The Consequences of Reckless Mortgage Lending

Housing-Market / Subprime Mortgage Risks Jul 08, 2007 - 01:53 PM GMT

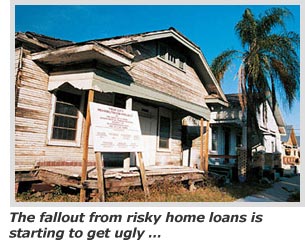

Mike Larson writes : The house down the street with the overgrown lawn and the cracked kitchen window …

The rowhouse stripped of its copper piping and filled with filth …

The cheap listing on your block, the one offered for thousands less than any comparable home …

If you haven't already noticed these in your neighborhood, chances are you soon will. They're the real-world consequences of the spate of reckless lending that took place during the housing bubble. And they're becoming ever more common as the toll of delinquencies, defaults, and foreclosures mounts ever higher.

The Ugly Truth on Loan Performance

The Federal Reserve started raising short-term interest rates in 2004. Longer-term interest rates followed, to a smaller extent, later on.

Now, higher rates should have suppressed demand for houses, cooled the real estate market off, and caused mortgage lenders to tighten their standards.

But the lenders had gotten used to living high on the hog. So, when rates started rising, they didn't pull back. Instead, they offered up plenty of exotic ways for people to get in over their heads. And since homes had become increasingly unaffordable, many borrowers jumped on the bandwagon.

Back in December, I told you about these newfangled mortgages in " The Dangers of Frankenstein Financing ." I specifically cited certain types of Adjustable Rate Mortgages and so-called "stated income" mortgages. And I pointed out that while these products historically had a legitimate use in a few isolated niches of the market, they were now being sold to every Tom, Dick, and Harry as "affordability" products.

Now, we're seeing the consequences of dangerous mortgages and the boom in subprime and high-risk mortgage lending …

- In the first quarter of this year, delinquencies on home equity loans were the highest since the third quarter of 2005. And the late payment rate on revolving home equity lines of credit is the highest since the second quarter of 2003, according to new data out from the American Bankers Association.

- The Mortgage Bankers Association says 0.58% of ALL mortgages entered foreclosure in the first three months of this year. That's the highest level in U.S. history!

- Things are downright awful in the subprime realm. The subprime delinquency rate jumped to 13.77% from 11.5% a year earlier. That's the worst in almost five years — despite the fact the unemployment rate is much lower now (4.5% vs. 5.7%).

And check out what's happening with mortgages made around the time that the bubble started bursting …

A whopping 14.51% of a specific group of subprime mortgages made in the second half of 2006 are already either being paid late, in foreclosure, or in a position where the underlying property has been seized. That's simply amazing considering these loans are less than a year old!

The "vintage" of loans from the first half of 2006 is performing even worse. Almost 18% of them are failing. That's a clear sign to me that lending standards were tossed overboard at precisely the wrong time.

What Kind of Fallout Can You Expect from These Delinquencies and Foreclosures?

As I mentioned at the outset, foreclosed properties are popping up all over the place. They typically aren't as well-maintained as inhabited homes or even "regular" homes for sale. Some have even been stripped of all their fixtures, wiring, and piping.

So, if you're trying to sell your home, a bunch of crummy looking properties in your neighborhood will make your job a lot harder.

To make matters worse, banks and lenders tend to be more aggressive when they price repossessed homes. So if you're competing against a lot of these so-called Real-Estate Owned (REO) homes, you'll have to lower your price to remain competitive.

What about the impact for investors?

Martin already talked about the details of the recent hedge fund blow ups at Bear Stearns, so I won't recap them here. Suffice it to say that the core problem is simple: The underlying loans backing many of these complicated Collateralized Debt Obligations and subprime mortgage bonds are performing terribly.

As long as that's the case, you can expect to see more credit blow ups and more hedge fund losses. That raises the risk of out-of-the-blue market swoons. You may want to take some profits or put on a hedge or two in your portfolio as a result.

Also, if credit performance continues to deteriorate, you could see even bigger losses show up on the books of Wall Street firms and major U.S. banks. Indeed, we're already seeing some banks that went overboard with risky real estate loans get into trouble.

That's one reason why certain stock market sectors, like regional banking, are doing so poorly. The Regional Bank HOLDRs Trust (RKH) , an exchange-traded fund that tracks the banking sector, is DOWN 2.9% so far in 2007 vs. a gain of 8.9% for the Dow Jones Industrial Average.

Bottom line: I would continue to avoid stocks in sectors exposed to the spreading credit woes. That includes mortgage lenders, home builders, and banks with lots of home lending exposure.

Until next time,

By Mike Larson

This investment news is brought to you by Money and Markets . Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com .

Money and Markets Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.