal to that “free market capitalism” that is supposed to unleash those “animal spirits” that drive consumer behaviors to unprecedented levels of optimism.

What if the mandate of the Wall Street barons is to pummel the plebes into a certain mode of behavior that excludes stock market outperformance?

The degree to which the legions of youthful new stock market investors are in “full-on denial” is evident by the manic-depressive knee-jerks that are now almost commonplace in the weekly gyrations of the averages. Now, as I wrote last week, stocks either have reached (or are soon to reach) an important inflection point where the urgency to reduce leverage within the hedge fund and ETF communities has subsided. At this point, risk assets including stocks, gold, and commodities, can embark upon multi-week advances that will result in highly-publicized pronouncements from the usual suspects (Cramer, CNBC, Larry Kudlow, etc.) that “the bear market is over!”

If it follows the pattern of other past secular bear markets, these prognostications will be our signal to raise cash and return to the defensive posture which we have carried since January 7th, 2022 when the “First Five Days” Early Warning Indicator went bearish followed by mid-January and end-of-January (“January Barometer”) sell signals. We flattened the volatility hedge this week with a 37.72% gain and since it represented a 15% portfolio allocation, it softened but did not stop the bear’s claws because the junior commodity names finally buckled under the onslaught of weak metal prices.

The good news for all of us arrived late Friday when I got the ultimate “Buy” signal for precious metals. You have often heard me comment upon the predictive power of nature with specific reference to my wonderful dog, "Fido.” I cannot tell you the number of times over the past ten years that I have thrown a hissy-fit over blatant interventions by the bullion banks or the PPT (Working Group on Capital Markets by way of the NY Fed trading desk) only to have Fido bolt from under my desk and wind up hiding under the tool shed in a hole he clawed out back in 2015. Well, yesterday morning, I expected a rally in the silver market but when it opened at USD $20.63 and then nosedived to $20.42 within seconds, I took my old wooden-shaft five iron and hummed it at the monitor only to have it miss the screen but take out a large bronze ornament shaped like a gong and go clattering into the corner. When Fido refused to surface from under his beloved “safe haven” despite handfuls of raw hamburger meat, it is usually because he has been suitably frightened by his lunatic master and when his lunatic master launches tirades of unimaginable sound and fury (as happened on Friday), it usually marks the end of the downtrend in my favorite metal prices.

After all, a lunatic master can only handle so much…

Follow Michael Ballanger on Twitter ;@MiningJunkie.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Aftermath Silver Ltd., Great Bear Resources, Western Uranium, Stakeholder Gold, Getchell Gold. My company has a financial relationship with the following companies referred to in this article: Getchell Gold Corp. and Western Uranium & Vanadium Corp. My firm no longer does consulting work for Stakeholder Gold.. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Great Bear Resources. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Western Uranium and Vanadium and Aftermath. Please click here for more information. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports (including members of their household) own securities of Getchell Gold, Western Uranium and Stakeholder Gold and Aftermath, companies mentioned in this article.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.