Euro Doomed to Fail as Governments Pull in Opposite Directions

Currencies / Euro Feb 03, 2009 - 02:53 AM GMTBy: John_Mauldin

Milton Friedman famously predicted that the euro would not last past their first economic crisis. This week we look at commentary by Niels Jensen that explores the news from Euroland. Can the euro survive? He explores a number of options which are most definitely not on the radar screen for most investors. It is good to get a perspective from those outside of our own back yard. Note that when he says "our country" he is referring to Great Britain.

Milton Friedman famously predicted that the euro would not last past their first economic crisis. This week we look at commentary by Niels Jensen that explores the news from Euroland. Can the euro survive? He explores a number of options which are most definitely not on the radar screen for most investors. It is good to get a perspective from those outside of our own back yard. Note that when he says "our country" he is referring to Great Britain.

Niels is the Managing Partner of Absolute Return Partners based in London (which is my European partner). I work closely with Niels for years and have found him to be one of the more savvy observers of the markets I know. You can see more of his work at www.arpllp.com and contact them at info@arpllp.com. The numbered footnotes are at the end of the letter.

John Mauldin, Editor

Outside the Box

Do BRICs (and Germans) Eat PIGS?

When the euro was introduced about ten years ago, the pessimists didn't give it much chance of reaching its tenth anniversary. The euro, or so the argument went, was doomed from the outset because of the wide spread in economic performance and discipline amongst the member countries. At one end you had, and still have, the highly disciplined, but also slow growing, economies of Germany and the Netherlands. At the other end you find the faster growing but poorly disciplined countries such as Spain and Greece. As icing on the cake, you also had, and still have, countries that lack in both departments, such as Italy, making it difficult for the union to 'gel' – well, according to sceptics.

There is admittedly an embedded weakness in the way the European currency union is structured. In the United States, arguably that largest currency union in the world, fiscal transfers between member states allow for the federal government to adjust for variances in economic performances. There is no such mechanism within the euro zone, which explains why the member states are subjected to a number of rules1. These rules require for everyone to exercise a high level of economic discipline. The problem is that there is little or no such discipline.

The best example is the huge spread in the rise of unit labour costs over the past few years. Unit labour costs measure labour (wage) costs adjusted for changes in productivity. It is probably the best measure that exists in terms of tracking the changes in competitiveness between nations. When the Stability and Growth Pact behind the euro was established, there was no reference made to unit labour costs which, with the benefit of hindsight, was a major mistake. Even Jean-Claude Trichet, the Head of the European Central Bank, who rarely admits mistakes, has publicly stated that if he could design the currency union all over again, he would push for a unit labour cost stability pact.

Back to the sceptics. What they failed to realise was that Europe, together with the rest of the world, was about to enter a period of unprecedented prosperity. The good times would not only gloss over the deeper problems, but the euro would actually go from strength to strength to a point where it now threatens to unseat the US dollar as the premier reserve currency of the world. It is therefore perhaps a mystery to some of you, why one should question the longer term viability of the euro. That is nevertheless what I intend to do.

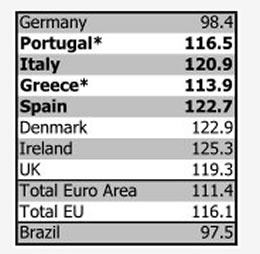

The problem, as I have already alluded to, is poor discipline amongst several of the member states. Ever heard of the four PIGS? This less than flattering acronym stands for Portugal, Italy, Greece and Spain, four members of the euro zone which are all in much deeper trouble than they are prepared to admit. They are often considered the 'antidote' to the BRIC countries, the fast growing emerging market economies of Brazil, Russia, India and China. Let's take a closer look at the unit labour cost index for various countries (see table 1).

Table 1: 2007 Unit Labour Cost Index (2000=100)

Notes: *2006. PIGS countries in bold. Source: http://stats.oecd.org/

Since the introduction of the euro, the PIGS have failed miserably to keep up with Germany on this measure of competitiveness. So has Ireland by the way, hence its current predicament. On the other hand, Brazil (the only BRIC country which the OECD reports unit labour costs on) scores very well on this account, a fact which is not going to make life any easier for the PIGS.

EU countries outside the euro zone, such as the UK, have also lost out to Germany in recent years, but the UK has been able to play a card which is not at the disposal of the euro zone members. That card is called devaluation. Whether by design or otherwise, the UK has received a massive boost to its competitiveness in recent months as a result of the sharp fall in the value of the pound. Italy used to play this card repeatedly back in the days of the Lira. So did countries like Denmark in the dark days of the 1970s.

Back in those days there was less economic integration and recessions were rarely global. Devaluations could therefore be used to stimulate exports. The situation today is fundamentally different. The global nature of the current crisis makes it far more difficult for any country to grow its way out through higher exports. The UK will offer a great case study to test whether devaluations are still a powerful tool.

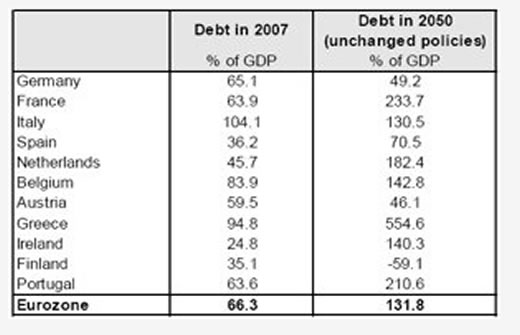

Another issue, which is potentially even more destabilising for the euro longer term, is the massive liabilities facing Europe as its population ages. We have borrowed table 2 below from Goldman Sachs which makes no secret of the challenges facing a number of European countries. Greece is clearly facing the biggest challenge. Public debt, which currently stands at about 95% of GDP, will grow to a whopping 555% of GDP by 2050 if the current pension and social security programme is left unchanged. The Greek government is painfully aware of this and have been working on several new initiatives. It was the passing of one of those new laws which caused the riots in Athens before Christmas.

Table 2: Actual Debt & Age Related Contingent Liabilities

Source: Goldman Sachs, European Weekly, 22/01/2009

Considering the poor record of fiscal discipline, many euro zone members will probably allow their debt to grow much larger before decisive action is taken. The problems are so massive – and the solutions so painful - that most politicians chicken out and pass the problem to the next generation of politicians.

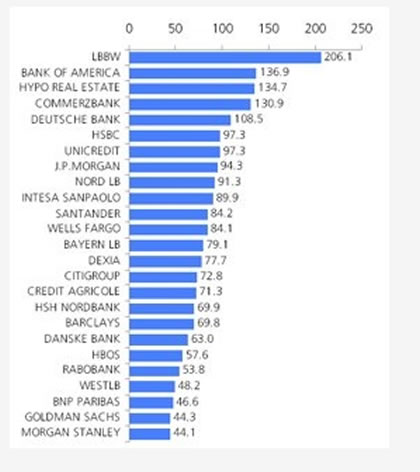

A third problem facing Europe is the sheer scale of the banking crisis. Although this is not just a European problem, European countries are probably worse off than the US because a larger part of European debt has to be financed externally. As you can see from chart 1, more than $2 trillion of European and U.S. bank debt needs to be re-financed before the end of next year. Unless there is a material improvement in market conditions, re-financing at such a massive scale is simply not doable.

Chart 1: Maturing Bank Securities in 2009/10 (USD)

Source: UBS

The European approach, at least until now, has been to save the banking system at any cost. It is therefore possible that a significant share of the re-financing cost will find its way to the sovereign balance sheets and hence ultimately to the tax payer. This could further destabilise the currency union.

All these challenges are surfacing as the global economy faces the worst year since World War II. I have noted that most economic forecasters are still quite sanguine about the prospects for 2010. Be careful. The models upon which these forecasts are built are based on experience from prior recessions; however, this is no ordinary recession and historical data is therefore largely irrelevant. I am becoming increasingly convinced that most of us are underestimating how long it will take to get the global economy firmly back on its feet again.

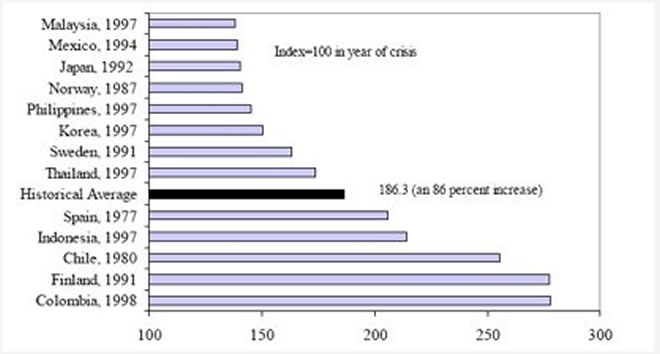

Kenneth Rogoff and Carmen Reinhart published a research paper about a month ago which should be mandatory reading for all investors2. They have studied every single banking crisis of the past 100 years and reach some rather unsettling conclusions. As they point out: "Broadly speaking, financial crises are protracted affairs".

Following a banking crisis, asset prices fall more and for longer than most investors realise (see charts 2a and 2b). So do output and unemployment. Most importantly, though, the real value of government debt explodes (see chart 2c) but not for the reasons you might think. Yes, the bailout costs are significant, but the main driver of rising government debt is actually the subsequent collapse of tax income.

Chart 2a: Decline in Real House Prices during Banking Crises

Peak to Trough Decline & Duration

Source: See footnote 2.

Chart 2b: Decline in Real Equity Prices during Banking Crises

Peak to Trough Decline & Duration

Source: See footnote 2.

Chart 2c: Cumulative Increase in Real Public Debt

First 3 Years following the Banking Crisis

Source: See footnote 2.

So when we are told that the bailout cost, although large, is still manageable, it is only half the story. The loss of tax revenue is another nail in the coffin and could lead to a dramatic – and unpredicted - rise in public debt. Have you heard any mention of that from your government?

At this point I need to introduce something as alien as the "flow-of-funds accounting identity"3:

Δ(G-T) = Δ(S – I) + ΔNFCI4

I rarely throw formulas at you for the simple reason that it scares many readers away. I urge you to stay with me for a bit longer, though, because this formula is critical in order to understand how the government response to the current crisis is likely to impact interest rates longer term. The equation states that any change in fiscal stimulus (Δ(G-T)) must equal the change in private sector net savings (Δ(S-I)) plus the change in net foreign capital inflows.

Translation: If our government stimulates the economy through public spending, as it is currently doing in spades, we must either save more or we have to rely on foreigners being prepared to invest in our country. There are no exceptions to this rule.

The key question, as our economic adviser Woody Brock points out, is what will cause this equation to hold true? It is quite simple. We will save more if we get paid more to do so (through higher interest rates) or if we are so scared of the future that we stop spending and start investing instead.

Foreign investors are no different. Now, with the trillions of dollars being spent around the world to shore up our financial system, the fear factor alone is not going to be enough. Higher – possibly much higher - interest rates will be required to ensure sufficient savings.

Obviously, there is another option at the government's disposal. The central bank can monetize some or all of the deficit by buying the bonds issued by the government. This line of action will keep Δ(G-T) down; hence the need for increased private savings (and/or capital inflows) drops accordingly. The problem with this approach, as an old Danish saying states, is that it is like wetting your pants to stay warm. Monetization executed on a big scale is highly inflationary in the long run, inevitably driving bond yields higher.

The good news is that we are very unlikely to loose control of inflation in the short run. The economy is simply too weak for that to happen. In Frankfurt, the 'eurocrats' are currently congratulating themselves that they, through strict monetary discipline, killed inflation in the aftermath of last year's explosion in commodity prices. The reality, however, is that the credit crunch killed inflation – they didn't - and Europe is now at a junction where even the smallest policy mistake could be very expensive indeed. In my opinion, the ECB has been way too slow in responding to the current crisis and they must act swiftly and reduce the policy rate to near zero levels in order to avoid a deep recession throughout the euro zone.

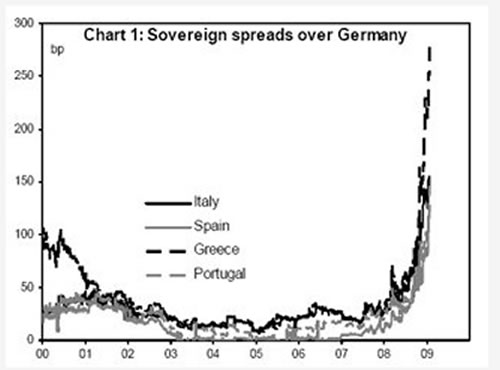

So, could all this lead to the destruction of the euro? Could the currency union actually break up? It is not that the risk to the PIGS has not been recognised by bond investors. As you can see from chart 3 below, investors in long dated Greek government bonds now earn about 2.5% more than they do by investing in correspondent German bunds.

Chart 3: PIGS Sovereign Debt Spreads over Germany

Source: Goldman Sachs, European Weekly, 22/01/2009

On the other hand, I may disappoint one or two readers (I will certainly disappoint Ambrose Evans-Pritchard of the Daily Telegraph who appears to have declared war on the euro), but I firmly believe that the euro will almost certainly survive the current crisis. I am much more worried about some of the member countries.

There is nothing in the Maastricht treaty which prevents a member country from leaving the euro, yet the decision to join is effectively irreversible. There are a number of reasons for this, the most important being economic costs. Take Italy which has a history of compensating for lost competitiveness through regular devaluations. If Berlusconi did the unthinkable tomorrow (sorry – nothing is unthinkable in Berlusconi's world), Italy's borrowing costs would explode. My guess is that bond investors would demand double digit returns on a Lira denominated bond to compensate for the dramatically increased devaluation risk. Already in a precarious fiscal position, Italy could quite simply not afford that.

So, if any country were to leave the euro, it would more likely be from a position of strength, and only one country possesses enough strength to pull that off in the current environment. That country is Germany. And, although the euro is not particularly popular in Germany, I believe it is extremely unlikely for Germany to make such a move unilaterally. There are several reasons for that – Germany's history in Europe being the most important.

At the same time, the fact that the euro has saved the bacon of more than one country in recent months - Ireland being the most obvious example - should not be ignored. For this very reason, the euro membership is actually far more likely to grow than to shrink as a result of the financial and economic crisis engulfing the world. The issue the EU has to deal with is whether the new applicants should actually be welcomed. Most of those who would want to join will bring plenty of baggage.

Another possible outcome, which you hear almost no mention of, is the possibility of a new Transatlantic currency. When I mention this possibility, everyone laughs, but think about it for a second. The economic crisis on both sides of the Atlantic is enormous. Both are resorting to the same formulas – large fiscal stimulus and quantitative easing (a word invented by central bankers because 'printing money' smacks too much of Zimbabwe). There is a real risk that the entire financial and monetary system on either side of the pond needs to be re-designed. If that were to happen, I am pretty confident that the Fed and the ECB would at least sit down and discuss the possibility of a joint currency. That would also allow the UK to join a currency union without too much egg on its battered face.

In the short to medium term, though, there is no such bailout on the horizon. In recent years, the weaker members of the euro, such as Italy, have managed to 'muddle through' (to borrow one of John Mauldin's favourite terms), mostly because the global economy has been strong enough to gloss over any weaknesses. D-day is now firmly on the horizon. As I see things, it is not inconceivable that a member country could be forced to default on its sovereign debt. Interestingly, any euro member country defaulting on its debt could (and probably would) carry on as a full member of the currency union. And I will bet almost anything that the EU would rather have one of its members defaulting on its debt than having to break up the currency union.

Another, and more likely, outcome is the possibility of one or more member countries coming under EU administration. This would almost certainly include the most painful of all cures – mandatory wage reductions in order to get unit labour costs back in line. It would be a lot easier for the government of, say, Greece to get the EU to do the dirty job than to do it itself. Civil unrest will no longer be the privilege of countries such as Indonesia or Thailand. The recent crowd trouble in Greece could very well turn out to be the dry run for much bigger and more organised labour market unrest across Europe as reality begins to bite.

For the time being, though, European governments continue to be in denial. When the IMF recently recommended that Spain implement various structural reforms, the idea was flatly rejected by Prime Minister Zapatero. In the meantime, you can sit back and prepare for the drama to unfold. Very simplistically, it is a choice between Zimbabwe and Japan. Our central bankers can choose to monetize their way out of the current slump and run the risk of much higher interest rates and a rapidly deteriorating currency like Zimbabwe or they can show fiscal discipline and accept perhaps ten years of below par growth a la Japan. Or they can find the delicate balance in between the two and everyone will live happily thereafter. But that requires both skill and luck.

--------------------------------------------------------------------------------

1 The Stability and Growth Pact is the main tool to keep economic policies (and hence performance) broadly synchronized within the euro zone. The pact states that no member country's gross stock of debt must exceed 60% of GDP and that the public deficit in any year must not exceed 3% of GDP. However, the pact allows for these limits to be broken under certain circumstances.

2 "The Aftermath of Financial Crises", Carmen Reinhart and Kenneth Rogoff, December 2008.

3 This part is taken from Woody Brock's latest research paper, SED Profile, February 2009. See www.sed.com.

4 G = government spending, T = tax revenues, S = private sector savings, I = private sector investments and NFCI = net foreign capital inflows.

After I finished writing this month's Absolute Return Letter, I came across an article on Spiegel Online which offers further thoughts on the same subject. You can read the article by clicking on the following link:http://www.spiegel.de/international/..

By John Mauldin

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2008 John Mauldin. All Rights Reserved

John Mauldin is president of Millennium Wave Advisors, LLC, a registered investment advisor. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Investment recommendations may change and readers are urged to check with their investment counselors before making any investment decisions. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staff at Millennium Wave Advisors, LLC may or may not have investments in any funds cited above. Mauldin can be reached at 800-829-7273.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.